Christmas is a time when we remember, honor and celebrate people whose life was the gift of service to others.

Credit unions attract and provide fertile ground for persons with this character. They create an ideal platform for assisting others at important junctures in their lives.

These individuals’ efforts are not measured solely by numbers; more important is the personal legacy of bringing “soul” to their work in the movement.

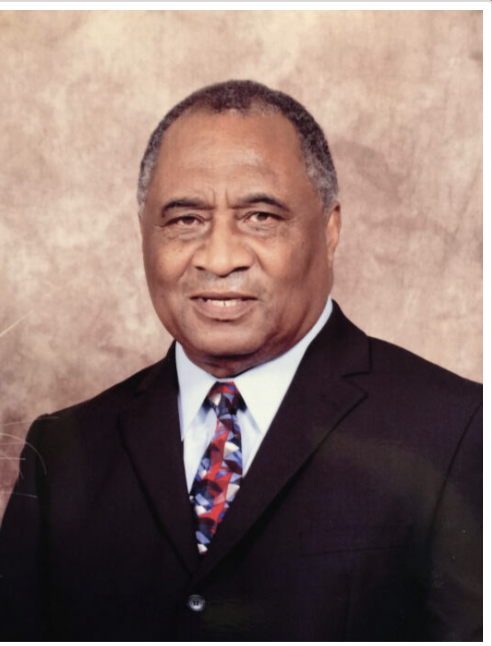

The following tribute to a long-serving credit union employee is by Jim Blaine.

James McArthur Williams (1943-2023)

Why do we so often become confused when taking the measure of greatness? Why are we so easily distracted – and dazzled – by the spectacle, the swank, and the swagger? Why do we so often miss who is truly important – and what really makes a difference in each of our lives?

Had the privilege of attending the funeral of a great man last week at St. Paul A.M.E. Church in downtown Raleigh. James Williams was a beloved husband, father, grandfather, brother, cousin, and friend. He married his high school sweetheart Ginger; he called her “Bread“. They had two children – JaSonne Yvette and James Eric.

James Williams was a veteran, 33rd degree Mason, Emeritus Board Steward in his church, graduate – and beyond ardent supporter – of his HBCU, “THE” North Carolina Central University – “Go War Eagles!“. James was a devoted family man at heart, loved traveling, and as an empty-nester, cruising with Ginger. A full life – important, meaningful.

James Williams came to work at the State Employees’ Credit Union in 1973. That was 50 years ago. That seems like a long, long time ago. Much has changed in that time, much hasn’t.

James McArthur Williams was the first Black employee to work at SECU. He faced some unusual challenges, not of his making. But he persevered, he persisted. James Williams was a senior lender at SECU for over a quarter of a century. No individual was more important in building the reputation for integrity and fairness at State Employees’ Credit Union than James McArthur Williams. With humor, grace, and kindness, James Williams navigated all the “historical difficulties”; he left a positive mark on all he touched; because he knew how you felt – he had walked in your shoes.

Thank you, James Williams, for helping me and many, many others to understand better.

Can an organization have a soul? As a faithful “soul man”, James McArthur Williams spent a lifetime showing us there is a path…

Can you measure greatness in people and in institutions? Here is what SECU members say:

“James will long be remembered as a person who showed many of us how to overcome obstacles in the world of finance. He demystified bank forms and protocols. And most importantly, he always encouraged patrons of SECU as we realized with God all things are possible!”

“James was our greatest ally at the State Employees’ Credit Union.”

“James and Ginger are two of the warmest people you’d ever want to meet. Many state employees knew James through the State Employees Credit Union in downtown Raleigh.”

After a public hearing, multiple written comments and some give and take between board members, these are some of my initial observations from last Thursday’s board meeting on the 2024 Agency Budget.

Only .02% of 1% was reduced in the final budget of $385.7 million by the board from the initial staff amount.

No discussion of why the Office of Information Serves (i.e. computer support) depends on contractors for 71% of its operations totalling $44.5 million.

A 16.4% in the federal credit union operating fee when the Operating Fund’s cash on hand now would almost cover a full year’s expenses. Or why the $24 million “carry forward” from 2023 (unspent amounts collected) is not returned to credit unions, but “reallocated” to 2024.

