Editor’s note: The following guest commentary is a response to the NCUA board’s July 18 proposed rule requiring written succession planning policies for all credit unions. One rationale was that this action would reduce the number of mergers now occurring due to a lack of available CEO or board candidates at times of leadership transition.

By Ancin Cooley

The succession planning discussion during last week’s NCUA proposed rule is about who will control the future of an organization’s resources: the member-owners versus transferred to an outside third party’s control?

Here’s the key question to keep in mind as you read my views:

Is the members’ loss of their charter and capital comparable to the costs of Board/CEO succession planning by any measure?

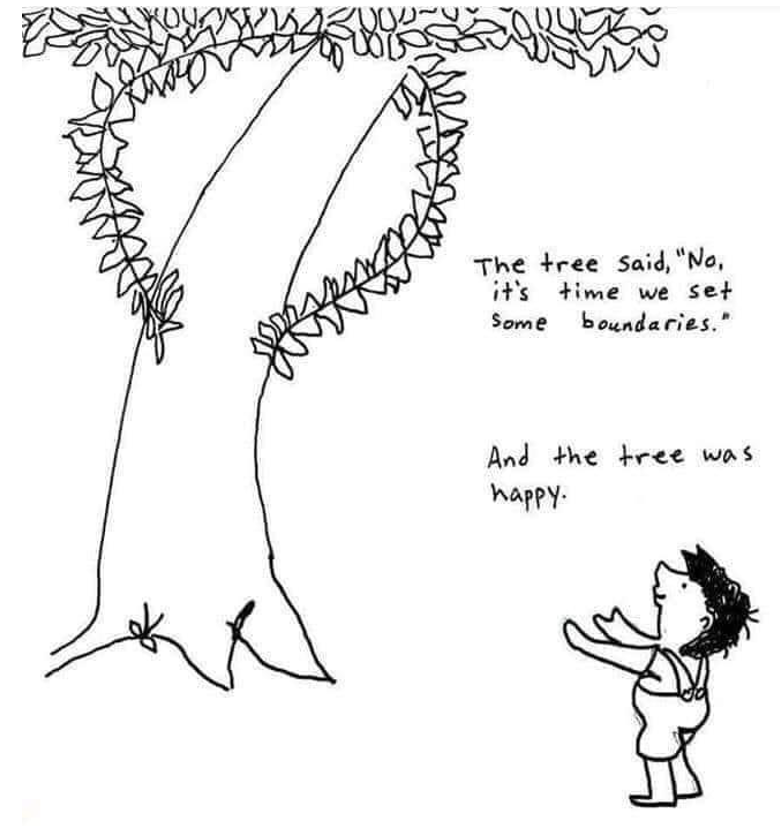

Bridging the Gap: “The Middle Way”

The solutions below are born of fatigue from reading about merger abuses and pragmatism. I’d rather a Board give a CEO what they feel he or she has earned in a manner similar to community bank compensation versus that same CEO attempting to convince their Board to merge for a “backend” payout from the surviving institution.

If we don’t openly address “backend” payouts post-merger, we won’t have a serious conversation on this issue. (Source: CU Merger Update Part II: More Management Comp Deals, Some Member Payouts, Usual Reasons and, Sometimes, No Reasons are Cited for Combinations)

Practical Solutions for Succession Planning

Let’s get down to business.

- Incentivize CEOs with Bonuses for Succession Planning Tasks: Offer financial incentives to CEOs for the annual completion of board succession tasks. This ensures that succession planning remains a priority and is executed effectively. (A colleague on LinkedIn thought this was a horrible idea, stating that CEOs are already getting paid to do their jobs. I agree with her logic, but I have also been working in financial institutions for 20 years. It won’t happen without a carrot.)

- Allow CEOs to Benefit from Capital Growth: Create a system where CEOs can benefit from the internal capital growth within their organizations, fostering a sense of ownership and alignment with the credit union’s success. For example, if a CEO starts with $8 million in capital and grows it to $24 million by retirement, they should access some of those funds in the form of a “liquidity event.” This approach reduces the risk of CEOs seeking payouts through unnecessary mergers.

Implementing these actions addresses the “elephant in the room” of self-interest driven mergers while aligning personal and organizational outcomes. The goal: fewer mergers and more stable, mission-driven leadership transitions.

Who is going to object to the solutions I’ve provided above?

- Credit unions that rely on one solution for their continued growth-more mergers

- Firms that provide secondary capital that support mergers

- Lawyers that offer merger services

- Financial firms, brokers and consultants that provide merger services

This collective group drives the marketing and PR surrounding mergers, shaping the narrative to their advantage. During the comment period, this same group will prompt state leagues to oppose what is truly in the best interest of the members, thus prioritizing their own financial gains.

The institutional efforts to grow via industry consolidation is a feasible external growth strategy. But it belongs in the banking open-market world, not the credit union cooperative model. Credit unions with merger growth plans are playing tackle at a flag football game. Cooperatives were intended to be perpetual by paying results forward, a different outcome entirely from private wealth accumulation.

Common Rebuffs Against Succession Planning

- Regulatory Burden:

Ah, the classic “regulatory burden” argument—how many times have we heard this one? It’s a tired refrain. But let’s break it down: What is the regulatory burden, and for whom? For the management teams who find it cumbersome? What if this so-called burden is a safeguard for the members?

