Knowing our shared past helps us to understand the present and envision the future. History provides our sense of community.

From the May 1985 NCUA News, Vol 2, No. 4:

From the recent interview on NCUA’s Video Network, Chairman Callahan praised the NCUA staff, saying, “It’s all working, the team is in place. There is a sense of confidence in the Agency, and it has infected the credit union movement with confidence as well.”

The Chairman is quick to credit examiners and other Agency personnel for the successes during his term: “Most people at NCUA have a good sense of where the Agency is going and how they fit into the picture. People at NCUA get the credit for what we’ve been able to accomplish because they brought us to the point we are now.”

He believes three years of unprecedented growth in shares, loans, capital and membership attest to the positive effects of deregulation and to the success of credit union managers and directors when given the opportunity to make their own business decisions.

As important as deregulation is to Mr. Callahan, increasing the examiner ranks and getting Agency staff out in the field, closer to credit unions is just as important. “Deregulation actually increased our supervisory responsibilities,” he said. “We told credit union officials ‘You run our institutions, and we’ll be there to help.’ It’s a partnership, and it works.”

P.S. See the reference above to NCUA’s Video Network. This interview was the final edition, number XXI. If anyone has this recording in their credit union collection, I would appreciate making a copy.

What does personal service really mean when a credit union has over 63,500 members?

Weokie Credit Union’s Mission Statement is:

Change lives in our community, one person at a time, by being the best place our employees have ever worked and our members have ever banked.

A Nurturing Voice

The CEO, Jeff Carpenter, gave permission to demonstrate how this is done, one member at a time, in this story from his March 2024 report to his team:

“Marlene is an elderly member who has been the victim of several recent frauds. The team got together to determine what WEOKIE might do to help (and not upset the member or violate privacy concerns). We determined that WEOKIE should try to get Marlene to add one of her children to her account, to help monitor the activity.

“It was also decided that Rhonda would make the call and Jeff S. would be there to assist in case things went sideways. Jeff’s take on the call:

“Rhonda reached out to Marlene this morning while Melinda & I listened in the office. She did an EXCELLENT job speaking with Marlene and conveying WEOKIE’s concerns about her account activity and how we can best help her to keep her accounts safe.

“After several minutes and a lot of small talk to gain Marlene’s trust, Rhonda was able to get her to agree to add her daughter added to the account to help with her finances. When I say small talk, it was over 50 minutes of conversation! It was like having a long discssion with a grandparent. You just let the conversation take its own flow and slowly steer it back to the intended purpose. Rhonda did awesome in this aspect. Her Nurturing Voice truly shined in this interaction.

“Rhonda maintained ownership all the way through by following up with Jessica at Main to: provide the details, including Marlene’s vulnerabilities to fraud; the estimated time when the two members might come in; a commitment to follow up when the meeting is set; a request to be notified to facilitate a warm hand-off; an explanation about the Risk department’s approval of the exceptions with a clear understanding of expectations of the member; and how our role impacts the member’s well being.

“This effort involved six employees and shows the role of teamwork, several of our monitoring tools, and our commitment to making this credit union the best place Marlene has ever banked!

“Special thanks to Joseph for sharing this member story and how Rhonda, Diane, Jeff S, Melinda, and Victoria worked together to take great care of Marlene.”

The Takeaway

That’s every credit union’s potential secret power: serving every member, one at a time.

I believe his observations apply to aspects of the cooperative system especially mergers of sound credit unions* now being presented to member-owners.

“First: The free market is a myth.

“The idea that the world would somehow be better off if there were zero rules protecting the masses from predatory investors is not only deluded and insane, but it’s unfathomably dangerous. A rules-free-market is a black market where the worst actors win.

“Capitalism is all about incentives, and investors have twisted the economy to incentivize extraction and exploitation.

“Second: The modern rules-free-market isn’t what the father of capitalism Adam Smith meant when he said “the free market.”

