Knowing our shared past helps us to understand the present and envision the future. History provides our sense of community.

From the May 1985 NCUA News, Vol 2, No. 4:

From the recent interview on NCUA’s Video Network, Chairman Callahan praised the NCUA staff, saying, “It’s all working, the team is in place. There is a sense of confidence in the Agency, and it has infected the credit union movement with confidence as well.”

The Chairman is quick to credit examiners and other Agency personnel for the successes during his term: “Most people at NCUA have a good sense of where the Agency is going and how they fit into the picture. People at NCUA get the credit for what we’ve been able to accomplish because they brought us to the point we are now.”

He believes three years of unprecedented growth in shares, loans, capital and membership attest to the positive effects of deregulation and to the success of credit union managers and directors when given the opportunity to make their own business decisions.

As important as deregulation is to Mr. Callahan, increasing the examiner ranks and getting Agency staff out in the field, closer to credit unions is just as important. “Deregulation actually increased our supervisory responsibilities,” he said. “We told credit union officials ‘You run our institutions, and we’ll be there to help.’ It’s a partnership, and it works.”

P.S. See the reference above to NCUA’s Video Network. This interview was the final edition, number XXI. If anyone has this recording in their credit union collection, I would appreciate making a copy.

What does personal service really mean when a credit union has over 63,500 members?

Weokie Credit Union’s Mission Statement is:

Change lives in our community, one person at a time, by being the best place our employees have ever worked and our members have ever banked.

A Nurturing Voice

The CEO, Jeff Carpenter, gave permission to demonstrate how this is done, one member at a time, in this story from his March 2024 report to his team:

“Marlene is an elderly member who has been the victim of several recent frauds. The team got together to determine what WEOKIE might do to help (and not upset the member or violate privacy concerns). We determined that WEOKIE should try to get Marlene to add one of her children to her account, to help monitor the activity.

“It was also decided that Rhonda would make the call and Jeff S. would be there to assist in case things went sideways. Jeff’s take on the call:

“Rhonda reached out to Marlene this morning while Melinda & I listened in the office. She did an EXCELLENT job speaking with Marlene and conveying WEOKIE’s concerns about her account activity and how we can best help her to keep her accounts safe.

“After several minutes and a lot of small talk to gain Marlene’s trust, Rhonda was able to get her to agree to add her daughter added to the account to help with her finances. When I say small talk, it was over 50 minutes of conversation! It was like having a long discssion with a grandparent. You just let the conversation take its own flow and slowly steer it back to the intended purpose. Rhonda did awesome in this aspect. Her Nurturing Voice truly shined in this interaction.

“Rhonda maintained ownership all the way through by following up with Jessica at Main to: provide the details, including Marlene’s vulnerabilities to fraud; the estimated time when the two members might come in; a commitment to follow up when the meeting is set; a request to be notified to facilitate a warm hand-off; an explanation about the Risk department’s approval of the exceptions with a clear understanding of expectations of the member; and how our role impacts the member’s well being.

“This effort involved six employees and shows the role of teamwork, several of our monitoring tools, and our commitment to making this credit union the best place Marlene has ever banked!

“Special thanks to Joseph for sharing this member story and how Rhonda, Diane, Jeff S, Melinda, and Victoria worked together to take great care of Marlene.”

The Takeaway

That’s every credit union’s potential secret power: serving every member, one at a time.

I believe his observations apply to aspects of the cooperative system especially mergers of sound credit unions* now being presented to member-owners.

“First: The free market is a myth.

“The idea that the world would somehow be better off if there were zero rules protecting the masses from predatory investors is not only deluded and insane, but it’s unfathomably dangerous. A rules-free-market is a black market where the worst actors win.

“Capitalism is all about incentives, and investors have twisted the economy to incentivize extraction and exploitation.

“Second: The modern rules-free-market isn’t what the father of capitalism Adam Smith meant when he said “the free market.”

