A June 26, 1984 gathering of “Old Timers:” current NCUA board members, prior Administrators, past General Counsels and senior staff celebrate the 50th anniversary of the passage of the Federal Credit Union Act.

Seated left to right: Deane Gannon, Joe Blomgren, Richard Walch and Bernard Snelick.

Standing left to right: Joe Bellenghi, Austin Montgomery, Fred Hayden, P.A. Mack, Ed Callahan, Elizabeth Burkhart, General Herman Nickerson and John Otsby.

A statement of cooperative enterprise from a church’s bulletin board

LEGACY

All of us are indebted to the past,

to those who precede us.

We drink from wells we have not dug.

We enjoy liberties that we have not won.

We share faith whose foundations we have not laid.

The Creighton FCU insolvency resulted from the sudden discovery of a $13.6 million hole in this reportedly $67 million asset credit union. The failure, NCUA’s largest in 2024, is apparently an unsolvable mystery. One in which the only suspect has died. As I first posted, NCUA has provided not a single fact about where any of the money went. Just speculation.

More incredible is the IG suggestion that there is no money missing, just a bunch of accounting errors. Moreover, no one seems very curious about finding out where money went. In the IG response to the Congressional inquiry he opens with the statement: “my office was not required to perform a material loss review. Additionally, NCUA informed us that the agency was not required to conduct a post-mortem review.” In other words, don’t look for any answers from us.

The one IG explanation is that the CFO, who died in April 2024 leading to the shortfall’s discovery. was covering up actual operating losses for up to 26 years. We’ll examine this idea later. In the IG’s summary review, no one within the credit union or NCUA examiners and external CPA auditors apparently saw any indications of irregularity during three decades.

The IG further assures Congress that an over “20 year review” of the CFO’s family records reveals no unusual credit union cash diversions. Yet this is still the person who carried out this cover up apparently alone, fooling every check and balance and division of duties for such an extended scheme.

Blaming a person no longer around, and who apparently took no funds, feels too convenient. Let’s look at the plausibility of the IG’s theory and facts we do know.

The Cash Came In

We know the members deposited the cash and the funds which went missing. When the $13.6 million shortfall was discovered, this hole was covered by underreporting shares by an almost equal amount. Shares balances in the March 30, 2024 call report were $61 million. Ninety days later the total reported by NCUA in their exam and the June call report was $74 million. This is the exact total change in net worth. And the same order of magnitude ($74 million) for Creighton members’ share liability when merged with Cobalt.

But where did the cash go? Here is the IG’s “official explanation” after reviewing all the information he reviewed:

NCUA officials believe the credit union failed due to bad accounting and financial statement fraud. The large deficit was hidden by the former CFO who exploited Creighton’s weak accounting system that allowed back posting, forward posting, deleting transactions, and hiding general ledger accounts when generating reports. Because no money was found to have left the credit union through this, NCUA officials believe the former CFO committed the fraud not for personal financial gain, but to make the credit union appear to be thriving in the eyes of its Board and membership.

The IG’s “Thriving by Hiding” CFO Motivation

Reread what the IG just asserted. Although we know the $13 million member deposits came in, “no money was found to have left the credit union.” This CFO was cooking the books just to hide operating losses for 26 years. This is what the IG wants us to believe?

Cash shortfalls creating a cumulative deficit can only occur if the credit union pays out that cash in some form (hidden operating expenses, fraudulent loans, fake withdrawals, phoney investments etc) What were those payouts? Some entity or person received these cash diversions hidden by accounting coverups for decades.

A brief IG reference is made to the management of the credit union’s 150 ATM’s for which the accounting was difficult to reconcile. This should have prompted questions such as, what accounts were used to fund the ATM operations? Who managed the cash deliveries and cash drawer balancing when machines were serviced? Was there an external servicing contract or were cu personnel responsible? The IG letter states: Fraud auditors reviewed ATM and lease payment accounting transactions. The regional director stated that the ATM accounting was extremely complicated due to Creighton having over 150 ATMs and the multiple ways in which income and expenses could be divided.”

The IG statement is an NCUA and auditor admission they could not figure out what was going on. Managing 150 cash receiving and paying ATM’s is similar to having to reconcile 150 teller cash drawers periodically. Cash comes from deposits and checks, and cash is with withdrawn by members from their share accounts.

NCUA’s Regional Director is reported to find that “ATM accounting was extremely complicated.” This is what should be expected from covering up a missing $13 million. But not a single instance of imbalance or shortfall is cited. Or even a reference to how the machines were managed.

And the closest we get to the smell of a smoking gun is not from NCUA or outside auditors, but from Cobalt which is quoted in the IG report:

“NCUA officials advised (note the passive voice) that in early October 2024, theylearned from Cobalt that after the merger, Cobalt determined that the former CFO understated expenses related to the ATM network to artificially boost Creighton’s income statement to appear to achieve a steady net income. The IG continues:

“Cobalt surmised that the former CFO was either not booking the monthly ATM expenses at all or was severely understating the expenses. Cobalt indicated the ATM costs alone should have been $255,000 each quarter. They determined the CFO booked around $120,000 per quarter to the office Operations account. Cobalt officials explained to NCUA officials that this would account for an approximate $500,000 to $550,000 reduction in net income per year if no other expenses were booked to the Office Operations account.

Cobalt officials explained that over more than 26 years, such an understatement would easily account for the $12.5 million deficit.”

One can only say Wow! to this explanation from Cobalt. NCUA did not make this finding. ATM expenses are for cash outlays for withdrawals and network operations. The bottom line is that someone or some entity was paid the money. Who wrote and signed the checks for these underreported expenses? The IG report makes it appear it was all just confusing bookkeeping.

Putting the Blame on a Fall Guy

Cash from members shares came in and $13 million cash ended up missing. For 26 years it was all the “fault” of a person no longer living. Which means that all of those who were simultaneously responsible for the safe and sound operation are let off the hook.

Among these listed in the IG letter are the CEO of 32 years, a senior accountant, the board, the supervisory committee, the outside auditor, special auditors and multiple NCUA officials from the supervisory examiner, problem case officers up to the RD’s office.

These were not just persons called in to observe a financial autopsy. They were directly responsible for this institution’s safe and sound operation in their various capacities in the many years before this failure came to light. Yet we read not a word about their roles including the person who oversaw the CFO and his senior accountant staff this entire time.

