A reaction to yesterday’s comments on the merger of Vermont State Employees Credit Union and New England FCU.

…but y’know, something still doesn’t look quite right?!?

Chip Filson

In the It’s a Wonderful Life movie classic, George Bailey is granted his wish and gets to see what life would’ve been like had he never been born. He’s shocked by the results.

There was no one to fight for market competition, equality, opportunity and ownership for the working poor and middle class. Bedford Falls is renamed Pottersville.

Pottersville is packed with bars, strip clubs, casinos, and pawn shops. It’s full of cops and traffic and lights and noise and strangers. It’s filled with colder, harder people, with more violence, gambling, mental illness, debt, and rampant consumerism.

As George Bailey stated:

“Just remember this, Mr. Potter: That this rabble you’re talking about, they do most of the working and paying and living and dying in this community.”

Yesterday’s post presented a long-standing loyal member’s critique of the Vermont State Employees (VSE) merger with New England FCU (NEFCU). His objections included:

How did this idea of merging two “financially strong” credit unions arise? In a May 2016 interview with VT Digger, Rob Miller talks of his “learnings” after being hired to the VSE CEO position, his first job in credit unions:

“I thought it would be boring, frankly, to work at a bank,” he said.

Then he learned about the organization’s mission, that it was a not-for-profit financial cooperative, and that anyone in Vermont could be a member.

“VSECU’s mission – to improve the lives of Vermonters – that really spoke to me.”

“I suddenly saw an organization that had the capacity and the resources to really fulfill its mission,” he said.

His background isn’t one that typically leads to the position like he now holds, he admits.

“My first day as CEO was my first day working at a credit union. That was a big step for the board to hire outside of the industry.”

He lights up when he talks about VSECU’s latest initiative, to offer equity financing to cooperatives in Vermont, which typically only have access to debt financing. (not an FCU option)

“Coops are an important part of any regional economic development strategy,” he said. “They are locally owned, and the owners are the customers – it’s a business model that is inherently more sustainable,” he said. “It’s like paying yourself. That’s a natural incentive for success.”

“At our core, we are a cooperative. We embody people coming together to help one another,” he said.

These sentiments are certainly proper. In light of his merger initiative, the remarks suggest that human nature cannot always be nurtured.

In contrast, the CEO of NEFCU has held the top position since 1987 (almost 36 years) and will continue in that role after merger. Miller, as CEO of VSECU arrived in 2014, inheriting 65 years of members’ loyalty, resources and institutional success. He will be President and COO of the newly combined operations.

Here is a 1.34 minute video of the two men talking about this “partnership” and why a new name is important to “building a new organization.”

It is easy to understand how the two CEO’s developed the transaction between themselves, and then sold it their boards and staff. Their motivations are straight forward. It was a succession plan and capstone for the CEO nearing retirement. For VSE’s Miller it was a personal opportunity to take over a firm almost three times the size of his current job. A win for both, at the members’ expense.

No one would want stop a CEO from moving to a new job at a larger credit union. Happens all the time. But in this case the circumstance of the CEO bringing his credit union with him to this new job is highly unusual.

In the video the two men talk smoothly about “building a new organization” of 500 people. This necessitates a new name since the legacy of the old ones would hinder this process. This marketing video was part of the sales campaign. All members need to do is just vote their approval.

If you believe this “new organization” is built on the movement’s uniqueness, listen for the number of times the words cooperative or credit union are used. Or how this merger helps members. Zero. There are no beliefs like those used in Miller’s Digger awakening interview above.

This short video is professionally staged, in a garden-like setting, background theme music, the casual dress and coffee cups on the table creating an impression of shared camaraderie. It is all part of the grift.

A transaction so shallow suggests this merger of these previously sound credit unions may not be as straight forward as presented. Without a carefully considered roadmap, all the hard issues have been kicked down the road.

Here are several reasons why this merger, like many, may end up reducing, not enhancing member value.

In September VSE reported $25.3 million in borrowings as 12-month share growth fell to just 1.8%. Even with a $20 million increase in shares, the credit union’s dollar dividends to members fell 28% from the prior year. Members are paying the price for this underperformance. The credit union reduced its average cost of funds to just 16 basis points, even though short term rates have risen to almost 4%. The unrealized loss on the $136 million of investments went from nil to $25 million over the past year.

Prospects are so poor in Vermont that the plan is to take members deposits and earnings and invest those out of state. A sure fire way to retain Vermonters loyalty!

Throwing members under the bus to support an undefined merger plan is not a sustainable strategy.

It’s a Wonderful Life portrays the eternal conflict in a market economy between self-interest and those who believe in community values and stability. These two CEO’s are following Potter’s model, putting their futures ahead of their responsibility to members. The two Boards bought into the shell game; the employees put their names in the merger Notice in contrast to the values they had expressed making VSE truly special.

As the shallowness of this effort becomes more exposed, it won’t just be the members who will pay the price; the employees will learn that $100,000 plus jobs are a luxury when institutional success is the primary goal.

VSE member Don Kreis foresaw this possibility in his comment letter: If the $1.1 billion Vermont State Employees Credit Union cannot stand alone, cannot be just as convenient as a bank while giving members more value and more control than a for-profit financial institution can, then combining with another credit union is a waste of time.

The problem is not size or resources. It is a market-based society’s ever-present challenge of balancing personal self interest and community. In an earlier blog, The Tragedy of the Commons, I expressed the view that this and similar mergers were a test of whether a unique credit union system can survive:

A coop system reliant on values as a differentiator cannot long continue with coops and market capitalist wannabes side by side. For the latter will continue to prey on the former until everyone joins in the rush to get their share of cooperative gold.