Communication transforms when it touches a person’s emotions. It transcends the moment. It becomes art. It helps us see beyond what we knew before.

The most difficult challenge for any organization is telling anyone why they should be interested in joining with you.

Messaging is more than competing for our attention with a product commercial or a clever brand. Ultimately, it must appeal to something inside. It should make us care.

He Gets Usis a video campaign that attempts to represent the “greatest love story ever told.” It suggests the relevance of christen belief in today’s context of religious decline or misuse.

This creative group states its purpose as follows:

We’ve done a lot of homework on our culture. We researched how people feel about each other and what they think about Jesus and Christianity. We’ve connected with thousands of people of various faith traditions and those who claim no religion. We spoke to all kinds of people — different backgrounds, beliefs, and, yes, political affiliations.

And this is what we’ve learned: From politics to sexuality and religion, so many of us feel like our values, beliefs, and identities are under attack by the ideological “others” around us. Many perceive those who differ with them on issues of justice, dignity, and humanity as not just wrong or misguided but also as evil. As enemies. We often see these “others” as close-minded, selfish, hypocritical — and if we’re honest, many of us respond in kind.

This week I will share several of the group’s “presentations” which look and are sometimes presented as commercials. But they are much more. They help us see, to understand more than we did before watching them.

The Credit Union Parallel

What do these “messages” have to do with credit unions? To be seen as relevant in today’s crowded social media is the same challenge credit unions confront. There are a number of organizational parallels.

The participation trend lines in most religious denominations are trending down. Smaller churches are closing. Larger ones are greying. Sunday or Saturday “sabbath” is a time for family errands, fun outings and preparation for the week ahead-not participating in a community of shared purpose. Society’s divisions are mirrored in our religious practice as presented in the group’s purpose:

The more ideologically defensive we become, the more we are willing to sacrifice things like kindness, patience, and the respect and dignity of others for the sake of victory — the righteous ends justifying the dehumanizing means. And it’s tearing us apart. We experience it in politics, in the workplace, in schools, and even in churches. And at the heart of the conflicts is a fundamental disagreement about what it means to be good.

Credit unions and churches no longer seem central to many persons’ lives. Our basic needs and core values, “to be good,” are fulfilled in other ways and commitments.

The He Gets Us videos try to show the relevance of lessons from generations ago for real people today.

My hope is to inspire rethinking for today’s coop messages. We need to move beyond the headlines and priorities of our current moment and rediscover the energy that made the industry a movement, an alternative to the status quo and rediscover who we can aspire to become.

The Immigrants

A hot button topic when people are polled about public issues for political campaigns is the flow of migrates to America.

The one-minute video, Refugee, presents this ongoing human circumstance with a specific context.

(https://hegetsus.com/en/featured-videos/refugee)

What I found equally compelling is the producer’s five-minute story telling how this video was assembled. The making of the Refugee video:

Does this message open one to a different way of seeing this issue? Does it stay with you after viewing? Does this human-centered perspective suggest a parallel in your credit union’s role?

I recently received a copy of a CEO’s description of a fraud/robbery event at the credit union.

The CEO’s summary was sent to all employees for two reasons:

To fully serve and assure any members whose accounts might have been affected by the event.

To convert the incident to a learning experience for the entire staff.

Here’s why the CEO believes full transparency matters:

“Whenever we take a loss I consider it a tuition payment. The least we can do is become smarter as a result of making that payment. We’ve already taken all actions to mitigate/manage the risk. Hopefully others can become smarter as well.”

In that spirit, here is his summary description of this very well-planned theft used with permission.

ITM Defalcation

Everyone should be up to date on the robbery that occurred in early March . Perpetrators placed skimmers on two of our ITMs in mid-February and removed them just over a week later. They captured the magnetic stripe data of all cards used during that timeframe, re-encoded vanilla gift cards and drained our ITM’s on a Sunday morning in mid March.

All affected member accounts were immediately made whole, and all cards were blocked and re-issued. We identified all member cards that were compromised and are almost through the process of blocking and re-issuing all of them.