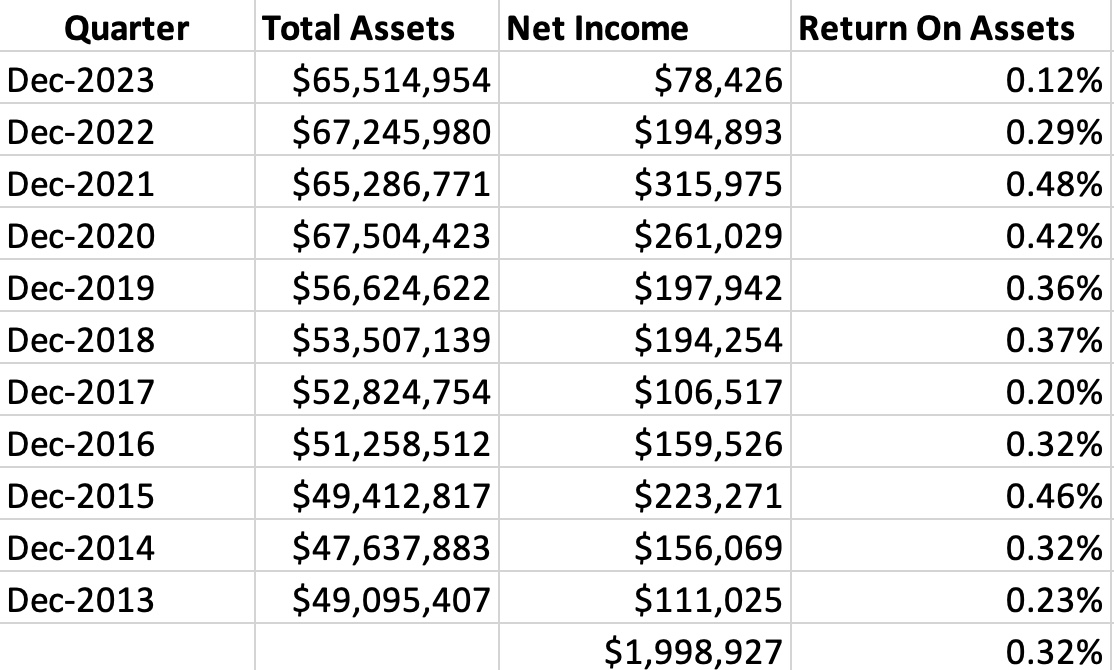

The Reported and Reconstructed Net Income

Here is what we know from the most recent eleven yearend call reports prior to June 2024.

Creighton FCU’s Reported Financial Performance

OK performance, but certainly not world beating. If one believes the IG’s theory, then the real result in this most recent eleven years was an operating loss of $5.5 million from ATM “expenses” plus false net income of $2.0 million. A $7.5 million difference somehow hidden by creative accounting.

However if one presumes a steady cash diversion as the problem, then adding back the estimated $500,000 or more per year means the credit union actually made $7.5 million—most of which was “expensed away.” This earnings would equate to an average ROA of 1.2% or four times the net in the call report. And a reasonable possibility.

The cash from member share growth came in. The cash went out the door as an “operating expense” somehow, somewhere.

A diversion of this magnitude for this long would seem to require several participants. Presumably the ATM’s were not deployed all at once. A system of diverting cash was initially set up and expanded as the network grew. Was some entity or person(s) servicing the machines somehow involved? Other credit union employees had to balance the ATM total cash receipts and disbursements to the general ledger. There had to be a system for quickly producing expense and suspense entries to cover up the missing cash for exams and auditors. No one person could fill all these roles.

Since the share shortfall was quickly found suggesting a second set of books, there is probably a similar recurring system for diverting cash to sustain this activity for decades.

All the people listed in the IG reports were in the room when this happened. But none of them was apparently asked for an explanation of how this could have occurred on their watch. For example how could the CFO have “managed” the expected net income without first talking to the CEO about the results?

After reviewing 20 years of the deceased CEO’s family records, and finding “no improper transfer of credit union funds”, the IG’s simple explanation is that “that the CFO hid this $12 million deficit by exploiting the credit union’s weak accounting system.” But how long had this “weak accounting system” been in place?

The lack of any IG mention of NCUA exam and CPA responsibility for “weak accounting” suggests a reluctance to learn who is accountable for what in this failure. Instead put the blame on the person no longer available, and who took nothing.

Questions the IG should have asked include: What were the examiners’ CAMEL ratings in the most recent years? What did the supervisory committee do? How did examiners record the problems of” back posting, forward posting, deleting transactions, and hiding general ledger accounts” now offered to explain the inability to find the shortfall? Did the CPA firm give a clean audit opinion?

The NCUA and IG’s failure to look at the standard processes for oversight and accountability reflects a flaw in the agency’s own structure. Handing problems over to another credit union to cover up NCUA’s supervisory failures, will only lead to more such failures.

Throwing a Credit Union Under the Bus

Cobalt FCU and their members are taking the hit for Creighton’s financial and supervisory failures. The immediate results of the Creighton merger in the September 2024 quarter include a share inflow of over $73 million; a reduction in undivided earnings of almost $7.0 million (from $115.6 to $106.5–( i.e. Creighton’s negative net worth); and an increase of 6,700 members versus declines in the immediate prior quarters.

Additionally, Cobalt’s net income from ongoing operations reported a $400,000 third quarter loss. The year to date net income is a negative $2.2 million. These combined changes resulted in Cobalt’s net worth falling to 8.1% from 9.2% at the September 2023 quarter end.

A Case Study of Failure-at All Levels

In the IG’s reply to Congress, he states one of the objectives was to report on:

the effectiveness of the National Credit Union Administration’s (NCUA) examination and oversight processes in detecting and preventing financial irregularities, and the role and performance of external auditors in this case. The letter covers none of these issues.

At this time no one yet knows where the missing cash has gone. NCUA has not worked very hard to get critical information on the event. The IG mentions a possible explanation suggesting there is no missing money-just accounting confusion. But the $13 million of member funds is gone.

NCUA seems to have distanced themselves from any further explanations, even citing Cobalt for the latest accounting examples. Yet overseeing the safe and sound operations of credit unions is NCUA’s number one priority. NCUA failed totally and quickly moved on in this case. They have literally closed the books, fended off queries and said there is nothing more to see here.

If this sudden $13 million failure is not a wakeup call, when will the senior leaders of the agency step up to the mike and take responsibility? The NCUA board is responsible for governing the agency, not staff.

The Board’s silence and turning over responses to the IG for a Congressional inquiry for its largest cu failure in 2024 is a leadership failing. The agency’s no comment and the IG’s second and third hand reporting, undermines pubic trust and confidence in NCUA’s administration. Congress, credit unions and the public want to hear from their leaders in a crisis, not the bureaucracy.

Perhaps it is time for a real change at the NCUA board.

The following essay is by Ancin Cooley a credit union consultant, educator and strategic thinker.

As cooperatives enter the new year and new administration, he asks what kind of system will we become: An increasingly capitalistic driven or a member-centric one?

His analysis raises several questions that merit discussion within a credit union and in national forums:

Can credit unions, as capitalist enterprises, solve the problems caused by capitalism?

Who will organize the public dialogue to work through these issues of tactics and motivation?

