Philosopher Bertrand Russell wrote almost a century ago, “the fundamental cause of the trouble is that in the modern world the stupid are cocksure while the intelligent are full of doubt.”

Chip Filson

Philosopher Bertrand Russell wrote almost a century ago, “the fundamental cause of the trouble is that in the modern world the stupid are cocksure while the intelligent are full of doubt.”

A recent news story’s headline: Sub’s Leaders Fired after Hitting Mountain.

The article described how the USS Connecticut, one of the fastest, most modern nuclear powered submarines had hit an underwater object described as a “mountain” in October.

The accident injured about a dozen sailors, but the sub navigated on its own back to Guam for a damage assessment.

One immediate result of the event is that the commander of the fast-attack sub, the executive officer and the senior enlisted Master Chief were all relieved of their duties. Vice Adm. Karl Thomas, commander of US 7th Fleet, determined that “sound judgment, prudent decision-making and adherence to required procedures in navigation planning, watch team execution and risk management could have prevented the incident,”

From the first day of active duty, every member of the military learns about responsibility and accountability. From the ordinary tasks of getting up, wearing the uniform, or cleaning a work area, everything is subject to inspection.

All responsibilities come with accountability. And when performance is above average there are awards and recognition beyond a positive fitness report. But there is also the reprimand in the file when something goes wrong. I received both in my four plus years of active duty.

I received the Navy Commendation Medal as Supply Officer during combat support operations:

“His outstanding managerial abilities combines with a ceaseless drive to accept and surmount challenges resulted in the establishment of many services for task group ONE SIXTEEN POINT ONE personal (the Navy Seal Team at Solid Anchor) that were not previously available. Filson’s leadership and devotion to duty reflected great credit upon himself and were in keeping with the highest traditions of the United States Naval Service.”

Fitness reports recommended “accelerated promotion and augmentation to the regular Navy.”

But there was also the letter of reprimand in the file. Upon being relieved as Supply Officer to transfer to shore duty, the audit of the ship’s store inventory found a shortage of $1,850. After repeated recounts, there was no explanation, but the event occurred on my watch.

Many think of military duty as primarily combat. I was a gunfire control officer. Several times this meant telling everyone to clear the mount so a sailor can take a 3 inch 50 round that failed fire and throw the dud over the side. Or the evening the siren’s sounded at Solid Anchor, the phosphorous flares suspended from tiny parachutes to light up the perimeter, the immediate scrambling of the two gunship helicopters, and running in night clothes to the bunkers built with sandbags.

These moments were the exceptions from much of the daily routine. Nevertheless, the concepts of responsibility and accountability applied to all our activities. Captain Mann personally signed off on every communication from the ship that I authored. He explained the only way his commanding officer knew how he was doing was from reading the ship’s traffic and whether the we arrived and departed port on time.

The military gave me the chance to meet some of the most honorable, decent, and effective people I have ever known. When I left banking to join Ed Callahan and Bucky Sebastian, it was not my thought to seek a government career. Rather it was seeing in them the same qualities that make the military service special. They believed that government employees are responsible to the public, that wise stewardship of resources is expected, and that everyone will be accountable for their duty. Success was always a team effort.

Government service for them was not about political ideology or power. Rather it was about serving the public. When Ed announced the three of us were leaving NCUA in 1985 to form an undefined new company, he explained that we had accomplished what we came to do at NCUA, and it was time to move on. Just like service in the military.

Yesterday I received a member notice dated November 4, 2021 announcing the proposed merger of the $457 million Heritage Credit Union with the $3.7 billion Connexus, both in Wisconsin. Each is very strong financially.

The required disclosures say that the Heritage President, a 40-year employee, will retire immediately after the merger. The additional benefits she will receive for her final action includes a $487,546 payment due as employment contract runs through 3/2/2023; continuing health care benefits of $1,750 per month through age 65; a lump sum payment on her 457(f) in the amount of $425,282; and a merger clause payout per her employment contract of $326,284. The total of the additional compensation known amounts is $1.239 million plus the monthly health benefits.