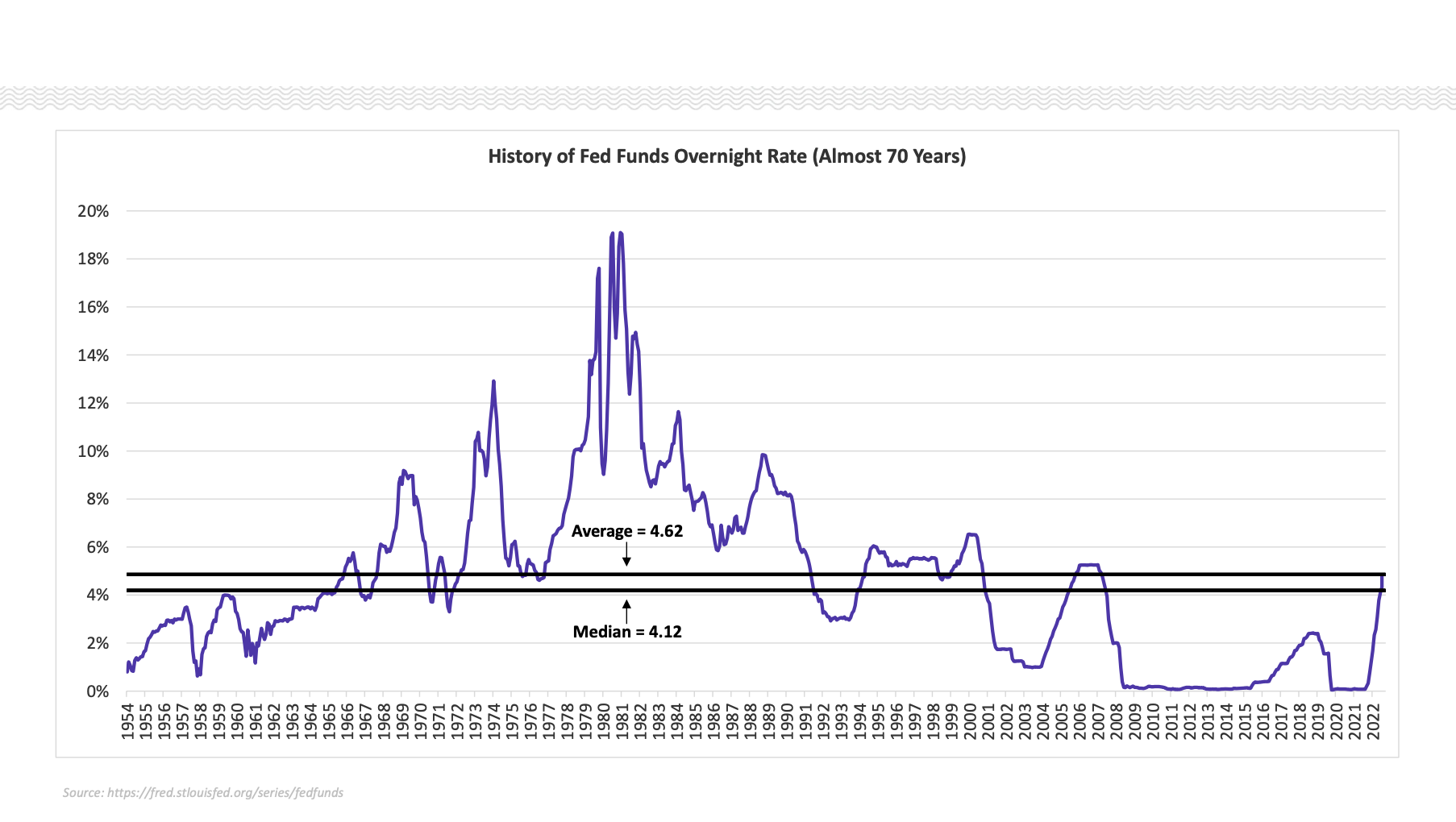

I. The history of the overnight Federal Funds rate from 1954 through 2022 is shown in the chart below. The sixty-eight year average: 4.62%. The latest update for March 2024: 5.33%.