If Credit Unions Are Leaning More Toward Capitalism, Which Version of Capitalism Is It Going to Be?

by Ancin Cooley

Credit unions once stood for the little guy. They were the warm, flannel blanket in a frigid financial climate: member-owned cooperatives dedicated to local communities, lower fees, and a sense of shared purpose. Lately, though, you’d be forgiven if you can’t spot the difference between your neighborhood credit union and the bank building down the street—right down to the slick marketing campaigns, steel-and-glass lobbies, and ballooning CEO compensation packages. It’s like spotting an old friend who has suddenly switched wardrobes, started drinking designer water, and embraced the virtues of “disruption” at all costs.

What happened to the sense of community?

Many people would argue that good old-fashioned capitalism got in the way. But here’s the key question: If credit unions have indeed started turning into miniature capitalist juggernauts, what version of capitalism are they embracing?

A Quick Tour of “-isms”

First, let’s zoom out for a moment. Think of economic systems like religions. In the United States, you can believe (or not believe) whatever you want, but a majority happen to identify as Christian. Similarly, the U.S. largely identifies as capitalist—again, not by official edict, but by cultural consensus. Communism has typically been deemed the boogeyman in American political discourse, evoking Cold War imagery of red flags and missile crises. Meanwhile, cooporatism—the idea that economic endeavors should be collectively owned and democratically managed—sprouted here as a folksy alternative to big banks and other monopolies, which is precisely how credit unions got their start in the early 1900s.

The Cooperative Spirit That Launched Credit Unions

Credit unions are essentially the love child of cooporatism. They’re not-for-profit, owned by their members, and ideally anchored in local communities. Picture townspeople pooling their money in a local fund, offering small loans to one another, and sharing in the success of their own modest financial institution. The whole idea was to stay small, neighborly, and member-focused—an ethos that resonates with the moral sentiments championed by Adam Smith (yes, that Adam Smith). Contrary to popular belief, the “father of capitalism” had a profound moral philosophy grounded in empathy, virtue, and social well-being. He believed self-interest guided by strong moral grounding could be beneficial for society at large.

Enter the Capitalist Invasion

But as in any good morality tale, the villain (or hero, depending on your perspective) storms in. Over the past few decades, many credit unions began embracing what looks suspiciously like Milton Friedman–style capitalism. Friedman, a famous 20th-century economist, asserted that a company’s sole responsibility was to maximize shareholder profit—no matter what. Translating that to a credit union context, the equivalent might be: “Grow the institution as large as possible, centralize power, and ensure the CEO and board benefit from the increased ‘scale.’”

Mergers, Mergers, Everywhere

We can see evidence of this in the recent wave of credit union mergers. From 2016 to 2021, the number of federally insured credit unions dropped from roughly 5,785 to around 4,900, according to the National Credit Union Administration (NCUA). That’s nearly 900 institutions gone or absorbed in five short years-most financially well capitalized. Sure, there are regulatory pressures, compliance costs, and technology demands that make it hard for smaller institutions to keep up. But it’s also true that once a credit union merges, the resulting entity can boast a bigger balance sheet, which often correlates with a higher profile and executive pay and perks.

Here’s the kicker: When two for-profit companies merge, shareholders typically cash out (or at least receive new stock that might increase in value). In a credit union merger, members get… nothing. No grand payouts, no bonus checks in the mail—just a letter telling them their local branch now has a different name and brand colors, plus perhaps a new CEO and board, not of their choosing. From a purely Milton Friedman perspective—where everything is about maximizing efficiency and returns for those at the top in control—this is entirely logical. From an Adam Smith lens—or even from a Bernard Harcourt–style argument for cooporatism—it’s ethically fishy: you’re sacrificing the well-being of the collective for the ambitions of a few.

Is It Ethical—Or Just Permissible?

But the capitalist incursion doesn’t stop at mergers. Increasingly, we see credit union leadership using member funds to influence lawmakers and regulators, effectively rewriting/interpreting the rules in a way that can benefit top executives over members.

One glaring example is how some CEOs and their associated “leagues” have lobbied for legislation or regulatory policies that dilute or obstruct succession planning rules. You’d think that ensuring a robust and transparent succession process would be an obvious good—central to the continuation of the cooperative charter—yet letters from CEOs to state leagues or directly to the NCUA often argue otherwise.

Why oppose a rule that fosters leadership continuity and protects the membership? Because lacking a formal succession plan effectively empowers incumbent individuals to shape the credit union’s future behind closed doors, sidelining the membership. Worse yet, this lobbying is paid for with member dues. The same phenomenon plays out at the league level, where executive leaders create a “league of leagues” with minimal or zero board director representation—a backroom labyrinth that often makes it easier for a small circle of CEOs and league presidents to dictate priorities.

Is this consistent with fiduciary responsibility and democratic governance? Perhaps not. But as long as it remains legal and permissible within existing frameworks, the line between “member-owned cooperative” and “CEO-centric empire” only gets further distanced.

Another Example: Overdrafts

Let’s give another example: overdrafts. The overdraft conversation, from my perspective, is played out in ways that run counter to the benefit and wishes of the majority of members. Those advocating for overdrafts to be maintained at existing fee levels often don’t dare ask their membership an obvious question—not whether members want overdraft protection at all, but rather what the actual cost should be. Should it be $30? $20? $10? $5?

Instead, the debate is too often framed as a yes-or-no proposition: You either support overdraft fees at whatever rate is charged or you’ll be forced to take a payday loan. That’s an intentional—and frankly misleading—form of argument that aims to scare members into complacency.

Meanwhile, there are far more pressing matters that credit unions could devote their time and resources to—such as the corporate ownership of single-family homes in local communities, which undercuts the credit union’s ability to provide mortgages to ordinary families. But too often, leadership is out of touch, clinging to outdated fee structures or doubling down on rhetorical defenses that only serve to alienate the very members they claim to prioritize.

The CUSO “Merger Exchange”: How Far Have We Fallen?

Now, let’s talk about the creation of a so-called “merger exchange” by a CUSO. Funded by other credit unions, this platform essentially lets CEOs put a credit union on the market—before even bringing the idea to the board or membership. Picture your realtor listing your home for sale without telling you first, then strolling back after the fact to grant you a 90-day comment period. It’s beyond absurd.

It’s also a stark symbol of just how far we’ve drifted from the original cooperative ethos. And the gall of it all—seeing credit union leaders hobnobbing at national conferences, patting themselves on the back while effectively circumventing basic member rights—feels dishonest and untrustworthy.

If we’re willing to normalize this practice, we should at least own up to the fact that the credit union movement is starting to look more like a private club for a handful of insiders than a community-driven, member-owned institution.

A Call to Conversation

As we watch the quiet suffocation of the original cooperative ideal under the weight of ever-larger, CEO-constructed conglomerates, we should ask ourselves: Are we actually okay with this? Credit unions were meant to be an alernative to the profit-at-all-costs and institutional-hubris of the banking establishment. Is it a betrayal of their founding principles to adopt the very model they were created to disrupt, or merely the inevitable seduction of capitalistic motivation and methods?