The practice of a retiring CEO selling the credit union as a final effort to create a personal golden parachute is not new. The most troubling aspect is the leadership failure by both the CEO and board ending all that Heritage had enabled–the shutting down of independent career opportunities for 124 employees, the ending of local relationships in 12 communities, and the betrayal 29,000 members’ loyalty first begun in 1934. This action is the antithesis of the credit union’s founding story on their web site-an event that enabled the professional leadership opportunities the CEO and board have enjoyed for decades.

But it takes two parties to make a deal. Connexus’ CEO and board agreed to these sale terms, issuing a joint press release. Merger math is simple: 1 + 1 = 1. The cupidity of the one side is matched by the morally comatose on the other. Members are not dumb. They see the self- dealing and loss of their Heritage.

Moreover employees of both organizations will look past the superficial statements of what’s in it for them. They will ask is this the kind of organization, leadership and values to which I want to be a part of?

This additional example of self-enrichment trumping fiduciary responsibility is even more troubling because the regulators-both state and NCUA-routinely sign off on these self-enrichment practices.

The concepts of responsibility and accountability have traditionally been the hallmark of effective public service—professionals in their conduct and expertise and conscientious in their duty.

The military’s example, combining honorable service with accountable conduct, is something we properly salute. We celebrate the values inherent in this public duty. But these concepts should not be limited to military employees.

The credit union system could stand much taller and be more potent if the traditions of honorable service that created the $2 trillion system today, were followed by those responsible for overseeing its conduct today.

The logic of mergers like Heritage and Connexus is nothing more than simple monopoly capitalism. Members become the means to growing ever larger, not the reason for the cooperative’s creation. Management’s self-interest has usurped member’s best interest.

A good first step would be to learn from the Navy example. There is an obvious regulatory shortcoming of “sound judgment, prudent decision-making and adherence to required procedures.” There needs to be “relief of duties.”

But that would take leadership at the top. Leadership that can distinguish cooperative purpose from corporate capitalism. And that remembers the values and commitments that created the credit union alternative in the first place.

Veterans Day tributes remind all of us what really matters in life, especially by those who aspire to public service.

At September 30, the credit union system’s net worth was 10%, or 300 basis points above the 7% well capitalized level.

Bank’s simple core capital ratio at June 30 is 8.83%. But comparing these two ratios is extremely misleading. For $1 of credit union reserves is much more valuable than $1 of bank capital.

Here’s why.

Credit union reserves (equity) is from retained earnings which is free in two senses of the term. Unlike banks, credit unions pay no taxes on their earnings. Whereas banks are subject to whatever their marginal tax rate is on each $1 of earnings.

As of June 30 banks pretax ROA was 1.67 for the first six months, but actual ROA was 1.31 after tax. It takes a $1.27 of net income, on average, for a bank to add $1 to retained earnings.

For credit unions, every $1 of net income adds in full to reserves. The same $1 in bank net income will, on average, convert to .78 cents of additional equity.

Banks have multiple sources of capital options. Of the second quarter’s $55.3 billion increase in bank capital, 40% came from additional stock and 60% from retained earnings.

But simple share capital comes with a price and longer term expectation. The price is whatever the dividend paying practice is for the bank. That is, the bank pays rent to use their owner’s capital.

At June 30, banks paid 51.9% of their earnings in dividends. Credit unions have no such “dividend” requirement, so it is “free” or no cost, in this second meaning as well.

Moreover, bank owners expect to see the value of their shares appreciate over time, a factor easily monitored by the daily stock price. Or through comparisons with multiple bank stock indices.

If a bank’s stock price falls below these industry indicators over time, investors can sell, sometimes to owners who will seek better returns or new management.

So when anyone starts to equate credit union reserve levels with bank capital ratios as an industry standard applicable to all, it is a false comparison.

The purpose of cooperative design is to provide financial services in the member’s best interest. One of the advantages credit unions have meeting this goal is that there is no conflict between the returns to owners and the benefits offered consumers. They are one and the same. In banking this tradeoff occurs continuously.

Credit union’s capital advantages versus banks are real and measurable. False comparisons not only mislead credit unions and the public; but it has the paradoxical consequence of causing some to lament the absence of capital options used by banks.