Democratic coops should deliver more than for-profit banks. We need more Don Keis’s in the movement– people of goodwill who serve, who are pro-human and who knit together the fabric of society.

We need more Bailey-like credit unions that give, that contribute, and that cement communal stability.

Taking easy money is brutally hard on members.

It’s also hard on the soul.

This is the comment George would have written about the Vermont State Employees Credit Union merger proposal with New England FCU.

We all remember George Bailey from the holiday film classic set in the fictional Bedford Falls. Here is a quick synopsis from a writer who maintains the story is a dire warning about today. And perhaps the credit union movement?

It’s A Wonderful Life (Jared Brock)

For those who haven’t seen the movie — no judgment, but what are you doing with your life?! — it’s a story about an angel who is sent from heaven to help a desperately frustrated businessman by showing him what life would have been like if he had never existed.

But the B-story is a prophecy about the times in which we live.

George Bailey (played by the great Jimmy Stewart) runs the Bailey Bros Buildings and Loan Association, a company that contributes to the community by building affordable homes for owner-occupiers.

Henry F. Potter hates George’s guts. Rather than contribute to the town of Bedford Falls, Potter’s full-time job is extraction — he owns the bank, the bus lines, the department stores, and plays slumlord to a tenement called Potter’s Field.

While Potter dreams of bankrupting the Baileys so he can create a housing monopoly to milk the middle class to permanent poverty, George Bailey dreams of building “airfields, skyscrapers a hundred stories high, bridges a mile long.”

But George Bailey’s day-to-day goal is singular:

To help every working family own their own home.

Donald Kreis, a long-time credit union fan, responded to VSE’s proposal to end the credit union’s 75-year charter. His comment letter as filed with NCUA:

From the other side of the Connecticut River, the plan to merge the Vermont State Employees Credit Union (VSECU) out of existence seems like a bad idea, and I will be voting “no” on the proposal. Here is why.

Why I care about VSECU

VSECU – which I first joined when serving a judicial clerkship at the Vermont Supreme Court in 1997 – is one of the five credit unions to which I belong. I have only one rule when it comes to financial services: I don’t do business with banks, at least not voluntarily.

Investor-owned banks are in business to extract profits from their customers. I have always wanted to share my financial resources with my neighbors (or fellow employees), and I would like them to share their resources with me. A credit union is a financial institution that exists to help my neighbors and me do that, in a manner that we democratically control for our mutual benefit.

Thus, when I needed to buy my first car almost 40 years ago because my employer, Associated Press, was transferring me to a place (Portland, Maine) where I could not function without an automobile, I secured my first-ever loan from the AP Employees’ Credit Union. I was still a kid, fresh out of school, and not terribly desirable as a credit risk.

But a loan committee comprised of my fellow AP employees understood the need as well as the high likelihood that a young wire service newsperson would not renege on a promise to his colleagues. So, I got the loan.

Unfortunately, the AP credit union is long gone. Almost every credit union to which I have ever joined since then is indistinguishable from a bank. The neighbor-to-neighbor, colleague-to-colleague quality is gone. The organs of democracy have atrophied, and annual elections have become an empty formality.

There is only one exception, and it’s the Vermont State Employees Credit Union. Over the years, it has taken the idea of democratic member control seriously. It is the only credit union to which I have ever belonged that actively and enthusiastically promotes its annual election process.

What Beats Jet-Skis and Snowmobiles?

I don’t think it’s a coincidence that the VSECU is the only one of my five credit unions that actively promotes “green” lending. While other credit unions send me flyers and e-mails urging me to borrow money for leisure purposes (snowmobiles, jet-skis, extra cars), VSECU understands that what consumers really ought to be doing is borrowing money to make their homes both more energy efficient and self-sufficient.

This resonates profoundly for me, as the state official in New Hampshire (the Consumer Advocate) whose job is to advocate for the interests of residential ratepayers. Electricity and fuel prices are soaring right now, a result of our over-reliance on natural gas and other fossil fuels. But consumers are reluctant to borrow money to pay for things they can’t see, hold or drive around.

A credit union that is serious about the welfare of its member-owners will strive to educate them and encourage them to make long-term commitments to things that will make them wealthier and more secure over the long run.

The Case for the Merger – Platitudes and Generalities

Thus I was frankly shocked to learn earlier this year that the board of the VSECU had voted unanimously to merge our democracy-and-green-energy loving credit union into the much larger (and much more bank-like) New England Federal Credit Union (NEFCU). It seemed so out of character.

Naturally I assumed there were facts and circumstances of which I was unaware. When I inquired, I was told that to the extent I am entitled to information that would help inform my vote, the insights would be contained in the official document I then received. It is entitled “Notice of Special Meeting of the Members of Vermont State Employees Credit Union and Plan of Merger.”

The official Notice document does indeed make a compelling case for the merger – but only if you are willing to accept platitudes and generalities.

In the section of the Notice labeled “Reasons for merger,” VSECU states that “both credit unions are financially strong” but “face many of the same obstacles and challenges, including an aging Vermont population with slow to no growth; rapid and accelerated technology changes; environmental, economic and social change; and increased competition from out-of-state financial institutions.”

Fair enough, but this begs the question of what advantages the merger would confer as the new mega-CU seeks to confront those challenges. Answer: having swallowed up VSECU, the former NEFCU will be “better equipped to tackle the challenges facing financial institutions in a rural state.”