Why don’t we ever see a CEO get on camera 90 or 100 days before the NCUA deadline and announce, “We’re merging our credit union into another one, and here’s why we’re doing it”? Why isn’t there an open town-hall discussion to engage the membership?

The answer is painfully simple: They do not want to give members the time or the platform to mobilize against a decision they’ve already made. It’s an unscrupulous reprehensible practice, and we all know it—and yet we allow it to happen on our watch.

A Time for Public Discourse

It’s worth having an open, unvarnished dialogue—among credit union members, boards, regulators, and even the broader public—about the future of institutions looking to give up their legacy purpose. Do we want them to remain true cooperatives, a vestige of “caring capitalism” that Adam Smith might actually applaud? Or is the tide so strong that they’re destined to drift ever further toward a Milton Friedman–style corporate destiny?

One thing’s for sure: if credit unions are going to adopt more capitalist practices, they should be upfront about which version of capitalism they’re championing—and what that means for the very members they were created to serve.

Contact Information for Cooley:

Ancin R. Cooley, CIA, CISA. Principal Phone: 224-475-7551 Email: acooley@syncuc.com

Some individuals believe leadership is about the spirit of the poem Invictus:that I am the master of my fate and the captain of my soul.

The majority, I believe, understand our future will more likely be shaped by communities and groups with which we participate, professionally and voluntarily.

The following is a selection of issues that we will encounter in the year at hand. In contrast to the certainty of Invictus, management guru Peter Drucker cautions: “Trying to predict the future is like trying to drive down a country road at night with no lights while looking out the back window. ”

Success May Look Boring

I start with an observation by banking consultant John Maxfield: Banking is a sport of unforced error. The harder one tries the worse one performs.

Tennis.

Ping pong.

Don’t be too ambitious.

Credit Union Leaders Out of Touch?

Outlining vital missions is the job of leadership. But this skill does not necessarily come with those in positions of authority. Consultant Ancin Cooley described one industry challenge:

A core question is about advocacy in our movement: Who are we really advocating for? If we claim to represent the interests of members, why does it so often feel like so much public energy is spent protecting interests that don’t align with members’?

So, should we be out in front of the overdraft fight or supporting legislation that limits corporate ownership of single-family homes? The response you get from some folks is often very telling. I often wonder who is actually making these decisions for the credit union movement because the direction we are going seems out of touch with our members and the communities we serve.

A good example to understand Cooley’s concern is the debate on credit card fees. This article clearly outlines the conflicting positions credit unions must balance for members. One of the author’s observations: “Nobody ever got rich through credit-card rewards, yet lives have been ruined due to credit-card debt.”

Innovative ideas and compliance mandates cannot create the kind of priorities that clearly define credit union’s unique role in the American economy. That can only come from persons who care deeply about their members’ future and financial lives. When leaders combine both mind and heart in their roles, it may be possible for coops to discover possibilities never imagined before,

“From Shakespeare: “The fault, dear Brutus, was not in our stars, but in ourselves.” So it is again. What my generation has done was only human. The self-restraint which, as the Founders realized, was essential to make the American experiment work, had weighed upon too many generations for too long.

“It could not, human nature being what it is, endure indefinitely, and it didn’t. It had indeed gone too far in some ways, and humanity has benefited from loosening some of those restraints.

“Now it will fall to future generations to re-establish some of those restraints and enable us to live together and solve new problems in the large, cooperative communities which their vast numbers now need to survive.”

The Proper Use of Artificial Intelligence (AI)

What if AI is unleashed and never quite controlled — not in the sense of a robotic takeover but, as Harvard law professor Jonathan Zittrain puts it, as a new form of asbestos: dangerous, everywhere and hard to get rid of.

Trump Administration: Uncertainty about Everything

( Analysis from Kellogg Insight, Northwestern University)

Two months have passed since the election and the policy landscape under a second Trump presidency remains as uncertain as ever. We suspect that the Republican-controlled Congress will squeeze some savings out of the budget, but not enough to have a material impact on economic growth

Economists generally view innovation as the main long-term contributor to living standards, as new ideas make people more productive and richer, freeing up time to innovate anew. But there is a second strand of thinking in the economic growth literature, and it holds that political institutions matter most of all.

Peter Thiel famously said, “We were promised flying cars; we got 140 characters.” With crypto we were promised DAOs and smart contracts; we got $100,000 Bitcoin.

Technical progress desperately needs to be matched by social progress that increases trust and delivers better decision-making — from neighborhoods to boardrooms to relations between heads of state.

The Outlook for Interest Rates

How will markets perceive the growing burden of national deficits and debt?

From Bloomberg Forecasts: Hopes that the Federal Reserve would keep up a swift pace of interest-rate cuts have dwindled. That means stocks and US consumers could face mounting pressure, and borrowing costs could remain higher for longer.

An Environmental Change That Aligns with Credit Unions?

In last year’s predictions roundup, I predicted that 2024 would see the housing crisis, and urban policy more generally, become more of a mainstream issue. Of course, that didn’t happen all at once, but I feel pretty good about the trajectory of these issues’ salience.

This year, I’m thinking about a laterally related issue that may have the wind at its back: the question of economic revitalization in small cities and towns.

However much (or little) the incoming administration may do in terms of housing affordability or lifting the fortunes of deindustrialized or “forgotten” places, the hope that they might do something about it was certainly a factor in Donald Trump’s victory. And a lot of small cities and towns are seeing new construction in their old downtowns for the first time in decades.

The eye-watering expense of housing in the biggest metro areas, the rising appreciation for classic urban patterns and the sense that perhaps we owe something to places that have lost out to globalization, may all combine to create a real movement or effort behind bringing back America’s intact but battered small old cities and towns.

Bank of Dave, part 2 was released on Netflix today. In this sequel to Bank of Dave, Dave Fishwick takes on a new and more dangerous adversary: the Payday Lenders. A trailer.

(https://www.youtube.com/watch?v=sled6bgiK78)

Brief Comments on the Week’s Events

From George Bernard Shaw:

On elections: Democracy substitutes election by the incompetent many for appointment by the corrupt few.

On due process: The theory of legal procedure is that if you set two liars to expose one another, the truth will emerge.

The more things a man is ashamed of, the more respectable he is.

On the outlook for 2025 by J. K. Galbraith, Harvard economist: The primary function of economic forecasts is to make astrology look respectable.

The American economy’s challenge: Can capitalism solve the problems created by capitalism?

Mark Twain: “Whenever you find yourself on the side of the majority, it is time to reform (or pause and reflect).”

Yesterday I received the following email signed by Patelco’s CEO Erin Mendez. It read in part:

Dear Charles,

As part of a member-owned credit union, you benefit from our commitment to your financial wellness. Our volunteer Board of Directors helps guide the credit union – and you can allow them to vote on your behalf, making decisions to benefit you. Our Board of Directors and senior leadership work together to guide Patelco and provide the best service and benefits for you.

