The country is going through the political throes and formal processes of a complete changeover of executive and political leadership in DC. This includes NCUA.

In late 1981 Ed Callahan had been confirmed as the next NCUA Chair. Before he had been formally sworn into the job, I asked what would be his toughest challenge would be.

Ed had been leading the Illinois Department of Financial Institutions for almost six years. In the Department, the credit union division oversaw 1,200 state charters. During this time the Illinois system had navigated multiple market and legislative changes implementing deregulation.

I assumed his response to my question would be about greater scale of responsibility, from one to 50 states and from 1,200 credit unions to 16,000; or, the increased size of the agency budget and staff; or, the more complex institutional and political environment in DC. This involved Senate and House hearings and NCUA membership of interagency committees such as the FFIEC or DIDC.

Ed’s Number One Challenge

His answer mentioned none of the above areas. His biggest challenge he said would be communication. That is to explain the direction he believed the NCUA and credit unions should undertake and why.

Callahan’s track record and leadership of Illinois cooperatives was described as deregulation. At a dinner celebrating his appointment before going to Wasington, the Illinois Credit Union League presented Ed with a framed sign he then hung in the Chairman’s NCUA office. It read:

Leadership of a Transition

However, what would deregulation look like on a national scale and all at once?

The first effort communicating this approach was a videotaped panel discussion arranged by the Illinois Credit Union League on January 8th, 1982. The title: Deregulation, What Does it Mean?

The video is 24 minutes. This conversation was the beginning of a dialogue to change the entire direction of the prior 50 years of federal credit union regulatory practice.

Several factors in this video are noteworthy. It was a joint NCUA-movement project. The Illinois League sponsored and produced the video. The panel included Jim Barr, the head of CUNA’s Washington office as moderator, three credit union CEO’s, and Chairman Callahan and NCUA Executive Director Bucky Sebastian.

The format is Q&A. Hard questions are asked. The dialogue is authentic due to the openness of the conversion.

The most important moment may be at minute 16. A CEO responds to Callahan’s deregulation approach by asking how much influence will credit unions really have in deciding this policy? Ed’s reply from the February 1982 NCUA Review, which printed a transcript of the video:

“Even though I think credit unions want deregulation, I am more committed to the fact that we have to respond to their needs. If they don’t want deregulation, we will see that it doesn’t happen.”

A second question by Jim Barr is simply. Why now? Go to minute 18 for the response.

This video was the first of 20 NCUA created during Callahan’s three and one half year tenure. It was one of many efforts to inform credit unions and the public about NCUA actions. To succeed, this approach required a leader who was accessible, informed and willing to listen to the industry.

The result was a tenure characterized by joint NCUA-industry efforts that repositioned the system for an entirely new era of market competition.

This video is one example of how the regulator and the industry collaborated so that the movement could thrive well into the future.

Communication went to all constituencies. These included the public and credit union press, the members, credit union leaders and other agencies of federal and state government, The outcome included some of the most consequential cooperative system innovations since the first credit union charter in 1909.

Leadership is never easy, especially in public positions. Developing and seeing through a successful tenure begins with the very first communication. In this transition. that began with a video that still provides meaningful lessons decades later.

Authority attracts followers. The power of a position is a reality whether that role is CEO of a credit union, a company, a regulatory agency or an elected official including the President of the United States.

People and the public have an instinctive respect for those in authority. But the process of validating one’s leadership is different for those in elected versus appointed positions. For appointed roles, there is a presumption of industry expertise or other skill that warrants the responsibility. The first steps matter.

Getting After It

Whichever path to leadership most will act quickly to affirm their new authority, sometimes dramatically. It both enhances the role and the perception of being in charge.

President Trump claims an electoral mandate “landslide.” In just one week he has issued dozens of executive orders, traveled widely across country, spoken to an international conference all in a very deliberate campaign to show there is new Sheriff in town. Getting after his agenda in a very public and energetic way, enhances Trump’s claims and intent to exercise his vision for the country.

NCUA Board Leadership

This impulse to demonstrate newly awarded executive power is also practiced by incoming NCUA board chairmen. This is especially the case when board appointees have little or no previous relationships with credit unions.

In February 2021 shortly after appointed chair by President Biden, Todd Harper announced his promotion in a Commander’s Call address to the Defense Credit Union Council.

As the COVID-19 pandemic rages on, we must smartly, pragmatically, and expeditiously address the economic fallout within the credit union system. To that end, when I first became Chairman, I issued my Commander’s Call to the agency.”

Time and again Harper used the imminent threat of “economic fallout” during his leadership independent of the industry’s performance and or critical mission issues.

In this same tradition, several days after being appointed Chairman Kyle Hauptman published his eight priorities in a press release. Many read like summaries from prior board meeting statements. Like Harper, he wanted to put his views out immediately.

These initial pronouncements were an assumed first step in asserting the authority of an appointed versus elected position in government. NCUA chair’s will routinely reference a restatement of safety and soundness oversight. Or in some cases an adaptation of the Administration’s governing priorities.

In Hauptman’s new role an important question will be how Trump’s priorities for the federal bureaucracy shape his administration. This is especially true for personnel policies and appointments, agency spending and regulatory and rules review. Will he assert NCUA’s independent agency status or try to implement Trump’s efforts to reform what the president calls the deep state?

The Most Critical Agenda Issue

While these opening statements are part of the ritual when appointed to NCUA leadership, the most important question that all chairs must answer is, In whose interest will they serve?

Will it be incoming administrations? The agency staff? Or the needs of credit union member-owners and their communities? Each constituency wlll have its special claims and interests.

When NCUA leaders arrive without a track record of working within the credit union system, the assertion of agency priorities can easily overlook the most important issues the industry faces. It is easy to repeat the regulatory mantra of safety and soundness without having to explain what that means. For example, from 2007-2024 the losses to the NCUSIF have averaged less than 1 basis point per year. So what are the underlying performance issues?

The Credit Union Way for Developing a Relevant Agenda

I believe the most important priority for NCUA leadership should focus on the credit union member-owners. “It’s the member, stupid” is how one prior leader explained the challenge. But how does one put members first?

The answer lies at the heart of the cooperative model. Leaders within the credit union system must talk with and listen to credit unions. For a relevant regulatory agenda, NCUA and credit unions should be co-creators for setting the priorities to enhance the mission of the cooperative system. And the well-being of its owners.

Not all credit union decisions involve a regulatory issue. But credit unions need to recognize individual actions can have system wide consequences on the reputation and public support for their special status in financial markets.

Just as Hauptman has drawn up his initial talking points, so too are credit unions, or their lobbyists, asserting their priorities: protecting interchange fees, the tax exemption and reducing over-regulation.

But are these the primary issues that should form a collaborative agenda for the next four years? How do credit unions balance their increasing financial stature with the absence of any effective member owner governance?

Is the growing mergers of sound credit unions and removal of local roots in the long term interests of the members? What is credit unions unique responsibility, if any, in addressing the needs of individuals left behind or the macro issues such as the national shortage of affordable housing?

Ultimately an effective leadership agenda is a collaborative process. No institution has all the answers. Listening to competing agendas and reaching a consensus is the art of political compromise.