What these advocates miss is the costs of these alternatives and the tensions in allocating income between the returns required by capital providers and consumer benefit.

Credit union’s simple leverage ratio has worked as an all-sufficient measure of capital adequacy for over 110 years. But its most conclusive advantage noted by one observer is something more: “It’s the genius of simplicity. Any fool can get complicated.”

From a retired 30-year CEO commenting on NCUA’s oversight of loans to credit union executives and directors- (2021).

“I hope NCUA has improved their guidance for loans to Management and the Board of Directors. We merged with a credit union that had a policy that Board members, management and their families could borrow $100,000 each unsecured. When we merged with them we found the Manager, his wife and two sons each borrowed $100,000 as well as the Asst Manager and two directors.

Each went bankrupt and the loans were never paid. When I challenged NCUA, CUMIS and our lawyers, they all said since they went bankrupt, we could not collect from them as long as the Board approved the policy allowing them to borrow up to $100,000 each unsecured. NCUA should have a policy that officials cannot have special terms that the members do not have. “

“. . . it seemed as though we would never escape the attitude that the regulator knows best. . . A dramatic change has taken place in the last few years. We now have a federal regulatory agency which openly concedes that credit union people know more about running credit unions than the agency does. . .

The relationship between credit unions and the regulatory agency is one founded on mutual self-respect, and on the realization that both sides share equally in the responsibility for the survival and future development of credit unions. . .

The nature of the federal bureaucracy being what it is. . .there will be a great amount of inertia to cause it to revert a less creative and less cooperative approach to regulating credit unions.

I would not like to see that happen.”

Frank Wielga, CEO Pennsylvania State Employees credit Union. Source: NCUA 1984 Annual Report

NCUA’s New Logo

“I wish I had kept the phone numbers and emails of CEOs that are now gone from view. Ex-CEOs that could tell me what they had wished they had done when they faced downward curves on the way to the end.

I worry that lessons lost and archived outside our industry are what is needed now.

What did we miss when we justified the NCUA or regulators’ actions to end an organization? What did we miss when no owners really dug into a vote to end a charter? What did we miss when the life-cycles of leaders and volunteers were more important than CUs needing young blood?

What did we miss when we followed models based on scale that left local communities and individuals on the sidelines? What did we miss that are the keys to turning a losing streak back towards winning?

Some might say we missed nothing, we witnessed progress and the natural march towards an industry’s maturation. But that sounds to me like short term winners talking.” (Randy Karnes, 2018)

NCUA was converted to an independent agency with a three-person board in 1977.

The results include 12,000 fewer charters and the elimination of 12,000 CEO’s and volunteer board’s leadership platforms. Their employees lost independent career opportunities as these organizations were shuttered.

The movement’s human capital–enthusiasm, insights and entrepreneurial spirit–has been lessened.

Communities have fewer options. As charters are pulled up by their roots, the movement becomes less diverse, less democratic, more concentrated and remote.

Credit unions are being depleted. No movement can sustain itself built on subtraction rather than addition and multiplication.

In the end there will be no need for an NCUA or logo.

In Illinois, the initial state credit union act prohibited officers and directors from borrowing from their own credit union. The act authorized chapter credit unions to meet those official’s needs as well as serve members of any groups too small to form their own credit union.

When I became Illinois credit union supervisor in 1977, this restriction had been removed. However the concept that persons managing money should be subject to special scrutiny remained. As one colleague noted, one aspect of our job was to keep honest people honest.

Illinois conducted an annual exam of its 1,000 plus charters. An important part of the onsite visit was reviewing all official family loans, their relatives and the travel and other expenses they charged the credit union.

Examiner Normal Glazer looked like a bookkeeper. He wore wire rimmed glasses, was slight of stature, talked in subdued tones and was a long-time state employee. He was a very thorough examiner, who knew accounting and more importantly, the many ways that humans might conceal wrongdoing.

I asked him how he reviewed the loan and savings verifications looking for fictitious accounts. It was simple-he selected a sample of each, and then looked up the names in the phone book. If there was no name, he dug further.

