NCUA’s September board discussions provided much positive information about the state of the industry and the funds credit unions provide to manage the agency.

- Credit unions are performing very well with net income running far ahead of 2020 and delinquencies/charge-offs at very low levels.

- Code 4/5 credit unions continue to decline and account for just .5% of total credit union assets. Code 1/2 CAMEL-rated credit unions are 97.1% of assets.

- There is a projected yearend operating surplus of $28.6 million from both this year’s budget ($15 million) and amounts unspent from 2020 ($14 million).

- Staff projects a yearend NOL for the NCUSIF of 1.28% primarily due to a slowing of insured share growth and low losses.

- Staff will publish the NCUSIF’s investment policy which is how the board oversees the $20 billion fund and its primary revenue driver, the portfolio’s yield.

- Three agenda items were added to the October through December agendas to finalize open proposals.

However, a significant update was overlooked. A result that benefits every credit union is the latest corporate AME financials posted on September 15. Those numbers show a payout to credit unions of $3.158 billion, an increase of $33 million from the March update, or more than the just revealed 2021 operating fund surplus. More details are provided below.

The Surplus Discussions

What will happened to the $28.6 operating fund surplus? Part is being “reprogrammed” i.e. spent. Seven new staff positions were approved which will have a full year’s impact of $1.9 million or $271,000 per position.

Of more significance, three of the positions are to enhance cybersecurity capability and three for the Office of Ethics counsel. One might conclude that the agency sees the vulnerability from its internal ethics issues as equivalent to risks from cybersecurity bad actors.

The NCUSIF’s June NOL calculation of 1.23% continues to significantly understate the actual ratio. As of July 2021 the NCUSIF’s retained earnings are $4.739 billion and insured shares at June 30 are $1.579 trillion. Dividing the two gives an equity ratio of .30 plus the 1% deposit true up required of all credit unions resulting in an NOL ratio of 1.30%. This continued underreporting of the NOL misleads both users and the public about the actual condition and trends in the NCUSIF.

A $176 Million “Cushion”

In several of the financial dialogues the word “cushion” was used to describe the accumulation of funds beyond those needed for operations.

Cushions are nice to have. They bring comfort to hard surfaces or strict budget limits. But credit unions have always worried that once their members’ money was sent to NCUA, it might not come back in NCUSIF dividends or be managed wisely.

At the end of July, the NCUA’s operating fund had a cash balance of $176 million and total fund equity of $139 million. This equity is at the highest level ever. The cash on hand is almost twice the annual operating expenses. Both are the result of NCUA assessing federal credit union operating fees in excess of actual expenses in every year since 2015 when the fund equity was just $38 million.

The $176 million operating fund cash earns minimal interest on its Treasury deposits. If this surplus was held in credit unions, members and the system would have a much higher return.

NCUA has chosen to roll over surpluses instead of returning funds to credit unions, reducing the OTR charged the NCUSIF, or lowering the operating fee to the actual projected net cash outlays. They have become a cushion for management undercutting effective control of both expenses and capital outlays.

Financial Cushions, Corporate Crisis, and Historical Myth Making

The NCUSIF’s current NOL cushion is even larger. Because 80% of the NCUSIF assets are from the 1% credit union deposit, the primary responsibility for NCUA staff is managing the fund’s equity ratio of .2% to .3%. This equity was originally caped at .3%. This was a legal constraint so that NCUA would not spend unconstrained the money credit unions provided in their open-ended, perpetual underwriting role. Amounts above the NOL cap must be returned as a dividend to credit unions.

CUMAA in 1998 gave the Board discretion to set a cap from 1.2% to 1.5%. In 2017 the NCUA Board, for the first time ever, raised the cap to accumulate excess funds above 1.3% from the merger of the TCCUSF. This was after the fund had expensed $748 million from the TCCUSF merger surplus to add to the NCUSIF’s loss reserve to liquidate two taxi medallion credit unions in 2018.

NCUA’s reasons for raising the NOL cap to 1.39% after this loss expense transfer were at best dubious and at worst, just made up. Multiple commentators pointed out these flaws in their comment letters about the TCCUSF merger.

