From a philosopher:

As a species, we can’t choose whether we worship — it’s built into us. However, we can choose what we worship.

Purpose and worship-two sides of the same coin.

Chip Filson

A segment from the March 14, Marketplace daily report on NPR follows. The interviewer is host Kai Ryssdal and the guest commentator is Daniel Tarullo who teaches at Harvard Law School.

Between 2009 and 2017, Tarullo was on the Federal Reserve Board of Governors; specifically, he served as oversight governor for the supervision and regulation committee.

Silicon Valley Bank (SVB) analysts are looking for situations where there are balance sheet or business model parallels that could lead to more bank failures. Tarullo asserts that management will always be first in line when blame is assessed.

However that is not the full story. He believes the proximate cause is closer to home–a regulator with a light touch.

I believe his last comment highlighted below describes NCUA’s approach to supervision. How else do you explain a credit union CEO and Chair giving themselves a $10 million fund under their sole control or $1.0 million dollar credit union CEO bonus upon merger, among other abuses?

Interview Excerpts:

Ryssdal: All right, so look, that’s why we got you on the phone. You ran, among other things you did at the Fed, the committee on supervision and regulation. And I am not the first person to ask, nor will I be the first person to ask, where were the regulators? Why did this come out of the blue?

Tarullo: That’s a huge question, isn’t it? There are two places to look: One is to supervision and the other is to regulation. Now, of course, we’re stipulating that there’s a management failure, but I think everybody would agree with that. So in terms of the government, the debate publicly has been, “Gee, were the 2018-2019 changes in the [Dodd-Frank] law and Fed regulations respectively to blame?” And, as I think you know, I was opposed to both the [rollback of the] law and the changes in the regulations.

But I don’t think there’s that direct of a connection between those specific changes and Silicon Valley. And so what that tells us is the failure was in the oversight by supervisors — people who were supposed to be watching whether things like the proportion of uninsured deposits was creating some unusual risks for that particular bank.

Ryssdal: That’s not terribly reassuring, I gotta tell you.

Tarullo: No, it’s not. And I think that the review that the Fed has launched — and it’s significant that it’s headed by the vice chair for supervision, Michael Barr, who is, you know, relatively new — I think the significance of having him run that rather than staff is precisely because they want to find out where the supervisory failures lay. Were they with the specific team that had responsibility for Silicon Valley? Or were the failures more widespread in the sense that Washington was providing kind of a light touch supervisory direction to them?

Ryssdal: What do you think?

Tarullo: I suspect that it’s a combination of the two. But given the signals that the Fed was sending, you know, in the last several years, I believe that part of it is just the “don’t be too tight in your supervision, you need to find legal problems before you tell the banks to change what they were doing.”

In talking with a retired CEO who still follows credit union events, I asked how his perspective had changed.

“I don’t feel the intensity or nuances from the grind of the day to day. . . or the tactical lust for short term passions.”

Without an organization’s boundaries, the retiree tends to be more observant of general trends.

An example of this capability is John Tippets, who retired as CEO of American Airlines FCU in the first decade of this century. In retirement he continued to consult in strategic planning sessions and speak at credit union events. During the 2008/9 financial crisis he was the interim CEO for three years at the troubled North Island Credit Union, which he saved from a regulatory closure.

Before his credit union roles John spent about 25 years in the for-profit world of American Airlines. Most of that time he was an Officer with Sky Chefs, an American airport restaurant and concessions, and airline catering, subsidiary.

He has had multiple retirements and career involvements. He and his wife Bonnie have written a book, Hearts of Courage published in 2008, the story of his father’s survival from a plane crash in Alaska in 1943. The story behind the book is in this 2009 article.

There have been two CEO’s since John at the credit union. The airline sponsor has gone through much turmoil including bankruptcy, mergers and leadership changes. The relationship of the credit union and its sponsor has continued strong even through numerous board changes.

The one strategic change John made as CEO was to take advantage of the TIP field of membership option. This permitted the personnel of other employers, co-workers at the airports, to become members of AAFCU. Airports in many ways became the credit union’s communities.