To help things run smoothly, we use proxies, which give authority for the Board to represent your interests when they vote. (A proxy is a person you designate to vote for you at meetings. By designating a proxy, you allow that person – in this case, a qualified member of our Board of Directors – to cast votes on your behalf.)

Update Your Proxy Today

Clicking the update proxy link brings the following instructions:

Updating your proxy only takes a few seconds and remains in effect for three years. By updating, you will:

Have your vote represented with no need to attend meetings

Provide authority to our member-centric Board of Directors

Allow qualified business people to look out for your financial interests, and those of all members

Your current proxy expiration date is 10/11/2023

My Concern with This Request

The email was sent from a no-reply@email.patelco address. This is a one-way message and recipients could not respond to the CEO’s signed request. Therefore I am taking this public route to voice my concerns about members transferring their basic franchise responsibility to incumbent directors.

Proxy voting is prohibited for federal credit unions. It eliminates the concept of the member-owners democratically (one-member, one-vote) electing their representatives. While a small number of states, like California, permit proxy voting in board elections, these statutes were passed before the 1934 Federal Credit union Act was in place. These initial coop governance models were lifted from existing mutual savings statutes that permitted proxies.

Proxies give existing leadership who already control the nomination process and the candidates selected, absolute control over director choice. Instead of empowering members, proxies further entrench existing directors. The process removes member-owners from any meaningful role in choosing their leaders. The unique democratic design of credit unions is rendered meaningless. Proxies shield directors from accountability to the coop’s owners via elections.

The Opportunity of the Annual Member Meeting

The annual meeting should be a celebration of member-ownership and institutional progress. Owner participation should be encouraged. Member voting is one of the ways this engagement is meaningful, not just a coronation. The second largest credit union in the country SECU NC has demonstrated that individual member voting is feasible in even in the largest coops.

Voting is a fundamental right of ownership. Credit unions should be leading examples of democratic governance. As the general public feels increasingly distrustful of elections and democratic processes for public institutions, credit unions should be an example of how this form of governance works. It can function well even when it comes to the management of their most critical matters of personal finance.

In the last several years Patelco has expanded aspects of its annual meeting agenda to encourage member engagement. Last year there was an extended Q&A with the Chair and staff responding to pre-submitted questions. The prior year CEO Mendez prepared a lengthy live presentation distinguishing Patelco’s liquidity and funding strategies from the recent Silicon Valley and other bank failures.

In 2024 Patelco suffered a major cyber attack. Some member services were limited for weeks. Much time and resources were required to stabilize the situation. Direct, open conversations with members at the Annual Meeting about this and other performance challenges are a way of sustaining member-owner confidence.

More importantly member enthusiasm for their coop is enhanced if the meeting includes both business and celebratory events. This gives directors the chance to connect with and be seen by members—not just spectators watching scripted formalities by the Chair presiding over a required agenda.

An Alternative Communication Approach

Rather than requesting members hand over their most important ownership role to the existing board, why not instead survey members about their experiences at the credit union? Give them the opportunity to become involved, to raise their issues (e.g.why is my HSA account dividend only .25%) and to encourage thoughtful engagement and attendance at the meeting.

A brief survey would show respect for members’ opinions, create interest in the upcoming meeting, and promote the cooperative difference of member-ownership.

The credit union advantage is the capacity to create long standing member ties. Credit unions should welcome participation. It would educate the owners about the credit union’s performance and their critical role in its success.

In brief: Drop the proxy solicitation. Seek member input. Demonstrate the credit union democratic governance model in action.

A closing suggestion: Please include your direct contact information in these kinds of member communications to show your openness to hearing our point of view to your message.

The TV story told of the $13.6 million dollar loss at Creighton FCU leading to its subsequent merger with Cobalt FCU in August 2024. Cobalt said this was the result of the “CEO’s retirement.” Both Peter Strozniak’s Credit Union Times article and I had written about this forced merger and the loss in its final June 2024 quarter of operations.

The merger was caused by an enormous deficit equal to 20% of assets uncovered following the CFO’s death in April. NCUA gave no explanation of what happened, where the money went or who was responsible for the follow-up. NCUA and Cobalt refused to answer any questions about the event. Problem resolved, no questions please.

But the TV news triggered immediate additional facts that NCUA has refused to provide the press and public about its actions. The TV reporter received a letter NCUA’s Inspector General (IG) sent to Omaha Congressman Mike Flood responding to his inquiry about the circumstances of the loss in November.

The IG response is linked here. The letter opens with an unusual disclaimer of direct responsibility as the IG and NCUA are not required to investigate this situation any further:

Because there was no loss to the Share Insurance Fund, my office was not required to perform a material loss review. Additionally, NCUA informed us that the agency was not required to conduct a post-mortem review for the same reason.

But the IG then proceeds to state facts from the public 5300 call report and details of all the external resources and NCUA officials who became involved when the CFO died in April. Those listed include a local CPA firm, the NCUA’s supervisory examiner, the regional director, associate regional director, the director of special actions and a problem case officer. NCUA requested the credit union hire a bond attorney, fraud auditor and an interim CFO to work with its problem case officer. On May 3 the case was transferred to the Western Region’s Special Case office on May 3.

The only NCUA offices not listed are those ultimately responsible for the oversight of NCUA’s federal credit unions: the Executive Director, the Director of Examination and Insurance and the NCUA board. By omitting any mention of their role, they are apparently excused from any accountability.

In October 2024 Cobalt reported to NCUA that the “former CFO understated expenses related to the ATM network to artificially boost Creighton’s income statement to appear to achieve a steady net income.” The IG’s explanation also includes this assertion of agency’s due diligence:

When reviewing the deceased CFO’s family financial records and computers that:The regional director also said the fraud auditors looked for all ways cash could have left the credit union and found no instances of cash removal.

The IG’s concluding paragraph provide NCUA’s theory of the case:

In summary, NCUA officials believe the credit union failed due to bad accounting and financial statement fraud. The large deficit was hidden by the former CFO who exploited Creighton’s weak accounting system that allowed back posting, forward posting, deleting transactions, and hiding general ledger accounts when generating reports. Because no money was found to have left the credit union through this, NCUA officials believe the former CFO committed the fraud not for personal financial gain, but to make the credit union appear to be thriving in the eyes of its Board and membership.

The IG’s Theory of the Case

Several observations from the IG’s summary. First all the information is second and third hand. The IG did not complete any direct review, but solely reported what others have said and done.

If this preliminary description is accurate, one has to believe this accounting coverup occurred over at least 26 years with an average operating shortfall of $500,000 per year between reported and actual net income.

To accomplish this alleged coverup, the CFO would have to keep two complete sets of books. As the deficits were recorded from share balances this would require hundreds of individual entries each quarter to balance out the shortfall but keep member statements accurate. Then these two sets of books would need to be updated quickly whenever external NCUA examiners and auditors arrived on site. Or whenever there was any external loan and share verifications.