If we truly embrace free markets, then if one CEO finds succession planning too burdensome, the members, through their directors, can find a CEO who sees it as a manageable task. The framing of regulatory burdens should always consider who is complaining and why.

During the recent open discussion on the matter, NCUA Board Member Kyle Hauptman mentioned a CEO who claimed that implementing succession planning would force his credit union to merge.

Is it the managers’ place to suggest to their members that putting effort into leadership continuity—to protect their charter—is going to result in a merger? Imagine if you owned a commercial building and asked your property manager to implement a succession plan. If your manager rebuffed with, “If you make me put this succession plan in place, we’ll be forced to sell the property,” what would your response be?

- Flexibility Concerns:

Some feel that a one-size-fits-all rule for succession planning would not consider each credit union’s unique needs. The NCUA proposal allows for broad discretion in implementation, enabling each credit union to tailor its succession plans according to its specific circumstances and needs.

- Cost of Implementation:

While developing and maintaining a succession plan involves some time and cost, these are minimal compared to loss of the charter. NCUA’s new charters are required to raise a minimum of $500,000 t0 $1.0 million to open for business. Thus, the loss of any charter for the membership, the community and the credit union cooperative system is huge.

Conclusion

Succession planning is not just a procedural necessity; it is an organizational imperative to ensure the continuity of the mission and values of credit unions. As we navigate the complexities of leadership transitions, let’s prioritize the long-term health and cooperative principles that define our organizations. By doing so, we can safeguard the future of credit unions and continue to serve our communities effectively.

Implementing practical solutions, such as incentivizing succession tasks and allowing CEOs to benefit from capital growth, can harmonize personal and organizational interests, leading to a more stable and mission-focused future.

In short, THERE AREN’T TOO MANY CREDIT UNION TRUE BELIEVERS LEFT. COOPERATIVE IDEALS SEEM TO BE A THING OF THE PAST. IF THE MOVEMENT HAS ANY CHANCE OF SURVIVING, FOLKS GOTTA GET PAID.

P.S. To all the institutions relying on mergers as their primary driver of growth.

The day after the merger, all the problems that existed before your merger will still be there. Only now they’re scaled and compounded.

Mergers teach you one thing: how to merge. You haven’t learned how to execute a strategy, build your brand, or manage the risks of a larger organization. You haven’t developed a talent pipeline. And candidly, you won’t have time to address any of these issues because you’ll be too busy dealing with the residual effects of the merger, such as core integrations and member withdrawals.

Mergers should accelerate a strategy that’s already working, not as the ignition for your growth. God bless and happy hunting.

If you are interested in further conversation, please reach me at acooley@syncuc.com or check out my YouTube channel here.

Credit unions are changing…

Credit unions are changing….4e964e48.jpg) Been searching for years for the original Indian meaning of that name. Recently, a friend told me he knew the origin. He said, it’s in the dictionary: “Uwharrie” means “unknown”. Really? Asked him for a copy of that reference for my files. Sure enough, the following week, in came a copy of the dictionary definition. It said: “Uwharrie – adj., probably from an ancient tribal name; meaning unknown.” Perhaps I just need to pick better friends….

Been searching for years for the original Indian meaning of that name. Recently, a friend told me he knew the origin. He said, it’s in the dictionary: “Uwharrie” means “unknown”. Really? Asked him for a copy of that reference for my files. Sure enough, the following week, in came a copy of the dictionary definition. It said: “Uwharrie – adj., probably from an ancient tribal name; meaning unknown.” Perhaps I just need to pick better friends…. “Downtown” the candy-striped awnings and improvised handicap ramp of Badin Town Hall and Police Department adjoin the Masonic Lodge #637. Then comes the post office with its single window, fleet of post office boxes, and well-used community bulletin board. Shading the post office is Memorial Park, flanked by a cedar tree honor guard for the seven Badin soldiers who died in World War II. And, out of sight up a short dirt road, is the best named roadhouse on the planet: The Bottom of the Barrel Disco and Cafe; now vacant, having recently burned to the ground. Bet that last party was a great one. Sorry to have missed it!

“Downtown” the candy-striped awnings and improvised handicap ramp of Badin Town Hall and Police Department adjoin the Masonic Lodge #637. Then comes the post office with its single window, fleet of post office boxes, and well-used community bulletin board. Shading the post office is Memorial Park, flanked by a cedar tree honor guard for the seven Badin soldiers who died in World War II. And, out of sight up a short dirt road, is the best named roadhouse on the planet: The Bottom of the Barrel Disco and Cafe; now vacant, having recently burned to the ground. Bet that last party was a great one. Sorry to have missed it! The beauty of Credit Unions used to be something you couldn’t easily wrap, bottle, or “spin”. Badin FCU is no longer there to make a difference – gone the way of merger. There are no longer any banks or credit unions in Badin. The aluminum plant, too, is gone.

The beauty of Credit Unions used to be something you couldn’t easily wrap, bottle, or “spin”. Badin FCU is no longer there to make a difference – gone the way of merger. There are no longer any banks or credit unions in Badin. The aluminum plant, too, is gone. … are we getting close to the Bottom of the Barrel on a lot of important things in our Country, including credit unions?

… are we getting close to the Bottom of the Barrel on a lot of important things in our Country, including credit unions?