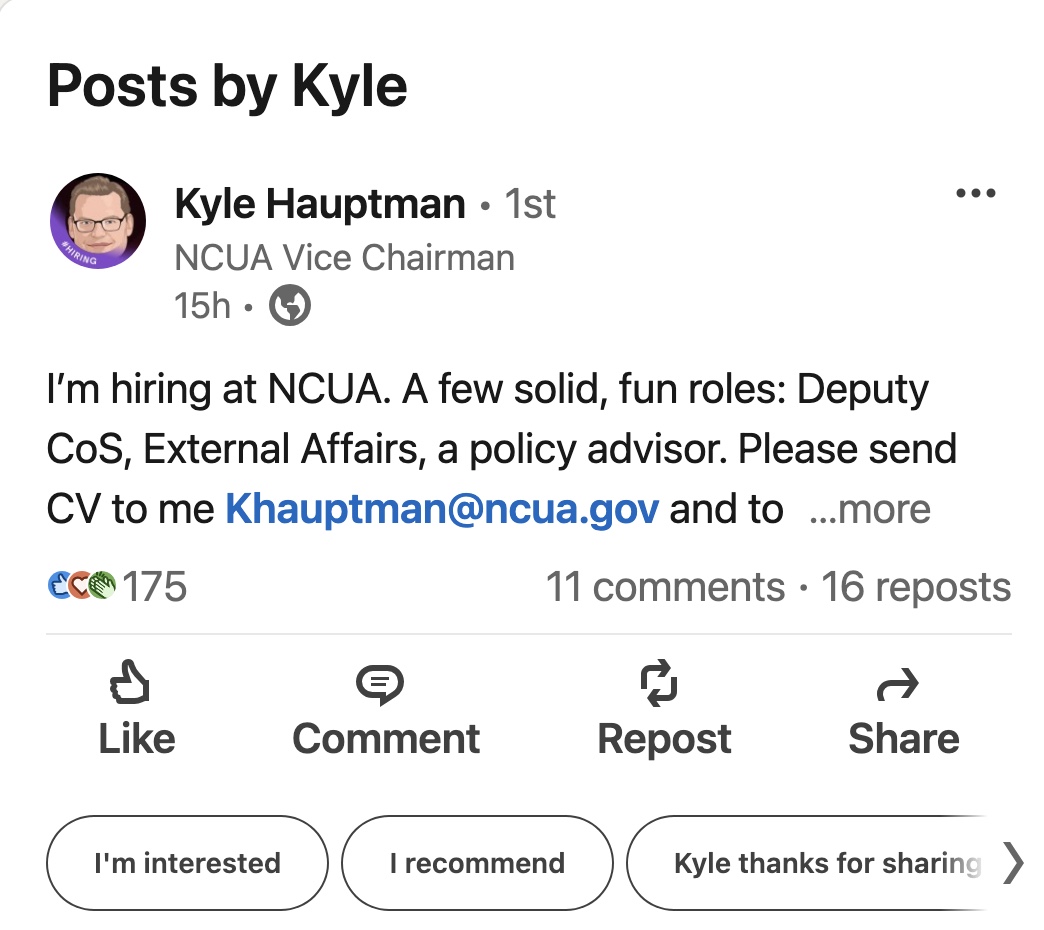

An unusual approach to assembling a leadership team for a government agency.

Persons interested might review his positions and priorities from a speech on September 9, 2024 to the ACU Congressional Caucus. In the opening paragraph he remarks that his term ends in August 2025 and his search for ideas for his “remaining days:”

Good morning and thank you. This conference is one of my favorites. One reason I’m here is to get ideas on how I should focus the remaining days I have left in this job. Around this time next year, the White House will likely announce a new Board Member. That’s because my term on the NCUA Board ends next August, so I have less than a year left. Whew, I was worried that would be an applause line.

Later he notes his regulatory approach:

in America, you deserve protection from an overbearing government. . .

If NCUA or other agencies ‘get over their skis’ and interfere in the private financial affairs of credit unions and their members, the resulting credit union use of NSF and overdraft services could have the paradoxical effect of limiting access to financial services for those who need it most.

Governments often have coercive powers far beyond any financial institution. . .

I want to mention two fascinating new technologies that we often hear about: Artificial intelligence, and blockchain and digital assets, which includes cryptocurrency. I’ve made clear that the NCUA shouldn’t be a technophobic agency. . .

In reading the full speech, there is no reference to credit unions as cooperatives and any role that design has in his regulatory agenda.

I had the opportunity to listen to a very small slice of NCUA’s Board’s public budget process for 2025-26 by watching the video of the November 21 discussion of the CLF’s spending requests for the next two years.

Although extremely small in the agency’s overall spending totals, I fear we see clearly in this simple example, the board’s inability to substantively assess spending requests.

A Brief Background

Several items from the CLF’s board action memorandum for November 21 provide some background for the hearing including these two points:

The purpose of the CLF is to improve the general financial stability by providing member credit unions with a source of loans to meet their liquidity needs and thereby encourage savings, support consumer and mortgage lending, and provide basic financial resources to all segments of the economy. and,

“(CLF) is owned by its member credit unions and managed by the NCUA Board”

CLF’s budget proposals were for $2,307,863 for 2025 and $2,448,263 for 2026. Salaries and benefits are 96% each year’s requests.

Several facts put this credit union owned public-private effort in perspective.

Total membership is 430, an increase of 32 in 2024, and 9.4 % of all credit unions. CLF’s balance sheet is $966 million and includes $44 million of net worth/retained earnings.

The Board’s Policy Failure

Each board member remarked on some aspect or other of the financials. Otsuka had no questions. She made an unexplained reference to “protecting the insurance fund.” Hauptman called the CLF a “buffer for the American taxpayer” and cited a vague reference to $18 billion of loans sometime in the past.

He reverted to his standard routine of demonstrating how to improve the “user experience” when contacting the CLF. He showed how staff had “made it easier to access” the CLF by removing the on-hold music replaced by an automated telephone routing message. He confirmed that a credit union inquiry would ultimately end at the CLF President’s desk, if no one else picked up the call before then.

He also pointed out that 3,300 credit unions (95% of those under $250 million in assets) had lost access when the special CLF-Corporate membership authority expired. Hauptman opined that credit unions should have multiple liquid cash sources which is how he arranged his personal financial management: “a credit card, home equity line and a margin loan established with a broker.”

As Chair Harper led off the discussion, one would have hoped for a focus on CLF policy and whether its purpose above was being carried out. Instead, he supported the budget in full and noted the 31 increase of members. He did ask about the cost of membership. The 4.46% third quarter member dividend was the only recognition that the CLF’s return to the owners was below market rates including the overnight Fed Funds yield. He again complained about Congress not renewing the special CLF authority for corporates to join by funding only a subset of their members.

Business as Usual While Failing the Owners

A critical capability of any NCUA board member is discernment. What is their understanding of the key issues in a staff presentation, especially when focused primarily on budgets? Is It really about numbers? Or should it be about whether the CLF is serving its owners?

All three board members stated that the CLF existed for the benefit of NCUA and the NCUSIF, not for the credit union funding owners. What are credit unions getting for their direct support of the CLF? In the presentation the number one productivity indicator and primary 2025 Planned Activity goal is to Provide CLF Advances as needed.

However, the CLF has not issued a loan to credit unions since 2009. Almost all of those advances, 15 years earlier, were to two corporates via the NCUSIF. They were very short term and not part of any overall recovery plan. I am ignoring a token $1.0 million mini-advance made to a small credit union in December 2023 and paid off early in 2024.

A Time of System Stress

The lack of credit union support and CLF membership is not a statutory shortcoming. It is a management one, an NCUA responsibility as stated in the staff memo above. During the 2022 and 2023 rising Fed rate cycle, liquidity pressures increased throughout the system. This concern peaked when the Silicon Valley and other bank failures occurred. However the CLF was totally missing in action this entire cycle.