Some “leaders” will want to avoid this task preferring to assert the power of their appointed or earned positions. Getting after it may work in the short run. Americans respect authority implied by the rule of law. But it is not a formula for lasting change as we see the current approach of a new administration just overturning the priorities of the former.

Credit unions and the regulator are at their most effective when each uses their special skills and experiences to work cooperatively furthering the best interests of members, not a partisan agenda.

Here is an example of how an NCUA board and credit unions responded to the issue of the movement’s federal tax exemption in a prior administration transition.

While credit unions focus on the threat of federal taxation, there is another event that could end the independent cooperative system. To understand how governmental agencies are reorganized, it is useful to review what happened to the separate S&L industry after a decade long series of industry and regulatory failings.

From an Inspector General Report dated March 2012: Title III of the Dodd-Frank Act sets forth provisions to address problems and concerns in the multiple agency financial regulatory system by abolishing OTS and transferring its powers and authorities to the FRB, FDIC, and OCC as of July 21, 2011 .

All OTS functions relating to federal savings associations, all OTS rulemaking authority for federal and state savings associations, and the majority of OTS employees transferred to OCC; OTS’s supervisory responsibility for state-chartered savings associations and OTS employees to support these responsibilities transferred to FDIC; and OTS’s authority for consolidated supervision of savings and loan holding companies and their non-depository subsidiaries transferred to FRB.

Prior to this 2011 transfer of supervision, chartering and examination, the separate FSLIC insurance fund had been merged into the FDIC in two steps. The FSLIC was abolished in August 1989 and replaced by the Resolution Trust Corporation (RTC). On December 31, 1995, the RTC was merged into the FDIC which became the sole deposit insurer for all thrift institutions.

The Presidential Transition Center describes one surviving regulator’s situation today: “The OCC is one of eight Treasury bureaus and has approximately 3,850 total employees. Headquartered in Washington, D.C. It has four district offices and a London office that supervises international activities of national banks. Operations are funded primarily by assessments on national banks and federal savings associations.”

Current numbers under OCC responsibility are approximately 1.500 national banks and federal savings associations and 50 federal branches and agencies of foreign banks.

The administrative head, the Comptroller, is nominated by the President to a five year term and confirmed by the Senate.

As of mid-2024 there were 556 surviving savings institutions. There was no single regulator however. Supervisory oversight of their $1.2 trillion total assets was divided among the OCC-242, the FDIC- 278 and the Federal Reserve-36.

An independent consolidated thrift industry does not exist today. Depending on each institution’s charter history and scope of operations, regulatory oversight is divided among the three federal banking agencies.

The Relevance of History

A goal of the Trump administration is greater governmental efficiency. Combining regulatory agencies is not a new idea. Merging the cooperatively designed NCUSIF into the FDIC, closing the unused CLF and transferring chartering and supervision to a new Treasury bureau would seem a reasonable proposal-for some.

A New North Star: Faster Alone, Farther Together

How might a single OCC administrator view this possibility? The following is from an exit interview with the acting OCC head during the Biden administration:

Michael Hsu, a longtime bank supervisor and former top Fed staffer, threw himself into what he describes as a dream job: running an agency full of examiners. The OCC chief was at the table as officials managed through a regional banking crisis and a crypto crash.

MH: I made safeguarding trust the North Star for all that we were doing…I feel good about what we’ve done.

I’m most interested in long-term, durable wins. I’ve been in government for 20 years, over 20 years doing this stuff. There’s nothing more frustrating than this kind of fleeting, pendulum-swing of announcements. . .

There’s a saying: Faster alone, farther together. I say it to my staff all the time, which is frustrating, because sometimes we have to slow down…But if you just do it alone, you can get the quick win, but then the next guy is just going to undo the quick win.

Responding to a Reorganization Review

To counter the inevitable suggestions for more coordinated financial regulation, the so-called level playing field, requires rethinking what is being communicated at every level about credit unions today.

Some areas for messaging might include:

An NCUA led by informed and articulate leaders presenting the contributions and role of credit unions and cooperative design to the pubic and Congress;

An industry performing with stable and successful financials capable of responding to ever-changing markets;

Meeting public and individual interest in and demand for cooperative charters to lift up local groups and communities;

Daily examples of member-owner benefit that rises above traditional service and product options from for-profit providers;

Leadership at all levels communicating the advantages of cooperative design. A former NCUA executive director once summarized credit union’s purpose with the phrase: “it’s the member, stupid.”

Much of today’s credit union commentary reads and sounds like all the other lobbying and jockeying with a new administration. Protect the status quo. Align one’s vision and “asks” with the incoming administration’s priorities.

That apprach may be smart politics. But credit unions did not succeed by preserving the status quo. What will their role be in responding to the numerous areas of unmet member needs and expectations? That response will position NCUA and credit unions as leaders for greater contribtions or, if not, as a part of governmental policy that needs rethinking.

In a full first day of pomp, circumstance and executive orders, a new regime took over the leadership of the U.S. government. Among the new President’s many actions was appointing Kyle Hauptman as Chairman of NCUA. What will this mean for the agency and credit unions?

Among the blizzard of Trump’s first day executive orders were a number directed at the administration of federal agency management. These orders included:

The requirement for all employees to return to office five days per week;

A freeze on hiring;

The removal of civil service protection on senior positions.

Ending all DEI training and policy implementation.

There were also multiple references to eliminating regulations and sending the people’s money back to them via reduced spending, and maybe lower taxes.

Chairman Hauptman’s term expires in August of this year. Will he follow these priorities of the new administration or assert independent agency status, and therefore not bound by these initiatives?

Hauptman has a number of initial decisions that will indicate what his governing practice will be including:

Who does he add to his team as appointees and what is their professional experience–credit unions or government employment? Or, purely political patronage?

What is his governing philosophy? Is the job a full-time leadership responsibility for the agency, or merely a policy setting role delegating to staff all interpretation and implementation?

What is his view of the role of the cooperative credit union system? Is the coop design unique, or just another form of financial choice in the marketplace? How does he assess the major trends in the industry including merger-acquisitions, the buying of profitable banks and the suggestion that credit unions be taxed?

Preparing for the Role

Hauptman announced his intent to become chair posting “openings” on LinkedIn several weeks ago. His view of credit unions and a governing agenda have never been spelled out. His statements on policy have been in response to Harper proposals, which he has largely supported including the longest, most intrusive rule NCUA ever added to the books, Risk Based Capital.

What will be his leadership style as Chair? How accessible will he be to the public, the press and to the credit union community? Will he listen in conversations or deliver scripted positions? Will he present objective and fact-based priorities or rely on general cliches about government’s role?

Can he articulate common purpose with the cooperative system founded on collaboration, or will he assert NCUA’s independence from credit union’s destiny or fate?

When problem events occur, will he respond with factual answers, send out staff to reply, or worse, just stay silent and avoid any comment as the press reports on credit union shortcomings?

People, especially those working in credit unions serving members, want to hear from their regulators. The coop democratic structure is intended to give responsibility to the members and their chosen leaders. Openness builds trust and confidence. Distance undermines the collaborative advantage which is the foundation of two vital NCUA facilities: the CLF and the NCUSIF.