The Secret Service and FBI joined local law enforcement and we are assisting their efforts as much as we can. A bond claim is being filed so we remain uncertain as to what net loss we’ll incur.

What’s Important

Several configuration and procedural changes were implemented immediately, a few more in the days that followed, with still other changes under consideration. What’s important is that no credit union system was compromised at all, we know exactly how the perpetrators did what they did, and are actively taking steps to mitigate any future loss exposure. The perpetrators did not obtain any personal identifiable information (PII) such as name, address, account number, social security number, driver’s license number, etc.

Rapid action was taken to both replace any funds taken from member accounts and to prevent a repeat of this in the future. Everyone in the financial centers and contact center did a great job interacting with impacting members.

Everyone a Risk Manager

The incident was not a “local” gang. This theft was perpetrated by professional thieves who move quickly from state to state. Collaboration is a credit union advantage especially when a CEO is shares his “learning experiences” with his peers. Thank you.

Who do members turn to when they believe their credit union is not responsive to requests for greater transparency or accountability? These situations can arise around bylaw interpretation, board oversight, and election conduct.

Following are two examples of members’ interacting with their state regulator when they believe accountability is lacking in credit union conduct.

A Live Hearing-NOW

The first is a hearing of the North Carolina Credit Union Commission at 10:00 AM EDT today. Several members have sought clarification of the regulator’s approval for bylaw changes, especially those that affect the board election process. The toll free call in number is 1 (984)-204-1487. The access code757767261#.

There are thirteen items on the agenda, but the primary one is an update by the state administrator, Kristina Ray, on all areas of her responsibility. The ability to listen to a live state update is an important opportunity not just for North Carolina charters, but for all credit unions who are interested in the state and federal oversight process.

A Member Complains- the Regulator Responds

A reader sent me a March 18, 2024 article form the Lost Coast Outpost titled:

The story is a press release from one of the candidates for Coast Central’s board. She filed a complaint with the California Department of Financial protection over the credit union’s failure to release vote tallies for the 2024 board elections.

As a result the credit union posted the vote totals for all candidates for the most recen two years with the Chairman’s reply:

“In response to members requests at the annual meeting and in the spirit of enhanced transparency and goodwill, we have taken the additional step of posting the vote totals from the previous year on our website. We hope this action demonstrates our commitment to transparency and our dedication to addressing the concerns of our members.”

Prior requests to the CEO for details of the vote had been turned down.

The complaint was filed by Carrie Peyton-Dahlberg who wrote the press release for the local paper. The posted results showed she had come in fifth place just 172 votes behind the fourth place elected candidate in the 2024 election:

Matt Wakefield: 1,641 votes (73.1%), elected to a 3-year term

Terry Anne Meierding: 1,600 votes (71.3%), elected to a 3-year term

Ron Rudebock: 1,520 votes (67.7%), elected to a 3-year term

Dane Valadao: 1,346 votes (60.0%), elected to a 1-year term for the remainder of a 2023 retiree’s term

Carrie Peyton-Dahlberg: 1,174 votes (52.3%), not elected

In her commentary “she urged Coast Central member-owners to use their comment cards to ask for further progress, such as publicly announcing board vacancies, revising board election rules so they don’t hinder election outreach, and changing the board appointment process so that future vacancies can be filled in a way that is more representative of community demographics.”

“Coast Central is moving in a good direction, including releasing these numbers, putting 2024 election reminders in each branch and making sure that its ballots were sent in clearly labeled envelopes. All of these are big improvements over the January 2023 election, and I hope this is starting a new trend.”

“Bit by bit, if member-owners stay involved, we can encourage Coast Central to move further down this path of listening to the people who own it.”

Democracy Takes Work

Releasing the actual votes in a member election would seem to be a fundamental requirement, a no-brainer. The California regulator seems to agree that members are entitled to know the actual votes cast in an election. That may seem like a small step, but is still not followed in all credit union merger and board elections-whether for state or federal charters.