The Notice goes on to promise “economies of scale and combined resources” that will lead to unspecified “further improvement and opportunities” in eight listed areas – everything from “expanded branch and ATM access,” to “improved homeownership and financing initiatives to reduce energy consumption and environmental impact,” to “favorable rates and lower fees to members.”

These justifications are unpersuasive. Note the lack of promises or concrete examples of things that VSECU cannot simply do as a stand-alone billion-dollar credit union.

Economies of Scale and the CU Merger Frenzy

The “economies of scale” claim is especially troubling. The usual route to merger-related economies of scale is for the newer and bigger organization to trim staff to avoid duplication of effort. But in this instance the Notice promises that “all employees will keep their jobs and current salaries as part of the proposed merger.”

Economies of scale are indeed a ‘thing’ in the world of credit unions, but the proposed demise of the VSECU stands out. According to the trade publication Credit Union Times, the National Credit Union Administration (NCUA) approved no fewer than 86 credit union mergers during the first half of 2022 – overall, credit unions are stampeding to combine with one another – but the proposed VSECU deal is bigger than all but one of them. And in that biggest deal of the first half of 2022, VSECU’s New York counterpart – the $5.5 billion State Employees Credit Union – is taking over the smaller Cap Com Federal Credit Union.

Most of the credit union mergers in the current frenzy involve much smaller institutions. And, indeed, the consensus among industry insiders is that a credit union with less than $300 million in assets should indeed consider merging with another CU in the interest of amassing the resources to confront technological change and industry competition.

A $1.1 billion institution like VSECU already has, or already should have, all the economies of scale it needs.

Not a Merger of Equals-Equity Transfer

Although VSECU claims the proposed deal is not a takeover of our CU by the NEFCU, here is how you know that claim is wrong. If this were truly a merger of equals, then the members of both CUs would have to approve it. Because VSECU members are surrendering control of their financial institution, they and only they get to vote.

If you don’t believe me, consider what this deal would look like if both institutions were publicly traded, investor-owned businesses. The board of the ‘new’ credit union will have 11 members, six of which are from NEFCU. In the for-profit would, that would be considered a surrender of control – effectively, a takeover.

The $3 billion NEFCU intends to pay no consideration whatsoever to the current owners of the VSECU for the right to control what used to be their credit union. According to the latest 2021 balance sheet in the required Notice, VSECU members have built up $95.3 million in equity over the years – not a dime would be paid out to them in exchange for surrendering control of their credit union to its bigger and more bank-like Vermont competitor.

Such a payout would be easy enough to achieve by liquidating some of the $434 million in investments the combined credit union would have, above and beyond the $2.5 billion in loans on the books.

But, instead, the proponents of the merger are asking the members of the VSECU to surrender control of their credit union to a former competitor for free. No board of an investor-owned business would ever dare recommend such a proposal to its shareholders.

What’s at Stake? The Very Soul of the Credit Union Movement

In a sense, the impending vote on the takeover of VSECU should be seen as a referendum on the future of the U.S. credit union movement itself.

As I have already noted, VSECU stands out as a credit union that takes its cooperative identity seriously, along with its fidelity to the Cooperative Principles – the key principle being democratic member control. The New England Federal Credit Union is just another credit union that is content to operate like a bank does.

Why is this so important to me? After all, I no longer live in Vermont. I belong to four other credit unions and I even serve on the supervisory committee of one of them. So I could easily just sign and turn my back on VSECU.

I care about this because of something said to me by the CEO of the credit union on whose supervisory committee I serve. When I first met the CEO, I told him about how much democratic member control, and the other six Cooperative Principles, meant to me as a volunteer credit union leader.

In response, the CEO pulled out a cell phone and waved it in my face. The CEO mentioned an adult daughter – this executive’s go-to proxy for a typical credit union member. “Do you know what she cares about?,” asked the CEO. “It’s not voting. It’s this.”

The “this” to which the CEO was referring was the credit union’s phone app that allows members to do their banking from the device they carry around with them in their pockets and purses.

If that’s truly what all of this comes down to, then I give up and so should everyone else in the credit union movement. Credit unions can and should strive to keep up with the convenience-enabling technology deployed by the mega-banks.

But if credit unions can’t deliver value to members above and beyond the convenience that for-profit financial institutions already offer, there is no reason for them to exist.

In other words, if the $1.1 billion Vermont State Employees Credit Union cannot stand alone, cannot be just as convenient as a bank while giving members more value and more control than a for-profit financial institution can, then combining with another credit union is a waste of time. Instead, the Board of VSECU should just pay out that $95 million in member equity and turn over its loan portfolio, its deposits, and its checking accounts to some ultra-convenient bank.

Do Not Succumb to Cynicism and Fear

Indeed, maybe we no longer deserve VSECU as we have come to know and love it. Maybe we are unworthy of a democratically controlled financial institution.

When VSECU first announced the merger, and the skeptics began speaking out, the Board and management circled the wagons instead of treating member activism the way it deserves to be treated – as a welcome expression of commitment to the institution they collectively own.

In that sense, the leaders of VSECU are no different than the board and management of every other cooperative that has had to deal with members who flex their ‘democratic control’ muscles and question their elected representatives.

Maybe it’s just human nature – but, if so, then maybe “democratic member control,” and other Cooperative Principles like “education, training, and information” (which suggests members should be fully informed about the business realities their cooperatives confront), are just outdated platitudes.