The Learning Challenge

For both individuals and organizations to succeed they must become learning entities. Responding to change is more than just adding new technology or professional expertise. It means sharing a vision while responding to the constant changes which we all face.

The Shakespearean actor Patrick Page stated that it takes at least 30 years to become an effective performer. Acting first requires knowing thyself, the motivations and awareness that comes from life’s experiences, relationships and multiple roles. But just as important is understanding the same characteristics in others-especially if you intend to present their character to the public in plays.

Leaders are formed in the same way. Leadership is not conferred by appointment to a role—no matter how deserving the individual interprets his or her selection. It is formed in the challenges of life—the wins, the disappointments and the strivings.

Now Hauptman has the chance to show how he will learn and lead. The fate of an industry may depend on how successful his growth can be.

A June 26, 1984 gathering of “Old Timers:” current NCUA board members, prior Administrators, past General Counsels and senior staff celebrate the 50th anniversary of the passage of the Federal Credit Union Act.

Seated left to right: Deane Gannon, Joe Blomgren, Richard Walch and Bernard Snelick.

Standing left to right: Joe Bellenghi, Austin Montgomery, Fred Hayden, P.A. Mack, Ed Callahan, Elizabeth Burkhart, General Herman Nickerson and John Otsby.

A statement of cooperative enterprise from a church’s bulletin board

LEGACY

All of us are indebted to the past,

to those who precede us.

We drink from wells we have not dug.

We enjoy liberties that we have not won.

We share faith whose foundations we have not laid.

The Creighton FCU insolvency resulted from the sudden discovery of a $13.6 million hole in this reportedly $67 million asset credit union. The failure, NCUA’s largest in 2024, is apparently an unsolvable mystery. One in which the only suspect has died. As I first posted, NCUA has provided not a single fact about where any of the money went. Just speculation.

More incredible is the IG suggestion that there is no money missing, just a bunch of accounting errors. Moreover, no one seems very curious about finding out where money went. In the IG response to the Congressional inquiry he opens with the statement: “my office was not required to perform a material loss review. Additionally, NCUA informed us that the agency was not required to conduct a post-mortem review.” In other words, don’t look for any answers from us.

The one IG explanation is that the CFO, who died in April 2024 leading to the shortfall’s discovery. was covering up actual operating losses for up to 26 years. We’ll examine this idea later. In the IG’s summary review, no one within the credit union or NCUA examiners and external CPA auditors apparently saw any indications of irregularity during three decades.

The IG further assures Congress that an over “20 year review” of the CFO’s family records reveals no unusual credit union cash diversions. Yet this is still the person who carried out this cover up apparently alone, fooling every check and balance and division of duties for such an extended scheme.

Blaming a person no longer around, and who apparently took no funds, feels too convenient. Let’s look at the plausibility of the IG’s theory and facts we do know.

The Cash Came In

We know the members deposited the cash and the funds which went missing. When the $13.6 million shortfall was discovered, this hole was covered by underreporting shares by an almost equal amount. Shares balances in the March 30, 2024 call report were $61 million. Ninety days later the total reported by NCUA in their exam and the June call report was $74 million. This is the exact total change in net worth. And the same order of magnitude ($74 million) for Creighton members’ share liability when merged with Cobalt.

But where did the cash go? Here is the IG’s “official explanation” after reviewing all the information he reviewed:

NCUA officials believe the credit union failed due to bad accounting and financial statement fraud. The large deficit was hidden by the former CFO who exploited Creighton’s weak accounting system that allowed back posting, forward posting, deleting transactions, and hiding general ledger accounts when generating reports. Because no money was found to have left the credit union through this, NCUA officials believe the former CFO committed the fraud not for personal financial gain, but to make the credit union appear to be thriving in the eyes of its Board and membership.

The IG’s “Thriving by Hiding” CFO Motivation

Reread what the IG just asserted. Although we know the $13 million member deposits came in, “no money was found to have left the credit union.” This CFO was cooking the books just to hide operating losses for 26 years. This is what the IG wants us to believe?

Cash shortfalls creating a cumulative deficit can only occur if the credit union pays out that cash in some form (hidden operating expenses, fraudulent loans, fake withdrawals, phoney investments etc) What were those payouts? Some entity or person received these cash diversions hidden by accounting coverups for decades.

A brief IG reference is made to the management of the credit union’s 150 ATM’s for which the accounting was difficult to reconcile. This should have prompted questions such as, what accounts were used to fund the ATM operations? Who managed the cash deliveries and cash drawer balancing when machines were serviced? Was there an external servicing contract or were cu personnel responsible? The IG letter states: Fraud auditors reviewed ATM and lease payment accounting transactions. The regional director stated that the ATM accounting was extremely complicated due to Creighton having over 150 ATMs and the multiple ways in which income and expenses could be divided.”

The IG statement is an NCUA and auditor admission they could not figure out what was going on. Managing 150 cash receiving and paying ATM’s is similar to having to reconcile 150 teller cash drawers periodically. Cash comes from deposits and checks, and cash is with withdrawn by members from their share accounts.

NCUA’s Regional Director is reported to find that “ATM accounting was extremely complicated.” This is what should be expected from covering up a missing $13 million. But not a single instance of imbalance or shortfall is cited. Or even a reference to how the machines were managed.

And the closest we get to the smell of a smoking gun is not from NCUA or outside auditors, but from Cobalt which is quoted in the IG report:

“NCUA officials advised (note the passive voice) that in early October 2024, theylearned from Cobalt that after the merger, Cobalt determined that the former CFO understated expenses related to the ATM network to artificially boost Creighton’s income statement to appear to achieve a steady net income. The IG continues:

“Cobalt surmised that the former CFO was either not booking the monthly ATM expenses at all or was severely understating the expenses. Cobalt indicated the ATM costs alone should have been $255,000 each quarter. They determined the CFO booked around $120,000 per quarter to the office Operations account. Cobalt officials explained to NCUA officials that this would account for an approximate $500,000 to $550,000 reduction in net income per year if no other expenses were booked to the Office Operations account.

Cobalt officials explained that over more than 26 years, such an understatement would easily account for the $12.5 million deficit.”

One can only say Wow! to this explanation from Cobalt. NCUA did not make this finding. ATM expenses are for cash outlays for withdrawals and network operations. The bottom line is that someone or some entity was paid the money. Who wrote and signed the checks for these underreported expenses? The IG report makes it appear it was all just confusing bookkeeping.

Putting the Blame on a Fall Guy

Cash from members shares came in and $13 million cash ended up missing. For 26 years it was all the “fault” of a person no longer living. Which means that all of those who were simultaneously responsible for the safe and sound operation are let off the hook.

Among these listed in the IG letter are the CEO of 32 years, a senior accountant, the board, the supervisory committee, the outside auditor, special auditors and multiple NCUA officials from the supervisory examiner, problem case officers up to the RD’s office.

These were not just persons called in to observe a financial autopsy. They were directly responsible for this institution’s safe and sound operation in their various capacities in the many years before this failure came to light. Yet we read not a word about their roles including the person who oversaw the CFO and his senior accountant staff this entire time.