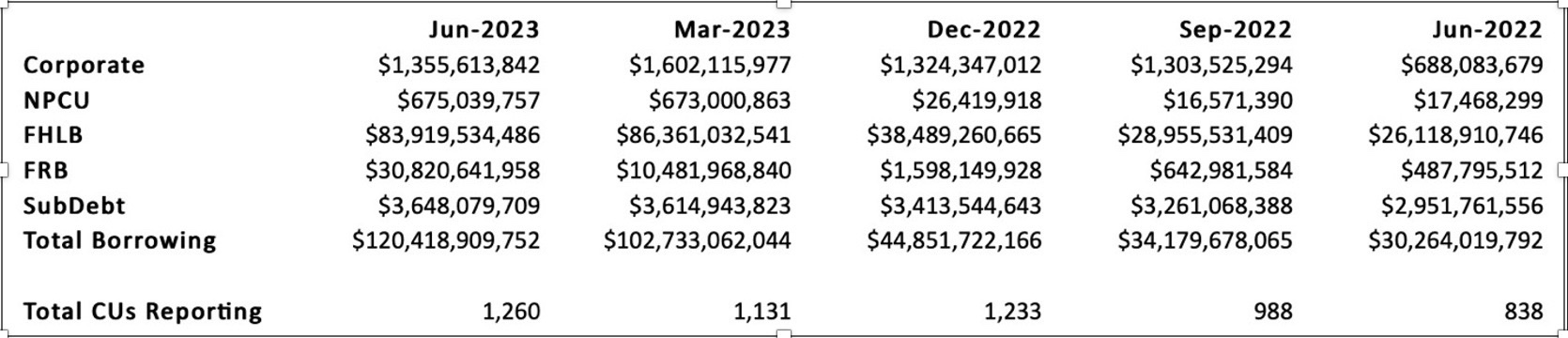

Instead, credit unions borrowed in record amounts from the Federal Reserve’s Bank Term Funding Program (BTFP) and the FHLB’s. For example, the September 2023 call reports show 307 credit unions with Federal Reserve borrowings of $34.9 billion, an average of $114 million. For these credit unions, the Federal Reserve represents 66% of their total borrowings. For 112 of this group, the Federal Reserve is their only source.

Credit union total assets of $2.25 trillion at 3Q 2023 were just 9.7% of total banking assets. However, their participation in the special emergency Federal Reserve lending program equaled 27% of the BTFP’s loans at yearend or three times cooperative’s share of total industry assets. And this Federal Reserve borrowing was only a quarter of all credit union borrowings at the quarter end of $130.3 billion.

During this entire liquidity crisis, the CLF was nowhere to be found, or even heard. No programs, no outreach, no public discussion. And it was not due to a poorly designed website or failure to target market. Rather the CLF’s credit union owners were completely left out and shut out of any role except sending in capital—for a below market return. The agency made no effort to assist credit unions because the board and staff view the CLF as a liquidity partner for the NCUSIF, not the industry.

Why the CLF Has No Interest is a post from May 2024 which shows that the credit union owners have been subsidizing the CLF due to its below market dividends. The CLF’s return is much less that paid by the FHLBs and corporates on their capital accounts. Even though the CLF has investment authority similar to FCU’s, its own portfolio was underwater at 2023 yearend and its yield trailed the overnight FF rate the entire year. But the board ignored those facts.

Credit unions do not view the CLF as a reliable partner in times of balance sheet stress. They have plenty of tested alternatives. Ones that don’t impose supervisory judgments on top of collateral security. The Board’s view of the CLF to serve the NCUSIF has made it a “vestigial organ” within the NCUA body serving no credit union owner-members.

What the Board Could Have Asked Staff

Following are some questions that board members might have asked if they had really focused on the CLF’s policy failures in this most recent period of liquidity need.

How many of CLF’s current members have outstanding loans elsewhere? How much and for how long?

What unused lines do CLF members report on the latest call reports?

Has the CLF developed any proactive lending programs in the two years since the Fed began raising interest rates in 2022? If yes, how were these communicated to owners?

Given the dramatic increases in credit union borrowing in both total dollars and numbers as shown below, what did the CLF do during the crisis? The chart below would be updated as context for the question.

Total Credit Union System Borrowings (June ’22 to June ’23)

Why should the CLF continue as a separate department with a staff of six and overhead charged by the NCUA board, when it could easily be a collateral responsibility with other senior examination and supervision staff?

The failure of NCUA board members to ask the most basic questions about CLF’s non-activity while routinely continuing to increase its spending is disappointing. It undermines the NCUA’s capacity to serve the owners of the fund.

The board has failed in its policy oversight role. With zero lending productivity, why is there any reason for a staff of six to keep lights on? The entire system shows increased liquidity demand and draws but relied entirely on every other contingency funding source while its own funded resource was moot.

If credit unions are to get their money’s worth from the CLF, the agency must show leadership by working with the owners. Contrary to one board member’s assertion, CLF effectiveness does not depend on its members; rather it depends on the management by NCUA. Otherwise, just merge the shop back into the bureaucracy from which it came. Save the credit unions money.

Editor’s footnote: If you want to see how another cooperative designed liquidity lender communicates with its owners, read this latest update from the FHLB’s newsletter.

(This is the second of two posts on the first and only National Examiner and Credit Union Conference in December 1984 organized by NCUA. Part one is here.)

In March 1984 when NCUA announced its organization of the first ever National Examiners’ Conference in December in Las Vegas, much skepticism was heard.

The first concern was “You will need professional planners or you’ll never pull it off.” But NCUA central, regional and field staff put the conference together piece by piece without hiring a single consultant.

To get the lowest possible hotel room rate, NCUA booked the MGM Grand Hotel for early December. The critics were not optimistic. “Credit union people will never come to Los Vegas two weeks before Christmas.”

And the ultimate quip, “You think credit unions are going to pay to meet with their regulator?”

Once the marketing started, a limit of two per credit union had to be imposed. As one credit union explained, “I knew it would be a sellout so I reserved 12 slots up front so I could take all my volunteers. We’ve never been to a credit union conference and a lot of things are coming down the line. I thought it was extremely important for them to see what was going on.”

By October the conference limit of 2,500 had sold out. No new registrations were possible. A wait list was set up.

Examiners Come First

More than 900 federal and state examiners and regulators met from Monday through close of business on Tuesday. The goal was sharing experience and expertise. One theme of the conference was the changing economy. America was moving into a new era transitioning from an industrial economy to an information one.

Financial transactions were about moving information for members. Credit unions were at the center of this change. According to the most recent American Banker consumer survey, they had become America’s favorite financial institution.

Chairman Callahan opened these initial sessions saying, “Better trained examiners and better communication between federal and state regulators and credit union officials are essential in a deregulated financial environment. This national conference is a chance to discuss current concerns and share problem solving techniques.”

Some examiners had been on the job for years; others for just months. One commented about this joint effort: “We’ve always been first cousins but never knew each other. I was surpirsed to learn how much we have in common.”

One professional challenge was the increase in examiner responsibility. NCUA had been delegating to the regions and their field staffs greater responsibility for safety and soundness. The need as one NCUA executive stated was “to get close and stay close” to credit unions.

Case studies were presented in breakout sessions to practice analysis and problem solving approaches. The Early Warning system of 1 to 5 ratings was reviewed. NCUA was the first federal regulator to share its individual ratings with the institutions it supervised. Not all agreed this was a good idea. One regional director said some credit union managers used the ratings as a measure of personal performance and for negotiating higher salaries.

Dual chartering came up at several panels. Private coop insurance representatives sat alongside NCUSIF examiners. The focus on choice of charter was critical to the evolution of the credit union system. Share insurance options were an essential component of a meaningful dual charter choice which provided a check and balance on each system’s responsiveness. It was pointed out that deregulation of savings accounts, field of membership options, and broader investment choices had occurred first in individual states before these were adopted in the federal system.

The Grand Convocation

On Wednesday 1,500 volunteers and professionals joined for panels, workshops, and informal conversations. There were over 300 speakers and 60 different breakout sessions. While some of the sessions were repeated, the plenary sessions and many of the panel discussions were filmed, edited and then rebroadcast on the conference’s 24-hour video magazine. These excerpts were shown over the MGM Grand’s in-house television giving attendees a chance to watch sessions they couldn’t make. The broadcasts also included live interviews and comments from attendees.

Major topics included the future of the common bond with a panel of both state and federal regulators; how to monitor investments and find useful information; whether deregulation was beneficial for consumers and financial institutions. Breakouts covered mergers, the role and future of CUSO’s, and changing examiner skills and new analytical data base resources.

Richard Breeden, the Vice President’s Deputy counsel for Financial Institutions, moderated the panel Is the Regulator Obsolete? Will technology and the speed of money transfers make it impossible to track critical changes in a timely way?

Federal Reserve Governor Martha Seeger described how deregulation had changed the role of regulators: “We must think of ourselves as business advisors, not as policemen. To me, examiners and credit union mangers are partners in fostering depositor trust and we have just got to work together in this.”