Among Norman’s discoveries was a $1.0 million embezzlement from the Scott Foresman Credit Union where the manager kept a double set of books and accounting ledger cards. When Norman’s tape of the individual ledger cards did not match the GL total, he sensed something was wrong. He refused to accept the “missing cards” explanation and found a completely separate set of ledgers with which he documented the full amount of the loss. CUMIS paid the claim he substantiated.

I cite this Illinois examination practice in support of Board member McWatters and others who have publicly observed that fraud is the most common cause of NCUSIF’s losses.

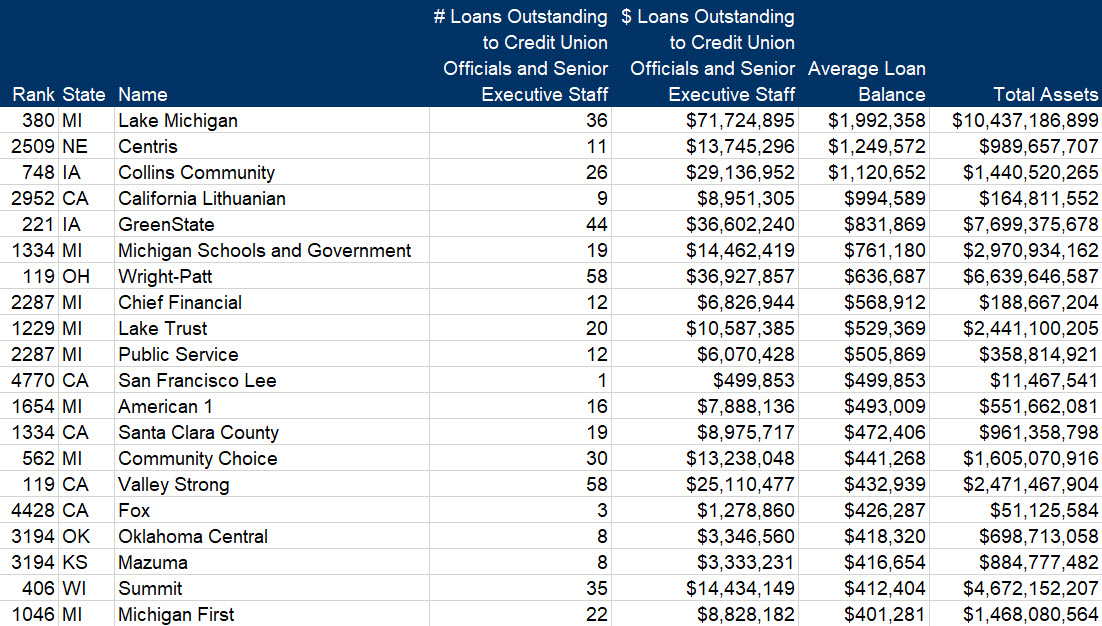

The historical concern about senior managers and directors engaging in self-dealing has a 5300 call report “echo.” Account codes 995 and 996 show the number of loans and total dollar amount to this leadership group. The table below lists the top 20 credit unions by highest average loan balance with total loan numbers and balances as one way of reviewing the data.

This table shows wide variations in this activity even among these 20. The list by itself might prompt some obvious questions; however, the point is NCUA still believes this is an activity for ongoing monitoring—or is it?

NCUA’s largest budgeted amounts and the majority of its workforce are dedicated to on-site exams. One assumes all loans, family related transactions and the expenditures charged by senior staff and directors to the credit union would be reviewed as normal exam protocol.

Reporter Peter Strozniak of the Credit Union Times regularly follows NCUA’s legal filings and court documents. From these records he describes the details of these internal thefts and other employee/director wrongdoing, unfortunately years after the credit unions’ failure. These detailed accounts show that examiners have overlooked extended periods of self-dealing.

A recent example is from the Time’s report of NCUA’s suing CUMIS for recoveries from Melrose Credit Union’s CEO. His October 15, 2021 story described one NCUA claim:

Prior to his 1998 retirement, Herb Kaufman, Kaufman’s father, was Melrose CEO and served as the board’s treasurer. In May of that year, Herb Kaufman became an independent consultant to Melrose under the terms of what the NCUA described as an unusual three-page agreement, which was signed by only one member of the board who turned out to be a life-long and close friend of Herb Kaufman.

