At the January NCUA board meeting staff presented the Agency’s 2023 Annual Performance Plan. It is 43 pages. With many outcomes. As stated in the Chairman Harper’s introduction: We have identified three strategic goals supported by ten strategic objectives and 19 performance goals. To meet these goals and objectives, the NCUA has also identified 45 indicators to measure performance.

Even with these many details, the document has a significant omission. The oversight was not mentioned by any board member. The absence may explain why the agency has been so ineffective in overseeing the most vital component of cooperative design.

The Missing Concept: “Member-owner”

The term member-owner is used once, in the Mission Statement: Protecting the system of cooperative credit and its member-owners through effective chartering, supervision, regulation, and insurance.

The term is never referred to again. Where one might expect to see the concept, instead the words “consumer “and “individual” are inserted. The word member does not even appear in the two highest strategic goals:

Goal 1: Ensure a safe, sound, and viable system of cooperative credit that protects consumers.

Goal 2: Improve the financial well-being of individuals and communities through access to affordable and equitable financial products and services.

Standard Plan Descriptions

The agency self description affirms that “the NCUA is an independent federal agency that insures deposits at federally insured credit unions, protects the members who own credit unions. . . But the protection throughout is interpreted only as consumer compliance. Nowhere is there reference to member-owner rights, interests, responsibilities or even education.

Here are examples of how the agency describes its responsibilities in various sections of the plan:

The NCUA protects consumers through effective supervision and enforcement of federal consumer financial protection laws, regulations, and requirements.

Throughout the year, the NCUA will continue to adjust its examination program and operations to maintain safety and soundness, protect consumers, and ensure compliance with anti-money laundering laws.

Provide timely guidance to the credit union system and examiners related to changes in regulations established to protect consumers.

Monitor consumer complaints and fair lending examination and offsite supervision contact results to guide consumer compliance program development.

Continue to provide a responsive and efficient consumer complaint handling process in the Consumer Assistance Center.

The NCUA will enhance consumer access to affordable, fair, and federally insured financial products and services through the following strategies and initiatives:

Performance Goal 2.1.2 Empower consumers with financial education information.