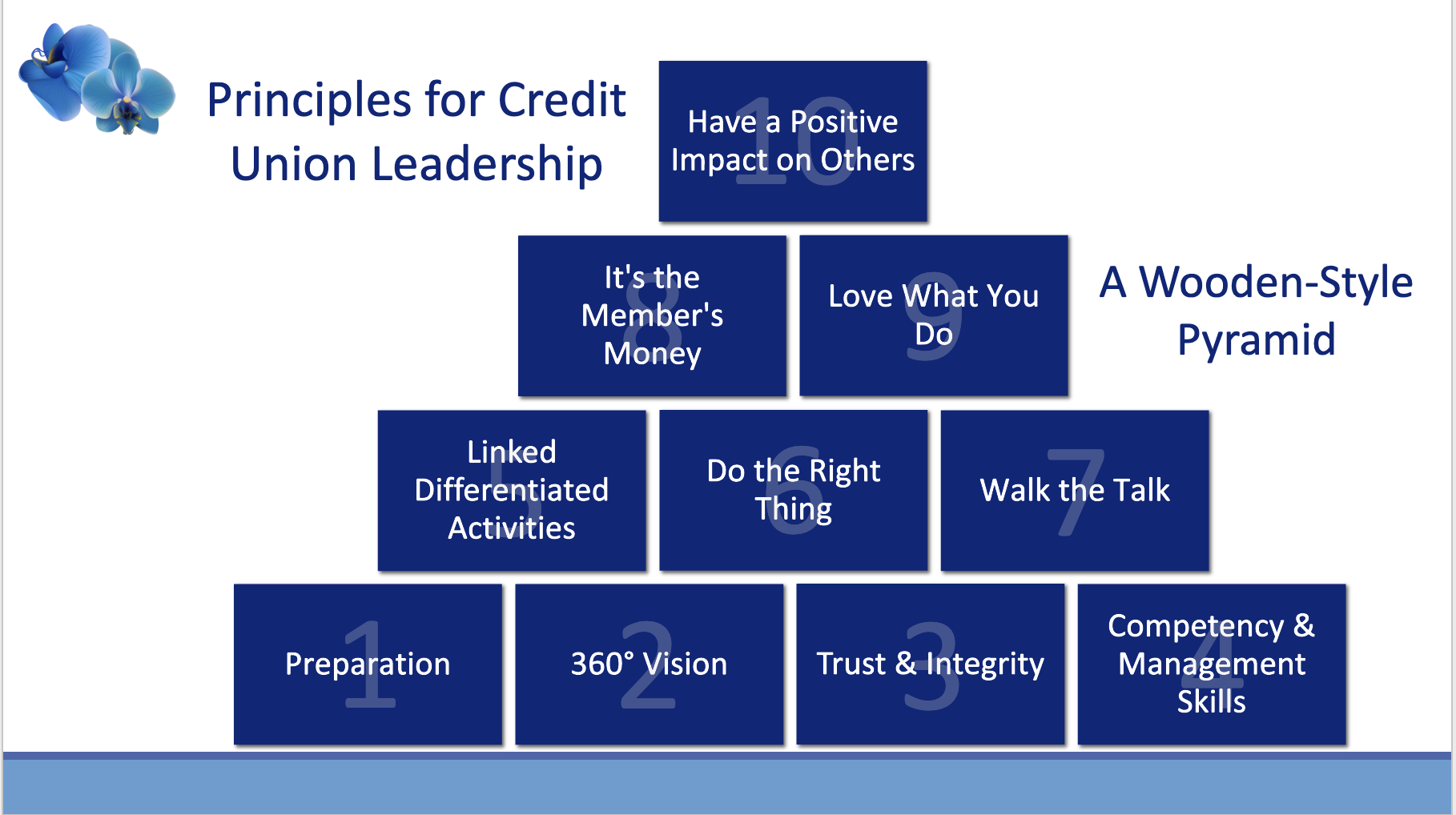

A favorite topic for John is his Principles of Leadership which he developed into a 50 slide presentation to the Aerospace conference in 2018.

The speech summarized his multiple professional and personal interests in a diagram similar to the UCLA basketball coach John Wooden’s nine principles of leadership. Here is John’s organizational template using a similar framework for credit unions.

The slides develop each of the nine points using examples from his numerous life experiences. The speech summarizes his approach to leadership. It also characterizes how he sees meaning in his multiple organizational and personal responsibilities.

John is now working on a book about his 25 years in credit unions. His activities are just one of multiple examples of credit union leaders who have stepped down but continue to follow credit union events. For many, these professional years are the most satisfying responsibility they have had.

Look around. There are examples of professional experiences and resources in every community, often like John, willing to provide perspective and an occasional assist. They see the world differently, often with more clarity than incumbents might assume.

And sometimes they are even delightful guests for the board, employees and members to hear from when those occasions arise.

In his book, John talks about his father’s recounting his story to youth leaders. Joseph would encourage them to keep teaching the lessons, because even though they might not seem to care, “kids are hearing and someday they may really, really appreciate what they learned.”

Life stories are not just for kids. For the past is never past, but always present.

