On December 23, 2021, NCUA filed a new rule, RBC/CCULR, in the federal register. It took full effect just 9 days later on January 1, 2022. This rule is the most consequential ever passed by NCUA, and the most damaging.

The change immediately affects 83% of 2021 yearend credit union assets.

Using a purported rationale of improving the safety of the system, the rule will result in the opposite outcome. It significantly handicaps the ability of credit unions to make decisions about how best to serve their members using their own experiences and judgments.

This catastrophic new burden will accelerate the merger of sound, well-run credit unions approaching the $500 million starting line for CCULR/RBC. It will energize this culling of hundreds of successful medium-sized local institutions now facing an overnight fundamental change in compliance burden.

The New Year Shock

Credit Union 1, Rantoul, Illinois, wins the award for the first credit union to publish its full 2021 Annual Report including year-end financial data and ratios.

The President’s Report by Todd Gunderson, CEO, contains the following upbeat assessment:

CU 1 loan portfolio growth was 15% as we extended $ 916 million in loans to our members throughout the year—an increase of 43%–and $276 million from the 2020 year. The additional loan interest income helped CU 1 achieve a record net income amount for the 2021 year, bringing net capital rate or our rainy-day fund up to 8.71% of assets. This keeps CU 1 well in excess of what regulators call a well-capitalized credit union, defined as 7% net capital.

CU 1’s total assets had increased to $1.226 billion or by 4.8%. At the same time, it raised its net worth ratio from 8.21% in 2020 to 8.71%.

Chair Bob Eberhert was equally proud of CU 1’s regulatory standing: “. . . our future . . .is about having the trust of membership by being a sound member-oriented financial institution that propels CU 1 to be awarded the highest rating that can be bestowed upon a bank or credit union by banking supervisory regulators.

These statements were accurate for exactly one day, December 31, 2021, when the books were closed.

CU 1 is the first of hundreds of credit unions that entered the New Year believing their past performance was at the highest standard. They will now find they are in a literal regulatory net-worth “no-man’s land” where no coop has ever been.

Enter Three Capital standards

Every credit union over $500 million in assets saw their minimum ratio for “well capitalized” raised from 7% to 9%, a 29% increase, on January 1, 2022.

No phase in, no transitions, no analysis of the consequences, and imposed despite no demonstrated need at the individual credit union or system level by NCUA.