The agreement contained a one-year renewable term that paid Herb Kaufman $5,600 a month for his services.

“Despite his obvious conflict of interest, Kaufman aggregated solely to himself the over site within the Melrose Consulting Agreement with his father,” the NCUA lawsuit reads. “Thereafter for more than 18 years, Kaufman covertly caused the renewal of his father’s Consulting Agreement without ever informing the Melrose board or otherwise bringing its continued existence to the attention of the Board.”

According to the NCUA, Herb Kaufman was paid $1,239,795 over 18 years and failed to generate any business for Melrose or provide any meaningful consulting services to the credit union. What’s more, Melrose also paid Herb Kaufman’s travel expenses of more than $26,000 even though his consulting agreement stipulated the travel expenses were to be paid by Herb Kaufman.

The facts offered by NCUA say the Melrose President paid his father (the retired CEO) for 18 years without a fully approved contract.

Assuming an annual NCUA and state exam, this arrangement went un-noted for almost two decades. How could this be? Same last name, monthly checks, a written agreement-it raises the question of what do examiners look at? And NCUA is asking CUMIS to pay up because the bond company should have detected this?

This is not the first time NCUA has sued CUMIS for credit union failures.

On April 23, 2010 NCUA placed the East Lake, Ohio-based St. Paul Croatian FCU in conservatorship with an estimated loss of $170 million, or almost the entire amount of insured shares balance. Loan fraud was among the primary reason for the CU’s collapse.

The IG significant loss report stated:

At St. Paul Croatian FCU, examiners didn’t assess the weakness of the credit union’s internal controls and failed to ensure that the credit union took corrective action on document of resolution issues.

How does NCUA atone for its exam failures? The CU Times report: The NCUA filed a proof of loss claim with CUMIS for nearly $72.5 million (St Paul Croatian FCU). However, because CUMIS’ fidelity bond has a $5 million coverage limit, the amount of money in dispute would be less than 7% of that figure, said Phil Tschudy, a CUNA Mutual Group spokesman.

Between this 2010 St. Paul failure and the October 2021 CUMIS suit for Melrose recovery, there have been repeated cases of significant examination failures over multiple exam cycles. Three of these are described in this post. The information, all from court proceedings, documents CEO embezzlements lasting years. In the CBS Employees FCU case, the CEO fraud extended for two decades resulting in an estimated $40 million loss to the members.

These recurring, costly examples, suggest that NCUA is not doing well its number one job of examination. Examiners should be given a whole new process and trained on reviewing self-dealing activity.

But it is hard for NCUA to fix a problem that is hidden from public scrutiny until years after the fact.

A second challenge is NCUA’s lack of transparency. It provides no information on its supervisory actions. The agency has said nothing about its current conservatorships, one of which is over $4billion in assets. But then years later court proceedings show how extensive and elongated the pattern of misconduct and coincident examination shortcomings were.

Generalized IG critiques of exam failures provide no details of the examiner oversights or any mention of accountability. The response to IG findings is by the same people responsible for the entire process in the first place.

With all the recent public remarks by NCUA leadership about cyber ransomware, cryptocurrency, DEI, climate change and other current “risk” topics, the agency seems unable to perform its most important, historically necessary, oversight function effectively.

Examinations produce pages of financial statements, ratios and trends, and checked boxes for policy adequacy. Almost 97% of credit union assets are held by Code 1 and 2 rated credit unions. The biggest risks are internal, not on the balance sheet.

Examiners should be training for conversations about all forms of self-dealing to see who approved what, when and why. These discussions should be part of the exam record. The topics should be raised and documented in the board exit conference. Without putting these activities in the light of day during exams, everyone presumes it’s OK to keep questionable activities in the dark, and out of the record.

Where is Norman Glazer when credit unions need his sixth sense, or rather common sense? For example he might look at the table above and ponder why are real estate loans to senior credit union personnel so much larger in the lower priced Midwestern states than in any of the more expensive big city coastal markets?

I know he would have challenged a $35 million dollar sinecure committed to a newly organized non-profit by two merging credit unions to support the “advocacy” activities of the CEO who arranged the merger.

