My earlier posts described how NCUA ignored two of the three explicit criteria in the PCA law when imposing RBC/CCULR rules on credit unions.

Before looking at the third constraining feature, “comparability,” there is a procedural violation in NCUA’s actions. The agency’s Federal Registration filing for CCULR and amended RBC was December 23,2021; the act took full effect on January 1, 2022.

The PCA act directs how these changes are to occur:

Adjusting net worth levels -Transition period required

If the Board increases any net worth ratio under this paragraph, the Board shall give insured credit unions a reasonable period of time to meet the increased ratio.

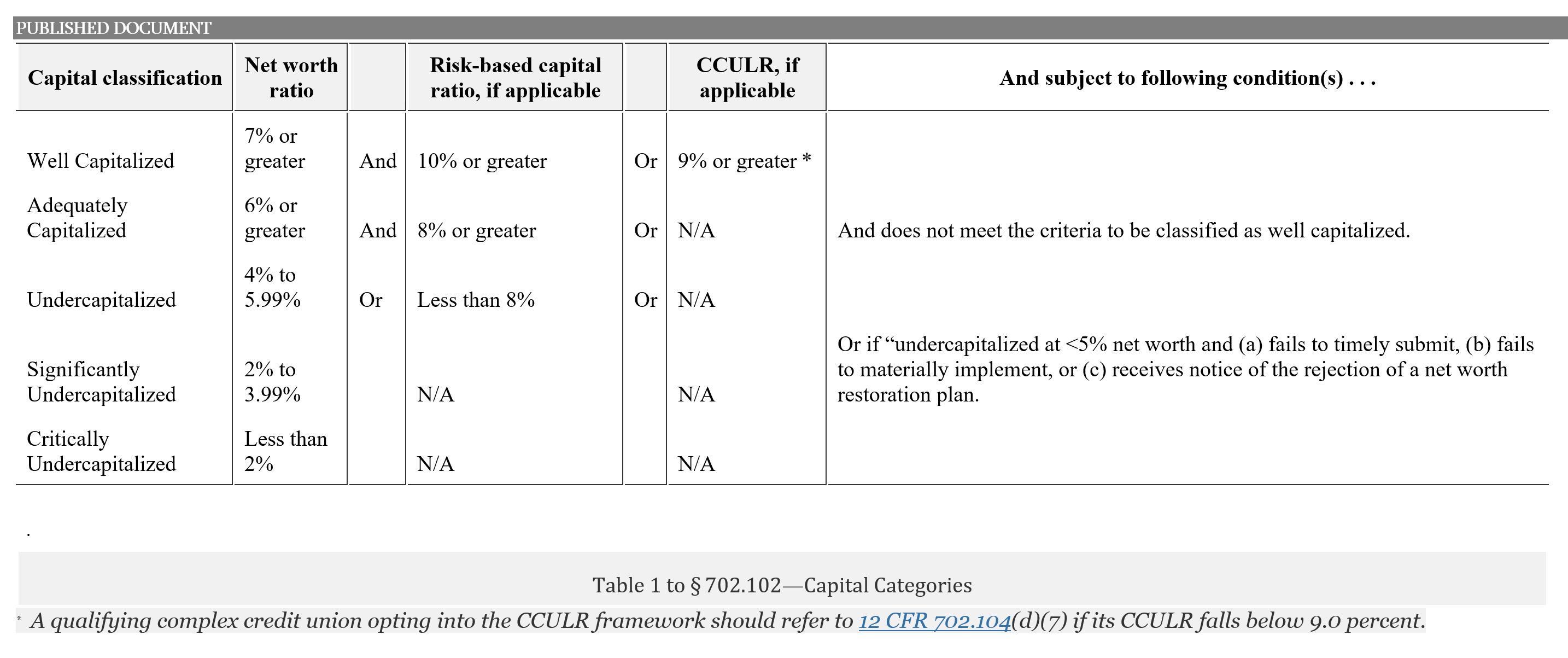

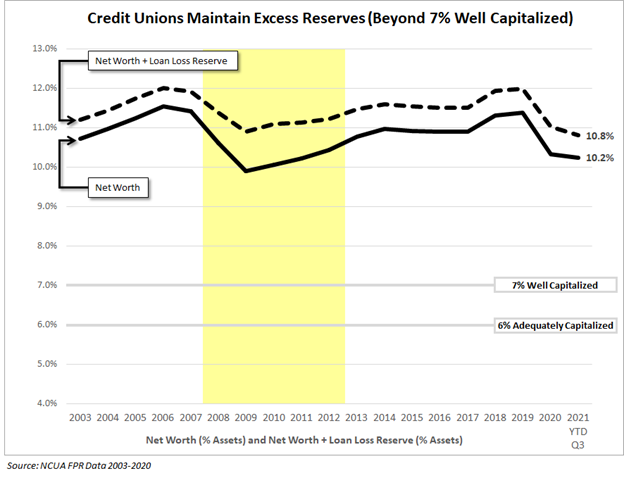

Credit unions were given 9 days to comply with CCULR’s 29% increase (from 7% to 9%) to attain a well-capitalized rating.

The Third Criteria for PCA Implementation

At its core, NCUA has only one explanation for its new RBC/CCULR joint rules:

Harper: The final rule is a balanced approach that gives complex credit unions a risk-based capital framework comparable to those developed by other federal banking agencies.

The combined rules’ minute details and hundreds of risk weightings are explained with multiple variations of one idea: “to ensure comparability with the banking industry.”

Nowhere is comparable defined.

If comparable means “the same as,” credit unions’ 10.6% net worth ratio at December 2021 already exceeds either banks’ core capital leverage ratio of 8.86% or equity capital ratio of 10.06% as reported by FDIC in their September 30 quarterly report.

Must credit unions now reduce their capital level to be comparable to banks’ average?

Obviously not. NCUA’s intent is that credit union net worth be measured with the exact same accounting details as the bank’s follow. Except banks have many more capital options for the numerator.

The rule’s 70+ risk weighting formulas, and multiple variations, applied to credit union assets were lifted directly from the banking model.

The rule duplicates bank regulations at every point even though the asset composition and financial roles of the two systems are drastically different.

This literal interpretation of comparable accomplishes one goal—NCUA now controls credit unions with the same power bank regulators enjoy. This should be no surprise as Chairman Harper has repeatedly praised FDIC bank regulation as the de facto standard he intends for credit unions and the NCUSIF.

This approach was followed ignoring the two system’s different histories, legislative purpose, financial design and most importantly, financial performance.