Why only four new charters justifies a 18% increase and 41 staff in the office of Credit Union Resources and Expansion(CURE); also when the industry’s total numbers declined by almost 170 credit unions.

Most curious was the increases in staff to a total of 23 and 20% budget raise to $6.4 million in the Asset Management and Assistance center when the total reported losses to date in the NCUSIF are just $1.0 million. The remaining corporate AME’s are to be disbursed soon. The office is spends more on staff than on the assets it oversees.

The CLF’s $2.2 million budget is nothing more than an effort to transfer NCUA’s overhead expenses to another set of books which credit unions fund separately. The CLF’s 4.62% third quarter dividend was at least .75% below what credit unions could earn in the overnight market, meaning NCUA requires members to subsidize this inert operation.

There are multiple other expenditures that appear with no specific goals or outcomes. The board discussions were general observations. Credit unions deserve more coherent and specific details to have confidence in how their funds are used.

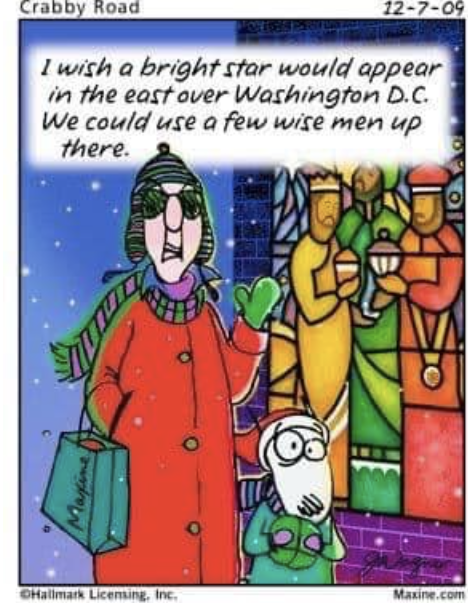

In the spirit of the season, this cartoon caught my eye. It summarizes NCUA’s budget review from a credit union perspective.

December’s NCUA board meeting will set the spending budget for 2024. What will be the guiding star in the voting, to borrow words from yesterday’s post We Three Kings?

Is the guiding star one that illuminates the unique design and resilience of cooperatives? Or will it enhance bureaucrat resources as the number of credit unions falls to its lowest level since before the passage of the 1934 FCU Act?

Rodney Hood’s Credit Union Service

Hood has served as an NCUA board member during three tumultuous financial decades. The first (November 2005-August 2009) saw the Great Financial crisis unfold. The second from April 2019 included the Covid national economic shutdown and the highest inflation since the 1980’s.

This meeting may be his final one as his current term ended in August. His two tenures over 18 years provide a unique perspective on the board. He brings a shared history of an important era for the cooperative system.

We can only understand and celebrate the present when we appreciate how it came to be. In the words of historian David McCullough, “history is who we are and why we are the way we are.”

Hood’s Focus as a Board Member

Relevant for today’s meeting is his support for the long time, traditional NOL cap on the NCUSIF of 1.3%, full transparency for all financial calculations including reserves, and most urgently, a more meaningful presentation of the fund’s equity ratio using current data in both the numerator (the 1% deposit) and denominator (insured risk.)

As chairman he oversaw the only year in NCUA history since 1984 that recorded an actual fall in NCUA’s expenditures. He has supported returning to credit unions the increasing surplus cash built up in the Operating Fund.

Another example of his expense focus is that his office is the only one of over 25 NCUA budgets to request a lower amount in 2024, by 1.8%, versus the current spending level. NCUA’s 2024 overall operating budget projects an 11% growth.

An Honorable Gentleman

The first time I met Rodney was at a credit union meeting in New York during the emerging financial crisis. He was and still is a true gentle man, unfailingly polite and easy to talk to.

His manner at NCUA board meetings is always respectful. Even when staff’s answers to his questions might be non-responsive, he never publicly challenged the presenter.

In his voting, he rarely dissents even when he disagrees with the motion or policy. He would explain his vote as either deference to the Chairman’s role or to promote bipartisanship. These acts of corporate courtesy were not the practice when he was chair.

As a board member in 2008 he approved an NCUSIF dividend when the NOL exceeded 1.3%. That was the last time a dividend was paid. This is a legal commitment intended to reward credit union’s perpetual 1% deposit underwriting. Last year he succeeded in urging the board to reduce the cash stockpile in the operating fund by giving credit on the FCU operating fee for 2023.