Popular sessions at both parts of the conference were led by Rex Johnson, the president of a newly charter credit union in Illinois. He had been deputy supervisor for the Chicago office of the DFI before taking over the cu startup. His had provided training for NCUA examiners using actual examples of credit underwriting prior to this conference. Rex’s unique collections of case studies generated a lot of interaction. He noted, “We had a lot of fun in the breakouts, but more important we learned a lot from each other”

The Bottom Line and Bigger Story

One of the guest speakers was former Marquette basketball coach Al McGuire. He remarked: “You’re a family; you’re a team and there’s no “I” in team. Credit unions are on a fast break and have unlimited potential. You must make the maximum effort and you must be together.”

The conference was a gathering where people could translate a belief in themselves and their credit union into practical terms. Comments included: I’d give it four stars , , , because of the enthusiasm of the people and the direct involvement of NCUA Chairman Callahan himself. Usually people at that level don’t become involved. He lit one hell of a fire in Las Vegas.”

That fire was because this first National Conference of examiners, supervisors and credit unions showed that their efforts were all part of a bigger story. Everyone contributes, no matter their credit union’s size or time on the job. What each does individually adds to the greater purpose of the cooperative system in America.

Selected Photos

Dick Ensweiler, President of the Illinois League, Callahan and Board Member Mack. The League presented Ed with a framed motto on his departing for NCUA, that read We Don’t Run Credit Unions. It was in the Chairman’s office at NCUA.

Larry Blanchard then editor or Report on Credit Unions. He worked for Austin Montgomery at NCUA, ran a credit union and has been involved with multiple credit union firms from TruStage to Callahans–still to this day.

Federal Reserve Governor Martha Seeger speaks to the full conference.

NCUA Executive Director Bucky Sebastian with regional directors Carver, Riley and Skyles.

Texas credit union Commissioner Pete Parsons and NASCUS Chair on a panel on dual chartering.

Carmen Hyland, credit union attorney, mother of Gigi. (corrected from first description) Her daughter became counsel for a corporate credit union, NCUA board member and President of the National Credit Union Foundation.

At a reception: Ted Bacino, NCUA Director of the Office of Administration, Laura Rossman, Senior Advisor to PA Mack, and Callahan.

There are two NCUA videos of the conference plus more than 300 more photos if someone wants to use in a more detailed report on the event.

On December 9th, 1984 a unique, one-of-a kind credit union event took place at the MGM Grand Hotel in Las Vegas.

The National Credit Union Examiners Conference was the inspiration of NCUA Chairman Ed Callahan. It reflected his belief that state and federal regulators had common purpose with the credit union community. While each had separate responsibilities their shared goals could best be accomplished through collaboration and continuing communication.

The Operational Context

This unprecedented national initiative was accomplished while NCUA was doing its “day job” overseeing 11,000 FCU’s and monitoring 5,000 state charters with NCUSIF insurance. The agency was in the process of completing an annual exam for all FCU’s for the third consecutive year. CLF membership, in partnership with the corporate system, included all 16,000 credit unions in its liquidity coverage.

The NCUSIF redesign was passed by Congress with complete credit union support. This structural change from cooperative principles created the strongest of all three federally managed funds-a fact still true four decades later.

The 1985 agency budget had been passed in the fall. It slashed spending by 4.9%. This spending cut enabled a third reduction in the FCU operating fee of over 20% for a total of 64% over the three yers. Moreover, it was NCUA resources that underwrote the conference including the attendance by all its field examiners plus regional and DC staff.

The credit union system was moving forward in the market. In August the agency reported credit union loans had grown 26.2% over the 12 months ending in June 1984. Member shares were in their third year of double digit growth following deregulation.

This year was also the 50th Anniversary of the passing of the Federal Credit Union Act, an event celebrated by the agency in many ways, including new chartering and total membership goals.

The Conference Launch

On March 14, 1984 NCUA’s press release announced the initiative: NCUA to Hold First Conference of Federal and State Examiners and Credit Union: It read in part:

“This National conference is a unique opportunity to bring together credit union officials, state and federal credit union examiners and regulators and representatives of the credit union trade associations,” said Chairman Callahan. “It will be a chance to discuss current concerns and share problem-solving techniques. Examiners need to be exposed to a wide range of ideas and procedures that will enable them to do a better job of ensuring the safety and soundness of credit union particularly in a deregulated environment.”

We want to make it possible for the public and private sectors to learn from each other and openly discuss the progress, and problems of the credit union movement.”

A registration card was placed in the NCUA’s 1983 Annual Report sent to every credit union in March 1984. It showed the two sessions, the first with examiners, and then followed with all credit unions joining from December 9 through the 14th.

The May 1984 NCUA News reported why registrants said they would be coming:

Don Beall, President of NASA FCU was quoted: I think this is a welcome relief from the past when we had little opportunity for constructive dialogue with the regulatory. The operational types and examiners live in different worlds.

Robert Sorin, Superintendent of the Ohio Division of Credit unions wrote: “The field staff has never had the opportunity to gather with other state or federal examinders to exchange ideas. . . we want to come away with some new friendships and many new ideas.”

And the price was right. NCUA secured the government room rate of $38 for all participants including spouses. Two people who choose to share a room would pay only $19 apiece.

A registration form was included in the June newsletter. A conference registration packet was mailed to all FCU’s that same month.

The form also announced that the agency had negotiated a substantial airline savings with United and gave a toll-free number for credit unions to call for discounts for Vegas flights.

In September the News headline read Two Per Credit Union Attendance Placed on Conference Attendance. The explanation: “Due to heavy demand, registration is now limited to a maximum of two persons per credit union, a move designed to allow as many credit unions as possible to participate.”

On September 28, 1984 the NCUA announced the conference was sold out. Registrations were coming in at 100 per week and the 2,500 person room capacity limit was reached two months ahead of schedule.

“We are thrilled but not surprised by this tremendous response. Credit unions were quick to recognize this will be the kind of learning opportunity they just can’t get anywhere else,” said Chairman Callahan.

The Conference Speakers

The conference schedule offered over 60 different panels, workshops and case studies. The sessions speakers included all three NCUA board members plus Federal Reserve Board Governor Martha Seger; Richard Breeden, staff director to the Vice President’s task Group on Regulations of Financial Services; former NCUA board chair Larry Connell, former FHLB Chair Richard Pratt, former NCUA board member Harold Black and Al McGuire former Marquette basketball coach, and current NBC sports analyst.

When the conference agenda was finalized, more than 300 speakers and panelists were listed including federal and state regulators, leading credit union professionals and trade associations officials.

In posts later this week, I will present some of the content offered and photos. I believe this will illustrate the unique charater and significance of this extraordinary event.

The Conference’s Significance

This National Conference was a celebration of recent success and a dialogue about the future of the cooperative system. It was not an addition on top of NCUA’s traditional roles of examination, supervision and administration. Rather it was a culmination of the values, practices, and common purpose for how NCUA had been involved with the credit unions since deregulation.

Chairman Callahan believed the single most critical responsibility of a leader was communication, both listening and sharing points of view. From frequent press releases, open press conferences, board meetings on the road, transparent dialogue was the foundation for common industry efforts.

This conference was designed as an optimum opportunity for these exchanges. It was the high point for a new relationship paradigm for NCUA with credit unions. This “tipping point” in the positive and constructive relationships between credit unions and regulators would stay in place substantially until undone by athe Financial crisis in 2008 and thereafter.

Recently I asked a person who has worked with credit unions in the past four decades, what she would like to see in the next NCUA Chair.

Her response: “Someone who cares about us.”

That simple statement felt profound. I circled back to ask how she might know if someone met this criteria.

In her words, the person would not be an outsider. Rather someone who has worked in or with credit unions. An example she cited are those CEO’s today who began their careers as tellers or branch managers to become leading CEO’s. They know the operations and culture that create success from the ground up.

Communications

This person, she said, would reach out and talk with, and more importantly listen to, credit unions.

Credit unions would be included as regulatory policy and priorities are developed. Communication would be ongoing and open. The industry would not be preached to. Rather the system’s success would be celebrated especially with examples that make members’ lives better.

Mutual respect would characterize interactions. The Chair would recognize that not all credit unions perform at the same level. For that is how life works. The multiple legacies of personal time, cooperative resources and member loyalties that are the foundation of today’s cooperative system would be recognized.