We live in cynical times. So, it is not surprising that, even in Vermont, both the proponents and the opponents of the buy-out of VSECU by a bigger credit union question the motives and integrity of the other side in this discussion. I refuse to succumb to that cynicism.

Thus, I am grateful to the VSECU Board of Directors for presenting this proposed merger to us for a vote, and for making its best case for why we should ratify the deal. They, in turn, should understand my frustration over not having access to all of the information they had at their disposal as they deliberated.

Lacking that information, or any other compelling reason to vote in favor of consigning the Vermont State Employees Credit Union and all it stands for to oblivion, I vote “no.” I urge my fellow VSECU members to do likewise, in the hope that the VSECU of the future will look less like a bank and more like a cooperative.

If this credit union, with its commitment to cooperative culture and public service, cannot survive and thrive as an independent, community-owned, democratically controlled financial institution, then all is lost. I refuse to believe that.

END

He has served since 2016 as New Hampshire’s Consumer Advocate, heading up a small but feisty state agency whose purpose is to advocate on behalf of the interests of residential utility customers before the state’s PUC and other bodies (including FERC). Previously he served as general counsel at the New Hampshire PUC, as a hearing officer at the Vermont PUC, and as a professor at Vermont Law School, where he still teaches on a part-time adjunct basis.

Prior to becoming a lawyer, he was a full time journalist for nearly a decade, first with Associated Press and then at the fabled newsweekly Maine Times.

He served for eleven years on the board of the nation’s second biggest retail food co-op (the Hanover Consumer Cooperative Society) including three years as president. He was a nine-year trustee of what is now known as the Cooperative Fund of the Northeast, a CDFI that loans money to cooperatives.

He believes credit unions ought to live by the cooperative principles – and take democratic member control seriously.

His custom when joining a new credit union is to follow up about a week later with a request for the CU’s bylaws and express interest in seeking election to the board. That has inevitably been met with something on the continuum between bewilderment and hostility, except at the CU that invited him to join its ALCO and Supervisory committees.

Early Saturday morning December 8th, 1984 Bucky Sebastian and Mary Beth Doyle, two NCUA colleagues, came by to give me a ride to Dulles Airport. We were going to Las Vegas for the largest credit union conference ever.

All state and federal examiners were together initially, then joined by over 2,000 credit union folk. It was a big deal, a capstone event, for celebrating a new era of credit union success.

Mary Ann had asked her mother, Barbara Ballmer, to come and help out with our two teenagers for the week I would be away. She got up, made breakfast and talked with Bucky and Mary Beth when they stopped in.

Late that night, December 9th, the phone woke me in my Las Vegas hotel room. Mary Ann had died at Sibley hospital. Her 4 ½ year battle with breast cancer was over.

We never talked about death. I felt that was like giving in to the struggle. She knew how sick she was, but never complained. Her dad was a doctor. He died before I knew Mary Ann. He had sent her away when his cancer was near the end.

Twenty years earlier, in April 1964, she wrote him when learning of his situation: “Pop, take care of yourself and keep your chin up. Cancer seems like a dreadful thing, but I maintain if there is a will, there is a way. I know you won’t let this get you down if you can possible help it.

I admire you and love you not only because you are my father but because of everything you have done and that you stand for. My ultimate goal in life is to be able to live up to all that you have taught me and do and contribute in my own way as you are doing in yours.” And she did.

In her own quiet way Mary Ann had prepared us for this event. All the Christmas shopping and wrapping was done. The new bikes for the girls were hidden in the garage. Presents had been sent to my parents, her sister and brother, and great grandma Filson. She had baked a half dozen of her favorite dark molasses fruit cake, wrapped the loaves in cheese cloth with rum, to age until they could be given as gifts.

Lara had just made the varsity basketball team as a freshman in high school. Alix was doing morning swim workouts and playing piano and singing in chorus. Both had run in the YMCA’s Thanksgiving Turkey trot. We watched.

The Christmas tree was up with stockings on the fireplace mantel. The new wallpaper in the hallway was finished and the laundry room cleaned and painted. Her Japanese inspired garden in the back yard was planted to have some color all year round. This was the time for the very deep red finger leaf maple and red berries on the nandina.

Signs and sounds of the season were all around. I was upset the world went on as normal when I just felt a deep black hole. Only later did I learn that Ed Callahan, NCUA Chairman, had opened the national conference with a moment of silence for Mary Ann.

One conversation I remember that December night was talking on the phone with Lara who assured me that everything was OK. Mary Ann, she said, was with her Father.

The first of two Memorial services was December 17th at Chevy Chase Presbyterian Church. The second was in Wilmette, from where we moved to Bethesda three years earlier. The minister at both was Wally Moore who had known the Ballmer family when he was in Midland, MI and had gone to McCormick Seminary with my dad. He was the minister at First Presbyterian when we walked into the Wilmette church in the winter of 1974. His life had been intwined with both of our families.

He described Mary Ann’s unique skill of creating order and beauty in all aspects of living, including house and garden. He talked of her deep relationships forged out of concern meeting need. A person described her as one of “God’s green thumbs” who even though when life was ebbing away, could reach out to others and affirm life in them.

In the mid summer of 1983 or ’84, a stranger came to our door. He was a young French student traveling around America as a tourist. His local contact for the Washington area had been lost. All his belongings were in his backpack.

Mary Ann invited him in. We shared our meals, helped with errands as he rested up. He continued on several days later. That fall when he returned to France he wrote Mary Ann several letters about his journey, what he was doing now, and thanks.