Part of the job—arguably the job—of good journalism is to expose that brokenness. It’s to shine a light in the dark places.

However by focusing so much on what isn’t working, we sometimes forget what is.

If ours is an era of building and rebuilding, what things are worth saving? What things are worth elevating? What things are worth remembering?

And:

America won’t be saved by politicians

or money

or technology

or celebrities.

It can only be saved across the land by “character.”

One writer’s key lesson from Sophocles’ “Antigone” is that fanaticism results when public actors fail to practice the one virtue capable of moderating the excesses of human nature: political prudence.

What is one of the most frequent excess? the Temptations of Power

The American Franciscan priest and writer on spirituality, Richard Rohr, has described this all too human aspect from his religious perspective. I paraphrase his cautions.

One fatal snare is to misuse power. “Maybe we could say it’s a temptation to be spectacular, to be special, to be important, to be showy. The tempter says, “Tell these stones to become bread” (Matthew 4:3). When we’re young, we all want that. We all want to stand out. We want people to notice us. We want to be something special and to do something special.”

Another excess is the temptations of power whether politically earned or from one’s professional position. “It’s not inherently wrong. There has to be a way we can use power for good. But until we’re tested, and until we don’t need it too much, we will almost always misuse it. If we’re not tested in the ways of power, very often we end up worshiping power to have power.”

It is easy to confuse disagreement with a person in authority versus someone who is misusing or even failing in their position and accountability.

I would call out three frequent symptoms of lapses in leadership:

Positions of power are generally temporary. The tenure can be especially problematic if the responsibly of the role is not fully grasped. Especially in situations in which a leader does not acknowledge agency-that is personal responsibility or accountability: “staff, our consultant, our experts recommended this action; this is how others do it or, the classic, this is how we have always done it.”

Prudence is also a personal quality. In successful leaders it can be marked by both empathy and humbleness.

I believe there are daily examples from peers or colleagues from which one can learn. Especially when sharing initiatives, experiences and challenges of mutual interest.

My former partner Bucky Sebastian would sometimes comment on the views or actions of persons in authority whom he believed in error: “Everyone has a purpose in life, even if it is to serve as a bad example.”

Credit union leaders -CEO’s, boards, regulators, trades and even vendors-are public actors. Prudence is cultivated in public arenas by the respectful exchange of arguments among those attuned to both their personal and their community responsibilities.

Identify those leaders to make common cause.

Learn from those who fit Bucky’s description.

The day of the Allied landings in France, June 6, 1944 FDR gave a prayer via radio for the country.

This six minute “devotion” is especially pertinent on the anniversary of Russia’s invasion of Ukraine, as when it was first spoken in 1944.

Roosevelt talks of sacrifices and “pain, sorrow, faith and unity.” He expresses everyone’s longings and hopes for victory and peace. It is a prayer proper in any war and especially this day.

(https://www.youtube.com/watch?v=a2IRcc-5RgA)

Love endures: Valentine’s Day 2023 Ukraine

The Next Generation Arrives: A Mother and Newborn in a Basement Maternity Room-Kiev

War’s Playground Today & for Tomorrow’s Peace

This 29 minute video presents the critical role this online English language startup has played in telling about events in Ukraine. It includes reporters’ personal stories and presents videos of their on site coverage. This is one of many new Ukrainian enterprises to support the country in this time of trial.

(https://www.youtube.com/watchv=MxQ3JxJwdX0)

I recently received the best return ever on an investment: $250 in value for each $1 sent.

Late last year I read about a 501 C3 nonprofit (RPI Medical Debt) that bought unpayable medical debt using donations and then retiring all the acquired debt for consumers. Several news articles gave details about churches and local governments using this method to help members of their communities.

A December 20, 2022 New York Times’ article Erasing Medical Debt described how the program had extended to major cities such as Chicago and Pittsburgh. The story stated that 18% of Americans have medical debt turned over to a collection agency.

I decided to test the RPI Medical Debt’s concept. Was the payoff “leverage” as great as claimed? The 100 to 1 debt abolishment standard sounded too good to be true.

I also wanted to learn how targeted the program could be as a potential initiative for credit unions. Credit unions are significant originators of consumer debt. They know how past due delinquencies on a credit report can undermine anyone’s financial options.

Contacting RPI Medical Debt, I asked to purchase and cancel all debt from Jasper County IN, whose county seat is Rensselaer. Our family lived there for over five years while I was in high school. The town is primarily a farming community, neither wealthy nor poor, but one where the population today is the same as when we were there 60 years earlier.

Based on my pledge commitment, RPI retired all the available outstanding delinquent medical debt for 423 residents of Jasper Country totaling $264,878. They had no more access to debt available in the country right then, although more debt certainly exists.