Source: Fred.stlouisfed.org/series/fedfunds

II. Interest payments on US Treasury debt surpasses a trillion dollars in 2023. The total interest paid last year was $1,062 billion.

From the Visual Capitalist article: “The cost of paying for America’s national debt crossed the $1 trillion dollar mark in 2023, driven by high interest rates and a record $34 trillion mountain of debt. . . As debt payments continue to soar, the Congressional Budget Office (CBO) reported that debt servicing costs surpassed defense spending for the first time ever this year.”

Questions: What do these two datapoints suggest about the future level of interest rates?

On February 15, 2024 the NCUSIF Investment committee bought a six year, three month $650 million bond yielding 4.26%. Is NCUA repeating the same IRR mistakes that led to the Fund’s two plus years of current under performance?

Learning to Say Goodbye

A final selection from He Gets Us campaign. The use of stories to communicate values.

Cooperatives are designed around specific organizational principles and values. The phrase people helping people is the classic assertion of the credit union difference. But how can this value distinction, if real, be communicated?

Many organizations face this challenge, especially, those committed to doing “good” in society. Take the example of showing love.

Everyone has a love in their life. In many instances this is another person-spouse, friend or soulmate. In other circumstances it might be a longtime pet. Or a passion so intense that it animates everything a person does-a lifetime committed to living a specific truth.

Imagine Love

The word love is used in many circumstances and about many activities.

How can this concept be communicated in art?

He Gets Us created an AI animated video with the prompt “imagine love”. The result is a series of impressionistic heart shaped valentine-like drawings overlapping the page.

The program’s users then added a series of prompts. These directed that love be shown the way Jesus talked about it-to feed the hungry, help the sick etc. The result is a compelling series of tableaus that show specific scenes any viewer would recognize.

This artificial translation communicates. Some drawings may even inspire. In these visualizations, love becomes an act, not just a feeling.

This brief video’s AI interpretation vividly contrasts the difference between belief and action.

Is It Art?

Are these creations art? Or merely automated serial productions? Do they have meaning?

If this exercise seems too artificial, then ask, how is it you show your love? For that is the question presented.

The AI exercise illustrates the difference between what we say and what we do.

This is a challenge all face daily, especially when leading values-based organizations.

Leaders in families, in organizations, or in life’s many daily roles know the difference illustrated in the video. For credit unions that is when people helping people is more than a slogan. It becomes the animating spirit motivating interactions with members.

The video series He Gets Us relies on multiple methods to communicate a vision of common humanity in an era of cultural turbulence.

It was funded by a group of Christian business leaders who were concerned about the relevance of spiritual values in a time when even religious communities have become part of the current impulse to take sides on every topic.

The videos push against this social divisiveness. Several were among the most watched ads from the last two Super Bowls, an effort that some felt was not the best use of funds.

They are intended to be a conversation starter. To build a bridge to a culture increasingly dubious about the role of spiritual values in contemporary life.

Unconditional Love in the Hardest Times

The group’s longer first-person, authentic life stories are memorable. This five-minute video is an example of a mother and her family’s unconditional love. Most of us have had the good fortune to experience this relationship as either a child or as parents. But perhaps not with the burdens this family encountered.

The video suggests our lives are not just a series of insulated, unrelated events. Human stories reveal deep truths which we may know only in part. They sometimes “speak” to us outside our conscious awareness.

Life Is How We Affect Others

The mother’s story shows a life of purpose a goal for which many aspire. She tells of learning the necessity of humility, “how to set aside everything we know to honor, respect and love another human being.”

In doing so, it suggests all are part of the great human cosmic enterprise. Life comes full circle for everyone. This narrative expresses the belief that we live in a world grounded in shared meaning.

On Monday I introduced the video series, He Gets Us. They were created by a group portraying the relevance of spiritual life today. The work presents pictures of our common humanity.