What did comparable mean when Congress mandated this new cooperative capital standard in 1998?

For 90 years credit union capital adequacy was based on a flow concept, setting aside a required percentage of total income before dividends, rather than a balance sheet, net worth ratio, measured at points in time. This new ratio standard was significantly different from credit unions’ prior practice of building reserves over time as a percentage of total income.

The Act explicitly required NCUA to “design the system, taking into account” the not-for-profit cooperative structure which cannot issue capital stock and relies only on retained earnings for reserves. When requiring a balance sheet ratio test versus a set aside from revenue, NCUA’s process must consider the listed differences in reserve structure and even the board volunteer composition.

The second change under PCA for credit unions is in a different section of the act:

d) Risk based net worth requirement for complex credit unions.

The agency is directed to include ” a risk-based net worth requirement for insured credit unions that are complex.”

Banks have no call out for complex. Risk based weightings are universal for all banks.

The new coop PCA model required a risk-based factor (weighting) for a defined set of complex situations which “take account any material risks against which the net worth ratio . . . may not provide adequate protection.”

These words clearly establish a different PCA model for credit unions than required of banks.

Cooperative PCA standards are clearly intended to be different. To assert that comparable means to duplicate, copy or be the same as banks practice is a misinterpretation of the Act.

Twisting a Law Reducing Burden to Impose a New Regulation

The most recent example of this misinterpretation of NCUA’s authority is Chairman Harper’s description justifying the CCULR option proposed by NCUA in July 2021, five months earlier.

Harper: We must, however, also recognize several legislative, regulatory, and marketplace developments since the NCUA Board approved the final Risk‑Based Capital Rule in 2015. For example, in 2018, Section 2001 of the Economic Growth Regulatory Relief and Consumer Protection Act directed the other federal banking agencies to propose a simplified alternative measure of capital adequacy for certain federally insured banks. The result of that effort became known as the Community Bank Leverage Ratio framework which became effective in January 2020.

There is a supreme irony citing President Trump and the Republican-sponsored Main Street Relief Act, to reduce regulation burden. Then to expand its application to NCUA’s rule making authority over credit unions.