Wally Moore closed his remarks saying, Mary Ann understood mercy, compassion and forgiveness. . .qualities which make it possible for us to believe. In Advent, we ask what will our blessing be? We will be blessed by that blessing which Mary Ann received and in which she believed—that the only gift we have to give in this world is ourselves.

Mary Ann and I lived in three countries prior to settling down in America.

She got a job at Dow Chemical, in London, so she could be near when I was at Oxford. She is at the National Gallery on Trafalgar Square in this 1967 photo.

We moved to Japan when I was assigned to USS Windham County, LST-1170, home ported at Yokosuka Naval base. She took the two children to play on the beach in Hayama where we lived the first 15 months with a Japanese family’s quarters while I was deployed. That’s Mt Fuji in the background hovering like a cloud.

That three years was followed by another sojourn in Sydney, Australia where I worked for the First National Bank of Chicago. Here they feed a joey, young kangaroo.

She made a home in every country in which we lived filled with lasting friendships.

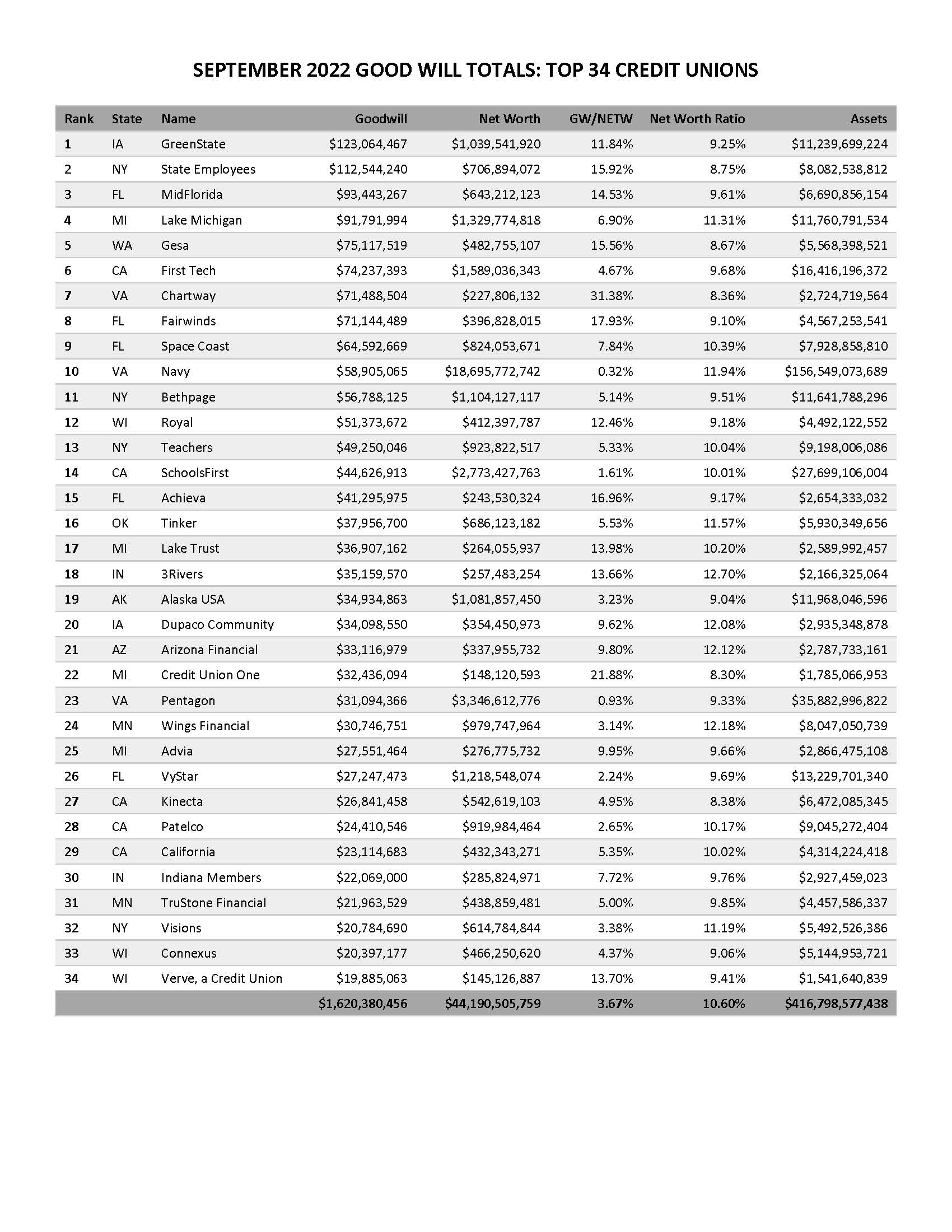

In this second blog I look at examples of goodwill. What are some of the financial and regulatory implications of this ever increasing intangible asset?

The following are the 34 credit unions (out of 277) with the largest amounts of good will at September 30, 2022.

The goodwill net worth ratio, column three, compares the size of this intangible asset to net worth. This ratio ranges from a high of 31% for Chartway to a low of .32% for Navy FCU. There is no regulatory limit on how high this percentage can be.

The goodwill net worth ratio, column three, compares the size of this intangible asset to net worth. This ratio ranges from a high of 31% for Chartway to a low of .32% for Navy FCU. There is no regulatory limit on how high this percentage can be.

While I do not know the details of every credit union listed, most of these goodwill leaders occur from either whole bank purchases or mergers with other credit unions. The first two names, GreenState and State Employees (NY) are examples of each activity.