The fiduciary concepts of care and loyalty would appear to have been erased from NCUA’s examination and supervision process a long time ago.

Credit union members pay the costs of these failures. However in the long run its is the public reputation of NCUA and the system that is at risk when examinations miss the obvious.

For generations men and women have been rising before dawn to row. These early morning workouts are dark, cold and damp. The sport is far from public view save for infrequent weekend regattas.

The physical and mental sporting challenge can be rewarding. But more unique is the setting–the never ending tableaus of dark nights transforming into colorful mornings of first lights.

Nature as it awakes, monuments bathed in artificial pre-dawn light, and the iconic sight of an “eight” participating in this classic ritual of humans and nature. That is rowing’s aesthetic experience that transcends the physical. And draws people of all ages back to the water.

Dawn’s dramatic opening fanfare

John F Kennedy Center for the Performing Arts

The Georgetown Waterfront

The half-awake moon over the Lincoln Memorial and Washington Monument

Monuments at daybreak

Rowers greet the dawn

Light announces a new day

Photos by Alix Patterson, a life long rower, rowing coach and parent. From high school through college and now in a master’s program on the Potomac River in Washington DC.

Several days ago, NCUA posted the August financial results for the NCUSIF.

The good news is that the fund continues to show positive net income. For the first 8 months the year-to-date net is $122.2 million versus $45.4 for 2020.

However, only 13% of the fund’s $19.2 billion portfolio matures in less than one year.

In contrast, at June 30 credit unions reported 53% of their total investments were under one year. Of that amount over half, or 38% of all investments were in cash and overnights.

Both credit unions and NCUA have access to the same economic forecasts. Why is there such a dramatic difference in how investments are being positioned in this part of the rate cycle?

At the September board meeting CFO Schied promised to publish the NCUSIF’s investment policy in response to a question from a board member. The $1.2 billion reported in new August investments shows why this transparency is so urgent.

The most important monthly decisions by the fund are selecting investment maturities. The board and credit unions should know the assumptions committee members used when making these decisions.

As listed in the NCUSIF financial report:

8/16/21 T – Note 600,000,000 $ 8/15/2028 1.01%

8/26/21 T – Note 100,000,000 $ 8/15/2026 0.84%

8/26/21 T – Note 100,000,000 $ 8/15/2027 0.97%

8/26/21 T – Note 100,000,000 $ 8/15/2028 1.11%

8/26/21 T – Note 100,000,000 $ 8/15/2025 0.66%

8/26/21 T – Note 100,000,000 $ 8/15/2023 0.22%

8/26/21 T – Note 100,000,000 $ 8/15/2024 0.45%

I calculate an average weighted life of 5.7 years and a portfolio yield at .943% for these seven investments.

The critical question is what were the committee’s assumptions that caused them to lock up $1.2 billion for 5.7 years at a yield under 1%. These actions also reduced the overnight account of over $1.0 billion in June to just $230 million in August. It lengthened the portfolio’s average maturity by over 100 days.

The decisions show a seeming absence of any market awareness. Two investments have the same seven-year final maturity. However between the August 16, $600 million first note purchase, and the August 26 $100 million second note at exactly the same maturity, the yield rose 10 basis points!

This 10 basis point lower yield on the first $600 million will cost the fund and credit unions $600,000 per year for seven years, or a total of $4.2 million over the life of the note. How did the committee make such an obviously untimely decision? Why has the committee continued to invest further out the yield curve when the consensus of most economists is that rates will be rising?

Shouldn’t the fund instead be rolling over these notes in 13 week, 6 month or one year Treasury bills yielding .05% to .15% in order to reinvest these funds as the markets move? For example the two year treasury bill has more than doubled in yield from the .22% return NCUA received in August.

I know of no credit union that would have made these investments with this average maturity and this yield with member funds. But that is what the committee did.

At the markets close today, the seven-year treasury note yielded 1.414% and has traded as high as 1.5%.

If the $600 million had yielded 50 basis points higher, this would generate $21.0 million over next seven years for the NCUSIF.

For the quarter the major topic on the economy has been inflation. Is it transient due to temporary structural issues or shooting way beyond the Fed’s 2% target?