This California precedent matters. Democracy can be a contagious activity. It is also a participant activity, not a spectator sport. Carrie Peyton-Dahlberg has done every member-owner a service by raising this issue of election transparency in her credit union. Hopefully, all regulators will soon see this fundamental accountability for a democratic process the same way.

During my college days five decades ago, the primary work-study jobs were dorm crew, dining hall or checking out library books. Students receiving financial aid were expected to work at least 10 hours per week.

As the decade of the 1960’s progressed, the college campus atmosphere inspired by the Camelot years of President Kennedy gave way to the increasingly anti-Vietnam war and civil rights movements.

New protest groups were spawned across campuses. These included SNCC, Black Panthers, SDS and multiple other efforts to support social and political change.

In a partial final year on campus waiting for my date with Uncle Sam, I saw a three-day occupation of University Hall and attended a student meeting where one of the participants placed a gun on the table to demonstrate his radical intentions.

Part of this campus mood was anti-business—all kinds, not just the protests against Dow Chemical or other business seen as supporters of war. Capitalist society was deemed responsible for the multiple wrongs protestors wanted to change in US public policy and social inequity. No one saw business, or entrepreneurship worthy of academic attention or support.

Still, students would occasionally use their university setting to develop start up ideas. One that became very popular in the ’60’s was Operation Match, a paper based computer analysis of questionnaires to provide participants names of potential dating partners. It was noteworthy, because it was an innovation that filled an ever- present social need.

Today’s Campus Environment

For the past decade there has been a revolution in both attitude and support for students in higher education who wish to create new business startups.

All of the top universities now have on-campus organized support, including courses for students and faculty who want to start new businesses.

Every listing is a top academic institution including Harvard, Duke, UT Austin to USC and UC Berkley.

Here is a description of MIT’s multi-option effort which is headlined with its $100k Pitch:

MIT delta v: An accelerator program that runs from June-Sept for MIT students with the ability to receive up to $20,000 in equity-free milestone funding.

MIT NYC Startup Studio: A startup studio in NYC for MIT students and alums with the ability to receive up to $20,000 in grant funding.

MIT Fuse: A 3-week micro accelerator for teams with at least one MIT student as a founder.

Amazon web services (AWS) now sponsors a nationwide competition for university based startups: “It’s no secret that some of the most successful startups were founded by members of the university community: from Ava Labs to Anyscale and InsightFinder, to name a few. At Amazon Web Services (AWS), we believe this is because students and faculty are often creative thinkers who are willing to take risks and collaborate with their peers—all essential qualities in a founder.”

“For current Harvard students, the Venture Incubation Program (VIP) within Harvard’s Innovation Lab fund is a 12-week program with mentoring and resources. Harvard’s Innovation Lab also hosts the President’s Innovation Challenge, where students can win funding money of up to $75,000 for a great idea. Judging criteria includes viability, empathy, rigor, ingenuity, traction, economics, and impact.”

Here in D.C. George Washington University sponsors an annual competition inviting students, faculty and their supporters to present business proposals and collect cash prizes and other forms of startup support and counsel.

Three finalists compete in one of four startup categories:

Consumer Goods & Services

Business Goods & Services

Social Innovation

Health Care & Life Sciences

Each finalist prepares a one-minute video of their business proposal. There are immediate cash prizes plus additional consulting and funding support:

First place winners selected from these tracks will each win $10,000

2nd place cash prize $7,500/track

3rd place cash prize $5,000/track

Companies have one year to register as an LLC to claim the money.

To see these young entrepreneurs’ ingenuity, passion, and commitment I would encourage you to sample one or all of the 12 finalists’ sixty second pitches which you can find here. Several that were intriguing were Siyeh Tech’s entry to accelerate the “Speed of Peace” after conflict, In-Locater, and Goal Plus.