Works of Art

I believe these videos are works of art. They have the power to evoke an epiphany. We may not know the full wisdom being offered. But one can feel the experience connecting with something inside you.

My hope is to inspire an appraisal of today’s coop messaging. The goal is to move beyond the headlines and priorities of the current moment to rediscover the passions that made the industry a movement.

A Second Language

Today’s selections begin with what seems a simple task, asking nonnative speakers what are most difficult sounds for them to pronounce in English.

But then each person acknowledges the real question is about the words we find the hardest to say emotionally in human interaction. In any language. This short introduction is the source for five longer personal stories from each.

The final speaker is from Finland. The words he found hardest to say emotionally arose in very difficult circumstances.

They were: “I love you.” Saying them makes us vulnerable. A phrase repeated often by rote but still changes lives when stated.

His story sketches the growth in his understanding of this universal expression that enriches all human relationships. It begins with a trigger warning.

Communication transforms when it touches a person’s emotions. It transcends the moment. It becomes art. It helps us see beyond what we knew before.

The most difficult challenge for any organization is telling anyone why they should be interested in joining with you.

Messaging is more than competing for our attention with a product commercial or a clever brand. Ultimately, it must appeal to something inside. It should make us care.

He Gets Usis a video campaign that attempts to represent the “greatest love story ever told.” It suggests the relevance of christen belief in today’s context of religious decline or misuse.

This creative group states its purpose as follows:

We’ve done a lot of homework on our culture. We researched how people feel about each other and what they think about Jesus and Christianity. We’ve connected with thousands of people of various faith traditions and those who claim no religion. We spoke to all kinds of people — different backgrounds, beliefs, and, yes, political affiliations.

And this is what we’ve learned: From politics to sexuality and religion, so many of us feel like our values, beliefs, and identities are under attack by the ideological “others” around us. Many perceive those who differ with them on issues of justice, dignity, and humanity as not just wrong or misguided but also as evil. As enemies. We often see these “others” as close-minded, selfish, hypocritical — and if we’re honest, many of us respond in kind.

This week I will share several of the group’s “presentations” which look and are sometimes presented as commercials. But they are much more. They help us see, to understand more than we did before watching them.

The Credit Union Parallel

What do these “messages” have to do with credit unions? To be seen as relevant in today’s crowded social media is the same challenge credit unions confront. There are a number of organizational parallels.

The participation trend lines in most religious denominations are trending down. Smaller churches are closing. Larger ones are greying. Sunday or Saturday “sabbath” is a time for family errands, fun outings and preparation for the week ahead-not participating in a community of shared purpose. Society’s divisions are mirrored in our religious practice as presented in the group’s purpose:

The more ideologically defensive we become, the more we are willing to sacrifice things like kindness, patience, and the respect and dignity of others for the sake of victory — the righteous ends justifying the dehumanizing means. And it’s tearing us apart. We experience it in politics, in the workplace, in schools, and even in churches. And at the heart of the conflicts is a fundamental disagreement about what it means to be good.

Credit unions and churches no longer seem central to many persons’ lives. Our basic needs and core values, “to be good,” are fulfilled in other ways and commitments.

The He Gets Us videos try to show the relevance of lessons from generations ago for real people today.

My hope is to inspire rethinking for today’s coop messages. We need to move beyond the headlines and priorities of our current moment and rediscover the energy that made the industry a movement, an alternative to the status quo and rediscover who we can aspire to become.

The Immigrants

A hot button topic when people are polled about public issues for political campaigns is the flow of migrates to America.

The one-minute video, Refugee, presents this ongoing human circumstance with a specific context.

(https://hegetsus.com/en/featured-videos/refugee)

What I found equally compelling is the producer’s five-minute story telling how this video was assembled. The making of the Refugee video:

Does this message open one to a different way of seeing this issue? Does it stay with you after viewing? Does this human-centered perspective suggest a parallel in your credit union’s role?