No Ownership Role or Protection

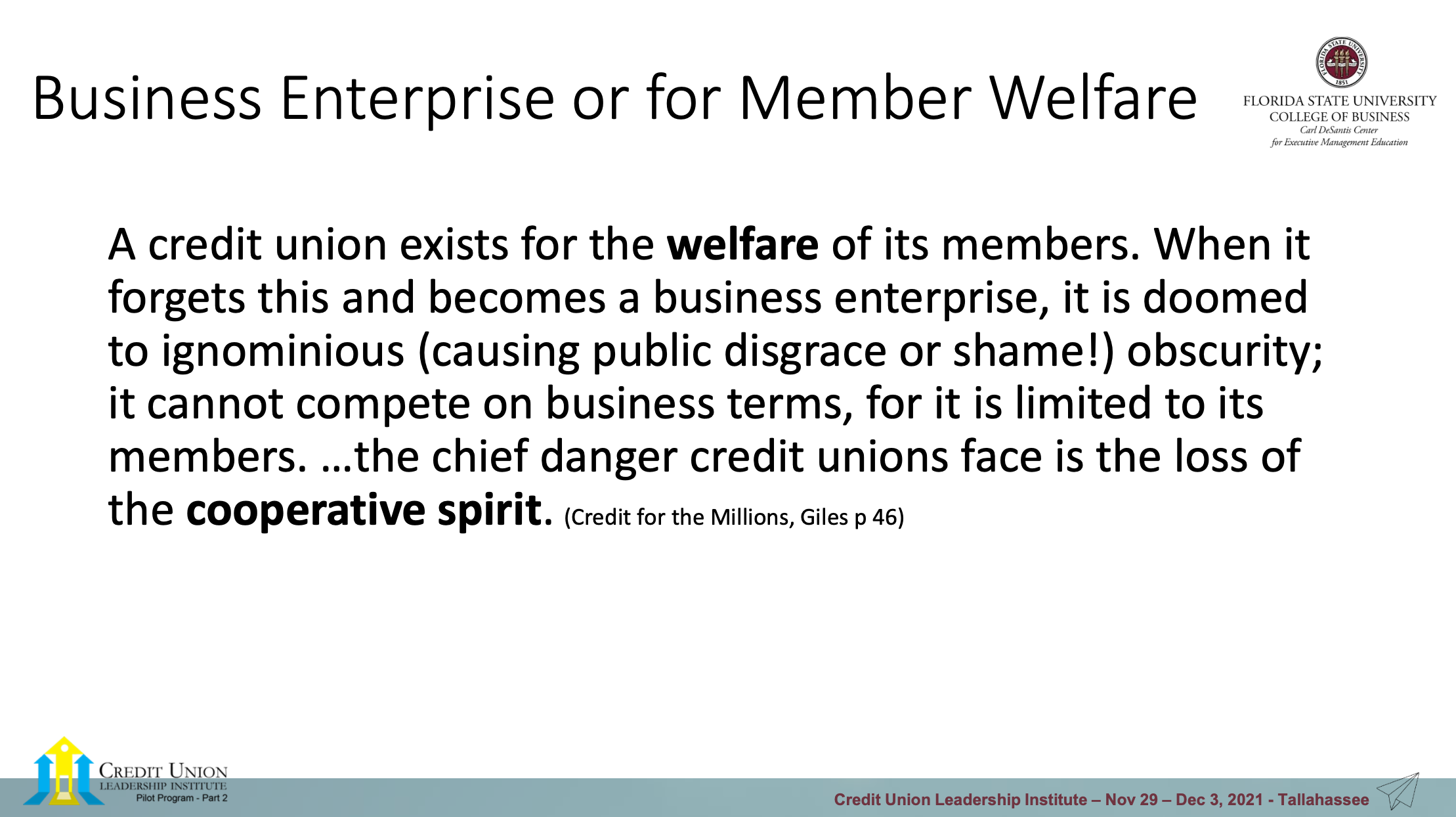

Those who originally organized the coop and their heirs who today own the institution, at least in design, are now nothing more than consumers.

Owners’ rights are not part of NCUA’s oversight. The agency protects “consumers” not owners, and safeguards “individual” not owners’ assets. The agency is nothing more than a cooperative CFPB with a safety and soundness function.

The Most Critical Function of Owners

In NCUA’s plan, member-owners have no standing, no rights and most of all, no regulatory attention. This significant regulatory omission is why some credit unions feel empowered to push all of the boundaries of self-interest and business enterprise with actions disconnected from owners’ well-being and value.

Democratic coop design was intended to be a check and balance, the all important governance process that every organization requires to remain accountable, safe and sound.

Even NCUA asserts it has a governance process: To ensure sound corporate governance, the NCUA will use the following strategies and initiatives: pg 29

The Consequences of No Member Ownership Role

Because of this regulatory omission, intended or otherwise, few credit unions today have any meaningful ownership participation. The organization’s aspirations are only those of the CEOs’ and boards’ ambitions. That often means business enterprise priorities over member welfare.

Credit unions are not subject to their peer’s competitive reviews as would be the case with a publicly traded bank stock. The institutional practices of mergers, sales and buyouts are not subject to any competitive process. Instead these executive transactions are private deals devoid of member input, meaningful public disclosures, no objective benefit and often lacking any economic rationality.

Just as NCUA has eliminated the ownership role of the member from its purview, so have many credit unions. Without owners, just consumers, there is no accountability for institutional performance in theory or practice.

A Dangerous Design

That is a dangerous model. Credit unions increasingly control billions in member funds and their collective savings (equity) in the hundreds of millions of dollars. They increasingly commit to long term projects such as subdebt borrowings, 20-year leases, and long term commercial real estate loans. The final outcomes of these decades’ length transactions may not be known until long past the tenure of the CEO who made the decisions.

Today most credit unions provide little to no transparency of their plans, priorities or projects to members. There are plenty of product and service marketing messages. But rarely are members informed about management’s goals.

The election of directors at the required annual meeting is fixed. There is neither a choice for directors nor director statements of their reasons for serving. Voting is by acclamation.

Without governance and a recognition of the owners’ role, the moral hazard of management decisions using the credit union’s resources increases. Upside risks all benefit the incumbents; but the downside possibility of failure from a bank purchase, national expansion or fintech investment, means the members or NCUSIF will pay the price.

If one believes CEO/Board self restraint is sufficient to ensure members’ best interests, then they have not paid attention to practices such as; the $1.0 million dollar bonus to the manager of a merging credit union; the $10 million transfer of equity to a private foundation; or the change-of-control payments inserted in senior management contracts.

The list of self-serving actions grows daily. Where money management for others is required, greed always lurks.

As just “consumers” or “individuals” member-owners no longer benefit from the most important reason for joining a financial cooperative.

Unless or until there is a meaningful acknowledgment of member ownership and management’s obligations thereto, the credit union system’s uniqueness, not to mention its soundness, will increasingly be at risk.