However, with the funds remaining the non-;profit acquired debt from at least one resident in every Indiana county. The total consumers helped were 2,291 with over $2.532 millions of their debt erased.

RPI had acquired the debt for less than a penny on the dollar. The total accounts closed (not individuals served) was 4,396. Of these 9.3% (409) were bought directly from hospitals. The balance was from the secondary debt market.

Much of the debt (86%) was 5 to 10 years old– specifically 1,812 accounts with balances of $1.9 million. Only 1.8% of the debt was less than five years; 1.2% of the debt had originated over 20 or more years earlier.

The average debt extinguished had a face value of $846. For me, an overwhelming proof of concept! A financial “loaves and fishes” story.

Consumers cannot apply to RPI for relief. Rather the non-profit seeks to buy debt in the open market on behalf of funders who donate or make pledges to support their goal of abolishing medical debt for individuals and families burdened by the payments.

To qualify a “soft credit report” is run to determine each individual’s eligibility for relief. Potential portfolios are prescreened by holders to identify those who qualify for abolishment of debt. A person must earn less than four times the local poverty level (nationally an amount of $111,000 for a family of four) or have debt that exceeds 5% of annual income determined by pulling a soft credit report.

With these qualifications, the debt is excluded from income and not subject to IRS taxation. The transaction is considered an act of charity by donors who support RIP’s mission.

Each consumer is sent a letter announcing the relief. The total debt abolished, number of accounts and creditor are identified.

The “good news” letter says there are no strings attached and encloses a page of FAQs to answer questions. Recipients may, but are not required, to share their story about what this relief means to their circumstances.

This nonprofit was founded in 2014 with a threefold mission:

Since inception the firm has provided $8.5 billion of debt relief helping 5,493,000 individuals and families.

The immediate possibility is straight forward: strengthen members of their primary communities by offering to retire consumers medical debt. When fulfillment data are known, celebrate the relief impact. Invite consumers to learn more about another people-helping-people organization, the credit union.

Such an effort is a “win” on many levels: for the consumer, the credit union, the community and even medical providers with outstanding debt.

If interested contact RIP Medical Debt and make a pledge for a test project. I would be glad to share my contact and the reports and information I received. My project was completed in under 45 days from initial contact to finish.

As vital consumer lenders credit unions are at ringside knowing the debt burdens members carry.

Three days ago a Washington Post article reported the story of a 72year old still struggling to pay off his $5,000 student debt from the 1970’s. This is just one area where a similar approach for relief may be prudent and desirable. An example from the article reported:

Years of administrative failures and poorly designed programs have denied many borrowers an off-ramp from a perpetual cycle of debt.

There are nearly 47,000 people like Hamilton who have been in repayment on their federal student loans for at least 40 years, according to data obtained from the Education Department. . . About 82 percent of them are in default on their loans, meaning they haven’t made a voluntary payment in at least 270 days. . .

The Supreme Court will shortly hear a challenge to the Biden administration’s efforts to forgive up to $20,000 per borrower in federal student loans. The Court many not allow the initiative to proceed.

Why not design a program similar to RIP Medical Debt and approach the Department of Education about purchasing the loans with the intent of extinguishing them?

Credit unions would be helping resolve the financial and mental stress of longstanding student debt for eligible borrowers (to be defined). Even at a penny or two on the dollar, the government would be receiving more versus 100% forgiveness.

The program could be targeted where relief is most needed. It could happen fast. A “scholarship-in-reverse” plan where college debt continues to burden individual’s lives.

Can the cooperative movement demonstrate their collaborative entrepreneurial capacity and address a critical public need?

Two final data points from the Post article on student debt:

From the time student loan borrowers’ first loans enter repayment, the median length of time it takes to pay in full is 15½ years. . . Federal student loans are discharged upon death.

Must individuals wait till death for common sense relief?

The stories we tell, define who we are. They preserve those moments in life that we value. For organizations they communicate the culture. For a country, they express its collective national aspirations.

Two of the brief stories below are from CEO Tim Mislanky’s monthly staff update for Wright-Patt Credit Union. They honor the credit union’s commitment to service, its foundational value.

The third is an account of a father’s efforts to respond to segregation an ever present legacy in their community.

These accounts are not mere history. Rather they give meaning to life today. As you read, ask what story might you tell about your efforts?

A WPCU member, who is also ex-military, took a Greyhound bus from Cleveland to Columbus for a close reopen account. She is advanced in years so she could not do it online. She arrived at Graceland at 5pm and we had appointments till close at 5:00 PM. Stacy Davison was the only financial coach for the remaining workday. Stacie gladly stayed to be sure that our member was taken care of.