What to Avoid

I believe most would agree with these characteristics. But her concern was if the Chair was “an outsider with an agenda.” That can lead to a tendency is to see credit unions as an “enemy” especially when in difficulty, rather than being part of a common cause.

This person reflected “how can you regulate if you keep credit unions at arm’s length?” Or if the appointee has never managed an organization, how can they be expected to do something they have never done before? Put simply, how can you regulate something you know nothing about?”

A Public Conversation on NCUA Leadership Now

The most consequential action by the incoming administration on credit unions will be the appointment of the next NCUA Chair. Hauptman’s term ends in August 2025.

It is easy to speculate how the broader Trump agenda might impact NCUA. There could be spillover from these efforts. However, the opportunity now is to articulate the factors that would characterize a successful NCUA leadership selection. One that would move the cooperative system forward in its special role addressing the needs of members and local communities.

This dialogue should include identifying potential candidates whose backgrounds suggest both experience and competence in leading an organization that has made a difference during their tenure.

Now is the time for those who believe in the cooperative model, to speak up and ask their affiliated organizations to do likewise. Bring forth names of persons who would bring insight and demonstrated competence to the Chair’s role.

For if credit unions and their affiliated organizations fail to express their views, how can the incoming administration see this appointment as anything other than a job for a loyalist?

If credit unions demonstrate their strong interest in this role, that enhances the chances of a meaningful choice for the next four years. And a more productive relationship between NCUA and all its constituents.

The 1980 election of Ronald Reagan brought a spirit of hope and joy for some. For others , deep concern about the future of the federal government’s role.

Recall Reagan’s policy priorities: Supply side economics-tax cuts, defense spending to counter the Soviet Union, tighter money supply, reducing the rate of government spending and deregulation. In August 1981, one of his first dramatic actions was firing 11,345 striking air traffic controllers and banning them from federal service for life after they refused to return to work following a contract dispute. Federal agencies and employees were worried about their future.

The Private Sector Survey on Cost Control (PSSCC), commonly referred to as the Grace Commission, was an investigation requested by President Reagan authorized in Executive Order12369 on June 30, 1982. In doing so President Reagan used the now famous phrase, “Drain the swamp“.[1] The focus was on eliminating waste and inefficiency in the United States federal government. The head of the commission, businessman J. Peter Grace,[2] asked the members of that commission to “Be bold and work like tireless bloodhounds, don’t leave any stone unturned in your search to root out inefficiency.”[3] (Wikipedia)

A year later when the Commission issued its report it called NCUA Board Chairman Edgar Callahan a “role model” for government agency executives. It noted that, “in one year, NCUA cut Agency staff 15% and its budget by 2.5% while maintaining their commitment to preserving the safety and soundness of the credit union industry.” (NCUA1983Annual Report page 3). What was this transformation like?

How NCUA and Credit Unions Fared During Reagan’s First Term

When Reagan took office, inflation for the prior year 1980 was 13.5%. The short-term Fed Funds rate was 13%. Federal Reserve President Volker’s goal was to drive inflation down by raising rates further if necessary.

The NCUA’s new Chairman was Edgar Callahan, whose immediate prior responsibility was over five years as Director of the Department of Financial Institutions in Illinois. DFI supervised over 1,000 state chartered credit unions. At the February 1982 GAC conference, the primary concern for the audience of national attendees was industry survival. Callahan said the response was to put responsibility for fundamental business decisions in the hands of credit union boards and managers, not the regulator. He called this multi-faceted change “deregulation.”

During the next three years NCUA became what the Grace commission described as a model for effective governmental performance.

The following are highlights of how NCUA changed from a November 15, 1984 agency press release titled: FCU Operating Fee Scale Slashed 24%; Third cut in Three Years

The excerpts from this two-page, detailed release describe how this unprecedented reduction was achieved.

The NCUA Board today slashed by 24% the operating fee scale for federal credit unions in 1985, bringing to 64% the fee scale cuts over the past three years.

The dramatic 24% cut will save federal credit unions more than $4.3 million in 1985 and has saved them $14 million since 1983, the first year in NCUA’s history that the fee scale was cut.

“For the third straight year, the efficient operation of the Agency has allowed us to put money into the pockets of federal credit unions, “ said NCUA Chairman Edgar Callahan. “It’s an impressive track record, one that the agency and entire credit union system can be proud of.”

“NCUA is the only federal financial regulatory agency that is assessing its constituents less this year, than it did three years ago and I think that is a tremendous accomplishment,” said NCUA Board Vice Chair P.A. Mack.

Federal credit union operating fees, which are pegged to a sliding scale based on federal credit unions’ assets, are the primary source of funding for the Agency’s operating budget. The fee pays for the Agency’s annual examinations of each federal credit union as well as its chartering, supervisory and administrative activities. NCUA receives no tax dollars. Operating fees, the earnings on the investments of those fees, and insurance premiums are the sole sources of funding for the agency.

(The next six paragraphs show the specific dollar impact on credit unions of different asset sizes including Ft Shafter, Hawaii Federal and State Employees and Navy Federal Credit Unions.)

Continued cost cutting efforts at NCUA, coupled with a projection for robust federal credit union asset growth and increased earnings on NCUA investments are the key elements that made a third consecutive operating fee scale cut possible.

The NCUA board attributed the Agency’s success in keeping costs down to high productivity by NCUA staff, personnel reductions and the shifting of resources from the central offie to the field where they are needed most.

For example, NCUA for the second consecutive year has completed an annual examination of each federal credit union, and achievement not seen since the mid-1970’s. Although total agency employment has been reduced by 15%, the number of examiners has increased to an all-time high (369). Getting back to a once-per-year exam cycle exemplifies the Board’s desire to promote safety and soundness while leaving the management decisions in the hands of each credit union.

The resulting gains in efficiency enabled the Board to reduce the Agency’s fiscal 1984 budget by 4.9%-the biggest cut in the Agency’s history. It was the third straight year the Board approved a total agency budget that was below the previous year’s request.

Federal Credit unions in the six months ended June 30, 1984 had grown 12.5% from $55.5 billion to $61.3 billion.

Taken together, the budget cuts, investment income and credit union growth are expected to leave NCUA’s operating fund with substantially more than it needs to meet its expenses. By slashing 24% from its operating fee schedule, the board is effectively eliminating a $3.4 million surplus. “We believe in returning as much as possible to credit unions,” Chairman Callahan said.

This action is another in a series fiscal and operational improvements the NCUA Board has approved of in the past three years. . . most recently the adoption of rules to revitalize the National Credit Union Share Insurance Fund (NCUSIF) transforming it from the lowest reserved to the strongest of the three federal deposit insurance funds. (End quote)

Some of the Lessons

Chairman Callahan’s leadership at the agency was based on professional competence, experience and pragmatic solutions. Some of his colleagues had worked with him on credit union issues for over five years. Internally Callahan placed responsibility for problem solving with the six regional directors. The agency had become top heavy in D.C. where issues got bogged down between 16 separate offices. He streamlined this structure into two primary responsibilities: an office of administration and the office of programs.

Resources were moved to the field so that an annual exam became the minimum standard for performance. Competence, not seniority or appointment status, were the criteria for responsibility. Mike Riley went from head office to become RD of the largest and most problem challenged region as the youngest RD ever. Rosemary Hardiman was board secretary and Joan Pinkerton, and Sandy Beach led public information and congressional affairs—all were appointees chosen by the previous Chair Larry Connell.

Money was not the most critical resource; it was management talent and willingness to innovate to resolve problems with effective supervision. Staff was provided enhanced training that included Video Network recordings such as Rex Johnson of Lending Solutions, leading sessions with examiners to identify sound and unsound loan underwriting. Another video session was a case study of an actual credit union problem for the agency led by a business school professor.

These efforts were supported by disciplined research, constant dialogue with credit unions and open, frequent communications. New data analytical tools (financial performance reports) from the call report were provided for both examiners and credit unions. NCUA board meetings were taken on the road so credit unions could attend and speak directly with senior staff and board members.

NCUA and credit unions worked collaboratively to transform both the agency-the CLF, the NCUSIF and the exam program-and the credit union system to the new world of open market-based competition. These institutional changes have endured even when subsequent Chairman were chosen from individuals with no coop experience, and several who had just lost a recent election (Senator Jepsen and Congressman Norm D’Amours). The agency staff and administration were comfortable working with the industry even when board members had little or no relevant credit union, regulatory or leadership experience.