The Reported and Reconstructed Net Income

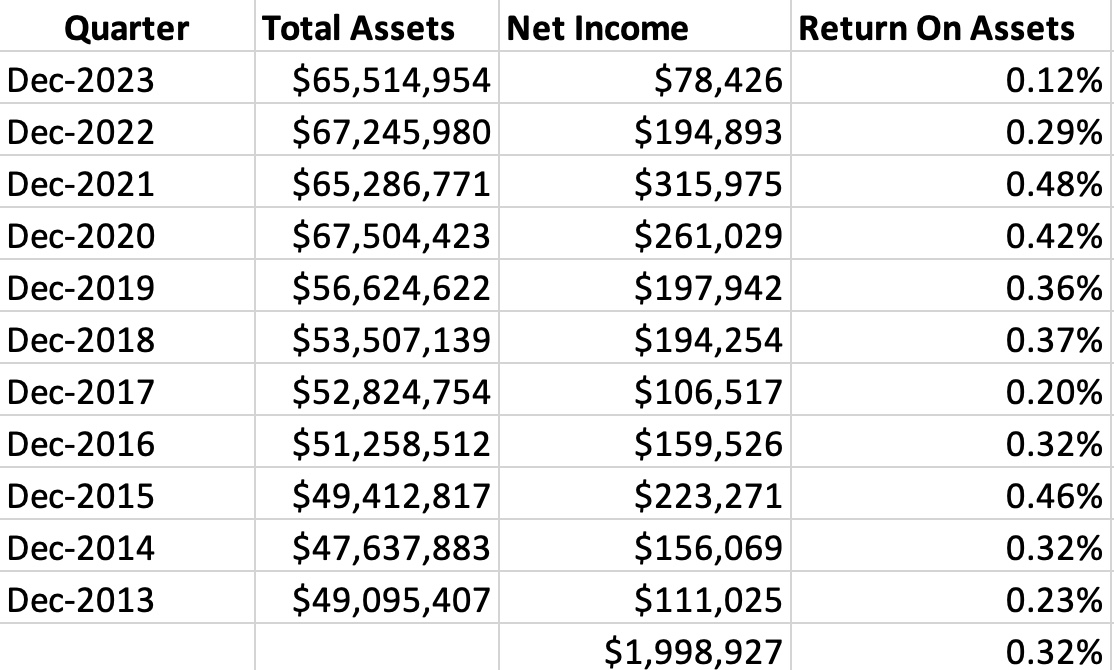

Here is what we know from the most recent eleven yearend call reports prior to June 2024.

Creighton FCU’s Reported Financial Performance

OK performance, but certainly not world beating. If one believes the IG’s theory, then the real result in this most recent eleven years was an operating loss of $5.5 million from ATM “expenses” plus false net income of $2.0 million. A $7.5 million difference somehow hidden by creative accounting.

However if one presumes a steady cash diversion as the problem, then adding back the estimated $500,000 or more per year means the credit union actually made $7.5 million—most of which was “expensed away.” This earnings would equate to an average ROA of 1.2% or four times the net in the call report. And a reasonable possibility.

The cash from member share growth came in. The cash went out the door as an “operating expense” somehow, somewhere.

A diversion of this magnitude for this long would seem to require several participants. Presumably the ATM’s were not deployed all at once. A system of diverting cash was initially set up and expanded as the network grew. Was some entity or person(s) servicing the machines somehow involved? Other credit union employees had to balance the ATM total cash receipts and disbursements to the general ledger. There had to be a system for quickly producing expense and suspense entries to cover up the missing cash for exams and auditors. No one person could fill all these roles.

Since the share shortfall was quickly found suggesting a second set of books, there is probably a similar recurring system for diverting cash to sustain this activity for decades.

All the people listed in the IG reports were in the room when this happened. But none of them was apparently asked for an explanation of how this could have occurred on their watch. For example how could the CFO have “managed” the expected net income without first talking to the CEO about the results?

After reviewing 20 years of the deceased CEO’s family records, and finding “no improper transfer of credit union funds”, the IG’s simple explanation is that “that the CFO hid this $12 million deficit by exploiting the credit union’s weak accounting system.” But how long had this “weak accounting system” been in place?

The lack of any IG mention of NCUA exam and CPA responsibility for “weak accounting” suggests a reluctance to learn who is accountable for what in this failure. Instead put the blame on the person no longer available, and who took nothing.

Questions the IG should have asked include: What were the examiners’ CAMEL ratings in the most recent years? What did the supervisory committee do? How did examiners record the problems of” back posting, forward posting, deleting transactions, and hiding general ledger accounts” now offered to explain the inability to find the shortfall? Did the CPA firm give a clean audit opinion?

The NCUA and IG’s failure to look at the standard processes for oversight and accountability reflects a flaw in the agency’s own structure. Handing problems over to another credit union to cover up NCUA’s supervisory failures, will only lead to more such failures.

Throwing a Credit Union Under the Bus

Cobalt FCU and their members are taking the hit for Creighton’s financial and supervisory failures. The immediate results of the Creighton merger in the September 2024 quarter include a share inflow of over $73 million; a reduction in undivided earnings of almost $7.0 million (from $115.6 to $106.5–( i.e. Creighton’s negative net worth); and an increase of 6,700 members versus declines in the immediate prior quarters.

Additionally, Cobalt’s net income from ongoing operations reported a $400,000 third quarter loss. The year to date net income is a negative $2.2 million. These combined changes resulted in Cobalt’s net worth falling to 8.1% from 9.2% at the September 2023 quarter end.

A Case Study of Failure-at All Levels

In the IG’s reply to Congress, he states one of the objectives was to report on:

the effectiveness of the National Credit Union Administration’s (NCUA) examination and oversight processes in detecting and preventing financial irregularities, and the role and performance of external auditors in this case. The letter covers none of these issues.

At this time no one yet knows where the missing cash has gone. NCUA has not worked very hard to get critical information on the event. The IG mentions a possible explanation suggesting there is no missing money-just accounting confusion. But the $13 million of member funds is gone.

NCUA seems to have distanced themselves from any further explanations, even citing Cobalt for the latest accounting examples. Yet overseeing the safe and sound operations of credit unions is NCUA’s number one priority. NCUA failed totally and quickly moved on in this case. They have literally closed the books, fended off queries and said there is nothing more to see here.

If this sudden $13 million failure is not a wakeup call, when will the senior leaders of the agency step up to the mike and take responsibility? The NCUA board is responsible for governing the agency, not staff.

The Board’s silence and turning over responses to the IG for a Congressional inquiry for its largest cu failure in 2024 is a leadership failing. The agency’s no comment and the IG’s second and third hand reporting, undermines pubic trust and confidence in NCUA’s administration. Congress, credit unions and the public want to hear from their leaders in a crisis, not the bureaucracy.

Perhaps it is time for a real change at the NCUA board.

The TV story told of the $13.6 million dollar loss at Creighton FCU leading to its subsequent merger with Cobalt FCU in August 2024. Cobalt said this was the result of the “CEO’s retirement.” Both Peter Strozniak’s Credit Union Times article and I had written about this forced merger and the loss in its final June 2024 quarter of operations.