All of these business ideas are either conceptually complete, if not already in beta. George Washington’s New Venture Competition is one of many in the higher education community. This is not only an “educational” institution responding to students’ interests; in some the university benefits from partnering as startups go to scale backed with venture capital.

These competitions are not standalone events such as a campus springtime arts festival. These programs are supported by courses, different “labs,” seminars and lectures on the art of pitch preparation and visits by university alumni speaking on their business success.

These educational innovations are helping to spark an ever-renewing stream of new business ideas with support systems intended to foster success. Students are encouraged to jump into the capitalist world and perhaps reap fame and fortune.

Simultaneously a parallel change for venturing has developed for college athletes. They can now receive income from their Name, Image and Likeness (NIL) endorsements by private businesses. Caitlin Clark is not only Iowa’s leading basketball player, but she also appears in commercials while her games are being broadcast. She may be the first million dollar undergrad student-athlete.

And Credit Unions?

Unlike my era in college, higher education is an active participant in American enterprise. What does this have to do with credit unions?

Cooperatives are missing in action. Students are not learning about personal finance from credit unions. Credit unions which have students in their FOM’s often see them as a secondary market opportunity.

Every company, professional sport franchise, consumer product, auto manufacturer etc. must resell its brand to the next generation of users. Or face the prospect of going out of business. Product loyalty, like religious observance, is not easily passed down in a family in today’s society of instant access and social media.

If credit unions miss this generation of college students, will they ever catch up as they move on in their careers and families?

In the 1980’s, NCUA played a very active role supporting new student led credit unions as described in this post. That effort is missing today.

Credit union’s absence from college and university campuses feels like a missed opportunity for attracting this generation of self-help innovators and strivers. How do coops become part of this new enterprise engagement by student entrepreneurs?

Today is Maundy Thursday of Holy Week. The day of the Last Supper and Jesus’ arrest in the Garden of Gethsemane.

Events on this and subsequent days include two intense examples of human motivation not limited to strictly spiritual contexts. Rather the story shows how any individual might react to events in their own life.

Prophets and Honor

Every social system has ways of recognizing the successful and the benefactors of their profession. In credit unions a major event is the Herb Wegner dinner, the occasion for presenting lifetime achievement awards to honor selected leaders.

These traditions salute individual’s values and/or performance that fulfill the goals of the industry: profit, service, innovation, growth or even longevity. Some goals are very tangible, others more qualitative.

Those Without Honors

But whose contribution does not get honored? The topic is raised at least twice in the New Testament:

In Mark 6:4 Jesus said to the crowd, “A prophet is not without honor except in his own country, among his own relatives, and in his own house.”

And, in Luke 4:24 (English Standard Version 2016): “Truly, I say to you, no prophet is acceptable in his hometown.”

Why this disbelief? Does familiarity breed contempt? Are we skeptical of any special insight let alone prophetic wisdom from persons we know well, have worked with over years. and who seemingly share the same experiences as everyone else? Why should one peer’s views be trusted over another’s?

There is an inherent caution to see those among us, whom we know well, as having special insight versus merely expressing a different opinion. Persons, often outsider who focus more on the message, are often more inclined to listen to these singular views.

Ordinary people can have extraordinary wisdom. Sometimes their outspokenness make them unpopular with those in authority or leadership. The “prophetic voice” is uncomfortable. It challenges current shortcomings often with a passionate hope for a different future. For those who are being challenged, this passion feels like anger.

I am not referring to the purveyors (often consultants) of innovation who promote operating improvements. The prophet’s concern is more deeply rooted in fundamental meaning and purpose.

The question for credit unions is, are there any prophetic voices challenging local or national priorities today? Who might they be? What is basis for their critique?

And if we can name none, what does that say about the state of our “movement”? Has consensus trumped wisdom?

The Thirty Pieces of Silver

A second example routinely pulled from Maundy Thursday is Judas’ betrayal of Jesus in the Garden for 30 pieces of silver.