Celebrating Success

The high point of this collaborative approach was the largest ever regulator-credit union conference held in December 1984 in Las Vegas, organized by NCUA. All state regulators and examiners and NCUA staff met with over 2,500 credit union attendees to hear from experts and debate the future. I will write more about this seminal event that has never been repeated.

The conference demonstrated the power of cooperatives to share and learn from each other. This was a summit that ushered in over three decades of credit union expansion and resilience as the S&L industry failed and the banking system and FDIC went through multiple bailouts.

The bottom line: as shown by this 1981 transition, new faces can be opportunities for creative leadership and strategic change. The 1981 selection of Ed Callahan as chair enabled NCUA and credit unions to become financial pacesetters for their members and the country. It is the quality of the appointee, not the party, that matters.

One should advocate for a similar considered appointment and proven leadership in this coming transition.

Writing about the future is easy. Rarely do readers look back when events have unfolded. Moreover such forecasts often reflect, not insight or wisdom, but rather one’s own efforts to protect vested interests.

However there are some reference points which can help us think about what a credit union might do going forward into a possible disrupted regulatory future.

Today I will review what Project 2025 says about federal regulation. I could find no direct reference to credit unions although I did not review all 900 pages.

Published in 2023, President-elect Trump has denied association with the ideas presented in the document. More than 100 conservative organizations were involved in its creation. I found the brief section I cite below had over four pages of extensive reference notes.

From page 705:One of the priorities of the incoming Administration should be to restructure the outdated and cumbersome financial regulatory system in order to promote financial innovation, improve regulator efficiency, reduce regulatory costs, close regulatory gaps, eliminate regulatory arbitrage, provide clear statutory authority, consolidate regulatory agencies or reduce the size of government, and increase transparency.

Merging Functions. The new Administration should establish a more streamlined bank and supervision by supporting legislation to merge the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, the National Credit Union Administration, and the Federal Reserve’s non-monetary supervisory and regulatory functions.

U.S. banking law remains stuck in the 1930s regarding which functions financial companies should perform. It was never a good idea either to restrict banks to taking deposits and making loans or to prevent investment banks from taking deposits. Doing so makes markets less stable. All financial intermediaries function by pooling the financial resources of those who want to save and funneling them to others that are willing and able to pay for additional funds. This underlying principle should guide U.S. financial laws.

Policymakers should create new charters for financial firms that eliminate activity restrictions and reduce regulations in return for straightforward higher equity or risk-retention standards. Ultimately, these charters would replace government regulation with competition and market discipline, thereby lowering the risk of future financial crises and improving the ability of individuals to create wealth.

From page 706: Direct government ownership has worsened the risks that government-sponsored enterprises (GSEs) pose to the mortgage market, and stock sales and other reforms should be pursued. Treasury should take the lead in the next President’s legislative vision guided by the following principles:

Fannie Mae and Freddie Mac (both GSEs) must he wound down in an orderly manner.

The Common Securitization Platform57 should be privatized and broadly available.

Barriers to private investment must be removed to pave the way for a robust private market.

The missions of the Federal Housing Administration and the Government National Mortgage Association (“Ginnie Mae“) must he right-sized to serve a defined mission.

(End Quote)

The text also states that Congress should repeal titles of the Dodd-Frank Act that created the Financial Stability Oversight Council (FSOC), a federal government organization which identifies risks, promotes market discipline and responds to emerging threats. Project 2025 defines the FSOC as a “super-regulator tasked with identifying so-called systemically important financial institutions and singling them out for especially stringent regulation.”

A Learning Event: The S&L Dissolution

In the late 1970’s the S&L industry held the largest deposit market share in California, much larger than banking competitors. This was before deregulation. Most depository firms were limited to operating in a single state or in some cases, a single location (Illinois).

Today S&L’s no longer exist as a separate industry even though 555 savings institutions with $1.2 trillion in assets still operated at June 2024. All deposits are FDIC insured. Of the total institutions, 241 are supervised by the OCC, 276 by the FDIC and 37 by the Federal Reserve. While state and federal chartered institutions still function, the system is under federal direction.

While there are many reasons for the loss of the S&L’s as a separate, independent financial segment, the dominant factor was that many of the causes were self-inflicted. These included a loss of special purpose, rapid multistate expansion through acquisitions, and balance sheets weighed down with fixed rate mortgages in a deregulated deposit funding environment after 1981.

After the mid 1990’s, there was no separate FSLIC insurance fund, no Federal Home Loan Bank Board to oversee the industry, and the FHLB liquidity system survived by serving all real estate lenders including credit unions. In most states the mutual charter exists as an anachronism, with no new charters being issued. At the state level supervision is provided by a single banking/financial institutions department.

While external financial events did contribute to the industry’s collapse, competitors did survive and thrive, especially credit unions. At the February 1982 GAC in D.C., CUNA President Jim Williams told new NCUA Chairman Callahan there was only one topic on credit union’s minds: survival.

Together credit unions and NCUA embraced deregulation and the changes in structure and oversight the new environment would require. Hunkering down , protecting existing ways and asking for more funding to address problems was not the approach.

Whether the new administration will be as disruptive of federal regulators as indicated in campaign rhetoric, remains to be seen. The lessons from an earlier era can be helpful: remember who you are and build on what brought success to this point in time.

Many of the factors in the S&L demise were self-initiated with leadership failures. Cooperative success in navigating external changes was accomplished though enhanced collaborative efforts between credit unions and their regulators. not each trying to go their own separate ways.

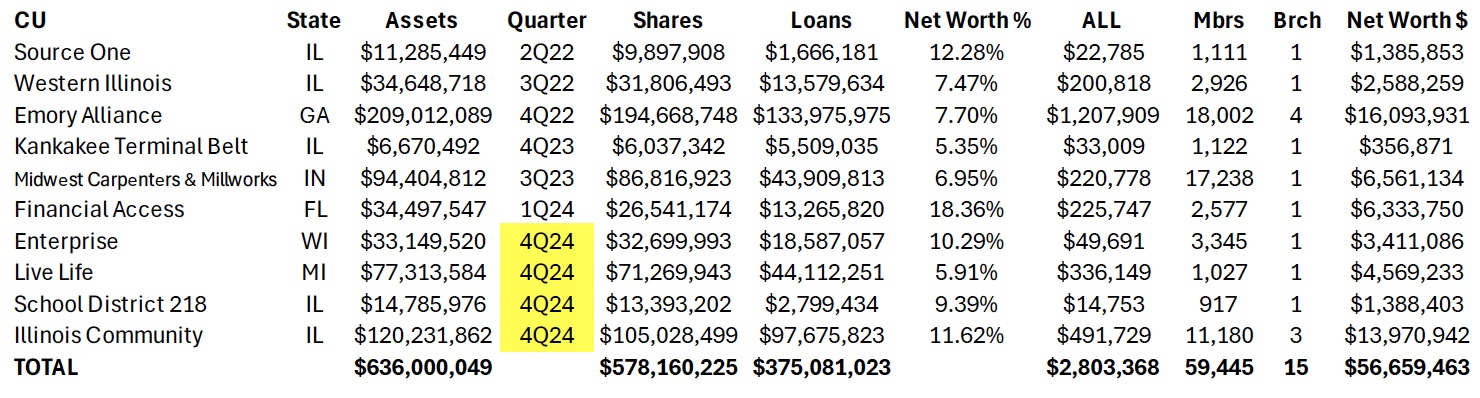

Synopsis:This detailed analysis of Credit Union 1 (Illinois) presents a pattern of declining financial performance covered up by multiple merger acquisitions, one-time sale events and rented capital. The future fortunes of eleven local sound credit unions have been destroyed in just two years. I believe this kind of predatory activity, left unexamined by all those in positions of responsibility, will lead to a reassessment of the advantages of the credit union charter by external legislators.

The article’s length is to present as much of the facts from these events so readers can make their own assessments. The situation summarized is I believe an example of internal industry reckless actions which present a false perception of success. The question for readers is: Does something need to change?

When there are no guardrails for a financial institution, anything goes. It is the law of the jungle; or what some describe as free market capitalism.

The dictionary definition of rogue is “an elephant or other large wild animal driven away or living apart from the herd and having savage or destructivetendencies.” Another reference is to unprincipled behavior by a person or persons.

This word rogue came to mind as I reviewed the activities and results of Credit Union 1 in Lombard, Illinois, since its conversion from ASI share insurance to NCUSIF in February 2022. A summary of the credit union’s merger tempo since this insurer changeover is shown in the following table for the ten already completed or scheduled to be by the 4th quarter of 2024.