The merger was caused by an enormous deficit equal to 20% of assets uncovered following the CFO’s death in April. NCUA gave no explanation of what happened, where the money went or who was responsible for the follow-up. NCUA and Cobalt refused to answer any questions about the event. Problem resolved, no questions please.

But the TV news triggered immediate additional facts that NCUA has refused to provide the press and public about its actions. The TV reporter received a letter NCUA’s Inspector General (IG) sent to Omaha Congressman Mike Flood responding to his inquiry about the circumstances of the loss in November.

The IG response is linked here. The letter opens with an unusual disclaimer of direct responsibility as the IG and NCUA are not required to investigate this situation any further:

Because there was no loss to the Share Insurance Fund, my office was not required to perform a material loss review. Additionally, NCUA informed us that the agency was not required to conduct a post-mortem review for the same reason.

But the IG then proceeds to state facts from the public 5300 call report and details of all the external resources and NCUA officials who became involved when the CFO died in April. Those listed include a local CPA firm, the NCUA’s supervisory examiner, the regional director, associate regional director, the director of special actions and a problem case officer. NCUA requested the credit union hire a bond attorney, fraud auditor and an interim CFO to work with its problem case officer. On May 3 the case was transferred to the Western Region’s Special Case office on May 3.

The only NCUA offices not listed are those ultimately responsible for the oversight of NCUA’s federal credit unions: the Executive Director, the Director of Examination and Insurance and the NCUA board. By omitting any mention of their role, they are apparently excused from any accountability.

In October 2024 Cobalt reported to NCUA that the “former CFO understated expenses related to the ATM network to artificially boost Creighton’s income statement to appear to achieve a steady net income.” The IG’s explanation also includes this assertion of agency’s due diligence:

When reviewing the deceased CFO’s family financial records and computers that:The regional director also said the fraud auditors looked for all ways cash could have left the credit union and found no instances of cash removal.

The IG’s concluding paragraph provide NCUA’s theory of the case:

In summary, NCUA officials believe the credit union failed due to bad accounting and financial statement fraud. The large deficit was hidden by the former CFO who exploited Creighton’s weak accounting system that allowed back posting, forward posting, deleting transactions, and hiding general ledger accounts when generating reports. Because no money was found to have left the credit union through this, NCUA officials believe the former CFO committed the fraud not for personal financial gain, but to make the credit union appear to be thriving in the eyes of its Board and membership.

The IG’s Theory of the Case

Several observations from the IG’s summary. First all the information is second and third hand. The IG did not complete any direct review, but solely reported what others have said and done.

If this preliminary description is accurate, one has to believe this accounting coverup occurred over at least 26 years with an average operating shortfall of $500,000 per year between reported and actual net income.

To accomplish this alleged coverup, the CFO would have to keep two complete sets of books. As the deficits were recorded from share balances this would require hundreds of individual entries each quarter to balance out the shortfall but keep member statements accurate. Then these two sets of books would need to be updated quickly whenever external NCUA examiners and auditors arrived on site. Or whenever there was any external loan and share verifications.

A person capable of this legerdemain bookkeeping effort for over 26 years was however not capable of managing the credit union’s financial performance with positive net income?

There is no explanation of how such a consequential scheme could have gone undetected from annual CPA audits, NCUA examinations. supervisory committee share and loan verifications and traditional separation of duties in the accounting shop. It was not discovered until the CFO’s death in April. New people quickly found the out of balance situation and the $13 million shortfall. The fact that the share shortfalls were recovered so rapidly and then transferred in full to Cobalt, suggests these two sets were readily available. An internal defalcation involving member share balances over three decades would normally be an auditing and forensic nightmare to reconstruct. But in this case resolved quickly.

Just Country Bumkins Fooling Experts

Finally, it strains credulity to believe there was no shortfall of funds. The cash had been received from the incoming share deposits. But the IG’s letter presents the assumption that the CFO just used “suspense accounts” to cover unrecorded continuing operating losses—that would average at least $500,000 per year. Why would a person go to this much trouble to just cover operating losses for which he was not directly responsible? If in fact it was failure to balance out ATM deposits and withdrawals—one suggestion—how could such a continuing imbalance go unnoticed for over three decades?

The IG report describes the accounting coverup: Specifically, the CFO had understated expenses related to the credit union’s ATM network to artificially boost Creighton’s income statement. And, The regional director stated that the ATM accounting was extremely complicated due to Creighton having over 150 ATMs and the multiple ways in which income and expenses could be divided.

A credit union of this asset and member size managing a 150 ATM network seems highly unusual. What happened to this system after the merger? Why were examiners and auditors unable to balance out this system for decades?

Assuming the CFO’s only rationale was to hide a continuing operating loss and that he received no benefit from his actions, one must ask who also might benefit from such a coverup? Who supervised the CFO? Is this just a situation of two country bumkins fooling all exam and auditing experts for decades?

NCUA’s Silence on This Failure

Until the IG’s December response to Congressman Flood’s inquiry, all responsible parties have said nothing about the situation. Press queries are referred to call reports and to Cobalt’s press release saying the merger was due to the CEO’s retirement, a completely false account. Why would the NCUA and Cobalt put out such a blatantly false and easily contradicted explanation? Was it to avoid addressing the $7 million or greater shortfall that Cobalt members will now cover?

One fact is clear, everyone, including the IG is distancing themselves from any responsibility for getting to the bottom of this $13 million loss. The IG presents second hand information and lists multiple NCUA involvements with everyone handing off the ball to someone else-either internally or externally. Cobalt does the cleanup. The IG quotes Cobalt’s theory of the loss from October, not NCUA findings, for the missing funds. The IG washes his hand because no “material loss” review is required, but he will consider adding a review to his 2025 “to-do” list.

When people in positions of responsibility have nothing to hide, they will speak up with their understanding of events and what more needs to be done. In this case there is silence for all parties, but most especially the highest levels of NCUA. The initial explanation of multiple decades of accounting coverups creating a $13 million shortfall seems unlikely and inconsistent with some of the data reported. It feels like there must be more to the story.

The True Shortcomings

NCUA’s lack of public candor is the real problem. No one at NCUA wants to take responsibility for the agency’s most fundamental role of overseeing a credit union’s safe and sound operation. Noticeably absent from IG’s account is the role of the three-member board, the information they received and the actions they did, or did not, take.

Did the Board approve the forced merger without member vote? If so, what was in the Board Action Memorandum about the situation and alternatives? Why was Cobalt FCU willing to absorb this accounting and operational mess with a $7.0 million loss which their members must now cover? Where is their upside, if any?

Why weren’t the previous NCUA annual (?) exam papers reviewed for how so-called unrecorded expenses could be disguised in other accounts (suspense and office expenses)? The three quarterly call reports clearly show the credit union reporting positive net income, but no increase in net worth until the yearend. Don’t examiners first review the accuracy of call reports as one of their first verifications? Etc. etc.