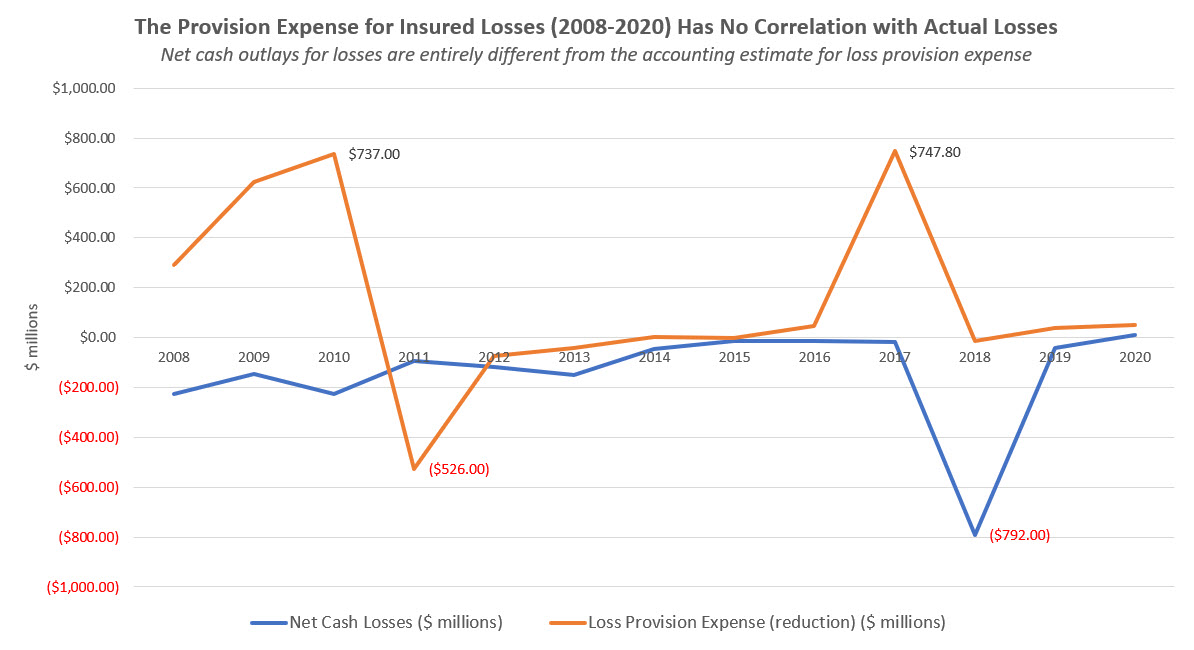

Today each basis point in the NCUSIF is worth $160 million. The 13-year actual loss rate (2008-2020) per insured share is 1.51 basis points. In every year since 2014 the actual cash loss in the NCUSIF has been under .5 basis points except for the taxi medallion liquidations paid in 2018.

Corporate Myth Making

The only push back against this actual loss record is referencing the Corporate debacle in 2009-2010. Chairman Harper again used this recurring trope at Thursday’s meeting. He stated that if Congress had not bailed out the NCUSIF, credit unions would have to write down their 1% deposit by 69 basis points causing a cascading problem in the industry.

Like myth makers in other areas of politics and society today, this fable continues even as facts completely contradict this historical story telling. Today the surplus from the corporate “legacy” assets exceed $6.2 billion and counting. The histrionic 2009 loss projections, made decades into the future, were completely at odds with the external TCCUSF audit results at that time.

The exaggerations reflected the fear and the uncertainty rampant during the crisis, not a considered analysis of options or actual performance. They were the result of “modeling myopia” arising from a complete misdiagnosis of the situation.

The State of the Corporate Resolution Today

Fortunately we know the outcome versus these hyperbolic forecasts. On September 15, 2021, NCUA posted the latest quarterly updates for the five corporate AME’s. It shows total projected recoveries to shareholders of four corporates of $3.158 billion, an increase of $33 million from the March quarter. As of June 30, $2.619 billion of the recoveries were still to be paid.

What is the cost of NCUA’s oversight of the AME’s? The answer: $4.825 billion to manage the P&A’s and all other expenses from the NGN refinancing. Subtracting the legal expenses charged each AME still leaves a total of $3.567 billion the agency expended administering the NGN’s and AME operations. In other words the net legal recoveries would just pay for NCUA’s liquidation expenses.

For comparison the total operating expenses for the NCUSIF from 2008-2020 were only $1.9 billion or half those of the corporate resolution program.

The TCCUSF surplus and fees paid into the NCUSIF over $3.0 billion and the $ 3.2 billion projected payments to shareholders, all come from the legacy assets.

The TCCUSF legislation provided no capital for credit unions. It provided only temporary liquidity draws, all of which credit unions were obligated to repay. The TCCUSF merely set up a separate fund for tracking the corporate resolution and moving the accounting out of the NCUSIF. However, all of the funding for any corporate losses and loan repayments came from a single source: credit unions.

Financial cushions can encourage misjudgments in difficult situations. The challenge today is not the adequacy of the historically validated NCUSIF structure and an NOL of 1.3. The real issue is the ability of NCUA to work mutually with credit unions when problems arise to resolve them in the most cost-effective manner.

The typical government instinct is that money can solve any problem. Without effective constraints on spending, NCUA’s solution will be to liquidate problems. Unrestricted spending is the real lesson from the corporate resolution. The results were catastrophic. How many more times must it be learned?