His approach to budgeting and board decisions to set meaningful agency guardrails reflects the experience and wisdom of his years of credit union service.

Should this be his last official board meeting, his perspective will be missed. As Pearl Buck’s observed “if you want to understand today you have to know yesterday.”

In recent Board meetings, Rodney has tried to raise important issues and seek meaningful data. What might he propose today to recognize credit union’s exceptional performance this year? Tune in at NCUA.gov at 10:00.

The Question in The Three Ships Carol

To recognize the pivotal nature of today’s many board votes, I believe the lyrics of the carol I Saw Three Ships are most relevant.

Here are some pertinent stanzas:

I saw three ships come sailing in On Christmas Day, on Christmas Day I saw three ships come sailing in On Christmas Day in the morning

And what was in those ships all three On Christmas Day, on Christmas Day? And what was in those ships all three On Christmas Day in the morning?

Tomorrow is the last NCUA open board meeting this year. And possibly Rodney Hood’s final one.

This is the most important Board event as it sets the spending limits for the agency all of whose funding is from credit unions.

The key question is whether the public will learn anything about the board’s ability to limit the staff’s desire for ever more spending? Has all the deal making been completed and the questions and answers fully scripted out, or will real board dialogue actually occur?

The meeting is critical because decisions are made about the NCUSIF’s normal operating level (NOL), the overhead transfer rate(OTR), and how the agency will be funding itself from FCU’s operating fee. Each of these directly affects credit union’s funding.

Budget Questions for 2024

Some of the issues that might be asked include the following;

Why does the “missions support” functions in the 19 DC offices need a 17.4% and 19 person staff increase, whereas the examination and field staff, the front line workers, gain only a 5% and 9 person increase? Where does the real work of supervision take place?

How is it that the highest paid staff in the nineteen DC offices are those in the 8-person Chief Economist with annual compensation of $329,000 each ?

Are two completely separate legal offices needed, one the 46-person general counsel’s office and the second the 8-person staff for business ethics?

Numerous other personnel additions would benefit from more information such as in the ombudsman, CURE or OCEO offices.

An explanation of why every office seems to require “contracted services” such as $44.5 million being spent by the Information Office, an increase of $3.5 million (8.6%). Is the agency in that much need of PR? What firms are benefitting from this largess?

There are three different offices serving the Chairman: his office, the office of the Board and a newly established office of the Executive Secretary with a staff of two but then increasing in the out years. Why is the new office needed given all the other support in place?

Why are key units left out of the pubic budget package, that is the details of the CLF’s ever expanding spending and the separate NCUSIF direct charges?

The Role of Democratic Debate

The composition of the board where only two may be of the same party, is intended to encourage discussion and the airing of different approaches to policy and oversight. This has not occurred with the current board. Bipartisanship, or deferring to the chair, is used to explain the lack of meaningful dialogue or alternative positions being put forward.

But debate is what makes democracy work well. Without a loyal opposition, the understanding of important options is lacking.

This is a story of a credit union led by an extraordinary CEO. It is so heartening that the writer prepared two articles to describe fully her accomplishments.

The headline says it all: The Tiny Credit Union Powering Brooklyn’s Economy. The author’s writeup illustrates the power of passion and commitment in service to a community.

This account is a beautiful gift for all who believe credit unions can do something special. It demonstrates the good will created with a small amount of resources and dedicated leadership.

My summary is to encourage you to link to the full accounts.

“With just $50 million in assets, Brooklyn Cooperative Federal Credit Union is a rounding error compared to the nation’s largest brand-name banks. But in terms of impact on marginalized communities, this tiny institution punches well above its weight.”

In this first segment, the writer, Oscar Abello, describes how the current CEO Samira Rajan -a graduate of Harvard’s Kennedy School of Government became involved.

She joined the startup in 2001 in a catch-all position as an AmeriCorps VISTA volunteer program. This paid her a stipend as the new credit union didn’t yet have enough income to offer her a salary. She became a loan officer. First loan she made, went bad.

In 2008 she became CEO.

The founding CEO Jack Lawson was a PhD student in economics at the New School in the late 1990s. He was looking for a part-time job related to his research. He received a grant from a local foundation to support his goal of organizing a credit union for the Ridgewood-Bushwick Senior Citizens Council. Over time this startup evolved to become Brooklyn Cooperative.