The Largest Credit Union Failure in 2024

The Creighton case is an example of institutional failures. The most serious is not the $13 million unexplained loss shutting down a federal credit union. But the total lack of responsiveness to the members and the public by NCUA’s leadership. In a crisis, leadership should come from the NCUA board members, not the professional staff. They are merely foot soldiers. The leaders are missing in action.

Is the best explanation NCUA can provide Congress and the public an IG summary of second-hand agency actions, a listing of all the professional resources sent and offering a third party’s partial explanations of what may have happened?

The buck should stop at the Board’s three desks. The board members are nowhere to be found or heard on the most significant failure in 2024. A long standing, apparently successful federal credit union collapses overnight and costs its members their institution and $13 million in combined resources.

More Precious than Dollars: Trust and Confidence

The NCUA board member’s inaction and silence when facing real problems in an open, prompt and responsible manner is a failure of leadership. Hiding from issues and accountability leads to internal coverups. It creates a lack of public confidence in the agency’s oversight. The perception that board members are not up to the agency’s most basic responsibility raises questions about their competency supervising other areas of credit union activity in which members good faith and trust (e.g.merger payouts) are routinely compromised.

After the TV investigation was reported on Monday, I received the following from a former Creighton member. It read :

Hi Chip – I ran across your coverage (in November) of Creighton Federal’s large shortfall. I am a customer there and had followed their directives to switch to Cobalt. Now I’m wondering if my money is safe at Cobalt! I liked some of Cobalt’s products (a money market savings account with high interest, for instance) and have been happy with their service so far. Still, your coverage of the slap-dash management at Creighton Federal, and its rescue by Cobalt has me wondering if I should move my money to another credit union in town that doesn’t have any problems (that I know of). Thanks!

Hopefully this case is at its beginning and the three members of Congress on the IG’s response will continue to press for actual facts, updated numbers and direct explanations for what happened. NCUA seems incapable of self-assessments. Credit unions should not expect perfection from their regulator, but they should have honest accountability.

Editorial update at 5:00 PM January 8.

Yesterday the WOWT station published this follow up report incorporating some of the IG’s December letters comments to Representative Hood.

Jimmy Carter’s life is a witness to making a transformative difference in the world by personal example and faith, versus the power of a position. This Thursday, January 9th, his legacy will be honored in a ceremony at Washington National Cathedral.

He has stated that the two great formative experiences of his life were the Great Depression and WW II. Today those events and their lessons seem from another era.

When he first announced his Presidential ambitions in December 1974, a Gallup poll asked voters to rank 31 potential democratic candidates. His name was not on the list. Yet just two years later he won the first primaries in Iowa and New Hampshire defeating nationally known opponents including Senators Scoop Jackson, Ted Kennedy and Robert Byrd.

At the July 1976 convention, he became the democratic presidential nominee.

He was a Southern Baptist who taught a Sunday School class whatever his position—as Governor, as President or as a private citizen. He lived his faith not by telling others what to believe, but by example.

In this official portrait by Robert Templeton (1929-1991), Carter is standing in the oval office as it was during his tenure. On the desk is a crystal donkey statute, a gift from the Democratic National Committee. This oil on canvas 1980 painting is in the National Portrait Gallery.

His Presidency and Credit Unions

Credit unions, as in other segments of the economy, were entering a period of regulatory and market transformation. Carter’s one direct initiative for coops was to ask congress to charter the National Cooperative Bank in 1978. The bank’s purpose was to advocate for America’s cooperatives and their members, with emphasis on serving the needs of communities that are economically challenged.

However, the unique role of credit unions in America’s financial system was not a singular focus.

Rather, changes in the industry during his four years were largely driven by credit union’s specific legislative efforts and external economic events. The destabilization of oil prices led to rising energy costs, increasing inflation and ultimately, the highest interest rates seen in the 20th century. These economic factors helped spark the need and response for the policy of deregulation in multiple sectors of the economy.

NCUA’s Institutional Redesign

Within the federal bureaucracy, Congress re-established the National Credit Union Administration (NCUA) as an independent agency in the executive branch on November 10, 1978 (12 U.S.C. 226).

The NCUA’s Central Liquidity Facility Act (CLF) (12 U.S.C. § 1795) was also created by Congress in 1978. The purpose was to provide credit unions their own source of liquidity similar to the Federal Reserve System’s discount window for banks and the FHLB system for S&L’s.

NCUA’s restructure gave President Carter the opportunity to appoint the three initial board members:

Lawrence Connell, Jr. – The Chairman, had previously been Connecticut Bank Commissioner. He served in the office of the U.S. Comptroller of the Currency (OCC) from 1958 to 1968.

Dr. Harold A. Black – A PhD economist, Dr. Black as a board member brought academic and financial expertise. He helped to integrate his 1962 freshman class at the University of Georgia.

P.A. Mack, Jr. – Served as Vice Chairman. Since 1971 he had been administrative assistant to Indiana Senator Birch Bayh. Mack was reappointed to a second term by President Reagan in 1984.

Connell, center; Black on left; PA Mack on right

This was the administration’s most direct impact on credit unions. It followed the practice that personnel appointments in government are in fact policy. In his Presidential appointments, Carter tried to make the government more representative of the American people. His domestic policy advisor Stuart Eizenstat stated that Carter appointed more women, Black Americans, and Jewish Americans to official positions and judgeships “than all 38 of his predecessors combined.”

In terms of enhanced member services, in 1977 credit unions lobbied Congress to authorize mortgage lending and share certificates for FCU’s, products that had been available in multiple state charters for years.

Economic Forces Precipitate Deregulation

Inflation hit 14% in 1980 and led to ever rising interest rates creating financial crises across major industries dependent on energy and sectors reliant on stable interest rates. These sectors were often subject to government regulations that set consumer prices, or rates paid to savers and charged to borrowers. These regulated industries were often limited in the scope of their services and in turn protected from direct market competitors.

Deregulation of these government-controlled sectors was introduced by the CAB in the airline industry, in long haul trucking, railroads and finally, the national monopoly known as Ma Bell, the AT&T phone company. The Carter administration also deregulated beer production, sparking today’s craft brewing industry.

Financial Services Deregulated

Financial firms reliant on charters and deposit insurance were especially impacted by the sudden and increasingly volatile rise in interest rates. In response, Congress passed the Depository Institutions Deregulation and Monetary Control Act of 1980 (DIDMCA ) signed by President Carter on March 31, 1980. DIDMCA had profound effects on financial institutions, including:

Increased Deposit Insurance: Raised the deposit insurance limit from $40,000 to $100,000 on individual savings accounts.

Authorized Interest-Bearing Transaction Accounts permitting credit unions and savings institutions to offer checking accounts, rather than relying on banks as payable through agents for their “share drafts or NOW accounts.”

Phased Out Interest Rate Ceilings for the banking industry by June of 1987. However, in March 1982 the NCUA board under Chairman Callahan eliminated all constraints on the terms and interest for savings in one regulatory action versus the six-year phased process implemented for S&L’s and banks.

In his signing statement, President Carter made only a brief reference to the bill’s impact on consumers: This is not only a significant step in reducing inflation, but it’s a major victory for savers, and particularly for small savers.