A person capable of this legerdemain bookkeeping effort for over 26 years was however not capable of managing the credit union’s financial performance with positive net income?

There is no explanation of how such a consequential scheme could have gone undetected from annual CPA audits, NCUA examinations. supervisory committee share and loan verifications and traditional separation of duties in the accounting shop. It was not discovered until the CFO’s death in April. New people quickly found the out of balance situation and the $13 million shortfall. The fact that the share shortfalls were recovered so rapidly and then transferred in full to Cobalt, suggests these two sets were readily available. An internal defalcation involving member share balances over three decades would normally be an auditing and forensic nightmare to reconstruct. But in this case resolved quickly.

Just Country Bumkins Fooling Experts

Finally, it strains credulity to believe there was no shortfall of funds. The cash had been received from the incoming share deposits. But the IG’s letter presents the assumption that the CFO just used “suspense accounts” to cover unrecorded continuing operating losses—that would average at least $500,000 per year. Why would a person go to this much trouble to just cover operating losses for which he was not directly responsible? If in fact it was failure to balance out ATM deposits and withdrawals—one suggestion—how could such a continuing imbalance go unnoticed for over three decades?

The IG report describes the accounting coverup: Specifically, the CFO had understated expenses related to the credit union’s ATM network to artificially boost Creighton’s income statement. And, The regional director stated that the ATM accounting was extremely complicated due to Creighton having over 150 ATMs and the multiple ways in which income and expenses could be divided.

A credit union of this asset and member size managing a 150 ATM network seems highly unusual. What happened to this system after the merger? Why were examiners and auditors unable to balance out this system for decades?

Assuming the CFO’s only rationale was to hide a continuing operating loss and that he received no benefit from his actions, one must ask who also might benefit from such a coverup? Who supervised the CFO? Is this just a situation of two country bumkins fooling all exam and auditing experts for decades?

NCUA’s Silence on This Failure

Until the IG’s December response to Congressman Flood’s inquiry, all responsible parties have said nothing about the situation. Press queries are referred to call reports and to Cobalt’s press release saying the merger was due to the CEO’s retirement, a completely false account. Why would the NCUA and Cobalt put out such a blatantly false and easily contradicted explanation? Was it to avoid addressing the $7 million or greater shortfall that Cobalt members will now cover?

One fact is clear, everyone, including the IG is distancing themselves from any responsibility for getting to the bottom of this $13 million loss. The IG presents second hand information and lists multiple NCUA involvements with everyone handing off the ball to someone else-either internally or externally. Cobalt does the cleanup. The IG quotes Cobalt’s theory of the loss from October, not NCUA findings, for the missing funds. The IG washes his hand because no “material loss” review is required, but he will consider adding a review to his 2025 “to-do” list.

When people in positions of responsibility have nothing to hide, they will speak up with their understanding of events and what more needs to be done. In this case there is silence for all parties, but most especially the highest levels of NCUA. The initial explanation of multiple decades of accounting coverups creating a $13 million shortfall seems unlikely and inconsistent with some of the data reported. It feels like there must be more to the story.

The True Shortcomings

NCUA’s lack of public candor is the real problem. No one at NCUA wants to take responsibility for the agency’s most fundamental role of overseeing a credit union’s safe and sound operation. Noticeably absent from IG’s account is the role of the three-member board, the information they received and the actions they did, or did not, take.

Did the Board approve the forced merger without member vote? If so, what was in the Board Action Memorandum about the situation and alternatives? Why was Cobalt FCU willing to absorb this accounting and operational mess with a $7.0 million loss which their members must now cover? Where is their upside, if any?

Why weren’t the previous NCUA annual (?) exam papers reviewed for how so-called unrecorded expenses could be disguised in other accounts (suspense and office expenses)? The three quarterly call reports clearly show the credit union reporting positive net income, but no increase in net worth until the yearend. Don’t examiners first review the accuracy of call reports as one of their first verifications? Etc. etc.

The Largest Credit Union Failure in 2024

The Creighton case is an example of institutional failures. The most serious is not the $13 million unexplained loss shutting down a federal credit union. But the total lack of responsiveness to the members and the public by NCUA’s leadership. In a crisis, leadership should come from the NCUA board members, not the professional staff. They are merely foot soldiers. The leaders are missing in action.

Is the best explanation NCUA can provide Congress and the public an IG summary of second-hand agency actions, a listing of all the professional resources sent and offering a third party’s partial explanations of what may have happened?

The buck should stop at the Board’s three desks. The board members are nowhere to be found or heard on the most significant failure in 2024. A long standing, apparently successful federal credit union collapses overnight and costs its members their institution and $13 million in combined resources.

More Precious than Dollars: Trust and Confidence

The NCUA board member’s inaction and silence when facing real problems in an open, prompt and responsible manner is a failure of leadership. Hiding from issues and accountability leads to internal coverups. It creates a lack of public confidence in the agency’s oversight. The perception that board members are not up to the agency’s most basic responsibility raises questions about their competency supervising other areas of credit union activity in which members good faith and trust (e.g.merger payouts) are routinely compromised.

After the TV investigation was reported on Monday, I received the following from a former Creighton member. It read :

Hi Chip – I ran across your coverage (in November) of Creighton Federal’s large shortfall. I am a customer there and had followed their directives to switch to Cobalt. Now I’m wondering if my money is safe at Cobalt! I liked some of Cobalt’s products (a money market savings account with high interest, for instance) and have been happy with their service so far. Still, your coverage of the slap-dash management at Creighton Federal, and its rescue by Cobalt has me wondering if I should move my money to another credit union in town that doesn’t have any problems (that I know of). Thanks!

Hopefully this case is at its beginning and the three members of Congress on the IG’s response will continue to press for actual facts, updated numbers and direct explanations for what happened. NCUA seems incapable of self-assessments. Credit unions should not expect perfection from their regulator, but they should have honest accountability.

Editorial update at 5:00 PM January 8.

Yesterday the WOWT station published this follow up report incorporating some of the IG’s December letters comments to Representative Hood.

Jimmy Carter’s life is a witness to making a transformative difference in the world by personal example and faith, versus the power of a position. This Thursday, January 9th, his legacy will be honored in a ceremony at Washington National Cathedral.

He has stated that the two great formative experiences of his life were the Great Depression and WW II. Today those events and their lessons seem from another era.

When he first announced his Presidential ambitions in December 1974, a Gallup poll asked voters to rank 31 potential democratic candidates. His name was not on the list. Yet just two years later he won the first primaries in Iowa and New Hampshire defeating nationally known opponents including Senators Scoop Jackson, Ted Kennedy and Robert Byrd.

At the July 1976 convention, he became the democratic presidential nominee.

He was a Southern Baptist who taught a Sunday School class whatever his position—as Governor, as President or as a private citizen. He lived his faith not by telling others what to believe, but by example.