Until his departure in 2008 he focused on seeking grants from local sources and the CDFI Fund to underwrite the startup expenses and “build the runway” for sustainability.

This process continues. Since Rajan became CEO, the credit union has received eight grants from the CDFI Fund, totaling $11.3 million.

The credit union today can underwrite loans with little to no collateral, to members with an average credit score below 650, and to members without social security numbers.

Residential mortgages for one to four family homes are more than half of Brooklyn Cooperative’s current loan portfolio.

But its small business lending efforts are especially critical for the credit union’s local impact.

Counting by the number of federally-guaranteed the Brooklyn Cooperative is ranked fourth, behind only TD Bank, Chase and M&T Bank. The cooperative’s average 7(a) loan size is $24,000.

The writer’s description of the CEO’s relationship with NCUA is also enlightening. This is Rajan’s candid opening comment:

“Every three years, we have literally a new examiner come in and they’d be like, we’ve never seen this before. Yeah, I know you’ve never seen that before. New examiners have to get their whole head wrapped around the fact that you’re going to be doing lending which is non-conventional, that you’re deliberately going to be lending, knowing that your loss rates will be higher than the normal and you’re going to be lending to borrowers who on paper don’t qualify. … It flies in the face of what apparently you’re supposed to be doing, which is lending only when you definitely have a 700 credit score.”

For the full account of this remarkable institution, read both articles. At the close the author asks the following of his readers and those who work in the cooperative system:

Brooklyn Cooperative is proof that it’s possible to build a financially sustainable institution that provides credit for a variety of purposes to people and communities like those it serves — Black and Brown, immigrant, low-income. . .it raises the question: should there be more credit unions like this one across the borough? Or across New York? Or across the country?

Serving Strangers

During this season, the mail brings more requests for donations than Christmas cards. There are two broad categories of asks. One is the multiple nonprofits serving the arts or education-choral groups, museums, Chautauqua and public television.

More plentiful are the organizations serving human need: Hope Hospital in Seattle, Achungo Community Center (Kenya), World Kitchen and dozens of local efforts to assist others, often strangers, this time of year.

A carol that recognizes this ever present reality of human suffering is Christ in the Stranger’s Guise. This arrangement by Karen Marrolli is from a summer choral workshop in Montreat, NC, and includes the words. They portray for me, Rajan’s example of service to her community.

A thought for the season by English poet John Betjeman: Advent 1955

The Advent wind begins to stir With sea-like sounds in our Scotch fir, It’s dark at breakfast, dark at tea, And in between we only see Clouds hurrying across the sky And rain-wet roads the wind blows dry And branches bending to the gale Against great skies all silver pale The world seems travelling into space, And travelling at a faster pace Than in the leisured summer weather When we and it sit out together, For now we feel the world spin round On some momentous journey bound – Journey to what? to whom? to where? The Advent bells call out ‘Prepare, Your world is journeying to the birth Of God made Man for us on earth.’

And how, in fact, do we prepare The great day that waits us there – For the twenty-fifth day of December, The birth of Christ? For some it means An interchange of hunting scenes On coloured cards, And I remember Last year I sent out twenty yards, Laid end to end, of Christmas cards To people that I scarcely know – They’d sent a card to me, and so I had to send one back. Oh dear! Is this a form of Christmas cheer? Or is it, which is less surprising, My pride gone in for advertising? The only cards that really count Are that extremely small amount From real friends who keep in touch And are not rich but love us much Some ways indeed are very odd By which we hail the birth of God.

We raise the price of things in shops, We give plain boxes fancy tops And lines which traders cannot sell Thus parcell’d go extremely well We dole out bribes we call a present To those to whom we must be pleasant For business reasons. Our defence is These bribes are charged against expenses And bring relief in Income Tax Enough of these unworthy cracks! ‘The time draws near the birth of Christ’. A present that cannot be priced Given two thousand years ago Yet if God had not given so He still would be a distant stranger And not the Baby in the manger.

Sir John Betjeman, CBE, was an English poet, writer, and broadcaster. He was Poet Laureate from 1972 until his death in 1984. He was a founding member of The Victorian Society and a passionate defender of Victorian architecture. He began his career as a journalist and ended it as one of the most popular British Poets Laureate and a much-loved figure on British television.

Love’s Multiple Meanings

Craig Hella Johnson is an American choral conductor, composer, and arranger. He was born on June 15, 1962, in Crow Wing County, Minnesota

One unique aspect of Johnson’s programming is his signature “collage” style, or composed programs that marry music and poetry to seamlessly blend the sacred and secular as well as the classical and contemporary.

In an interview he notes: Music is a spiritual language of the freest kind. It doesn’t matter what your denomination or nonbelief or tradition is, because it’s about connecting with something larger than ourselves.

This work combines the well known Christmas carol Lo, How a Rose E’re Blooming, with a poem, The Rose.

This was the final song of our Christmas concert yesterday. As you listen, it may bring a tear or two.

To understand today’s blog, I would ask the reader to first look at this TV news report on credit unions from KPBS. It is accompanied with a two-part written story by Scott Rodd, the station’s investigative report published on November 29, 2023.

The reporter has a good understanding of credit unions’ public image. His TV story opens with an interview from a member who states “they (credit unions) are not supposed to be in this for making the big bucks.”

The story counters the long asserted public image of credit unions as serving the “little guy.” The key data point is that credit unions are no different from banks when it comes to overdraft fees charged members, even though cooperatives routinely present themselves as “better than banks.”

He quotes the CEO’s statement in San Diego County Credit Union’s annual report that her goal is “putting people first and profits second.” This would be an interesting ranking for any coop leader.

The reporter reinforces this contrast of public image versus organizational behavior by pointing out the CEO’s total compensation has “increased seven-fold over the last decade to nearly $12 million dollars according to the according to SDCCU’s latest financial statements.”

The articles provide examples from other area credit unions of the role of overdraft fees along with six figure CEO salaries. His thesis is that credit unions are not actually what they claim to be, “community-based alternatives to big commercial banks.”

Lessons from This Reporting

The two-part story was triggered by the first disclosure of overdraft fees required by all state chartered financial institutions in California.

By focusing on this newly disclosed datapoint, the writer suggests that credit union rhetoric and practice do not align because “these fees are typically paid by “the most vulnerable” customers.”

Several observations. Compared with banks, credit unions are not as transparent in operational disclosures. Member-owners have significantly less public information than do bank owners. This is not just about OD fees but many other areas of operations including executive compensation. Only state charters, not federal credit unions, must file a IRS 990 which requires compensation data be disclosed.

Lack of transparency prevents members from having critical data about their credit union’s performance, in both ordinary and special circumstances such as merger or buying banks. Regular public information is also the best antidote to limit self-serving behavior.

Credit union leaders work in a capitalist economy. Often it is difficult for those in coop leadership roles to overcome the residual lures of capitalism. It is easier to adopt the priorities and practices of for-profit competitors than create the innovative options member-ownership offers.

The result of this investigative reporter’s story is “brand devaluation.” It presents credit union as no different from the alternatives cooperatives were meant to counter. It is a loss of real value in the both the public and political market place.

Talking to the Press

Repeatedly throughout his two part series, the reporter tells of his attempts to interview the leaders of the credit unions he is covering. These efforts for comment include the California Credit Union League.

By not participating, credit unions reinforce the idea that they do not have an explanation or response to the writer’s point of view.

One leader is an exception: Bill Birnie, CEO of Frontwave. He goes on camera to talk about the credit union’s courtesy pay product. He discusses his current salary openly with the reporter.

He apparently was the only credit union person willing to engage on this sensitive topic. The story was more than just OD fees and the members this affects. It goes personal by contrasting this practice with the compensation of those implementing the fees.

Leadership is more than trumpeting success. It also requires a willingness to address criticism and possibly poor judgments. This is especially so when done in public where the critic may have the last word or “already has the story written.”

Leadership when confronted with alternative points requires character, a willingness to listen, and the courage to sit down with one’s questioners.

In this case, apparently only one person was willing to stand up and be responsible. I don’t think it was an accident that it was Bill, who came to credit union leadership later in life. Here is a short synopsis of his career before coops:

Bill is a 25 year veteran of the US Marine Corps, retiring in 1997 at the rank of Sergeant Major with combat service in Operations Desert Storm in Kuwait and United Shield in Somalia.

