Last Thursday, January 18, 2024 D. Michael Riley a career credit union professional died. He was 77 years old and is survived by his wife of 41 years, Lori.

After serving in the military, Mike graduated from the University of Alabama joining NCUA as a field examiner in 1972. A little more than 13 years later (May 1985) he succeeded me as Director of the Office of Programs. This responsibility included overseeing the newly capitalized NCUSIF, the CLF and the Agency’s Supervision and Examination programs.

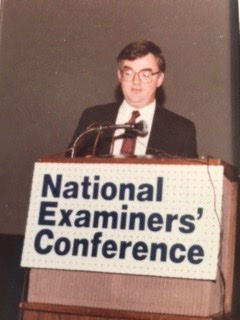

Regional Director Riley speaking at NCUA’s December 1984 National Examiners and Credit Union Conference.

Rising to the Top

His meteoric rise to the highest responsibility in agency reflected his ability to get things done. In 1982 he was reassigned from NCUA’s Central Office to become Director in Region Six-the Western part of the United States.

California was the epicenter of problem credit unions exacerbated by double digit inflation and unemployment and the number and size of credit unions. I believe Mike, at 35, was the youngest examiner ever promoted to RD at NCUA.

Chairman Callahan believed that effective supervision required the leadership of the six RD’s, not rule-making in Washington. They were the critical managers of the agency’s most important responsibility—the examination program. Success was achieved not by cashing out problems with insurance money; but by developing resolution plans unique to each situation and underwritten by cooperative patience.

Regional Directors Allen Carver, Mike Riley, Lyn Skyles and Executive Director Bucky Sebastian at the December 1984 NCUA Conference.

A Passion for the Movement

Mike’s progress from new examiner to RD in a decade is a testament to his grasp of credit union operations. Most importantly he bought into the changes Ed Callahan was seeking. He knew how to get things done, an uncommon trait in a bureaucracy. He had the ability to work with everyone, but was not a “yes” person.

Last July I wrote a brief article about Ed’s time as a football coach and how that influenced his approach to leadership: The Roots and Legacy of a Credit Union Leader.

Mike responded: Great article, I know he taught me a lot.

When Ed left after three years and eight months as NCUA Chair, the small team of five whom he brought from Illinois also left. Senator Roger Jepsen, the next NCUA Chair, did not have a background in either administration or credit unions.

This is when Mike made his most critical contribution. Significant change in a governmental bureaucracy will not last if successors do not believe in the new directions.

It is a bureaucratic reflex that when a Chair leaves, staff reasserts their priorities. This is especially the case when incoming Board members have little or no prior credit union experience. Instead Mike insured the fundamental tenets from the Callahan era of deregulation were sustained.

Hitting the Ground Running

When returning to DC in 1985 as Director of the Office of Programs, he testified with Chairman Callahan on the CLF’s annual budget appropriation within his first 30 days. In September 11 and 12, 1985 he was NCUA’s spokesperson to the House Banking Committee on credit unions’ condition as the new NCUA Chair had yet to take over.

As reported in NCUA News September 1985, he said “federal credit unions had strong gains and a remarkable track record in an increasingly competitive, deregulated environment.” He called the capitalization of the NCUIF, “the most significant development since its founding in 1971. It had quadrupled in size solely through the financial support of insured credit unions.”

In the wake of the Ohio and Maryland S&L crises, he stated NCUA supports the dual chartering system and the option of private insurance for state charters. “This arraignment has served the credit union movement well, providing strength and innovation out of competition.”

For the next ten years (1985-1995) as Director of Programs Mike continued the critical administrative and policy priorities that Callahan had implemented. These included an annual exam cycle, total transparency of performance, expense control. the CLF’s expansion to every credit union and promoting the uniqueness of the credit union system.

In the years he led the Office, failures caused the downfall of the FSLIC and the separate S&L industry, the initial bankruptcy and refunding of the FDIC and ongoing economic cycles. However credit unions and the funds NCUA managed continued their steady progress. Growth in credit union service and members expanded across the country.

Continued Interest in the Movement

In May 2023 post I wrote about the dangerous goal of NCUA’s goal of seeking parity with other regulators. He commented: Outstanding article. Thanks for laying out so clearly. It’s hard to get into the nuts and bolts but somehow NCUA’s operating costs needs to be reduced, fewer administrators and more hands on folks.

He also had a dry sense of humor with an affable southern temperament.

I recall his moderating a GAC panel of two former NCUA Chairs, Ed Callahan and Senator Jepsen. He led a revealing conversation with charm and wit. If someone has a cassette tape of this session, it would be illuminating to hear how Mike navigated the discussion of these two leaders.

People liked Mike. His colleagues were family. Lori and he would hold an open house every Christmas inviting both NCUA and credit union friends.

After leaving NCUA in the mid 1990’s, Mike worked with Callahan and Associates and then on his own as a consultant. He was a Trustee of the TCU mutual funds family.

His Views on Today’s Trends

Mike wrote about current credit union events in this complete post in April 2023. He was concerned about worrisome trends in credit unions leading to their “creative destruction.” He draws from his early years as an examiner overseeing 30-40 credit unions. He closes with this observation on mergers:

This ongoing march continues. The merger of two sound credit unions without some legitimate reason doesn’t seem to be member oriented. I still think of the members of those small credit unions who received services such as buying a washer that no one else would do.

Bigger is not better if the member does not benefit. How many of these mergers produce lower loan rates , higher dividends, or distinctly better products at a lower price? Carried to the extreme we will be left with 20 credit unions that are no different than large banks.

(and on NCUA’s role)

Schumpeter opined “If someone wants to commit suicide, it is a good thing if a doctor is present.”

Memorial Service Details

A service of celebration and resurrection will be held on Saturday, February 10, 2024, at St. Luke’s United Methodist Church (UMC) at 304 South Talbot Street, St. Michaels, MD.

The family will welcome friends and relatives at St. Luke’s UMC from 11:00 AM to 12:00 PM, which will be one hour prior to the service at 12:00 PM.In lieu of flowers, memorial contributions may be made to Habitat for Humanity Choptank, Salvation Army, St. Luke’s UMC, or Talbot Humane.