As discussed in Part I goodwill is an intangible asset representing future economic benefits arising from assets acquired in a business combination, traditionally mergers or purchases.

It is not part of equity or retained earnings from a presentation standpoint.

Goodwill lacks physical substance. It is an accounting estimate based on assumptions used to project potential future value. Unlike mortgage servicing assets which are also an intangible, goodwill can’t be bought or sold.

If credit union A merges with credit union B which has goodwill on its books, credit union A receives no benefit. Credit union B’s goodwill is devalued to zero. It is not carried over onto credit union A’s books.

As the underlying benefits are realized, impairments to goodwill can be recorded. A credit union can also amortize goodwill over ten years. In both instances those charges flow through the income statement and reduce retained earnings.

In either option, all goodwill must be assessed for impairment at least annually.

For credit unions following CCULR: Goodwill is not part of Net Worth (numerator) for ratio purposes but is included in total assets (denominator) to determine the net worth ratio (NWR). Goodwill balances must be less than 2% of total assets to opt into CCULR.

For credit unions subject to RBC: Goodwill is a reduction from the RBC Numerator and also from the Denominator.

In corporate America public companies report over $4 trillion of goodwill on balance sheets, primarily from mergers and acquisitions.

While accountants agree on what goodwill is, how to value that goodwill after it’s passed onto the buyer’s ledger sparks plenty of argument.

There is much uncertainty about forecasting goodwill’s future benefit for a firm – it involves more judgement calls than many accountants are comfortable with. And while goodwill is listed as an asset on the balance sheet, is it really worth its stated value? What if it was a bad buy at an inflated price in the first place?

In June 2022 FASB announced it had given up on a four-year effort to simplify goodwill accounting determinations. The current annual impairment test remains the requirement versus a straight line annual amortization approach.

When creating goodwill, credit unions have all of the same accounting challenges as public companies but none of the checks and balances .

The ongoing difficulty is assessing post acquisition performance to see if it is meeting the values projected when the goodwill was first established.

In cooperatives this is made much more difficult because in both mergers and acquisitions, there is virtually no public disclosure of an acquisition’s costs let alone future projections.

For purchases, credit unions rarely report the total price paid(except when a bank is publicly traded) the broker and transaction fees, the future impact on ROI or ROE and the longer term performance goals to be achieved. For mergers, no details of a combined operational plan are provided just the asserted advantage of bigger size and more capital.

Most large mergers and whole bank purchases take years for operational and business integration to be fully realized. These transactions generally end relationships and market presence created from years of continuous service. That history and local advantage is now gone.

In some large credit union mergers a whole new corporate brand and identity are part of the combined entity’s future business plan. Shedding past connections to create a whole new market persona would seem to undermine a valuable legacy.

Credit union mergers and bank purchases are not market based transactions. They are private deals negotiated for mutual advantage by CEO’s and then announced to members. Because there is no transparency or numbers provided, little future monitoring possible.

Both transactions create goodwill but the credit union is playing with members’ house money. If the deal works out after three or four years, whatever benefits of expansion have been achieved are trumpeted as the result. If the bank purchase was overpaid, there is no stock price or performance metric that would highlight this misjudgment.

The bank owners are paid a cash premium for their shares from the members’ savings. They have left with cash in hand. If a transaction is poorly priced or managed, then the goodwill is written down from members’ existing capital.

The goodwill concept allows managers to pay premiums for purchases absent any performance goals. In a merger, goodwill in excess of book net worth just enhances the ongoing credit union’s capital but members receive nil for this value.

When leaders operate in a closed environment, unconstrained by member or board governance, personal ambition can run amok.

With no meaningful credit union disclosures to members or the public in either mergers or bank purchases, managers are free to wheel and deal. A number of CEO’s have been very public about their “nonorganic” growth plans. Goodwill is the intangible asset created to make things appear OK regardless of price or terms.

The animal spirits of capitalism are quickly embraced versus the cooperative focus on members’ well being. But unlike truly competitive markets, there is no stock price or market assessments monitoring performance.

When goodwill accounts begin to approach 10% or higher of net worth, the credit union has disguised its ability to produce operating earnings. To keep the game going, more purchases and goodwill are pursued, always justified by scale and more diversification.

At some point the economy turns, the acquired assets become overvalued and members are given the short stick as dividends are reduced to keep up the ROA goals. In several of the credit unions listed dividend payments were reduced in 2022 versus 2021 to sustain ROA even though short term rates have risen by over 3%.

Staff layoffs are another indication of overcommitments. Examiners or accountants will start to question the goodwill asset’s value.

The goodwill that underwrites cooperatives can quickly turn to ill-will. When members realize their collective legacy in mergers was transferred to solely benefit senior managers, the loss of confidence will undermine both the new entity and the cooperative system’s reputation for fair dealing.

When the out of state or out of market bank purchase shows no growth, the tactic of buying market share begins to fail.

The facade of goodwill falls away for both the credit union and the members. Once gone, it is lost forever. That is what intangible means.

Tis the season for evoking goodwill. Company/organizational holiday parties, the daily mail full of greeting cards, Giving Tuesday, community food drives and dozens of other personal and firm initiatives make Advent a time of joy.

Wonderful and colorful decorations enhance this sense of a special time of year. Sporting events promote opportunities to help others. Even if there is constant hurry up, it is a toward good ends.

Concerts and carols bring back familiar lifelong memories. There is even a heavenly musical declaration of good will in music.