Here is a summary of the reference Harper cited:

Title II Regulatory Relief and Protecting Consumer Access to Credit

Section 201. Capital Simplification for Qualifying Community Banks. This section requires that the Federal banking agencies establish a community bank leverage ratio of tangible equity to average total consolidated assets of not less than eight percent and not more than 10 percent. Banks with less than $10 billion in total consolidated assets who maintain tangible equity in an amount that exceeds the community bank leverage ratio will be deemed to be in compliance with capital and leverage requirements.

There is no mention of NCUA anywhere. NCUA had not even implemented RBC when the bill was signed in May 2018. There was no basis for credit unions to ask for regulatory relief from a rule not in effect and deferred three times at that point.

The congressionally enacted CCULR option was a banking industry effort for an alternative to a flawed and burdensome RBC rule. FDIC’s vice chair Thomas Hoenig had been a long standing vocal critic of RBC.

Further evidence that this section 201 did not include NCUA is that NCUA is specifically named in two other parts of the bill that explicitly provide regulatory relief for credit unions:

Section 212. Budget Transparency for the NCUA. This section requires the National Credit Union Administration to publish and hold a hearing on a draft budget prior to submitting the budget.

Section 105. Credit Union Residential Loans. This section provides that a 1- to 4-family dwelling that is not the primary residence of a member will not be considered a member business loan under the Federal Credit Union Act.

To claim NCUA’s authority for CCULR, Harper refers back to the 1998 PCA bill. He then uses the “comparability” reference to presume authority in a bill passed twenty years later and in a section specifically omitting any reference to NCUA .

The result of this newly found authority is to increase credit unions’ restricted capital. As stated in the Board memo: ”The Board believes that a CCULR of nine percent is appropriate because most complex credit unions would be required to hold more capital under the CCULR framework than under the risk-based capital framework.”

A False Narrative

NCUA was not given CCULR authority. It is a false narrative permeating RBC/CCULR that credit unions’ rules can exactly copy bank rules.

This duplication-interpretation overlooks the two-decade reality that credit unions were fully compliant with their PCA risk based net worth (RBNW) model and repeatedly surpassing banks in financial performance under it.

The staff perpetuates this duplicating justification in its board memo: A special note that most, if not all, of the components of the CCULR are similar to the federal banking agencies’ CBLR.

The Consequences of Unconstrained Regulation

There are immediate and long-term unfortunate consequences when authority is improperly interpreted and asserted. This erroneous RBC/CCULR precedent will undermine the credit union system’s unique role and diversity, directly contrary to PCA’s intent to respect cooperative character.

It sets an example of agency interpretation independent of fact, statutory language and prior compliance precedent.

Board Member Hood pointed out this long-term risk in his December board comments:

We now have (PCA compliance) with our risk-based network requirement. This law gives this board serious responsibilities which we must faithfully uphold, but this does not mean that since the bank regulators established a risk-based capital regime, we must follow them.

I actually worry that once we decree that 7% may no longer be adequately capitalized, then whether it’s this board or a future board that settles on an 8%, 9%, 10% net worth in the complex credit union ratio, as some say in North Carolina, the barn door is now open to that interpretation or that change.

I worry that we may have set an arbitrary standard above the law that a future board can easily change at any time.

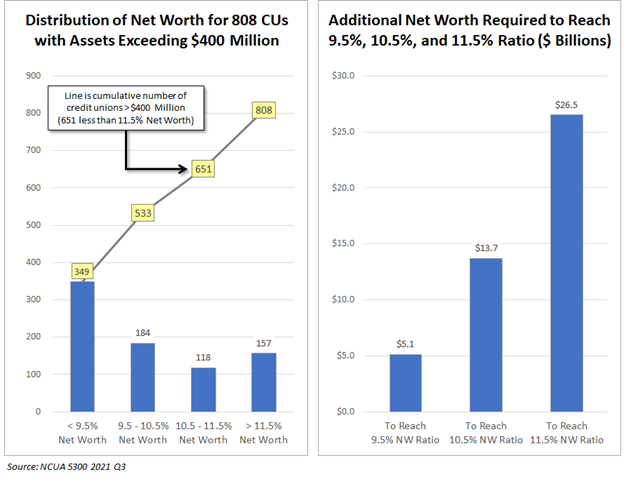

There is much more at stake from RBC/CCULR than approximately $30-40 billion of forced sequestration and newly required credit union capital. And the rule’s faulty legal standing.

The central issue is whether the NCUA board is willing or able to support the continuing evolution of a unique cooperative financial system in its regulatory actions.