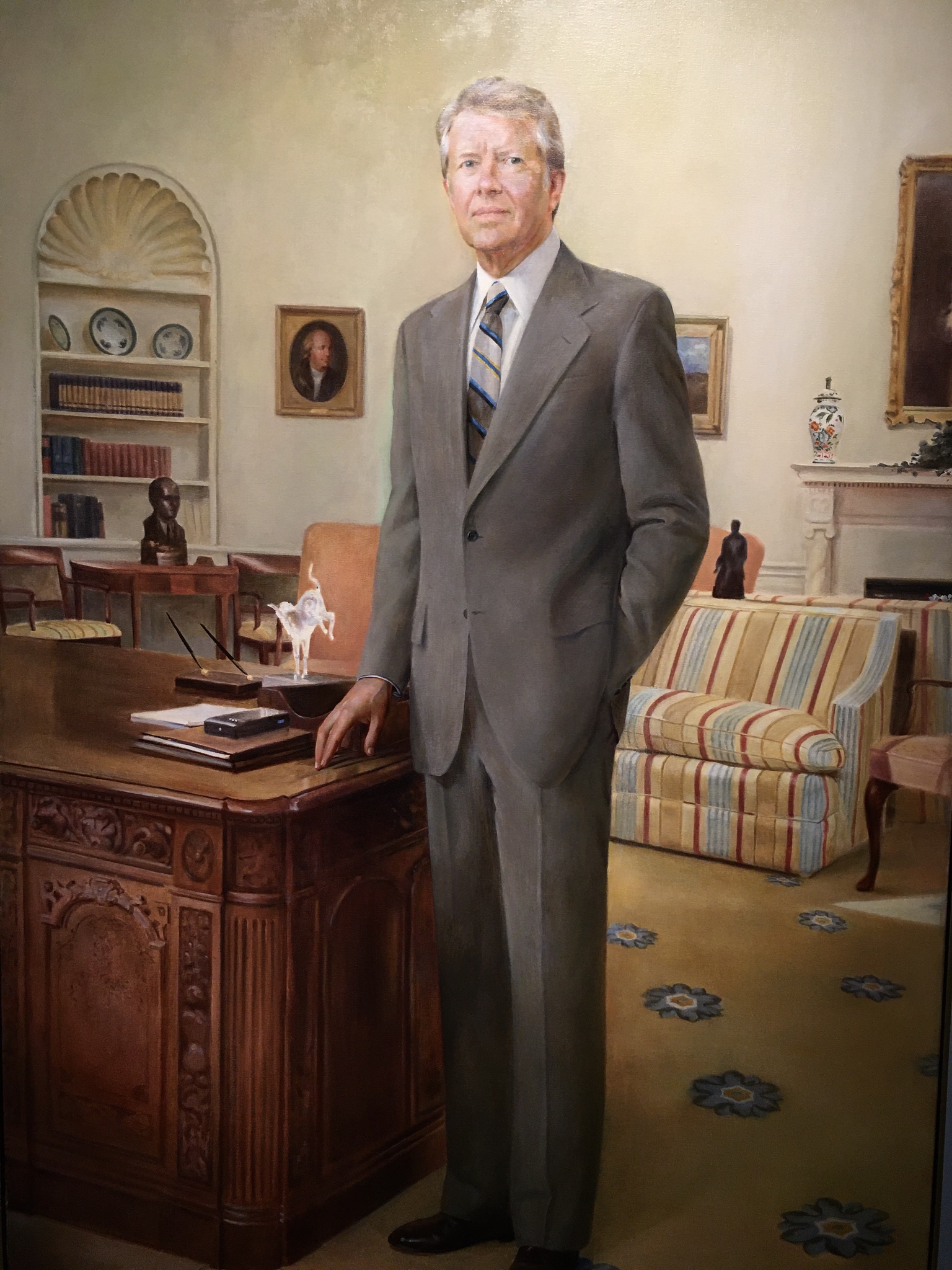

In this official portrait by Robert Templeton (1929-1991), Carter is standing in the oval office as it was during his tenure. On the desk is a crystal donkey statute, a gift from the Democratic National Committee. This oil on canvas 1980 painting is in the National Portrait Gallery.

His Presidency and Credit Unions

Credit unions, as in other segments of the economy, were entering a period of regulatory and market transformation. Carter’s one direct initiative for coops was to ask congress to charter the National Cooperative Bank in 1978. The bank’s purpose was to advocate for America’s cooperatives and their members, with emphasis on serving the needs of communities that are economically challenged.

However, the unique role of credit unions in America’s financial system was not a singular focus.

Rather, changes in the industry during his four years were largely driven by credit union’s specific legislative efforts and external economic events. The destabilization of oil prices led to rising energy costs, increasing inflation and ultimately, the highest interest rates seen in the 20th century. These economic factors helped spark the need and response for the policy of deregulation in multiple sectors of the economy.

NCUA’s Institutional Redesign

Within the federal bureaucracy, Congress re-established the National Credit Union Administration (NCUA) as an independent agency in the executive branch on November 10, 1978 (12 U.S.C. 226).

The NCUA’s Central Liquidity Facility Act (CLF) (12 U.S.C. § 1795) was also created by Congress in 1978. The purpose was to provide credit unions their own source of liquidity similar to the Federal Reserve System’s discount window for banks and the FHLB system for S&L’s.

NCUA’s restructure gave President Carter the opportunity to appoint the three initial board members:

Lawrence Connell, Jr. – The Chairman, had previously been Connecticut Bank Commissioner. He served in the office of the U.S. Comptroller of the Currency (OCC) from 1958 to 1968.

Dr. Harold A. Black – A PhD economist, Dr. Black as a board member brought academic and financial expertise. He helped to integrate his 1962 freshman class at the University of Georgia.

P.A. Mack, Jr. – Served as Vice Chairman. Since 1971 he had been administrative assistant to Indiana Senator Birch Bayh. Mack was reappointed to a second term by President Reagan in 1984.

Connell, center; Black on left; PA Mack on right

This was the administration’s most direct impact on credit unions. It followed the practice that personnel appointments in government are in fact policy. In his Presidential appointments, Carter tried to make the government more representative of the American people. His domestic policy advisor Stuart Eizenstat stated that Carter appointed more women, Black Americans, and Jewish Americans to official positions and judgeships “than all 38 of his predecessors combined.”

In terms of enhanced member services, in 1977 credit unions lobbied Congress to authorize mortgage lending and share certificates for FCU’s, products that had been available in multiple state charters for years.

Economic Forces Precipitate Deregulation

Inflation hit 14% in 1980 and led to ever rising interest rates creating financial crises across major industries dependent on energy and sectors reliant on stable interest rates. These sectors were often subject to government regulations that set consumer prices, or rates paid to savers and charged to borrowers. These regulated industries were often limited in the scope of their services and in turn protected from direct market competitors.