Following the 1980 DIDMCA legislation, NCUA authorized Share Draft Accounts, a service that banks had contested when introduced by state-chartered credit unions earlier in the decade.

A final administrative action triggered by inflation was Executive Order 12201—Credit Control of March 14, 1980. In this order, President Carter granted the Federal Reserve authority to control the growth of credit, including all loans extended by credit unions and other financial intermediaries. The intent was to lower inflation by limiting loan demand growth at the institutional level.

An Agency in Need of Administration

Other than the three NCUA board appointments, President Carter’s administration had little direct comment about the cooperative financial sector.

When Ed Callahan became NCUA Chair in October 1981, the agency was still in a period of reorganization. Agency staff was top heavy in DC with 16 separate offices including a consumer examination program run independently of the six regional offices. There were departments doing tasks and reports the same way as ten years earlier, despite the new challenges of deregulation. Examinations were on a two-year cycle, at best. Semiannual call reports were not collected from all credit unions. The NCUSIF was cash poor and used 208 assistance to help credit unions regain solvency. The CLF had only several of the over 40 corporates as agent members, and only a handful of the almost 16,000 natural person credit unions had joined. There was uncertainty about how the CLF itself would be funded. In brief, the NCUA in 1981 had too much regulation and not enough administration.

Carter’s Legacy

Most of the changes in NCUA structure, the CLF, and even the enhanced mortgage and certificate services were sought by credit unions and underway before Carter took office in January 1977. Credit unions had seen deregulation work at the state level but implementing that policy on a national basis was at best uncertain.

The combination of economic headwinds and changing market competition led CUNA President Jim Williams to say their primary goal was “survival” at the February 1982 GAC conference. In response Chairman Callahan in his first GAC address said the solution was deregulation for credit unions coupled with a simultaneous upgrading of the agency’s supervisory capabilities.

A Leader’s Impact

However Carter’s influence goes far beyond his time as President. While his administrative and policy challenges were not viewed as successful when he left office, his insights and leadership perspective are now being reassessed. For example, his reasons for establishing independent departments for energy and education are now seen as critical to America’s future.

But the most memorable contribution may be his calls to common sense individual accountability. In his 1979 “Crisis of Confidence Speech” he challenged Americans to acknowledge their responsibility for the urgent national economic worries. He said in part:

In a nation that was proud of hard work, strong families, close-knit communities, and our faith in God, too many of us now tend to worship self-indulgence and consumption. Human identity is no longer defined by what one does, but by what one owns. But we’ve discovered that owning things and consuming things does not satisfy our longing for meaning. We’ve learned that piling up material goods cannot fill the emptiness of lives which have no confidence or purpose.

His concern about society’s desire for the bigger, the newest, the “always more” is still a dominant motive today. For a person who grew up on a peanut farm in rural Georgia, lived through the depression, and who left military service to run the farm when his father died, character mattered more than material net worth.

Capitalism promotes and relies on consumer demand. This incessant drive has become endemic in society. When credit union leaders talk about progress in terms of billions, have we lost the cooperative focus on member well-being to the market’s alternative ethos of institutional dominance?

The title of his first book when announcing his intention to run for president was Why Not the Best? It was about renewing the can-do American spirit. The question Carter poses for us is can we invert our thinking about credit unions as successful financial institutions and again see them as a movement by and for the people.

An elegy for Jimmy Carter, Jr.

by Paul Hooker, a retired Presbyterian pastor, presbytery executive, and professor who lives in northeast Georgia

Goodbye, fierce and gentle warrior, farmer with your hands full of good soil. You grew things.

You made your choices for weal and woe, held your power loosely, let it go; asked nothing of others you asked not of yourself.

In extraordinary times, you were an ordinary man — not a hero, not a saint, not a role model. You looked into our eyes and told the truth as best you understood it. We did not listen.

We wanted fairy tales of false greatness, glib promises of never-ending good times, eternal morning in a land immune to night — Lies, all, and so you warned us.

But comforting calumny is easier to hear than stony fact. We turned away to worship at their shiny altars these gods of glory, greed, and gore.

You wavered not an inch from your convictions, smile undimmed by public humiliation; you went back to planting crops in fields where no one else thought they could grow:

Peace in bloodied ground, homes in urban lots, love stretched like a wedding canopy over time and patience and simple faith.

Do not despair. The fields you plowed still wait their harvest. See, even now they bear your quiet fruit.

An unusual approach to assembling a leadership team for a government agency.

Persons interested might review his positions and priorities from a speech on September 9, 2024 to the ACU Congressional Caucus. In the opening paragraph he remarks that his term ends in August 2025 and his search for ideas for his “remaining days:”

Good morning and thank you. This conference is one of my favorites. One reason I’m here is to get ideas on how I should focus the remaining days I have left in this job. Around this time next year, the White House will likely announce a new Board Member. That’s because my term on the NCUA Board ends next August, so I have less than a year left. Whew, I was worried that would be an applause line.

Later he notes his regulatory approach:

in America, you deserve protection from an overbearing government. . .

If NCUA or other agencies ‘get over their skis’ and interfere in the private financial affairs of credit unions and their members, the resulting credit union use of NSF and overdraft services could have the paradoxical effect of limiting access to financial services for those who need it most.

Governments often have coercive powers far beyond any financial institution. . .

I want to mention two fascinating new technologies that we often hear about: Artificial intelligence, and blockchain and digital assets, which includes cryptocurrency. I’ve made clear that the NCUA shouldn’t be a technophobic agency. . .

In reading the full speech, there is no reference to credit unions as cooperatives and any role that design has in his regulatory agenda.

I had the opportunity to listen to a very small slice of NCUA’s Board’s public budget process for 2025-26 by watching the video of the November 21 discussion of the CLF’s spending requests for the next two years.

Although extremely small in the agency’s overall spending totals, I fear we see clearly in this simple example, the board’s inability to substantively assess spending requests.

A Brief Background

Several items from the CLF’s board action memorandum for November 21 provide some background for the hearing including these two points:

The purpose of the CLF is to improve the general financial stability by providing member credit unions with a source of loans to meet their liquidity needs and thereby encourage savings, support consumer and mortgage lending, and provide basic financial resources to all segments of the economy. and,

“(CLF) is owned by its member credit unions and managed by the NCUA Board”

CLF’s budget proposals were for $2,307,863 for 2025 and $2,448,263 for 2026. Salaries and benefits are 96% each year’s requests.

Several facts put this credit union owned public-private effort in perspective.

Total membership is 430, an increase of 32 in 2024, and 9.4 % of all credit unions. CLF’s balance sheet is $966 million and includes $44 million of net worth/retained earnings.

The Board’s Policy Failure

Each board member remarked on some aspect or other of the financials. Otsuka had no questions. She made an unexplained reference to “protecting the insurance fund.” Hauptman called the CLF a “buffer for the American taxpayer” and cited a vague reference to $18 billion of loans sometime in the past.

He reverted to his standard routine of demonstrating how to improve the “user experience” when contacting the CLF. He showed how staff had “made it easier to access” the CLF by removing the on-hold music replaced by an automated telephone routing message. He confirmed that a credit union inquiry would ultimately end at the CLF President’s desk, if no one else picked up the call before then.