Through the close reopen process, Stacie found out that our member came all the way from Cleveland via the bus and hoped to get a bus back to Cleveland that same night. Stacie got online to try and help our member find a bus schedule to Cleveland, but there were no buses available until the next day.

Our member was then going to take a public transportation to a homeless shelter to stay the night. She had brought her dinner and breakfast with her to be prepared if she had to stay overnight.

It was dark and unsafe for our member, so Stacie told the member she would take her to the shelter. Stacie looked online to see if the Holiday Inn had a room, so she could pay for our member to stay the night in comfort, they did not, and the member would not let her do that. Stacie offered to drive her back to Cleveland, but the member declined.

On the way to the shelter Stacie tried to buy her a hot dinner, but the member said “I will eat what I brought from home.” The member said the shelter served dinner, so she could eat there also.

Manager’s comment: This is an example of going above and beyond for our member and, a great example of a servant’s heart.

Heidi recently worked with a member who shared personal details with her about how she was having financial difficulties and surviving on eating one hot dog per day. The member was having extreme difficulty being able to afford food in her home. Heidi went into action and found information about area food banks that she shared with the member.

A week or two later, the member returned to the member center. She told Heidi (while crying) that Heidi gathering those resources and sharing them with her was “life changing.” The member said that she was able to contact two food banks, and that both were able to provide food to her. She also shared with Heidi that she has now also secured a temporary part time job.

Manager’s Note: Because of Heidi’s work, we are developing a guide about food banks and area resources that can be shared with members.

A family story prompted by yesterday’s post about Springfield, Illinois and integration in the 1960’s.

My father, editor of the afternoon daily in a small city in the mid-Ohio Valley (population about 40,000), was about the same time fighting an uphill battle to change the status quo there. He spoke out a lot in his editorials and made himself unpopular with a certain type of citizen.

Sometimes the telephone would ring during dinner and my father would slip away and answer. “Who was it this time?” my mother would ask. “Oh, just another one of my sidewalk editors,” he’d say. But actually, some of them were calling to threaten him—and us. He didn’t stop promoting integration in schools and businesses and elsewhere.

As a ruling elder in the First Presbyterian Church he was hastily summoned to the church narthex one hot and un-air-conditioned summer morning where he weighed in successfully in an off-the-cuff decision to let a neatly hatted and gloved black woman stay for the church service.

A visitor from Texas, she had just come in and sat down in a pew causing a flurry of concern especially with another ruling elder who came to my father and said: “What shall we do?” No black person was thought to have darkened the church door before. There were supposedly only about 50 black families in the city and they had their own churches. Thankfully, nothing happened to the visitor and she worshipped unbothered along with the rest of us. But that kind of acceptance only went so far.

I remember well my father’s repeated consternation about a popular downtown cafeteria where the local Brotherhood Committee met regularly to plan interfaith events designed to promote tolerance and understanding. The Rev. Preston Smith, a loved and respected pastor of one of the local black churches was the only person of color on this committee that included a representative of the tiny Jewish community and Father O’Reilly of St. Xavier’s downtown catholic church.

Everyone except Rev. Smith went through the line and got his food, but someone else had to fill a tray for him and take it to the back room where the meeting was held. My father finally challenged the cafeteria’s owner: “Bill, why won’t you serve Preston just like the rest of us?”

“I’d like to. I really would, but I just can’t. It would ruin my business; people wouldn’t come. I’d lose everything.”

Some years later, the cafeteria closed for other reasons. I still have a brass plaque of the Brotherhood Award from 1968 engraved to my father for “Distinguished Service in Human Relations” presented by the local chapter of the National Council of Christians and Jews.

Recently our electricity company informed me that this month’s average temperature was 3 degrees warmer than the same period one year ago.

The New York Times asked in a recent article Why Hasn’t It Snowed Yet in New York City? The lead pointed out that this is the longest stretch of winter without snow since 1973. Plenty of rain. No Snow. City residents can still travel upstate to Buffalo if they long for a real snow storm.

Here is what this time of winter used to look like here at home in Bethesda.

Earlier this month some of my plants took an early peek to see what was going on.

The daffodils are now 3-4 inches high.

Hyacinths are poking their budding heads up.

Scottish heather is blooming early, normally it waits till February.

The neighbor’s forsythia is trying to catch up as well.

And even my early summer red poppy plant is making an appearance:

All I can say is that it is good I’m not a skier. Here is a picture of a popular slope in Europe last week:

More rain today. Temperature 45 degrees. I’ll just have to content myself with memories from 2022.