Memory can be the key to understanding events. It provides vital perspective for the present and context for future plans.

Last Friday October 13th was an important event in NCUA and credit union history from 13 years ago.

It was the anniversary of the payoff of the most recent loan made by the CLF. It may in fact become the last loan the Facility ever extends. Reviewing this event illustrates why this public-private cooperative partnership has failed to play any meaningful role since in the credit union system.

Here are excerpts from NCUA’s Media Advisory of October 13, 2010 with the headline:

NCUA Repays $10 Billion in Corporate Loans

Using proceeds from selling performing assets of two formerly conserved corporate credit unions, the NCUA yesterday repaid $10 billion plus interest to the Department of the Treasury.

NCUA raised the $10 billion by selling select assets from US Central and WesCorp . . .(including) securities backed by performing residential and commercial mortgages, credit card receivables, student loans and auto loans.

The proceeds allowed NCUA to repay a $10 billion loan from the Treasury to NCUA’s Central Liquidity Facility which in 2009 transferred the $10 billion to the NCUSIF in order to lend $5 billion to each corporate. . . while they were in conservatorship.

Paying off the $10 billion in loans clears the balance sheets of both the CLF and the Share Insurance Fund,” said NCUA Charmain Debbie Matz.

The Significance of This Event

Since that October 13the payoff, the CLF has made no loans. Or even offered a lending initiative.

When putting US Central and four other corporates into liquidation in September, NCUA eliminated the joint plan that gave all credit unions access to the Facility.

The Agency had no backup proposal. A brief history of this period and the Agency’s effort to mandate liquidity via regulation versus a shared cooperative option is described here.

The Current Liquidity Borrowings by Credit Unions

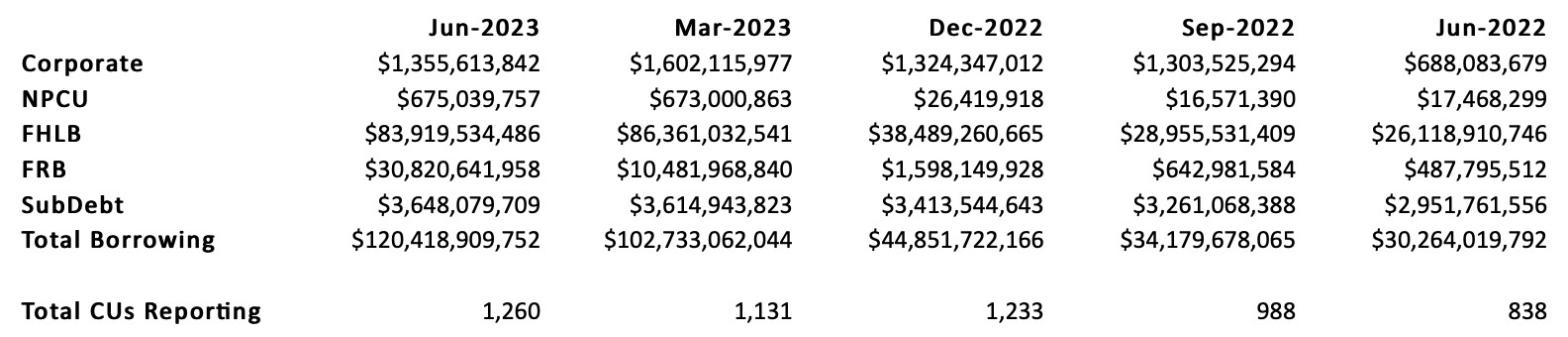

In the first six months of 2023 credit unions increased total borrowings by $75.6 billion to a total of $120.4 billion at June 30. The two major sources for these funds were the FHLB system which increased loans by $46 billion and the Federal Reserve, a $29 billion lending expansion.

Even natural person credit unions increased deposits in other credit unions by $650 million via brokered non-member deposit programs.

The CLF with almost $900 million in capital and $20 billion in borrowing authority is missing in action.

This absence is not because no need exists or a shortage of resources. Rather it is an inability to work cooperatively with credit unions. The Federal Reserve announced its new Bank Term Funding Program on March 12 or in days following the Silicon Valley bank failure.

NCUA does not lack statuary authority as suggested by board members to serve credit unions. It lacks collaborative leadership.

The Lesson from the Last CLF Loan

But credit unions took an important lesson from this CLF loan payoff. The borrowing was designed by NCUA to provide for NCUSIF’s liquidity not the corporate credit union’s well being. Immediately after the two corporates were in liquidation, NCUA sold the best performing assets versus using their earnings to minimize losses to the fund.

The borrowings were to support NCUA’s regulatory priority, not to assist with a corporate’s liquidity management.

When put into liquidation, three of the corporates reported positive capital including US Central, Southwest and United. The CLF was paid off. The Agency funded the subsequent liquidations of all five corporates by going to Wall Street to issue NCUA guaranteed notes to fund the ongoing asset recoveries. These new borrowings were at rates many times higher than the cost of short term deposits and the rate on CLF borrowings.

Credit unions saw that the CLF was not a resource for their use. It was only a means for NCUA to manage the NCUSIF’s cash flows for its obligations to the insured corporates’ members. CLF’s borrowings were not for sustaining the corporates operations. In Matz’s characterization the loan payoffs: “clears the balance sheets of both the CLF and NCUSIF,” but at the expense of the corporate members.

Mandating Membership

In a recent interview before the NAFCU caucus Chair Harper reinforced this view that the CLF is only an NCUA tool, not a shared responsibility. He said staff had been requested to review lowering the current $250 million asset threshold for credit unions required to have a federally backed liquidity source (the Federal Reserve or the CLF). That is to force more credit unions by rule to join the CLF.

When given a choice, credit unions have overwhelming decided to belong to the Federal Reserve rather than the CLF, which has only 390 regular credit union members. The CLF is seen as simply an arm of the regulator, not a resource for credit unions.

As outlined in an earlier analysis, credit unions no longer view the CLF as a reliable partner in times of balance sheet stress

This 13th anniversary of the last loan payment is another milestone. It marks a year of no progress in making the CLF relevant for the credit union system. Rather, it has just become another funding source for growing a bureaucracy with no obvious role.

Editor’s note: Here is how one corporate recommended the CLF be changed in a 2011 comment on NCUA’s proposed liquidity regulation:

Alloya was among approximately 62 organizations commenting on the proposed regulation. The corporate’s comments centered around continuing the CLF, but making it closer in capital structure and operational nature to the Discount Window (immediate availability, little or no capital requirement), maintaining corporates as the agents for the CLF, allowing corporates to borrow from the CLF, CLF Board representation by credit unions and better investment returns on CLF stock through longer term investing.

The majority of credit union and corporate comments were similar and found value in continuing the CLF, but suggested that the structure (either capital or operational or both) be changed to preserve value. Another large portion of the comments were in reference to allowing the FHLB to act as a source of emergency liquidity.

None of these suggestions were adopted in the final rule or in CLF operations.