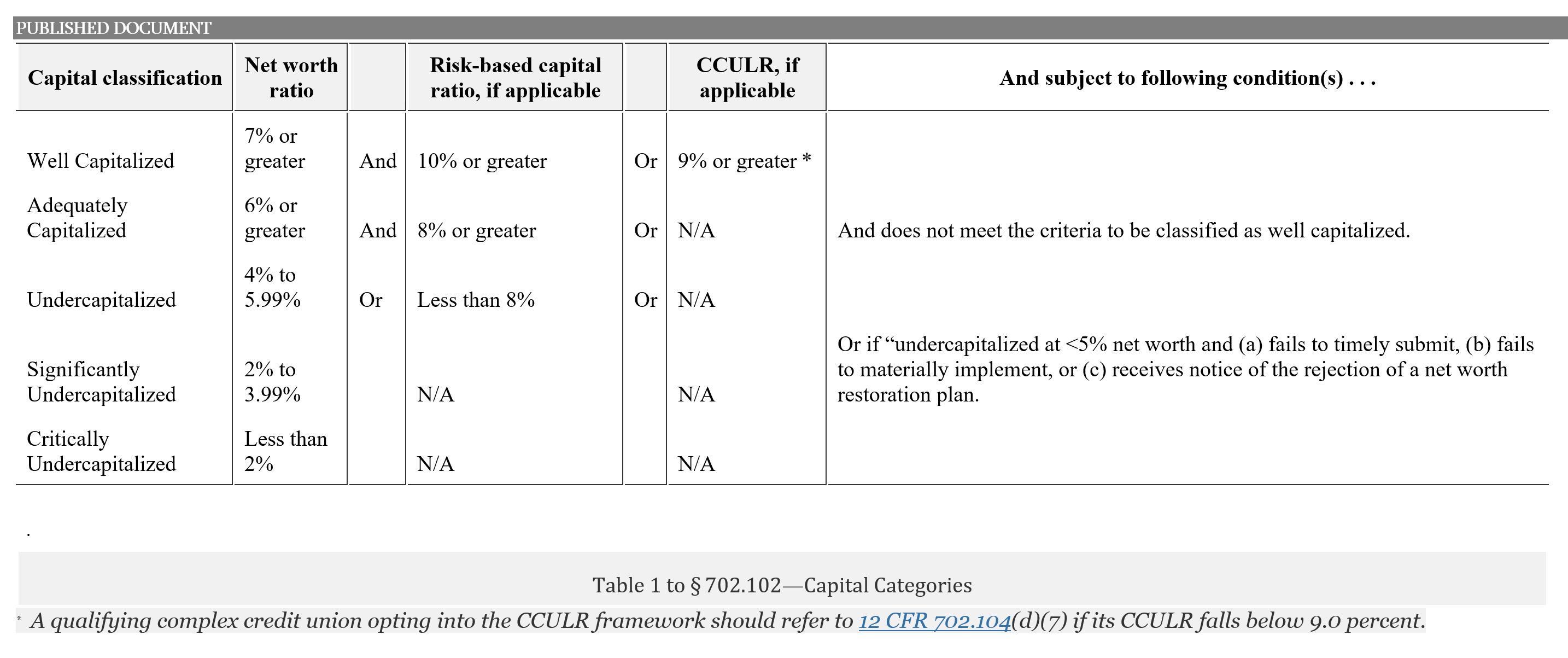

From one simple, easy to compare century-long standard, these institutions are now subject to three interlocking capital requirements. These rules entail multiple options for calculating the numerator for “capital reserves” under the three standards.

The denominator, or “total assets,” now requires hundreds of specific math calculations as well as evaluating alternative methods. These factors include whether the asset is on and off the balance sheet, multiple time periods for determining “average” assets, and every asset’s relative risk calibrated precisely to a government mandated and calibrated formula.

The chart below presents this new tri-part capital era. The system has gone from the left column of clearly understood and applied net worth of 7% with five gradations, to the completely open-ended 500+ page-RBC/CCULR formulas and criteria.

A Direct Member Tax

The rule handicaps credit unions from spending money to lower fees (eg. overdraft charges), offer better savings or loan rates or even initiate critical programs such as cyber security or ESG initiatives.

Instead, this income must now be put into reserves where the amounts already set aside have proven more than sufficient through every previous financial crisis.

Every one of the 100 million plus members in a credit union subject to, or nearing this rule’s reach, will pay the direct costs of this regulatory tax in higher fees, lower savings or higher loan rates.

The members most affected will be those at the margin, with lower credit, just starting out after leaving school, or returning to the labor force; that is those traditionally perceived as higher risk.

Hundreds of Credit Unions Impacted

Hundreds of credit unions like CU 1 now find their “well-capitalized” regulatory standing downgraded overnight. From understanding and complying with a capital standard proven over 100 years, they are immediately thrown into a regulatory purgatory.

RBC/CCULR is a purgatory of changeable definitions and formulas in which every asset decision is now subject to a government-dictated risk rating.

Every credit union over $500 million in assets (83% % of total assets) can now be whipsawed between two different capital standards. NCUA reserved the authority to impose the capital model they want, regardless of the credit union’s choice.

No more respect for credit unions’ four-decade track record of demonstrated risk management honed in the marketplace since deregulation.

These two draconian rules of 500 pages are in effect now. No phase in, no transitions, no analysis of the consequences, and implemented with no reference to the actual capital soundness of the industry.

It is a regulator taking an action because it can. The traditional due processes and institutional checks and balances, at the board level, failed.

Uncertainty About Cooperative Soundness Undermines Public Confidence

The agency gave itself the authority to micro-manage every asset decision made daily by 5,000 credit unions. It is the most extreme example of an independent regulator asserting control over every aspect of a credit union’s operations.

This rule is the worst kind of regulatory putsch possible. It is an assumed authority run amok.

It throws the credit union system into a public relations debacle. For credit union leaders it creates a compliance wonderland of uncertainty about the rules of the game.

Will all CAMEL 1 rated credit unions below 9% now become CAMEL 2?

Will this incentivize the sale of subordinated debt with members paying the added cost of capital to be compliant?

How does anyone– the regulator, the members, the public– compare credit union performance with three very different ways of measuring “well capitalized”?

Will this intrusive regulatory grading of every asset decision override credit unions’ learned experience? And inhibit serving members and making investments required to stay competitive?

In upcoming posts I will show why RBC/CCULR is “the fruit of a poisonous tree.”