The economy’s continued supply shortages are now estimated to extend into mid 2022. Today the Fed will release its interest rate and monetary policy steps going forward. The tapering of bond purchases is expected and many forecasters foresee a Fed rate increase sometime in 2022.

Unfortunately recent NCUSIF investments will be a drag on its revenue for years to come. Continuing to invest in a period of historically low interest rates using the same ladder approach as in years of more normal rates makes no sense. These unusual investment decisions hurt credit unions and their members by causing revenue shortfalls for the fund.

The NCUSIF’s incremental investments should instead be rolled over in very short maturities and then re-invested as rates move into ranges consistent with the yield requirements for the NCUSIF’s operations.

The investment committee is presumably the same senior NCUA officials who oversee examination and supervision priorities. What would their response be to a credit union making these investment decisions?

Timely and transparent presentations of the cooperatively-owned NCUSIF financials is a commitment made by the agency when the 1% underwriting deposit was implemented. Fund results should be posted as soon as they are ready.

There needs to be a discussion in the published report of the investment actions, or none, made during the month. That is one critical way to build confidence in the management of this unique credit union resource. And to insure decisions are made in credit union members’ best interests.

One of history’s many lessons is that organizations, institutions and even countries rarely end their existence because of external forces.

Leadership failures, not competition, cause the demise of most businesses and non-profits.

In the credit union system today it is easy to see examples of this failure of leadership oversight described by Warren Buffett. The technical term for this activity is governance.

Rarely do credit unions have elections for directors; CEO’s end their reign and opt for one more big payday by selling their coop to another; CEO’s buy banks with members’ savings without disclosing relevant details or future returns to their nominal owners; etc.

Here are Buffett’s view of these institutional failures. The question is whether your credit union could be fairly characterized by one, or all?

How are the member-owners represented in your credit union? Are they are just well-served customers? What is necessary for credit unions to reverse the all too frequent examples of leadership and governance failures now occurring? And accepted as “usual and customary”?

It is not a shortfall of capital that causes most credit unions to turn in their charters. It is the absence of character and awareness of the member’s “common good” by leadership.

When every credit union performance measure is a number, one consequence is that everyone has a price.

Our neighbor’s yards have been filled with signs of the season these past several weeks. They include white ghost-like specters hanging from trees, scattered skeleton parts on lawns, mock tomb stones and the endless variety of orange-lighted pumpkin carvings-some real and others plastic.

Halloween is a secular recognition by costume and irony-trick or treat-of the final reality that we all share.

Our neighbors invite us to join with them around an open, outdoor fire pit with the greeting of “Happy Halloween!” Adults accompany children dressed as multiple characters on their door-to-door hunt for sweets and show.

Yet Halloween is about death’s reality-sort of. One of the most popular poems in England is Thomas Gray’s Elegy Written in a Country Churchyard. It captures the haunting challenge of life observing death.

Published in 1751, the narrator uses the setting of a church’s graveyard to mediate on the inevitable fate of everyone, whether rich or poor, known or unknown, skilled or day laborer. It begins:

The curfew tolls the knell of parting day,

The lowing herd wind slowly o’er the lea,

The plowman homeward plods his weary way,

And leaves the world to darkness and to me.

The poet then enters the churchyard cemetery:

Beneath those rugged elms, that yew-tree’s shade,

Where heaves the turf in many a mould’ring heap,

Each in his narrow cell for ever laid,

The rude forefathers of the hamlet sleep.

The breezy call of incense-breathing Morn,

The swallow twitt’ring from the straw-built shed,

The cock’s shrill clarion, or the echoing horn,

No more shall rouse them from their lowly bed.

The remainder of the poem’s 32 stanza’s is a meditation on the democracy of death no matter one’s station in life. From the poor to the powerful.

Let not Ambition mock their useful toil,

Their homely joys, and destiny obscure;

Nor Grandeur hear with a disdainful smile

The short and simple annals of the poor.

The boast of heraldry, the pomp of pow’r,

And all that beauty, all that wealth e’er gave,

Awaits alike th’ inevitable hour.

The paths of glory lead but to the grave.

The complete poem can be found here.

Happy Halloween!?