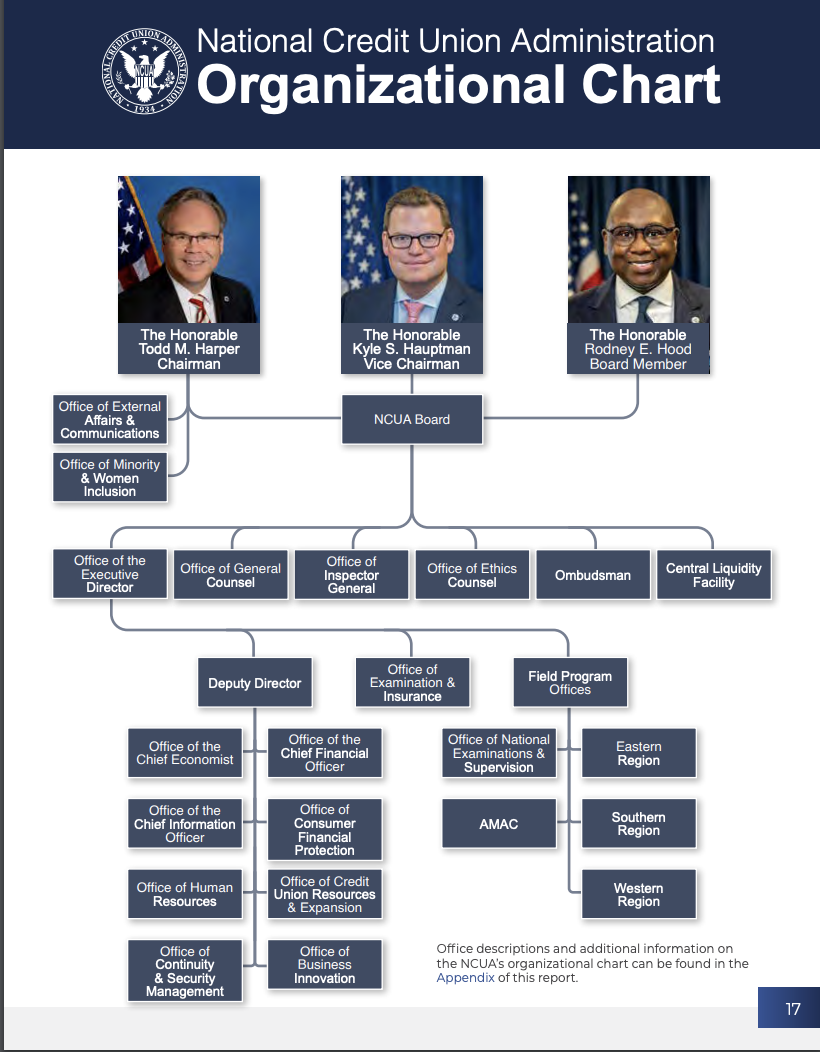

1982 was a consequential year for NCUA, credit unions and the future of the cooperative system. The Penn Sq bank failure occurred in July. The NCUA board approved the total deregulation of shares in April, and there were multiple credit unions with 208 assistance trying to turn around. The agency’s new leadership implemented a complete reorganization to become more effective.

NCUA’s 1982 Annual Report described these events and Chairman Callahan’s explanation for the redesign of the agency’s structure.

“The third area I want to report to you is decentralization because I think that ties in with regulation. We had a very strong Central office, a very talented Central office and one that was developed over time for a very good reason.

As I viewed it, it had become so talented and strong that the very mundane operational things that our field people tried to do got caught up in this pipeline—this pipeline of talent and centralization in Washington.

Seldom did things come out in a very efficient manner. Everyone was overdoing their job so we found that decentralization was the answer.

We found it necessary to cut the size of the Washington office by a third, to re-channel these resources to the field and to delegate to the regional directors the responsibility of using these resources in a timely way to get the exam cycle down to an annual one, to give backup and information to the field examiners, and to make those decisions on-site that involve safety and soundness, chartering, and supervision.”

The most important decision in the Agency’s management of its personnel was to reverse a five-year trend of increasing numbers of personnel in the Washington office and to reallocate. positions and personnel to the field. (Page 43)

More Growth-Limited Office Time

Today NCUA’s central office continues to expand in numbers and new departments. The budget continues to increase as the number of credit unions falls. Moreover even with the Covid emergency over, the agency requires D.C. personnel to be in-office only two days per pay period.

Is now time to reevaluate NCUA’s organizational trends? And accountabilities?

Many companies, non-profits, and other civic organizations including credit unions are adjusting their corporate structures. News reports of layoffs are daily events. One analysis in particular caught my attention about the reasons for Google’s layoffs. Here is an excerpt with examples very similar to patterns in DC:

A lot of tech workers were hired to do nothing: I’m not happy about anyone losing a job. But among the tens of thousands laid off from big tech companies, some people are coming out to admit that they did literally nothing at their jobs. . .

Meanwhile, now that bosses are accustomed to all their mid-level remote employees who never come to the office, they’re realizing that the jobs can actually be super remote, like maybe in Bangladesh.

In order to get promoted to senior levels (starting from director up) your organization needs to look a certain way. There are boxes you have to tick including having the right people at the right levels underneath you.

The long term approach to this would be to grow your people and that this will naturally happen if you’re working on things that matter. The trouble is that this takes time and you’re never more than 6–18 months away from a potential reorg that might make you start again from scratch. Ambitious people also tend to be impatient. So, what do you do?

You start vanity projects and hire. You hire in people at the right job levels so your organization has the “right” shape to it. You chase after vanity metrics about you looking good like active users rather than how useful your product is. You use your authority to subvert the promotion process so that your promo candidates get through even if they don’t deserve it.

You avoid performance managing people out because every headcount matters in your quest to make the next jump. You step back from confronting your peers over toxic behavior because you need their support for promotion. Eventually your cargo cult gets you where you want to go.

Another reason that Google is wasteful is that it’s too easy. The people inside it don’t see it as a business as they don’t have to struggle against the market forces everyone else has to deal with. Why would you when ads is so profitable?

This complacency means senior leaders often follow their personal agendas above all else. Empires rise and fall. Too often I saw that personal ambition trump doing the right thing for users, the business or employees.

The root cause is the leadership because it’s their personal ambition over running their part of Google like a business. I’ve seen people promoted to VP based on a set or vague promises they haven’t delivered, mass hiring and vanity metrics. Google can go to great lengths to protect people in senior leadership positions way beyond what they would do for the rank and file.

Et Tu NCUA?