This most dramatic announcement is in the Messiah’s fourth chorus, Glory to God. As described in Luke 2 v.14, the heavenly hosts sing to shepherds of Jesus’ birth: Glory to God . . . and peace on earth. This opening is followed by repeated proclamations of “Goodwill towards men.”

Angels celebrating a new era in words repeated still today.

Goodwill is not limited to this holiday season. In everyday usage, goodwill is the feeling of trust, loyalty and support that emerge from a relationship or event. It is the bond greater than any underlying transaction. It is much more than a feeling of satisfaction.

Rex Johnson, the credit union lending guru, described this as the art of converting members to fans, not just spectators.

For cooperatives, goodwill is an essential component of their market advantage. It is rooted in members’ belief that the credit union acts in their best interest. It is embedded in cooperative design. Current generations expect the fruits of their loyalty will be passed to future ones.

When active, goodwill underwrites member relationships giving credit unions a competitive standing no other firm can match. Although real, it shows up nowhere in a credit unions ordinary financial reports.

There is also an accounting term, goodwill. It is an intangible asset. It arises when a credit union acquires a bank or merges with another credit union. The excess of book value over fair market value of the net assets gained, creates accounting goodwill.

Credit union accounting goodwill has grown dramatically. The first reported total as of March 2009 was $160 million. At September 2022, the total was $2.2 billion recorded in 277 credit unions. Since that initial March date, it has grown at an annual rate of 21%.

Goodwill is only 2.2% of these 277 credit union’s net worth. But in some cases it is much higher: 31% of Chartway’s and 21% of Lake Michigan credit unions’ total capital.

Goodwill is classified as an asset because it provides an ongoing revenue generation benefit that extends beyond one year. It may include such items as customer relationships, liabilities (shares) acquired at below market rates, corporate expertise, operating (FOM) authorities, or proprietary technology.

Goodwill is recognized only through an acquisition. Unlike member relationships, it cannot be self-created. It is the excess of the “purchase consideration.”

Negative goodwill arises if the acquired assets are purchased at a discount to their fair market value (FMV) and is referred to as a “bargain purchase.”

A description of goodwill accounting and how it works is at this site.

Since December 2018 the total of accounting good will has doubled to the present $2.2 billion. The reasons are two: premiums paid on whole bank purchases and mergers with credit unions uncovering significantly understated value.

An example of the premiums on whole bank purchases is GreenState which reported $123 million (12% of its net worth) as goodwill. The second highest is State Employees in Albany at $112.5 million (16% of net worth) as a result of its merger with Capital Communications.

Because accounting goodwill is an intangible asset, there are numerous issues about how it is considered in net worth calculations, its amortization, and its role in financial decisions.

Tomorrow I will look at the largest reported individual goodwill totals, NCUA’s view of the asset and how it could change the future of the cooperative system.

The following are excerpts from two CEO November reports to their employees with examples of credit unions acting . . . like credit unions.

From Day Air: Heidi and the Accounting area started with 95 dormant accounts with balances totaling $279,000 and worked those numbers down significantly to keep member money from being turned over to the State of Ohio in compliance with escheatment laws. Most of those members were located so balances of only $26,000 from 35 accounts are being remitted to the State.

From Weokie’s Vice President, Operational Support:

We had a deceased account that was up for escheatment, and I noticed that there was a beneficiary, Nick, listed but that we had never heard from him.

I asked Paula about this and all we had was return mail for this person. I noticed an old cell phone listed on the card and suggested we call as most people don’t usually change a cell number, even if moving out of state.

Paula called, left a message, and the beneficiary returned her call the same day. He was still in the same apartment building in New York but had changed apartments.

After confirming we had the man we were looking for, Nick began to tell Paula that he had been adopted and never really accepted by his extended family (cousins, aunts, uncles) but did have one aunt and uncle that were always very kind to him.

Long story short, Nick will now be receiving just over $436,000 that he was not expecting.

Most of time when we escheat there is not much money but when I saw this account with $436k, I could not see letting this go so easily.

To me, $436,000 is life changing money and so happy that this money will be paid out as our deceased member had wished.

One of our primary value propositions is that we’re local. We’re Dayton area people helping our friends and neighbors in the Miami Valley with their finances. It’s easy for people to be attracted to fintechs and Internet banks, but when you have a problem being local can be all the difference.

I just heard a story of someone who was using Chime, had a problem and couldn’t get the issue resolved. Of course, Chime doesn’t have any local offices – just a website and an 800 number.

Here at Day Air, we’re human and so make mistakes. The difference is that we’re local, we’re here to help our friends and neighbors, we’ll address the situation and make it right.

Day Air’s Selected market updates for staff::

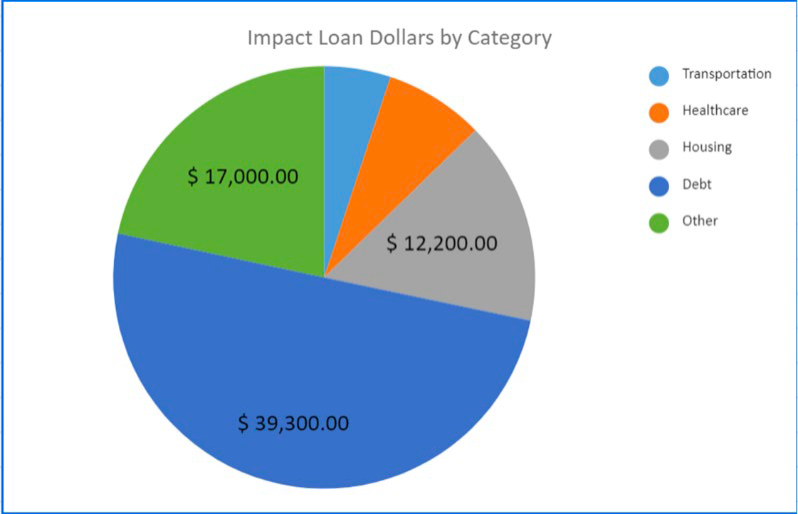

We hit another milestone in November as the credit union has now contributed $125,000 to the Community Impact Fund to support our zero-interest loan program for members of Team WEOKIE who have found themselves in financially stressed positions.

