The response to my request for blog topics was blunt: “Board governance! Perhaps stemming from the frustration I feel on my own board. No relevant questions. No strategic discussions. No pressing in on how we can be better. No self-evaluations. Credit unions won’t survive with boards who simple show up and say aye.”

Then I learned how one election stimulated a complete renewal of the board’s role.

The Story

Frontwave Credit Union CEO Bill Birnie was “stunned” to learn the number of members who applied to compete for three open board seats in the 2021 annual election of directors. “Normally we have to beat the bushes for board and supervisory members.”

This year was different. The nominating committee approved ten applicants for a spot on the ballot. All submitted written statements with their professional background and why they wanted to volunteer.

Contested elections were rare at Frontwave (renamed in 2018) and even in its earlier era as Pacific Marine Credit Union.

The credit union put out its routine “Calling all Leaders” appeal in July of 2020 via email, a web posting and a member mailing on September 15. Headlines included: “Frontwave members make good leaders” “Got Frontwave Values?” “Help Members Financial Dreams Come True,” along with facts on the open positions and terms.

Highly Qualified Applicants

Among the applicants were nine with college degrees including four with MBAs. Their occupations included an active-duty marine, VP of finance, SVP asset-liability manager and budget analyst. Most had experience in an area of finance or management.

In addition, they were active volunteers in the community. Some examples: a college trustee, school district board member, and current board or past officer of nonprofit organizations and educational associations.

Why the Surprising Interest?

Since renaming as Frontwave, the credit union has grown over 40% to $1.1 billion in the highly competitive San Diego market. Bill, the President, had rejoined the credit union 2015 after serving as CEO for Eagle Community Credit Union. Bill believes that the dramatic increase in volunteer interest is a response to the credit union’s innovative spirit shown by its rebranding, and its increased visibility in the community with 14 branches, only five of which are on base.

The credit union’s surveys documented a 35% increase in positive member satisfaction, another factor galvanizing participation. The volunteer surge, Bill believes, reflects a growing respect for the credit union in the community.

Reasons candidates gave for their interest included:

- “To bring expertise, energy, and intellectual capital to power Frontwave’s success and strengthen our community. To represent the diversity and social culture of my community.”

- “I would like to help Frontwave reach their objectives and build value for members…lead(ing) to greater financial success of our members.”

- I want to have a “meaningful personal commitment to serve veterans and specifically Marines; real potential to have a tangible, lasting impact on their quality of life.”

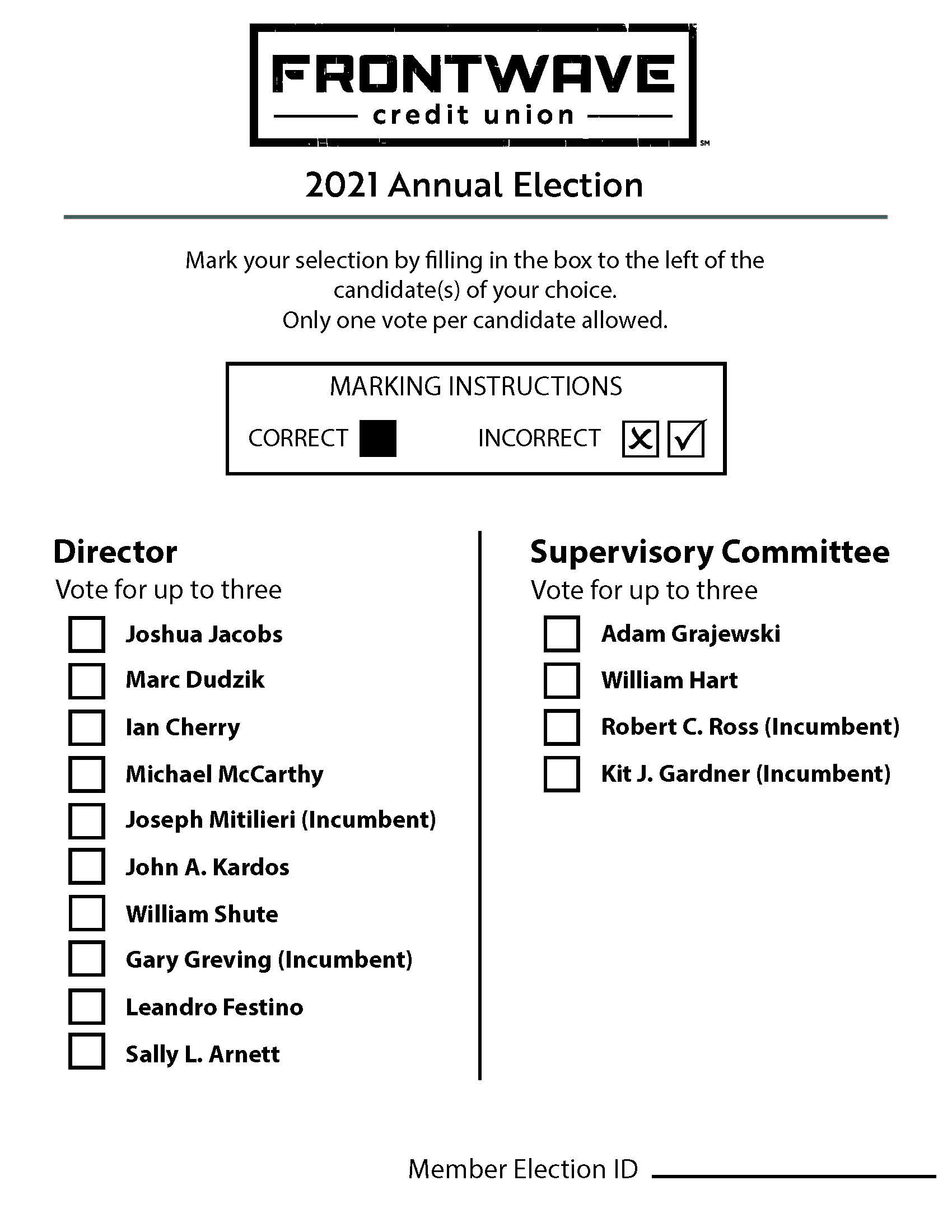

The Vote by Members

The online voting period extended from February 24, 2021 to March 24, 2021. Members could submit ballots at any of the branches from March 8, 2021 to March 19, 2021. The vast majority voted online. The number voting, 583 members, was almost equal with the last election in 2018.

The electronic ballot form provided an opportunity for members to comment on the voting and election process. Their comments were positive, particularly placing the candidates’ information within the ballot:

- “The (digital) interface is very easy to use…I like being able to open a page with all the bios while viewing the ballot at the same time.”

- “The bios gave a very personal involvement.”

- “The voting process is great reading all candidates listed in the process I didn’t know them, but by reading their bio gave me an idea of what they are all about. love it.”

- “I was so sure that this online voting process would be difficult, but amazingly, it wasn’t and I’m glad I was able to vote. Thanks.”

- “Very fast way to cast my ballot. I like to vote this way.”

- “WOW a lot of qualified candidates. This is the first time I have seen so many people run for a voluntary position. Good luck.”

- “I haven’t met any of these people, so I am voting based on the bios alone; they all seem like strong candidates to me.”

Lessons to Build On

Both management and board see this enhanced member interest as a “wake up” call for the credit union. Members were engaged in the election. The current age and tenure of the board suggests there will be more openings going forward.

The board is embarking on a self-assessment to evaluate their current skills and ascertain what the credit union needs going forward. The directors will provide the nominating committee guidance about the qualities and experiences they seek in candidates. The timeline, candidate qualifications and selection process may require further refinement with this new level of engagement.

While initially surprised, Bill Birnie now views this elevated interest as an opportunity to enhance the board’s contribution and engagement. The election has begun a process of board renewal: “We’re required to hold an annual meeting of the membership and, if needed, conduct an election. If we are going to do this, we are going to do it right.”

My reader above opined: “Credit unions won’t survive with boards who simply show up and say aye.” This example could be the best response to this “board governance” challenge.