In addition, the $12 million Synergy Partners CU, Chicago announced on October 17 a members’ vote for January 2025 to merge with Credit Union 1. That would increase to 11 mergers in only two- and one-half years. These will transfer over $650 million in total assets and over 62,000 members’ financial futures to Credit Union 1’s control.

In its October 2024 Member Notice, Synergy listed 23 Credit Union 1 branch operations in six states including the head office in Lombard, Illinois. The two furthest branches are in Bradenton, FL (1,230 miles) and Henderson, NV (1,750 miles apart).

Other new or ongoing initiatives along with this accelerating merger expansion activity include:

The credit union’s continuing and new sponsorship and marketing promotions with four outside organizations:

The Western Conference tie-in: On October 3, 2024 the Big West Athletic conference announced Credit Union 1 had become its official financial and literacy partner and the entitlement partner for the Mountain West Basketball Championships and all Olympic Sports Championships.

On June 3, 2022 Credit Union 1 announced agreement to purchase the $311 million NorthSide Community Bank, located an hour north from Lombard in Gurnee, IL. Both boards approved the transaction subject to regulatory and bank shareholder approval. The deal was not completed. There was no public explanation.

In May 2023 Credit Union 1 announced it would serve New York cannabis entrepreneurs who plan to open marijuana businesses as part of the state’s CUARD coalition. The same CUTimes article reports, “Credit Union 1 has been selected to participate in the Illinois Department of Commerce’s Cannabis Social Equity Loan Program and is also the preferred banking partner of the Chamber of Cannabis in Las Vegas..”

Even with these multiple marketing and business initiatives, the core of Credit Union 1’s growth efforts are mergers. The operational intensity of acquiring and converting 11 credit unions (six outside Illinois) and all associated member and vendor relationships in just over two years would be a major operational challenge for any organization.

The immediate question is how will the members of the merged credit unions benefit?

In the Member Notices posted on NCUA’s website for these combinations, the wording used under Reasons for Merger, Net Worth and Share Adjustment or distribution are identical. Members’ collective reserves are never distributed to owners even when the merged ratio is higher than Credit Union 1’s.

But zero is not what several of the merging CEO’s and senior staff are gaining.

Rewards for the Enabling CEOs

In the case of the $34.4 million Enterprise CU in Brookfield, WI, the 24-year tenured CEO, Jeff Bashaw, will receive a minimum ten-year contract with a base salary increase of $38,000 on top of his current compensation. I estimated (absent the required 990 IRS filing) that to be a minimum of $125,000 per year plus a $100,000 bonus upon closing. Total minimum amount $$1,350,000.

The credit union is in sound shape at 10.6% net worth, a profitable, single branch with low delinquency. After turning over his CEO responsibility, Bashaw’s role if any will be a branch manager or other honorary title. This ten-year contract with a pay raise seems merely a lengthy sinecure. The 8 employees and 2,815 members receive nothing-except the retiring CFO who will receive a bonus and severance of $110,000.

A Minority Depository Institution Leader?

At the $34 million Financial Access FCU in Bradenton, FL, the situation is more complicated. The credit union prior to merging, reported a 1Q ’24 loss of $517, 310. However, its net worth was still high at 18.4% ($6.4 million) and delinquency of only .39%. Was this a temporary loss or other problem?

In this merger CEO Sherod Halliburton is receiving a total of $3.2 million composed of a bonus of $125,000, an eight-year employment contract at $200,000 per year, and 100% immediate vesting of a $1.5 million split life benefit plan. He no longer has any CEO responsibility as the credit union will become merely a branch operation. The 15 employees and 2,577 members of Financial Access received nothing for their loyalty.

In a CEO Profile published by Inclusiv in February 2022, prior the merger efforts, Halliburton is lauded for his leadership. The article remarks on “his strong community ties and business acumen and how he decided to “bet on me” when offered the CEO position” eight years earlier. Further he points out that he is “one of a limited number of African American men running a financial institution and he accepts the great responsibility accompanying that honor.”

The profile lists his efforts “toward racial equity and responsibility.” He states, “We’ve gone from a somewhat negative perception . . . to now being viewed as a vital part of the economic infrastructure.” The credit union received two technical assistance grants to upgrade technology to meet his goal to double membership in three years. He closes with this affirmation: “We’re here to change lives. I want that to be the enduring message even when I’m gone.”

This Bradenton community credit union which he described as “a vital part of the economic infrastructure” no longer exists. Halliburton is now a Market VP for Credit Union 1 for the next eight years.

An October 2024 Approved Merger

The most recent example of CEOs cashing in is the $116 million Illinois Community CU with over 11% net worth and delinquency of .5%. In this acquisition, CEO Thor Dolan will receive a minimum in immediate total benefits of $1,904,494.

This total is described in the Member Notice as follows: a retention bonus of $150,000; deferred compensation of $50,000; a salary increase of $33,724 added to his 2023 reported 990 compensation of $245,770 or $279,494 per year (no employment length given}; and immediate 100% vesting of a $1,425,000 split dollar 20-year life insurance benefit plan.

This salary increase is despite the fact he is no longer CEO, either managing branches or a regional rep, both with no CEO operating responsibilities. Every additional year he remains employed will add another $280,000 to the package. There is no indication the 38 employees (except the CEO and CFO) gain any assurances of employment; and the 10,482 members receive nothing.

The Fates of the Merged Employees and Members

Each Member merger Notice posted by NCUA which I reviewed includes two standard assertions:

The credit union’s branch location(s) will remain open and become a part of Credit Union 1’s nationwide branch locations.

Employee Representation: Employees of the credit union will be offered employment with Credit Union 1.

However intended, neither of these statements have proved lasting in practice. Comparing the branch listing in the August 2023 Kankakee Valley Notice with the latest listing in the Synergy’s October 2024 Notice, six of the branches in the earlier Notice no longer exist, including three for Emory CU in Georgia and three for Illinois credit unions with single branch operations.

As for employees’ fate, for the twelve months ending June 2024, Credit Union 1 reported a reduction of 67 FTE from 418 to 351.

As a result of Credit Union 1’s merger strategy, there will be eleven fewer local charters which were operating well, a reduction of 70-80 volunteer directors and member committees, and loss of all local relationships and legacy brands.

All member savings and loans, collective capital, liquidity and fixed assets are now in the full control of an institution for which the members have no connection or first-hand knowledge. And in some cases thousands of miles distant. Ironically, Credit Union 1 states in all its promotions that anyone can join, so if members really thought this was a better deal, they could join anytime. But that would be a much harder marketing task than just purchasing the business by paying the CEO—and getting the members’ accounts and accumulated reserves for free.

Members also have a totally new financial institution relationship to navigate. The Credit Uniion 1 material sent to each member post-voting is a 15 page pdf system conversion process and timeline. Member instructions include setting up new payment and loan options, establishing digital accounts and using online financial tools.

Depending on the version usent, the membership agreement for each merged credit union is a minimum and 20 pages. It contains essential information about fees, rates, funds availability, mandatory arbitration and multiple other disclosures which few will be able to read through. The members will learn through experience how everything has changed.

An important difference in Illinois state versus federal charters is the use of proxy voting in all member required elections, including mergers. For Illinois credit unions, proxies are controlled by the board. I did not see this fact disclosed in the FCU mergers, where proxies are not permitted. In essence, FCU members turn their voting governance power over to a new board. These directorst can routinely reappoint themselves without any member vote. More about this later.

Implementing a Capital Markets Strategy-Without the Risk

Credit Union 1’s merger campaign is an adaptation of a traditional capital market strategy of hedge funds and investment firms. Except these buyouts of numerous, smaller independent firms in an industry (think hospitals, barber shops, rental housing, or local HVAC firms) require putting their own capital at risk. These new hedge fund owners then burden their acquired firms with the debt used to finance the buyouts, strip and sell the highest value assets, reduce costs and services to pay for the debt coverage, and ultimately resell the merged business back to the market for a capital gain.

Credit unions reverse this model in mergers—they use the acquired assets, not their own members’ capital, to finance these acquisition sprees. Except when buying banks. The equity in these “mergers” is often transferred in full with no payout to the owner-members. The only necessary sales pitch required is to convince the CEO to bring the board along. There is zero risk to the continuing credit union. The “acquisition” is free. The members lose all their financial and institutional legacy and become subject to the control of a board and CEO that will be completely new to them.