Bill is an example of what it means when “we thank someone for their service” and what it brings to their subsequent civilian roles.

A Seasonal Song in a Time of Conflict

One of the most recognized Christmas songs is I Heard the Bells on Christmas Day.

On Christmas day, 1863, Henry Wadsworth Longfellow—a 57-year-old widowed father of six children, the oldest of which had been nearly paralyzed as his country fought a war against itself—wrote a poem seeking to capture the dynamic and dissonance in his own heart and the world he observes around him.

The words go from despair (There is no peace on earth,” I said;”For hate is strong, And mocks the song”) to hope:

The following persons are in transition. They have dedicated most of their professional lives to the service of credit unions.

A Farewell Address

Jim Dean arrived at Affinity Credit Unions, Des Moines Iowa five years ago. It was a turnaround situation in multiple respects. In September 2023 the credit union was awarded NAFCU’s credit union of the year recognition.

The following is from his farewell message to the credit union members and the team he led.

“As the saying goes, days pass slowly but years go by in a blur. When we moved here from Illinois in September 2018, my commitment to the board of directors was to work as your CEO for five years. It’s been a pleasure leading this member-owned cooperative into its 75th year, but now is the time for me to retire and let a new leader take over.

“Our mission statement and vision of Building Better Lives was an important change introduced five years ago. That has been the focus ever since and we have made this a reality. We have excellent staff from front to back & our volunteers are engaged and motivated to work in your best interests.

“We don’t focus on the community to earn rewards but have earned rewards and the highest acclaim in large part because of our community impact.

“Our marketing focuses on our brand. If you compare our offerings to those big credit unions who do this, we line up quite well throughout our entire product line.

Yes, our commercials talk about the Best Credit Union Ever, but having received the National Credit Union of the Year in the $500 million and under category is something to shout about.

“We might add that our credit card program is the best ever as well as our checking accounts in terms of fairness and transparency.

“Highlights of my time include our Building Better Holidays campaigns. Non-profit organizations are reluctant to promote themselves, so we’ve done that for many in our community.

“We fought hunger in partnership with the Food Bank of Iowa & through our six-year partnership with the Iowa Wild and by working with organizations like Meals from the Heartland.

“When COVID-19 shut down Iowa, and much of the world, we immediately communicated our decision to waive all fees, allow payment deferments, and alleviate financial pressure that lost wages brought. We closed our lobbies and transitioned many employees to remote working for the first time ever.

“I’m very proud of the annual meetings we have conducted. Member democratic control, as well as education, are two of the seven principles on display the second Tuesday of May each year.

“Most of all, I’m proud of our people. This includes our leadership team, employees, and volunteers. They understand what working in the member’s best interest means and that is emphasized by all managers daily. This is a relationship business and much of our recipe for success.

“I probably should mention that our financial performance has been off the charts excellent, something we don’t mention often.

“My door is a quick left as you enter the Hoffman lobby. The door is (almost) always open, so stop by this month to say goodbye or maybe hello for the first time.

“Thank you for this opportunity.”

Honoring a Lifetime

On October 3, 2024 the cooperative community will inducte five new honorees in the Cooperative Hall of Fame in Washington, DC. One is a credit union veteran. Here is his brief resume from the announcement.

Introduced to credit unions in the late 1970s, Clifford Rosenthal has spent his career promoting financial equity and inclusion in the nation’s most overlooked and underserved communities.

Growing up amidst transformative campaigns for social justice in the 1960s, Cliff began his cooperative journey by organizing and managing food cooperatives in New York City and Connecticut. This led him to Washington, DC, and the National Association of Farmworker Organizations where he was tasked to organize a credit union to serve its members.

Upon his return to New York, Cliff joined the National Federation of Community Development Credit Unions (the Federation), first as a volunteer until he was hired as staff. By early 1983, the Federation was preparing to close for good after federal funding was eliminated.

Sustained by his conviction that community development credit unions (CDCUs) were important and must be preserved, he once again took on a volunteer role as the Federation’s Executive Director. In partnership with Annie Vamper, the pair rebuilt the Federation into a catalyst for transformative change.