We have granted $89,161in loans with $43,576 having been already repaid and making these funds available to be re-loaned to other team members who find themselves in financial difficulty.

A chart showed how the $89,000 in loans has helped employees.

After the Gettysburg Address, the most memorized speech in high school is Martin Luther King’s I have a Dream speech.

Dreams drive human aspiration. The inspire political and social movements. America is a land built on the hopes of a better life by the millions seeking this land of opportunity.

Many a credit union purpose statement includes the goal of helping members achieve their dreams. At their best, cooperatives nurture communities that uplift each other.

Dreams also become entwined with human ambition. In a competitive market-driven economy, it is inevitable that some will be captured by the impulse to grow and dominate.

Patient organic increase, member by member, is not fast enough. I have described examples of PenFed’s over two dozen mergers of successful, long-serving credit unions that have nothing to do with its prior market or roots. These mergers are incentivized with staff payouts followed by layoffs and ultimately the ending of local presence in exchange for virtual, digital service.

GreenState in Iowa is one of the highest performing credit unions in the country. But that record was not enough. They have pursued three or four whole bank purchases outside their home state to achieve even faster growth.

It is no accident that when the economy turned and the real estate markets and rise in rates created headwinds, these were two of the first institutions to announce staff layoffs.

Sometimes dreams come at the expense of others. At some point, ambition distorts dreams. Survival dominates decisions.

Chasing dreams of a bigger, commanding future has resulted in some leaders overlooking the incredible success that was right in front of them. That oversight is the danger every CEO and board will face.

The risk of this loss of perspective about the value of what has been created can be acute with new leaders. The push and pull between past success and future direction can be traumatic. One observer has described this tension as follows:

“One side says do MORE – more TACTICS, for MORE people, for MORE communities, etc.

One side says do the same.

Now doing the same is more – more of the right things, for right reasons, and for the right people. But it sounds like less – people, especially people not vested in the “right” things intuitively chose more, new, often along the lines of the competition.

Professionals are easily swayed toward competitive calculations based on just MORE and peer trends and ideas that serve professionals.

Therefore cooperatives are a niche easily outgrown and defeated as missions wane, as purpose grays, retires and dreams end.”

Examples of both positions are abundant in credit unions today. The test of any system, especially one that claims to be democratic, is whether we can discuss what troubles us. The founding generations will continue to move on with their dreams.

Cooperative success is more than management tactics. The good news is that it only takes a few leaders dedicated to this unique approach to member well-being to preserve the ideals, not just the balance sheets, they inherited.

“Forgive us our debts, as we forgive our debtors.” We say these words in the Lord’s prayer. Where have we seen this ever done in “real” life?

Society, especially market-based ones, do not practice debt forgiveness. Capitalism is built on finance, i.e. all kinds of debt—corporate, consumer and government.

In the bible, the Jubilee year – occurring after every seventh Sabbath year, thus, every 50 years is an economic, cultural, environmental and communal reset, when the land and people rest, and all those who are in slavery are set free to return to their communities. (Leviticus 25:1-13).

Debtor’s prison or indentured servitude, was a reality in England and other countries for those who failed to pay up. It was the basis of more than one of Dicken’s novels. Scrooge is more than a Christmas story. It was reality.

President Biden’s forgiveness of either $10,000 or $20,000 in student debt has been met with gratitude by millions of former students who have applied for this reduction.

On the other hand, multiple organizations and opponents have taken to the courts to stop the plan absent Congressional approval. The question of whether the President has the authority to do this unilaterally is now before the courts.

Some former students who paid off their loans, feel this action is unfair to those who honored their obligations.

Credit unions were founded to provide debt. Credit for members funded by savers. Often the phrase “for provident and productive purposes” is intended to show debt as a positive event.

Founding stories such as that at BECU where a small group employees contributed 50 cents each in 1935 to create Covenant credit union to provide tool loans during the depression, are apocryphal.

Credit unions spend much effort and processes to make sound loans, track delinquency and minimize loan losses.

But debt forgiveness? That is rare indeed. Recently this video by Canvas Credit Union shows the power of debt forgiveness. Addie Greenacre, a long-time Canvas member, wife and mother was surprised with a $40,000 loan payoff as part of a drawing during an auto refinance promotion.

It is a powerful example of what removing the burden of debt can mean to a person.

(https://www.linkedin.com/company/canvasfamily/videos/)

How do credit unions founded to provide debt ensure that loans lift up and don’t become a lifelong burden?

Looking at the Canvas Credit Union model one sees an organization dedicated to financial well-being. In their words, We’re here to Help You Afford Life.

While this “debt forgiveness” may have been a promotion, it demonstrates the power of jubilee thinking for people, and a community.

As credit unions review their personal loan portfolio at yearend, seeking those with the longest tenure or constantly rolling over draws, might a debt jubilee be a timely addition to every credit union’s service profile?

It can literally change a person’s life. Isn’t that what credit unions were meant to do?