We learn in the Notices that no staff or board due diligence or alternatives is presented. There is rhetoric about “technology and systems that align with members needs.” And, how “internal core values align with our own and . . . confident (that) members will experience a much needed upgrade in the quality of service.” No facts, just vague promises.

These same words were used in the eleven Notices showing the abdication of any director or CEO independent assessment. The words are merely a formula from previous transactions to pass regulatory approval. The members are given no objective measures or specifics that would identify better rates, fees or specific services. Just indefinite promises.

As for core values, institutions don’t have values, people do. So the acquirer’s goal is to find CEOs willing to cash out of their leadership role, rather than evaluate what is in the members’ best interest.

The Numbers Show the Urgency in Credit Union 1’s Merger Efforts

Some readers may believe this is just another example of self-dealing in mergers. It is. But there is a major financial imperative driving this effort.

Credit Union 1 is desperate for mergers not simply for growth, but because its financial performance is a house of cards. For the past five years it has been unable to generate a normal operating net income from its own balance sheet assets. As a result, it has turned to non-operating gains, acquired and borrowed capital (sub debt) and other financial options that disguise its very poor or sometimes non-existent internal rate of return. Here are some of the numbers.

At December 2021, Credit Union 1 had $106.8million net worth ($98.9 Undivided Earnings -UDE- and $8 m other reserves). The net worth ratio was 8.7%. Net income of $13.8 million that year was largely driven by a $7.5 million non-operating gain on sale of fixed assets.

At June 2024, the credit union reports just $88.6 million in undivided earnings, $8 million in other reserves for a total $96.6 million, that is $10 million lower than at December 2021 total.

To report an acceptable net worth ratio the credit union now includes $20.5 million in subordinated debt (borrowed capital), $45.1 million in equity acquired from credit union mergers, and a $7.1 CECL transition reserve. Without these non-operating additions to reserves, Credit Union 1’s net worth ratio would be only 5.8% versus the reported 10.2%.

But even the $88.6 million in UDE at June 2024 is misleading. At yearend 2020 the credit union reported $16.9 million in land and buildings. Three and a half years later, June 2024, the total is just $2.9 million. In the same period the credit union reported $15.1 million gains on sale of fixed assets. In the 18 months ending June 2024, the credit union also had non-operating gains on loan sales of $4.6 million.

It is not possible to determine how much of these sales are from Credit Union 1’s own assets or from the loans and fixed assets acquired via mergers. These sales amount to almost $20 million of the $88.6 reported UDE in June 2024. These are one-time events that are reported in net income thereby adding to retained earnings, but in fact are non-operating, one-off gains.

Safety and Soundness Questions

If these one-time gains are subtracted to show actual operating net worth generated from continuing operations, the net worth ratio from internal operations would be only 4.6%. Hence the credit union’s drive to raise external capital (sub debt) and acquire other credit unions’ reserves. Its dependence on external capital and one-time sales raises significant safety and soundness questions.

Internal operations are not generating sufficient capital to maintain required net worth minimums. For example, in the full year 2023, the credit union would have reported an operating loss of $429,000 except for the one-time gains on sale of fixed assets and loans. Through the first six months of 2024, the credit union’s ROA is only .39% or just .23% without extraordinary gains. (all data from NCUA tables)

The financial results are in even steeper decline than what is presented. If one considers the impact of adding merged shares and loans from the preceding four quarters prior to June 2024, there are critical balance sheet trends. These five mergers added approximately $210 million in loans and $346 million in shares to Credit Union 1’s balance sheet. Without these external gains, the credit union’s decline in outstanding loans for the 12 months ending June 2024 would have been $288 million or 24%. For shares, the falloff would be $73.3 million or a negative 5.5%, not the 4.6% increase reported. The credit union also relies on $35 million in external borrowings for funding.

Since converting to NCUSIF, the credit union has reported growth and acceptable ratios only through the acquisition and then sale of fixed assets and loans, and using the free transferred capital to maintain its required net worth.

What to Do About a Runaway Credit Union?

Once NCUSIF-insured in 2022, Credit Union 1 has been on a merger and marketing binge which is hiding serious financial performance shortcomings.

In all credit unions the Board, as a group, holds the direct, legal fiduciary responsibility for the performance of the credit union. The Board members approve all policies and hire the leadership. The buck stops with the Board members – all of them.

This is especially true in Illinois which has an unusual provision in the state act that allows the board to collect proxies from all its members, thus giving the board full decision-making authority in all areas, including mergers.

This is the reason for the extended proxy explanation in the Notices of Merger of the five Illinois chartered credit unions which reads in part:

Illinois permits voting on merger proposals only at the meeting or by proxy. If you do have a proxy. . . you may do nothing, and the board will vote in favor of the merger in your sted. . . If you have a proxy on file, to vote NO you must revoke that proxy by giving written notice to the board secretary. . . and then assign a new proxy to an attending member.

This is why all mergers of Illinois’ state-charters are reported as virtually unanimous. The process also puts a higher standard for due diligence and fiduciary responsibility on board members as they are now acting directly for the member.

There have been several recent class actions against credit unions around improperly disclosed overdraft fees and cyber breaches. When merged Credit Union 1 members confront the reality of losing their independent cooperative some may be deeply upset. With their board’s unilateral actions and failures to document their duties of care and loyalty, these transactions could become fertile ground for such actions.

Where Are the Regulators?

Except for the several federal charters merged, initial approval is by the state as Credit Union 1 is Illinois chartered. Most of the credit unions merged in MI, WI, GA, IN and IL are state chartered. All the data cited above is in public call reports and in multiple year analysis formats on NCUA’s website.

The trends for Credit Union 1 are clear, the extraordinary payments to CEOs presented in the Notices, the copy-book wording in the Notices all the same, and the vigorous public marketing communications easily reviewed for this nationally aspiring credit union.

NCUA routinely signs off on all mergers even those characterized by extraordinary self-dealing (eg. CEO contracts with change of control clauses), no clear business logic or member benefit, and Notices with misinformation, disinformation and missing critical facts for any member to make an informed vote on the issue.

There are indications that this hands-off response is the NCUA staff and board’s preferred laissez faire policy. The outcome is fewer credit unions by encouraging smaller credit unions to merge with larger ones driven by monetary payouts to achieve their policy of industry consolidation. But of course there are no asset limits as recent merger announcements have demonstrated.

The explanations for this dual chartering supervisory failure are wanting. In some instances, it may be a repeated failure by staff to do any elemental analysis. To my knowledge, there has never been a regulator “look back” to see if any of the merger commitments were followed up—even in a situation involving $12 million in members’ capital diverted to the merging CEO and Chair’s newly organized non-profit.

Regulators appear to lack a common sense understanding of events, not wanting to see or address the obvious conflicts of interest and board fiduciary failures. They thereby become part of the problem, abetting the worst aspects of cooperative leadership.

The result is no regulatory guidance or even backbone to stand up for members‘ interests or rights. There is no director-board check and balance on CEO’s ambitions or performance. And no regulatory effort to hold accountable those credit union CEOs who use their positions of power and institutional wealth to take advantage of the member-owners of acquired credit unions.

A System Circling the Political Drain?

Instead of expanding member economic opportunity, credit unions are imitating the tried and profitable capital market efforts to roll up their smaller locally focused brethren though payoffs and the rhetorical promises of better service through—even if only virtual.

Credit Union 1’s “purchased members” have lost the heritage and identity their cooperative predecessors passed on to them. Trust and loyalty earned over generations is gone. Members will vote with their feet when they learn there is no more advantage to being with Credit Union 1 versus dozens of other online financial offerings just as easily accessed.

Credit Union 1 has maintained its regulatory financial requirements only by acquiring other credit unions’ capital reserves, one-time sales of fixed assets and loans, closing local branches and letting employees go, and borrowing sub debt capital. These are efforts to buttress its balance sheet and cover its inability to earn an acceptable return on its own assets for its member-owners.

This practice will eventually be found out, the mergers will end. and the credit union’s safety and soundness will be much more closely scrutinized.

However, in the meantime, eleven local credit union charters are destroyed, their professional and community leadership roles ended, members’ long-time relationships to their credit union dissolved and the industry’s reputation put at political risk.

As Credit Union 1’s financial short comings become increasingly apparent, their external relations with Notre Dame athletics, the U of I Chicago campus, the new WCC partnership and Tinley Park Amphitheater will be in jeopardy. So too the industry’s public image.