Think of how often this metaphor is used to accuse someone taking an action for monetary or other rewards seemingly to betray their personal beliefs.

Rev. Megan Brown takes a more nuanced view of Judas’ motivation:

“Judas was not a peripheral bystander, but one of the twelve, the inner circle of disciples who had accompanied Jesus in his ministry and in a shared, communal life together.

Surely Judas knew the implications of his actions. Surely, he knew that the chief priests and the elders were growing weary of this rabble rouser, Jesus, and that they wanted him gone. This exchange, and the kiss that follows later are ominous moments in the life of Jesus and his followers. They leave one wondering about Judas’ motivations. “

Judas was a believer. Some have interpreted his action as driven by deep disappoint that Jesus was not radical or bold enough in his Jerusalem journey. The march from the Mount of Olives to the Temple should signal a rebellion against Roman rule, not a pacificist call to turn the other cheek.

Or, maybe he sensed that the multiple political forces mobilizing against this upstart rabbi from Nazareth were becoming too strong; so he decided to go to the other, more likely “winning” side.

Perhaps he was emotionally confused by the historical intensity of the Passover remembrance, the increasing crowd appeal of Jesus and the growing immanence of a life-making choice.

What we know is that Judas deeply regrets his actions, attempts to return the silver coins and commits suicide.

Judas shows us the very human side of intense hope and belief. Is this a movement that will go in the directions I believe it should? Is there another option to this leader’s course of action? How does one express dissent if convinced current directions are not the best?

How many initial “reformers” give up their quest from exhaustion, just to get on with life, and be comfortable with their peers?

Whether Prophetic Voice or Judas?

All movements have both personalities in their adherents. We all might cite leaders who took courageous stands or whom we believe compromised their duty to their followers.

That is what makes leadership so critical, and often controversial. It is also what makes public dialogue so vital.

We live in an era where there is continuing reinterpretation and debate after millennia about faith, whether Christian, Jewish, Muslim or just a value-centered life. While many believe that truth, when proclaimed, is universal; even some would challenge that assumption.

The one common approach that all faith and other “movements” followers have ultimately taken to succeed, is to pursue these issues in community. People aligned with one another agree to listen and learn together how their differing perspectives can arrive at common purpose or priority.

The Necessity of Community

Scott Galloway has put the power of relationships in a much broader context in his precent post Mammal.ai.

“Within and across species, relationships are essential to surviving and thriving. . .

“Humans have speedballed the power of relationships. Physically we are weak, slow, and fragile, with mediocre senses and absurdly long infancies. Yet, thanks to our superpower of cooperation, we’ve dominated our environment and become the apex of apex predators. There are more birds in captivity than birds in the wild. . .

“We are wired to seek and sustain relationships and cannot survive without them. The future of the human race won’t turn on space travel or climate tech, but on our ability to attach to others. A sense that we matter, that we can call on and be called upon by others to ease burdens and celebrate joy.”

It is not coincidence that the last moments of Maundy Thursday’s Biblical events were spent in community. Christians call it The Last Supper.

Music for Holy Week

Stabat Mater, by Antonio Vivaldi (1712). There have been many beautiful settings depicting the scene of the Mother of God standing in sorrow at the foot of the cross.