Deregulation of these government-controlled sectors was introduced by the CAB in the airline industry, in long haul trucking, railroads and finally, the national monopoly known as Ma Bell, the AT&T phone company. The Carter administration also deregulated beer production, sparking today’s craft brewing industry.

Financial Services Deregulated

Financial firms reliant on charters and deposit insurance were especially impacted by the sudden and increasingly volatile rise in interest rates. In response, Congress passed the Depository Institutions Deregulation and Monetary Control Act of 1980 (DIDMCA ) signed by President Carter on March 31, 1980. DIDMCA had profound effects on financial institutions, including:

Increased Deposit Insurance: Raised the deposit insurance limit from $40,000 to $100,000 on individual savings accounts.

Authorized Interest-Bearing Transaction Accounts permitting credit unions and savings institutions to offer checking accounts, rather than relying on banks as payable through agents for their “share drafts or NOW accounts.”

Phased Out Interest Rate Ceilings for the banking industry by June of 1987. However, in March 1982 the NCUA board under Chairman Callahan eliminated all constraints on the terms and interest for savings in one regulatory action versus the six-year phased process implemented for S&L’s and banks.

In his signing statement, President Carter made only a brief reference to the bill’s impact on consumers: This is not only a significant step in reducing inflation, but it’s a major victory for savers, and particularly for small savers.

Following the 1980 DIDMCA legislation, NCUA authorized Share Draft Accounts, a service that banks had contested when introduced by state-chartered credit unions earlier in the decade.

A final administrative action triggered by inflation was Executive Order 12201—Credit Control of March 14, 1980. In this order, President Carter granted the Federal Reserve authority to control the growth of credit, including all loans extended by credit unions and other financial intermediaries. The intent was to lower inflation by limiting loan demand growth at the institutional level.

An Agency in Need of Administration

Other than the three NCUA board appointments, President Carter’s administration had little direct comment about the cooperative financial sector.

When Ed Callahan became NCUA Chair in October 1981, the agency was still in a period of reorganization. Agency staff was top heavy in DC with 16 separate offices including a consumer examination program run independently of the six regional offices. There were departments doing tasks and reports the same way as ten years earlier, despite the new challenges of deregulation. Examinations were on a two-year cycle, at best. Semiannual call reports were not collected from all credit unions. The NCUSIF was cash poor and used 208 assistance to help credit unions regain solvency. The CLF had only several of the over 40 corporates as agent members, and only a handful of the almost 16,000 natural person credit unions had joined. There was uncertainty about how the CLF itself would be funded. In brief, the NCUA in 1981 had too much regulation and not enough administration.

Carter’s Legacy

Most of the changes in NCUA structure, the CLF, and even the enhanced mortgage and certificate services were sought by credit unions and underway before Carter took office in January 1977. Credit unions had seen deregulation work at the state level but implementing that policy on a national basis was at best uncertain.

The combination of economic headwinds and changing market competition led CUNA President Jim Williams to say their primary goal was “survival” at the February 1982 GAC conference. In response Chairman Callahan in his first GAC address said the solution was deregulation for credit unions coupled with a simultaneous upgrading of the agency’s supervisory capabilities.

A Leader’s Impact

However Carter’s influence goes far beyond his time as President. While his administrative and policy challenges were not viewed as successful when he left office, his insights and leadership perspective are now being reassessed. For example, his reasons for establishing independent departments for energy and education are now seen as critical to America’s future.

But the most memorable contribution may be his calls to common sense individual accountability. In his 1979 “Crisis of Confidence Speech” he challenged Americans to acknowledge their responsibility for the urgent national economic worries. He said in part:

In a nation that was proud of hard work, strong families, close-knit communities, and our faith in God, too many of us now tend to worship self-indulgence and consumption. Human identity is no longer defined by what one does, but by what one owns. But we’ve discovered that owning things and consuming things does not satisfy our longing for meaning. We’ve learned that piling up material goods cannot fill the emptiness of lives which have no confidence or purpose.

His concern about society’s desire for the bigger, the newest, the “always more” is still a dominant motive today. For a person who grew up on a peanut farm in rural Georgia, lived through the depression, and who left military service to run the farm when his father died, character mattered more than material net worth.

Capitalism promotes and relies on consumer demand. This incessant drive has become endemic in society. When credit union leaders talk about progress in terms of billions, have we lost the cooperative focus on member well-being to the market’s alternative ethos of institutional dominance?

The title of his first book when announcing his intention to run for president was Why Not the Best? It was about renewing the can-do American spirit. The question Carter poses for us is can we invert our thinking about credit unions as successful financial institutions and again see them as a movement by and for the people.

An elegy for Jimmy Carter, Jr.

by Paul Hooker, a retired Presbyterian pastor, presbytery executive, and professor who lives in northeast Georgia

Goodbye, fierce and gentle warrior, farmer with your hands full of good soil. You grew things.

You made your choices for weal and woe, held your power loosely, let it go; asked nothing of others you asked not of yourself.

In extraordinary times, you were an ordinary man — not a hero, not a saint, not a role model. You looked into our eyes and told the truth as best you understood it. We did not listen.

We wanted fairy tales of false greatness, glib promises of never-ending good times, eternal morning in a land immune to night — Lies, all, and so you warned us.

But comforting calumny is easier to hear than stony fact. We turned away to worship at their shiny altars these gods of glory, greed, and gore.

You wavered not an inch from your convictions, smile undimmed by public humiliation; you went back to planting crops in fields where no one else thought they could grow:

Peace in bloodied ground, homes in urban lots, love stretched like a wedding canopy over time and patience and simple faith.

Do not despair. The fields you plowed still wait their harvest. See, even now they bear your quiet fruit.

An unusual approach to assembling a leadership team for a government agency.

Persons interested might review his positions and priorities from a speech on September 9, 2024 to the ACU Congressional Caucus. In the opening paragraph he remarks that his term ends in August 2025 and his search for ideas for his “remaining days:”

Good morning and thank you. This conference is one of my favorites. One reason I’m here is to get ideas on how I should focus the remaining days I have left in this job. Around this time next year, the White House will likely announce a new Board Member. That’s because my term on the NCUA Board ends next August, so I have less than a year left. Whew, I was worried that would be an applause line.

Later he notes his regulatory approach:

in America, you deserve protection from an overbearing government. . .

If NCUA or other agencies ‘get over their skis’ and interfere in the private financial affairs of credit unions and their members, the resulting credit union use of NSF and overdraft services could have the paradoxical effect of limiting access to financial services for those who need it most.

Governments often have coercive powers far beyond any financial institution. . .

I want to mention two fascinating new technologies that we often hear about: Artificial intelligence, and blockchain and digital assets, which includes cryptocurrency. I’ve made clear that the NCUA shouldn’t be a technophobic agency. . .

In reading the full speech, there is no reference to credit unions as cooperatives and any role that design has in his regulatory agenda.