I believe Credit Union 1’s actions are a threat to the future of the cooperative model. Every system has “bad actors.” That is why there are regulators. When directors fail in their fiduciary roles, and supervisors abdicate their appointed oversight responsibilities, the system’s integrity is at stake.

When other credit unions remain silent, state regulators default in their oversight, and NCUA appears unconcerned about the consequences of these events, it is only a matter of time until cooperatives forfeit their unique role in the American economy.

And should that day of reckoning come, thousands of credit unions trying to do the right thing will be end up in the same reduced status as their rogue colleagues.

A 2023 documentary film’s message puts credit unions right at the center of our current political angst.

The film is Join or Die. ( this is the 3 minute trailer) It is based on the work of social scientist Robert Putman who in 2000 published a book called Bowling Alone. It documented the decline of local organizations that create the connections on which individuals built their trust in and sense of community.

The author calls this foundation of mutual confidence and relationships “Social Capital.” In his analysis, these organizational connections have real value.

The film updates this decades long continuing trend of increasing social isolation. He believes the loss of local networks has contributed to the decline of confidence in American democracy. For it is in our connections with multiple organization that we develop awareness of mutual obligations and the common good.

The Credit Union Example

The cooperative movement, and especially credit unions, were founded with social capital. Unlike other profit making firms, only minimal shares were pledged by organizers to receive a credit union charter. The Field of Membership was the existing external network that provided the connections giving a new charter its mutual support and market focus.

The net worth or financial capital requirement was a flow concept. Either 10% or 5% of revenue had to be set aside into reserves until a certain ratio of net worth to risk assets was attained.

In the 1998 Credit Union Membership Act this “flow” concept of capital adequacy was replaced with a “stock” measure–that is the ratio of net worth to assets. This financial point in time definition was expanded by the 2022 imposition of a risk-based capital. This raised the well capitalized ratio from 7% to 9%.

The founding cooperative bond of social capital was replaced with financial ratios. This transformation was accelerated as credit unions evolved their fields of membership into new groups, areas or criteria with little connection to each other. Instead of established connections, credit unions began relying on new brand creations and marketing to establish a their presence in the markets they sought to serve.

A Second Factor

As credit unions moved further and further from points of connection with relationships of trust, a second decline was in member-owner governance. The annual meetings no longer featured contested board elections; rather the board nominated the same number of internally selected candidates as vacancies. No member votes were cast; the positions were filled by acclamation.

This resulted in the erosion of any pretense of democratic governance. Increasingly self-appointed boards grew further and further away from their members. Credit unions were not alone. Putman’s work suggests that over half of America’s social/civic infrastructure has disappeared since he first wrote.

As these foundational experiences of local connection are lost, individuals become more isolated. And with that feeling, so does confidence in the governmental process, both locally and nationally.

One can debate whether credit unions contributed to, or are just another example of, institutions caught up in a fundamental transition of community relationships. It is certainly possible to find longstanding successful credit unions still serving their core markets. One indicator is a credit union’s name such as Wright-Patt Credit Union. The counter evidence would be examples where the institution has repositioned itself with growth efforts based on leveraging of members’ financial capital with mergers or bank purchases.

The film highlights Putman’s analysis of what makes American democracy work.

It explains why our traditional political process of compromise is much more difficult.

Finally he suggests what can be done about it.

While the film documents the loss of social infrastructure, there is good news. As the trends are laid out, the film closes with the message, “You can decide to change history.” The “financialization” of credit unions with their loss of a social capital bonding can be recovered. But how to start?

Re-establishing Credit Union’s Social Capital Advantage

A recent communication from the Texas Credit Union Commission’s monthly newsletter provides a place to reaffirm this core cooperative asset. Change comes from the top. Here is an excerpt from their Newsletter that I believe directly speaks to Putnam’s concerns.

The Importance of Board Meeting Attendance in a Time of Rapid Technological Change

Critical to the long-term success of a credit union is an active, involved board that provides proper oversight of operations and a sound strategic direction for the future of the credit union. One of the keys to ensuring that a board is successful is regular, participatory attendance.

This is particularly true given the rapid pace of technological change and the need for partnerships with financial technology companies (“Fintechs”) to provide services wanted by your members. . . Management and the board must ensure that . . .the Fintechs chosen are a good fit for the credit union and the membership.

Board involvement is important in Fintech selection and other important strategic decisions affecting your credit union. The issue of board attendance is a tricky one. Board members are volunteers with their own jobs, families, and busy lives to balance in addition to the voluntary obligations of serving on a credit union board. However, missed meetings seriously diminish the effectiveness of the entire board, and a director’s irregular or inconsistent meeting attendance could result in removal from the board. . .

It is important for board meeting minutes to reflect if a director’s absence is excused or unexcused. The lack of a record of an affirmative vote by the board is construed as an unexcused absence. . . Once a director misses . . . the prescribed number of meetings . . .there is nothing the board can do except to fill the vacancy with a new person within sixty days. . .

This Texas regulator’s message is a clear reminder of every board’s guiding role and responsibility, from NCUA’s three directors to the system’s smallest of credit unions,

This is an important leadership statement from one component of the credit union’s unique dual chartering system. Board members should actively Join in their roles, or credit unions could Die.

There have been pivotal years in credit union history, none more so than 1984.

NCUA and credit unions celebrated unprecedented market place, legislative and industry financial success. NCUA issued over 100 press releases over the 12 months. These announcements covered credit union performance, agency initiatives, and multiple press and political comments on the cooperative system. Here is a very small sample, in date order, of these Agency communications:

Jan 4: American Banker reports credit unions grow faster.

Jan 11: CLF pays quarterly dividend of 9.0%.

Jan 16: NCUA Acts to recover Penn Square losses

Feb 15: Credit Union Stamp Released in Massachusetts

Feb 29: Symposium on College Student Credit Unions

Mar 6: Financial Performance Reports a Hit

Mar 9: NCUA Board to Meet in Tucson

Mar 14: Credit Unions Fastest Growing Financial Institutions

Mar 21: Callahan Testifies Before Senate Banking Committee on Insurance Fund Capital

Mar 24: NCUA to hold First Conference of Federal and State Examiners

Apr 4: Banking Committee Approves Capitalization Bill

Aor 18: NCUA Names Koppin Supervisory Examiner of the Year

Apr 30: Credit union Statistics for March

May 15: NCUA Central and Regional Office Realignment

May 24: NCUA Investment Hotline Unveiled

May 30: Credit Union chartered for Cannon Hills Employees

June 19: 50th Anniversary Celebration

June 22: President Issues FCU Week Proclamation

July 18: President signs Bill to Strengthen Insurance Fund

July 26: NCUA 1985 Budget down 4.9%

Aug 21: FCU Growth Surges at Midyear

Aug 31: Two Per Credit Union Limit Placed on Las Vegas Conference

Oct 9: Board Adopts Capitalization Rule

Oct 12: Credit Union Membership tops 50 Million

Oct 22: Credit Unions Most Popular Financial Institutions

Nov 15: Board Slashed Operating Fee Scale 24%

Nov 23: Seger, Breeden, Connell, Pratt Announced as Speakers at Las Vegas Conference

Dec 18: American Banker Reports CU’s Growing Faster than Thrifts

Over 70 additional releases about key Agency and credit union events were issued.

All of these releases were amplified in the monthly NCUA News sent to all credit unions as shown in the samples below.

Additionally, NCUA created a Video Network in which the Agency communicated significant changes and events both internally and with credit unions. Here is the brief opening segment of an hour long video introducing the recapitalized NCUSIF.

In 1984 there were over 16,000 active credit unions. All FCU’s were examined annually overseen by six regional offices and a staff of just over 600. The brief excerpts above of the Agency’s wide-ranging activities and reports are a tiny sample of the interactions and communications with the credit union system, Congress, the White House and the public press.

These events occurred in the third year of Ed Callahan’s chairmanship which began in October 1981. The NCUA board, Bucky Sebastian, Executive Director, and the Senior staff believed that public service is a public responsibility. Senior employees were available, willing and eager to engage with all constituents. And most importantly. accountable to those who entrusted their funds and members’ futures to the regulator for oversight.

A highpoint of this interaction was the December 1984 National Credit Union Conference organized and led by NCUA with the support of the credit union system. It was a first for NCUA, and the largest conference ever held at that point in credit union history. The event was a coming together to celebrate the cooperative system’s growing relevance and success. And to share views about the future of the movement by all those who were dedicating their lives to their members’ well-being.