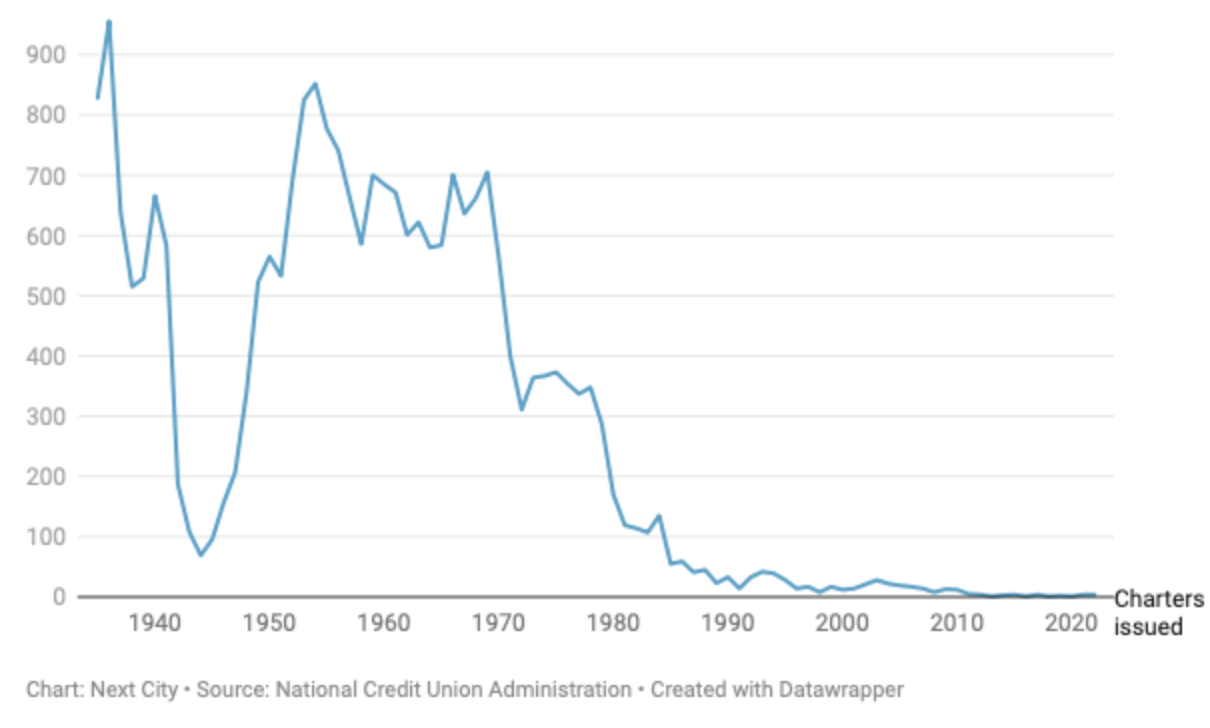

Oscar Abello is the senior economic writer for Next City. His focus is community initiatives that bring opportunities to those left behind by existing financial options. New credit union charters are an area of special interest.

The announcement of this new charter’s background has been reported by the credit union press. Abello’s story focuses on the difficulties of the process. Here are some of his observations:

Chartering a new credit union today is like traversing a long-lost trail through the woods, one that used to be well-traveled but is now overgrown, littered with fallen trees and other obstacles no one has had to navigate in many years. Prior to 1970, there were 500 to 600 new credit unions chartered across the country every year. After a steep decline to near zero, the numbers have never recovered. Over the past 10 years, fewer than 30 new credit unions have been chartered across the country.

New Credit Union Charters

The annual number of new credit union charters issued nationwide by the federal government, as published in the annual reports from the NCUA.

According to Inclusiv, a network of credit unions that focus on community development, minority credit unions across the country are closing at the rate of one per week, making the new Arise Community Credit Union’s chartering even more urgent if that trend is to ever be reversed. (Editor’s note: all credit unions close at a rate of more than three per week). . .

Arise hopes to fill in the gap left behind by other more conventional banks and even other credit unions. Predatory lenders have jumped into the gap left behind by the retreat of the mainstream banking system from certain communities. African Americans are twice as likely to live within 2.5 miles of a payday lending storefront, compared with all Minnesotans. . .

Chartering a new credit union is a huge lift. It’s been nearly eight years of organizing for Arise, but it’s not uncommon for aspiring credit union organizers to take multiple years between initial conversations to raising startup capital to finally getting a new charter. The Association for Black Economic Power also had to deal with a leadership transition along the way — it’s now led by Debra Hurston. The new credit union has its own CEO, Daniel Johnson, who has deep family ties and professional ties to the Northside of Minneapolis.