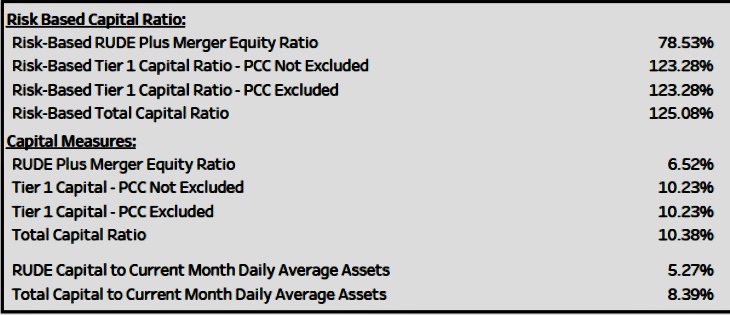

The Good: 125% Risk Based Capital Ratio for a $6.6 Billion Credit Union

If you were ever curious about the difference between a state and federal credit union regulatory environment, the open public meeting of the North Carolina Credit Union Commission the past Tuesday, April 9, is an eye-opener. (It was online).

In 90 minutes a listener received comprehensive, transparent. and timely information from multiple presenters. The topics covered state and national legislative priorities by a League representative and a thorough state-of-the industry review for all 29 state charters (ratios with and without SECU) by the Commissioner. There were updates on the status of the state system: sixteen credit unions have the low income designation and one pending merger.

Administrative briefings on the Commissioner’s office including an examination update (one done, six in process, and 22 to go), examiner training and staff openings.

At the agenda’s completion, the chair solicited comments from the attendees. Credit union members presented concerns about the Administrator’s oversight of SECU bylaw changes. One questioned the Administrator’ support for House Bill 410 to change the operating authority for North Carolina state charters.

The meeting showed the accessibility and transparency of the state’s regulatory environment. All were welcome. It was an open town hall with democratic participation and citizen oversight.

An Up-to-the-Minute Market Update

One of the most interesting reports for me was by Fred Eisel, CEO of Vizo Financial Corporate which serves the Carolina market and credit unions in 40 other states. His information was timely, positive, and specific. Several of his points: liquidity is growing in credit unions with corporate shares up and borrowing by members down. Vizo’s financial results are strong enabling increasing returns for members. Credit union operations are stable.

However, the number that struck me was Vizo’s Risk Based Capital Ratio at March end of 125%–that is not a typo.

Vizo financials through February are posted on their website. It has extensive disclosures of balance sheet and income statement details, shows total available liquidity of $6.5 billion, and includes nine measures of capital adequacy.

Fred sent me the March 2024 numbers showing the 125% RBC ratio.

Vizo’s Multiple Capital Calculations

The NCUA’s RBC requirement for well-capitalized corporates is 10%. Vizo’s ratio is twelve times that standard. Moreover, the corporate’s total capital exceeds 10% of assets.

Vizo CEO’s presentation of March’s final data just seven working days after month end, is extraordinary. It is a disclosure practice documented with web posting, that every credit union might model for their members. The timeliness is a tribute to the credit union’s management. It is also a standard NCUA should emulate in its reporting of the three funds it manages for credit unions.

The Bad:

Coffee hit a 30-month high today. The commodity is up 16% so far this year. One of the reasons is a heat wave in Vietnam.

Cocoahas been soaring due to weather problems in Africa. Cocoa is up 150% so far in 2024. (source: stocks at Night by CNBC Pro April 11, 2024)

The Beautiful: Eclipse Pictures

From my driveway by Luis Escalante who was repaneling my workroom in Bethesda, MD. Luis used my eclipse glasses to cover his camera lens.

From the shores of Lake Ontario by Scott Patterson, CEO Credit Union Student Choice.

His commentary on being in the moment: Clouds didn’t cooperate to see the sun much, but we did get total darkness for a few minutes. Very eerie. The expansive lake view let us watch the darkness line approaching across the water and then see the full daylight on land in the far distance. A thrilling experience.