He also pointed out that 3,300 credit unions (95% of those under $250 million in assets) had lost access when the special CLF-Corporate membership authority expired. Hauptman opined that credit unions should have multiple liquid cash sources which is how he arranged his personal financial management: “a credit card, home equity line and a margin loan established with a broker.”

As Chair Harper led off the discussion, one would have hoped for a focus on CLF policy and whether its purpose above was being carried out. Instead, he supported the budget in full and noted the 31 increase of members. He did ask about the cost of membership. The 4.46% third quarter member dividend was the only recognition that the CLF’s return to the owners was below market rates including the overnight Fed Funds yield. He again complained about Congress not renewing the special CLF authority for corporates to join by funding only a subset of their members.

Business as Usual While Failing the Owners

A critical capability of any NCUA board member is discernment. What is their understanding of the key issues in a staff presentation, especially when focused primarily on budgets? Is It really about numbers? Or should it be about whether the CLF is serving its owners?

All three board members stated that the CLF existed for the benefit of NCUA and the NCUSIF, not for the credit union funding owners. What are credit unions getting for their direct support of the CLF? In the presentation the number one productivity indicator and primary 2025 Planned Activity goal is to Provide CLF Advances as needed.

However, the CLF has not issued a loan to credit unions since 2009. Almost all of those advances, 15 years earlier, were to two corporates via the NCUSIF. They were very short term and not part of any overall recovery plan. I am ignoring a token $1.0 million mini-advance made to a small credit union in December 2023 and paid off early in 2024.

A Time of System Stress

The lack of credit union support and CLF membership is not a statutory shortcoming. It is a management one, an NCUA responsibility as stated in the staff memo above. During the 2022 and 2023 rising Fed rate cycle, liquidity pressures increased throughout the system. This concern peaked when the Silicon Valley and other bank failures occurred. However the CLF was totally missing in action this entire cycle.

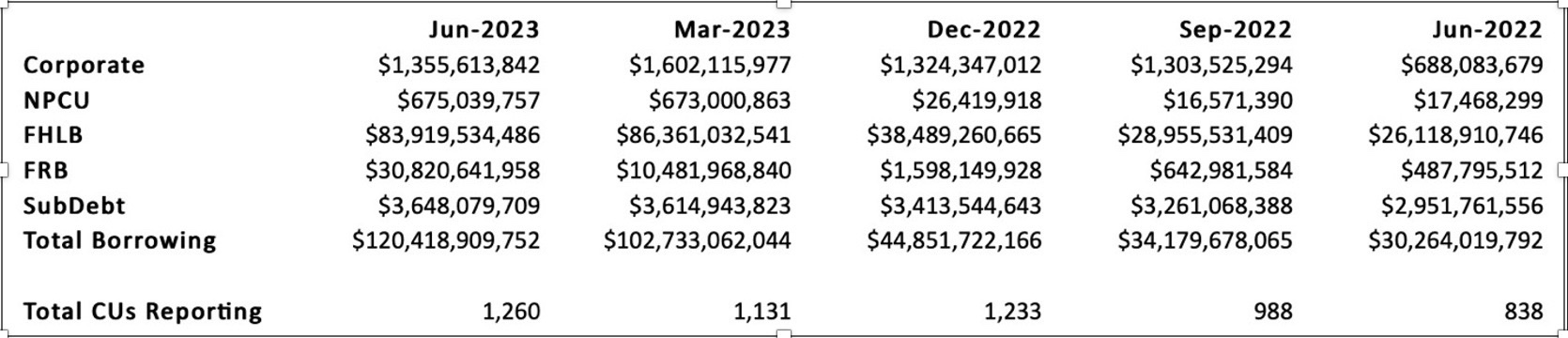

Instead, credit unions borrowed in record amounts from the Federal Reserve’s Bank Term Funding Program (BTFP) and the FHLB’s. For example, the September 2023 call reports show 307 credit unions with Federal Reserve borrowings of $34.9 billion, an average of $114 million. For these credit unions, the Federal Reserve represents 66% of their total borrowings. For 112 of this group, the Federal Reserve is their only source.

Credit union total assets of $2.25 trillion at 3Q 2023 were just 9.7% of total banking assets. However, their participation in the special emergency Federal Reserve lending program equaled 27% of the BTFP’s loans at yearend or three times cooperative’s share of total industry assets. And this Federal Reserve borrowing was only a quarter of all credit union borrowings at the quarter end of $130.3 billion.

During this entire liquidity crisis, the CLF was nowhere to be found, or even heard. No programs, no outreach, no public discussion. And it was not due to a poorly designed website or failure to target market. Rather the CLF’s credit union owners were completely left out and shut out of any role except sending in capital—for a below market return. The agency made no effort to assist credit unions because the board and staff view the CLF as a liquidity partner for the NCUSIF, not the industry.

Why the CLF Has No Interest is a post from May 2024 which shows that the credit union owners have been subsidizing the CLF due to its below market dividends. The CLF’s return is much less that paid by the FHLBs and corporates on their capital accounts. Even though the CLF has investment authority similar to FCU’s, its own portfolio was underwater at 2023 yearend and its yield trailed the overnight FF rate the entire year. But the board ignored those facts.

Credit unions do not view the CLF as a reliable partner in times of balance sheet stress. They have plenty of tested alternatives. Ones that don’t impose supervisory judgments on top of collateral security. The Board’s view of the CLF to serve the NCUSIF has made it a “vestigial organ” within the NCUA body serving no credit union owner-members.

What the Board Could Have Asked Staff

Following are some questions that board members might have asked if they had really focused on the CLF’s policy failures in this most recent period of liquidity need.

How many of CLF’s current members have outstanding loans elsewhere? How much and for how long?

What unused lines do CLF members report on the latest call reports?

Has the CLF developed any proactive lending programs in the two years since the Fed began raising interest rates in 2022? If yes, how were these communicated to owners?

Given the dramatic increases in credit union borrowing in both total dollars and numbers as shown below, what did the CLF do during the crisis? The chart below would be updated as context for the question.

Total Credit Union System Borrowings (June ’22 to June ’23)

Why should the CLF continue as a separate department with a staff of six and overhead charged by the NCUA board, when it could easily be a collateral responsibility with other senior examination and supervision staff?

The failure of NCUA board members to ask the most basic questions about CLF’s non-activity while routinely continuing to increase its spending is disappointing. It undermines the NCUA’s capacity to serve the owners of the fund.

The board has failed in its policy oversight role. With zero lending productivity, why is there any reason for a staff of six to keep lights on? The entire system shows increased liquidity demand and draws but relied entirely on every other contingency funding source while its own funded resource was moot.

If credit unions are to get their money’s worth from the CLF, the agency must show leadership by working with the owners. Contrary to one board member’s assertion, CLF effectiveness does not depend on its members; rather it depends on the management by NCUA. Otherwise, just merge the shop back into the bureaucracy from which it came. Save the credit unions money.

Editor’s footnote: If you want to see how another cooperative designed liquidity lender communicates with its owners, read this latest update from the FHLB’s newsletter.