Understanding the critical role capital plays in low-income communities and CDCUs, Cliff pursued a two-pronged strategy to capitalize CDCUs by creating new channels to mobilize private investments and by expanding sources of public financing. This eventually led to the birth of the CDFI Fund in 1994 after President Clinton signed the Riegle Community Development and Regulatory Improvement Act. As well, he worked to secure NCUA’s allowing low-income credit unions the privilege of raising secondary capital.

I understand Cliff has another book to be released about his many adventures with low income credit unions.

Washington Credit Union Daily’s New Home

Credit union’s self-awareness depends much on the writers and press dedicated to telling the industry’s stories. One person is David Baumann. He has been covering the credit union industry for more than seven years, first at the Credit Union Times and then at CUCollaborate.

Based in DC, his blog is free on Substack. His focus is the multiple legislative, regulatory, and political developments affecting credit unions. Readers may go to his website, call up a story or scroll down to the “subscribe” option.

The Changing Seasons of Lives

I first heard a performance of O Love by Elaine Hagenberg (b. 1979) a week ago at American University’s December chorus concert.

The concert’s title was Stay with Me. The selections presented the theme of relationships on which all depend.

The beautiful melody might not fall strictly into the Christmas music genre. Rather, it is a message for all seasons.

The words have a story. George Matheson, a Scottish Presbyterian minister, found himself at age 20 alone when he went blind and his fiancé decided to break off the marriage. She left him. He turned to the Lord. In the darkness of the moment, he wrote this hymn in five minutes. It never needed any editing.

Today’s carol and credit union story is captured in the opening line of the music below. First, the credit union’s account.

Every Touchpoint Matters

This is the story of a member contacting the President of his Credit Union after reading the monthly Newsletter. And what happened next. (used with permission)

From: Daniel H. <dh@xxx.com> Sent: Wednesday, November 15, 2023 11:32 AM To: Jeff Carpenter <jeffc@weokie.org> Subject: Thank you

I received your news letters In Regards of thanksgiving and all the delightful things Weokie does for their members. my wife and I are thankful for you and the company for providing good deeds to the community. we ourselves have been struggling and I’m not going to lie. our account has been at struggles with overdrafting every month to make ends meet. but we work every day to try to improve ourselves to be better. one day our account will stay on the positive side and look forward to all the new adventures to come.

I loved this message because our member, who is going through some health and financial challenges, was simply thanking WEOKIE for being such a great community citizen.

Thanks to Diane we were able to learn more about his account. We agreed that I should reach out to see if a meeting would be of interest. I engaged in an email exchange with Daniel and coordinated a meeting with Daniel and his wife Jessica to meet with Patrick and myself at South.

Setting up a Meeting

Patrick did some great work preparingfor the meeting. Together we probed to learn their story and understand how they got to this situation. Much was from their trying to help so many others in their family.

Patrick talked through lots of options. I might have added some too, but in the end, Patrick was able to convince everyone (yes, including me) that taking “one step” not sixty, was the best path forward.

We extended a significant signature loan to get them out of the mountain of high-risk debt that was pushing them to the brink of financial collapse. Patrick was empathetic, yet firm, in his conversations. He was able to gain agreement to eliminate Courtesy Pay, for WEOKIE to handle the pay-offs, and to set up automatic loan payments on the day their monthly income is credited to their WEOKIE account – all of these help mitigate our risk.

We met with them, took the loan application, approved it, and paid off their high-interest loans in 48 hours. That led to the following email from Daniel:

From: Daniel H. <dh@xxx.com> Sent: Tuesday, November 28, 2023 3:47 PM To: Jeff Carpenter <jeffc@weokie.org> Subject: thank you

Jeff

My wife and I would like to thank you for the help you and your team for the opportunity to help us succeed in our goals and for giving us Patrick to work with. he was an awesome gentleman. he worked hard to help us out and succeeded in getting what we needed done for a good approval. I’m looking forward to a good start in bettering ourself. we will keep in contact and keep you updated on our success.

thanks again

Dan and Jessica

Special thanks to Melissa, Diane, and Patrick for letting me participate in living our vision of making a difference, one person at a time. And affirming that “every touchpoint matters” is a good strategy.

Today’s Music of the Season

The Wexford Carol is a traditional religious Irish Christmas carol originating from the town Enniscorthy in County Wexford. The subject of the song is the nativity of Jesus Christ. This recording is from Clare College, Cambridge in composer John Rutter’s arrangement, which begins with Good people all.