It would have been easier — and quicker — for Hurston if her group just brought in an existing bank or credit union as a partner organization to provide access to credit and basic financial services to the Northside.

But Hurston says in surveys, town halls and just informal conversations over the years, the Northside’s desire for its own institution has only gotten stronger.

“The mistrust in the banking community, it’s not a small thing, and it can’t be fixed overnight,” Hurston told me last year. “We’re starting from the wrong spot…if I have to protest in front of you to make you treat me right. Something’s not right about that. So no one from our communities has ever asked me if we should just partner with a larger bank.”

Insight for Those Who Care

Abello’s reporting should be a boon to the credit union community. For as Robert Burns wrote of this ability to see what others may not:

O wad some Power the giftie gie us To see oursels as ithers see us! It wad frae mony a blunder free us, An’ foolish notion: What airs in dress an’ gait wad lea’e us, An’ ev’n devotion!

Music For Holy Week

Christ on the Mount of Olives, by Ludwig van Beethoven (1803)

The local Shakespeare Theater’s run of the story of Lehman Brothers family in America incorporates multiple themes. They are all very much present in America today. I believe they can inform the credit union story.

The play is an adaptation of a novel about the Lehman family. Three actors portray 55 different characters in the 163 years of the family’s timeline.

Although the firm’s $600 billion bankruptcy was the central drama of the 2008 financial crisis, the family had long been absent from any leadership roles when this occurred.

An Immigrant Story

The play is the story of a German Jewish family settling in Montgomery Alabama in 1844. After first opening a dry goods store, they expand to become “middle men” in the cotton trade between southern plantation growers and Northern textile mills.

They eventually open a New York office to enhance their trading activity and expand to other commodities post Civil War. These trades include wheat, coal, iron ore, that is the raw materials at the center of America’s industrial revolution.

As their trading activities expand they become a “bank” and underwrite the new industries being founded from railroads to computers and entertainment after WW II. Eventually these material commodities are supplanted by stock trading which brings the firm close to collapse in 1929. Outside owners will now control a majority of the firm.

Post WW II trading activity dominates its traditional investments in other industries. These traders buy out the firm’s presiding CEO, Pete Peterson, putting their priority on a strategy that eventually leads to the 2008 failure.

The story of growing economic wealth is interwoven with the family’s old world religious and family values. Jewish celebrations are initially central to life, but gradually become less so as succeeding generations assimilate into American culture. Their religious observance is “reformed.”

A Three Part Saga

Part family history, part portrayal of evolving moral values and part the story of how finance becomes central to American enterprise give the play multiple layers of meaning.

As I watched this century and a half saga, many parallels with the present day credit union story come to mind.

Credit unions have largely moved away from their focus on a local group or community to become a diversified mixture of legacy founders and new market expansions. The values and passion so critical for success in early years have been replaced by professional managers brought in for their expertise.

Growth becomes central to reporting success. Corporate wealth creation versus member well-being is celebrated. Instead of open governance, oversight is increasingly concentrated in a few hands where leaders perpetuate their tenures. Rather than paying their success forward to future generations, incumbents explore options to cash out when their term in leadership is ending by turning control over to other firms.

The Past Is Gone

The Lehman family gradually lost control of their “bank” when market circumstances required new capital. Evolving financial trends for their trading skills also changed the firm’s purpose. Middleman roles gradually evolved from buying and selling actual commodities, to underwriting new businesses and then merely trading pieces of paper, i.e. stocks. Ultimately finance became just digital transactions.

In this new world, everything becomes a number. And everything has a price. Finance becomes just a way to make money, versus investing in tomorrow’s economy.

Buying and selling (acquisitions) become critical skills. Member/customer trust is eroded because consumers no longer believe you will be there for them. Money management becomes the epicenter of success. All ties to previous values and economic roles are ended.

That in short is the story of Lehman Brothers creation. Is it an object lesson for credit unions?