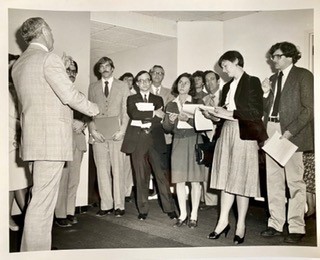

One of the vital initiatives Ed Callahan took as Chairman of NCUA was to take the monthly public board meetings “on the road.” Over a period of two and half years, public board meetings wewre held in all six regions. Often in locations that coincided with already planned league or national conferences.

For example the July 1982 board meeting was held in Chicago at the same time as NAFCU’s annual meeting. That was the same weekend that the Penn Square bank failure occurred. Because of credit union investments with uninsured Penn Square Bank CD’s, the Board meetingt attracted widespread interest.

Constituents Meeting Their Regulators

The purpose of these outside the beltway public events was to give credit unions a chance to attend meetings and see the board at work. In addition the visits often involved credit union conversations, local newspaper interviews, all which raised the profile of the credit union system and the movements embrace of deregulation. The visit from DC raised the profile of an areas credit unions and their contributions to their their communities.

These interactions created awareness of NCUA’s activity and leadership. It gave senior DC based staff direct conversations with credit union leaders on their home turf and in the various economic circumstances around the country.

Each board meeting was followed by an open press conference where Chairman Callahan and staff would answ questins from the media and credit union attendees.

Today’s Public Meetings

Yesterday’s NCUA board meeting was broadcast live, an effort going back years and accelerated by COVID’s cancellation of inperson events. It is a practical way for many to watch a distant public meeting live or later by video. While interaction is not sought, the slides and other presentation data can be downloaded by viewers.

Decades later this board live broadcast have replaced the on-the-road visibility which was discontinued after Chairman Callahan’s tenure ended in 1985.

But does it make a difference whether Board meetings are viewed via digital broadcast or in person in a physical serrting?

Why In-Person Matters

Tim Calkins is a marketing professor at Northwestern University’s Kellog Management School. He uses remote learning sessions in both his class room lectures and private consulting assignments.

The Covid epidemic nade virtual delivery a necessity. The use of remote, live virtual meetings has continued as an accepted option for many organizational inernal management meetings as well as public events such as member annual meetings. Sessions can be interactive and seemingly similar in content to in-person events with the same purpose.

Moreover, virtual events can be a more effective use of time by both presenter(s) and participants. No travel, recordings can be made at once, and AI edit summaries produced. The reach can be unlimited by audience size, location, or time zone. What’s not to like?

Following is Tim Calkins’ assessment of why in-person still brings benefits that virtual sessions cannot duplicate from an article he posted last week:

The Project

Over the past quarter, I’ve had the chance to work with a leading company on a competitive situation. There were new entrants in their industry and the company was formulating a response. This was partly a strategy question and partly a political question: getting the team and the senior people on board.

I did the project remotely. I taught a class session for the team on Zoom, had multiple phone calls and then participated in two team planning sessions in a hybrid format.

The Problem

The project is winding down, and I’m not feeling great about it. I think I made a positive contribution, but not as much as I could have, for a very simple reason: I wasn’t there.

This wasn’t a problem for the class session; I can teach effectively on Zoom. It was definitely a limitation in the work session.

There were lots of problems with being remote. The first issue was that I couldn’t hear much of the conversation; I was picking up about 60% of the discussion. I could follow along but I missed some of the context. Then, it wasn’t easy for me to jump in; I didn’t know how I was showing up in the room, so I found it awkward to make a comment. I also couldn’t read the room. I couldn’t see how my comments were being received. Were people nodding and agreeing? Or rolling their eyes?

Perhaps most important, I wasn’t there for the open times: before the meeting, during the breaks, after the meeting. These liminal times are critical when it comes to influencing and building relationships. During a break one can follow-up on a comment, ask a question to clarify a point or just build a relationship.

In hindsight, I should have insisted that to take on the project, I had to travel to the company for the key meetings.

I didn’t do this because my schedule has been hectic, so travel would not have been easy. And the company didn’t request it; they routinely did hybrid and remote meetings.

The Learning

My takeaway is simple: don’t do a strategic project if you can’t be physically present.

I don’t need to take on company projects; I only accept a new program when I think I can add value and will learn something.

Going forward, I’ll pick and choose with a bit more care. I’ll still teach remotely, but I’ll only do strategy working meetings when I can be in the room.

The Opportunity for NCUA or Any Board with Public Accountablity

Might a new NCUA Chairman revisit the idea of taking Board meetings on the road? Such events could accelerate relationships, learning about local credit union circumstances and most importantly, building trust that can only be created person to person.

If a credit union improves its capital ratio while its members’ average credit score drops, did it have a good year?

We don’t have a standard way to answer that and I think that’s a problem.

Financial health metrics for institutions are mature, required, and reported quarterly. Member financial health metrics are voluntary, inconsistent, and often absent.

To my credit union colleagues: