At the Western CUNA Management Scoool, students are discussing the future of credit unions. Is the cooperative system just another financial option for Americans or does it have a different public priority from its founding and subsequent tax exemption?

Some assert what makes credit unions different is that the system is based on values. Some would point to the seven or eight cooperative principles as one indicator of the difference from for-profits.

But can institutions have values? America was founded on values, especially the freedoms and rights founders asserted were enabled by democratic rule, that is the consent of he governed.

Are Organizations People?

The Supreme Court has repeatedly ruled that organizations (such as corporations and unions) are “legal persons” and possess First Amendment free speech rights. Landmark cases like First National Bank of Boston v. Bellotti (1978) and Citizens United v. FEC (2010) established that political spending and advocacy by organizations are protected forms of free speech.

But institutional design, or legal character, do not guarantee virtuous conduct. Individuals are the source for corporate decision making. All organizations need individuals to participate and in some instance, to get their future back on track. Even credit unions.

The Challenge of Power

Calling credit unions financial service providers is not incorrect, but the issue is why we believe that is credit unions’ defining characteristic. The challenge is not that the description is wrong, but why is it the primary focus.

People can lead credit unions but may have their outcomes set on the wrong things. Some believe and act as if it the size of the balance sheet along with the supposed advantages of scale are the critical factors in credit union success. Size denotes market power and can lead to market and financial dominance.

But credit unions succeed not with conventional approaches to market conquest, but with relational power. That is the trust and service that promotes members’ financial well being. Trust does not come in big or small packages. It is present or not in an organization’s action. A lesson Rudy Hanley used to guide his tenure at Schools First for almost 30 years.

Institutions don’t have values. People do. The responsibility for ethics and justice lie not in some abstract organizational concept, but directly with the individuals who design, participate in, and regulate that system.

The democratic credit union governance can be an advantage in achieving this relationship power. For democratic participation should enable constant debate to restate what ethical boundaries and values should be embedded in the financial rules of the game. Is this how your credit union acts?

What is credit union’s most important strategic advantage?

Is it the tax exemption? Their superior volunteer and professional ledership? The democratic member-owner design? Their origins and long standing member relationships? Is it superior size and scale? The ability to buy out their for-profit competitors in private? Or, the classic non-answer, It depends?

At this summer”s Western CUNA Management School, there will be discussions of strategy and the advantages credit unions bring to market competition.

Here is one perspective, not directly about credit unions, but which would certainly align with many successful credit unions’ approaches. As you read, ask what is the prevailing narrative for credit union strategy? Does that approach fit your credit union?

As journalists, we’re constantly thinking about narratives. At Next City, we’ve been grappling with the question of how narratives change, or how new ones emerge. Part of the answer is ultimately doing the work it takes to do things differently than the way they’re done in prevailing narratives.

In one prevailing narrative, economic development is about “attracting and retaining” large corporations to “create better, higher paying jobs.” Tax incentives emerge to support deals that fit the narrative. Commercial or mixed-use lots that fall into city-owned hands get placed into the hands of whichever developer can assemble the “highest and best use” business plan, meaning they can attract the highest possible paying tenants.

So much of what I’ve come across over the past 10 years at Next City has been about doing economic development differently. Community power over land, worker power over business, local power over finance. All of the different models for how those basic concepts manifest have emerged from conversations on the ground about how the prevailing economic development narrative doesn’t serve their communities.

Talk may be cheap, but it plays a role, too. The prevailing narrative about economic development gets reinforced through regular nationwide convenings of economic development professionals, urban planners, developers, and investors where attendees are all caught up in that same narrative. And they all play a role in implementing and entrenching it further.

Last week in the Bronx, I witnessed something I’ve seen only a handful of times, though it’s becoming more frequent in recent years: More and more of the people behind these models, people who are trying to do economic development differently, are finding resources to connect and share notes across different local contexts, from coast to coast and everywhere in between.

There’s even a term they’re using to start describing this network of hyper-local initiatives: “trans-local.” (one credit union CEO calls these efforts networks)There’s a lot they have to learn from each other, even if they’re operating in different legals framework and funding ecosystems. Parallels are quick to emerge, like the role of certain buildings or spaces as a sort of community organizing anchor that draws community members in to start having conversations about how they can play a role in doing things differently.

A Case Study Illustrating the Topic of Local Economic Development vs. Transfer of Leadership?

The following are links to a current, ongoing example about two opposing credit union approaches to community economic resilience: Stay local or transfer leadership and resources to distant, out of area organization?

Many relevant financial facts and future claims are outlined in this series of blog posts about the proposed merger of the 85 year. $4.5 billion , Sacramento SAFE Credit Union with the $29 billion BECU whose main office is in Tukwila, WA, (links)

Read or listen to claims for the merger versus the facts of the two credit unions’ current financial performance. Which option would you think is in the members’ best interests? How does your decision influence your approach to strategy for your credit union?

You can post your oinion in the comment section-or use in your final year’s class project.

Yesterday began the 2026 Western CUNA Management School (WCMS) two week summer session.

WCMS is one of several industry sponsored professional education opportunities. The curriculum is covered over three years with the two week sessions for in-person classes and social networking experiences.

The on-campus portion is on the Pomona College campus with students living in dorms. Classes are led by college professors, industry veterans and outside experts. WCMS has evolved over its 60 years as the credit union system, financial services and the economy have all undergone significant transformation.

The purpose has remained constant as presented on its website.

Developing Leaders

Advancing

Credit Unions

WCMS’s immersive curriculum blends academic rigor with real-world application. Graduates return as strategic, confident leaders ready to innovate, solve challenges & drive results.

The Test of Education:Knowing the Right Questions to Ask

How does any organization, industry or community assess the quality of its educational programs? Is it basic organizational skills learned? Applying technology to recurring management issues? Analyzing financials or applying other business oriented courses and strategic theories to coops?

Education evolves. Curriculum is never static. However the strength of a credit union based course should be the ability to understand more about the unique cooperative model. And how its evolution for over 100 years has created the current $2.6 trillion depository based non-profit financial system.

Enhanced skills are beneficial but often insufficient to fully appreciate the cooperative legacy that has been paid forward by prior generations to today’s aspiring leaders.

For the next two weeks I will periodically pose questions or topics that I believe would stimulate important discussion about the state of the industry today.

History Matters Because Credit Union Design Is Perpetual

This month’s CUSO Magazine is presenting various aspects of credit union founding events. A recent article in the series documents the loss of contemporary printed publications created by the leagues, industry newsletters and even regulators. (link). There appears to be no central repository for personal, organizational or public records for future research.

Without an examined knowledge of the movement’s several eras, it is more difficult to understand and present future cooperative contributions. The default strategy can just become adopting competitor’s tactics, a surefire way to lose cooperative purpose.

The Final Exam Questions for WCMS Graduation

Because history can inform both present and future potential, the following would be my first questions for WCMS’s final exam. It assess one’s knowledge of credit union history and its relevance for today in three brief essay answers.

When Filene set out to form credit unions in the US having seen examples elsewhere, what was his “theory of change” for American society? Why did he believe a cooperative, credit union approach, was the best option among a number of new consumer focused financial experiments at the time?

2. Why did Filene hire Roy Bergengren? What did he feel the nascent movement needed in Bergengren’s skill set? Did the two founders have disagreements about how to proceed?

3. Do these founding events have echoes in today’s credit union movement? (Theory of change, strategies/tactic for movement success, leadership skills)

When History Changed a Critical Understanding

These questions may appear to be more liberal arts versus business skill sets. However this is the kind of discernment students will need when encountering practical challenges today and how simlar events were addressed in the past.

For example in 1982 when NCUA Chair Ed Callahan and Bucky Sebastian were seeking to understand the history of the field of membership in the Federal Credit UnionAct, they went to Massachusetts to learn about the movement’s founding practices. They wanted to know the background of the concept. Was it about more than a legal interoperation of the word groups?

In Filene’s home state, a cradle for the early movement, they learned that most initial state charters included local communities along with a sponsor. The field of membership was meant to fit individual circumstances not force prescribed boundaries or limits on who could become a member.

That was the basis for their bringing greater regulatory flexibility to the FOM interpretation of the FCU Act.

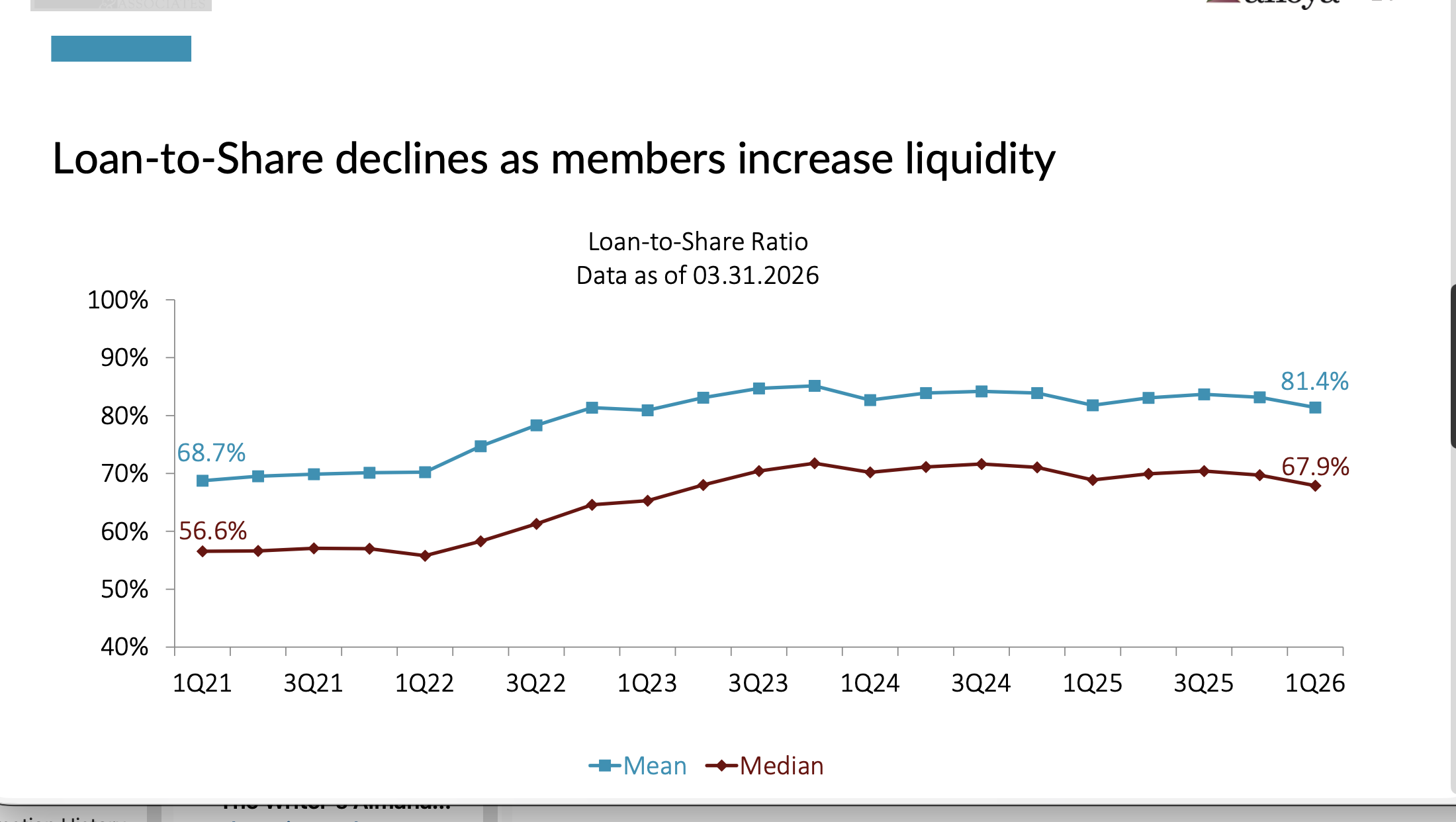

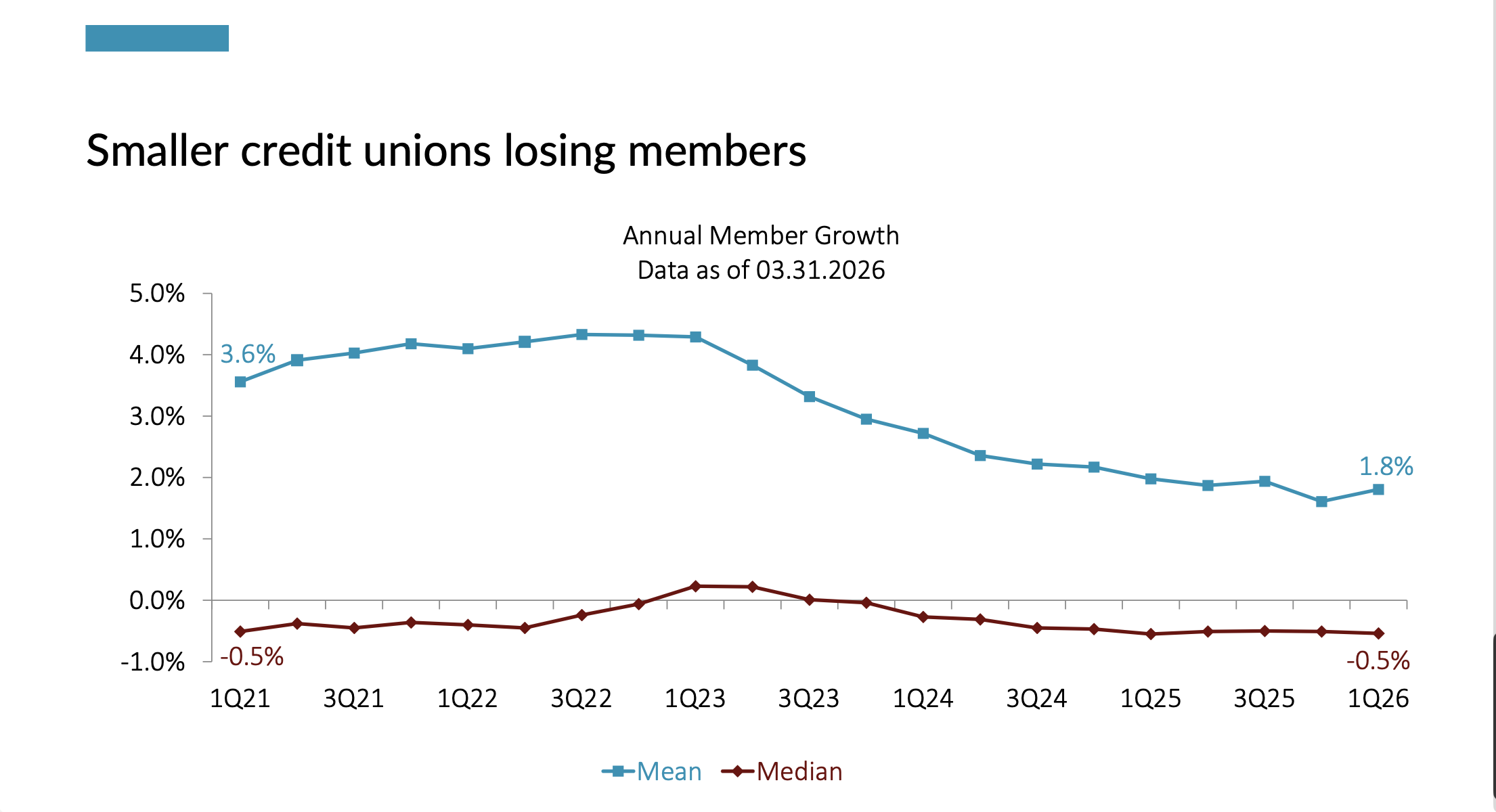

For over a year in their quarterly Trendwatch industry uupdates, Callahans has shown long term trends using both average ratios (the mean) as well as the median for industry level performance.

The mean is the weighted average outcome for all credit unions. Obviously this approach gives more significance to larger institutions’ trends versus smaller. The median shows the middle number where 50% are below and 50% are above the number being tracked. Here are two examples of these analytical outcomes:

Callahan’s graphs illutrate these different ways to present data. While overall trend lines may look similar, there is a real difference when interpreting individual circumstance or peer comparisons.

The Impact for Credit Unions Member Analysis

Yesterday the web site Visual Capitalist published a chart that ranked the 30 Richest Countries in the World by average wealth per capita, that is total wealth divided by population. The second ranking presented the mean or middle total for per capita wealth.

As one might expect America ranks second in average wealth at $695K per person, behind first place Switzerland at $910K. America’s economy has long been one of the largest in the world in total and per capita. No surprise there. On average Americans are well off.

The second column tells a different story. When ranking by the median, the US number is $69K per person. That is 50% of population has less than that amount and the other 50% more. That number places the US in 28th position out of the 30 countries, just above Greece and Germany.

No other country of the 30 in the UBS Glpbal Wealth Report ranking for 2026 had such a radical difference between the the mean and median average wealth per person.

The US reports the widest distribution in the wealth ownership gap between the very wealthy and the rest of the population.

The Credit Union Implications

This is not a new finding. But it shows the extreme difference when placed in the context of other wealthy nations. Moreover, in America this wealth distribution disparity is growing.

In credit union analysis member participation is often calculated. The result is frequently referred to as the 80:20 rule. That is 20% or a small number of members contribute 80% or more of loans or deposits balances. These generally better off members are a much sought after class by all financial providers because of their impact on the firm.

But is an 80:20 outcome in member relationships where the credit union model is most effective? Has your credit union looked at the mean and median income or net worth distribution of your members? Or in the market(s) you serve? Is the marketing priority to gain more profitable, higher balance members or grow across all income levels?

The critical question is whether credit union business models and practices are contributing to and worsening the wealth gap, or trying to improve community equity? Does a credit union’s fee structure, loan pricing policy and savings rates favor the well-to-do? Do the less well off pay more for loans and earn less on their smaller savings balances?

One former credit union CEO who worked tirelessly to ensure there was not a wealth bias in the coop’s practice was Jim Blaine when he led SECU NC. With his approach the credit union became the second largest in the country. Pricing and fees were equitable for every member.

Measuring mean and median member income could be one of the most important indicators of credit unions fulfillling the movement’s public duty justifying its tax exempt status. Or it might indicate the constant pull and siren appeal of the greater market’s for-profit forces.

How credit union’s respond to America’s growing disparity in its distribution ever increasing wealth could determine the movement’s future, that is either profit or non-profit.

Sometimes a simple story can portray an entire philosophy, strategy or organization’s culture. No corporate manuals, strategic plans, or even special training sessions are needed.

For example in the Bible when Jesus says his second great commandment is to love your neighbor as yourself. His critics ask, Who is my neighbor? Jesus then tells the story of the Good Samaritan. It is about a traveler attacked and robbed by thieves, and left injured lying alone on the road. His fellow countrymen pass by. He is helped by a stranger, who is not from his country, religious tradition or ethnic background.

The following story is the lead in a CEO’s monthly staff update. It is long because the event was extended. If you knew nothing more about this credit union other than this episode, you would surmise that it is probably very successful in traditional performance measures. It is, but that is not the primary purpose. It succeeds because of a culture that tries to fulfill the special purpose of a cooperative charter for its members and communities.

My only edits are to protect the individuals named and the credit union’s identity. I would call it the story of A Credit Union Good Samaritan, because as in the original, the person assisted was not even a member of the credit union.

From a Cooperative CEO

This month’s story highlights Mary, a long-time shared-branching customer supported by Rose at our Central Avenue Member Center.

Mary is associated with an out-of-state shared-branching credit union and visits our location about once a month to withdraw a small amount of money. As an older individual, she prefers managing her banking in-person and occasionally stops in for general assistance. Over time, Rose developed a strong, trusting relationship with Mary.

One afternoon, Mary arrived visibly distressed. When Rose asked how she was doing, Mary shared that she was feeling overwhelmed. She requested her account balance and withdrawal limit, and upon hearing the details, her anxiety seemed to increase. Mary mentioned needing to make a phone call to confirm something and stepped into the lobby.

While on the phone, Rose could overhear parts of the conversation. Mary sounded frustrated and repeatedly referenced taking cash to Walmart, which immediately raised concerns. After ending the call, she returned and requested to withdraw the maximum amount allowed.

Recognizing several red flags, Rose began asking thoughtful follow-up questions. Initially, Mary was hesitant to share details, explaining that she was sending money to her granddaughter. With patience and care, Rose continued the conversation, and Mary disclosed that she had been on the phone since early that morning with someone claiming to be from “FCC Loss Prevention.” This individual told her there were suspicious charges on her account and instructed her to withdraw funds to resolve the issue.

At this point, Rose explained the warning signs of a scam and expressed concern that the situation did not seem legitimate. Although Rose could not directly access Maary’s account because she is not a our member, she encouraged Mary to contact her home credit union using an official phone number to verify the claim. Rose explained that if there were legitimate concerns, her credit union would be able to confirm and secure the account.

Mary agreed and returned to the lobby to make the call. As the situation progressed, Rose realized Mary had never fully disconnected from the original caller. The scammer quickly adapted their story, now claiming to be from Mary’s credit union after overhearing the conversation. Rose could hear Mary beginning to question the caller, asking how to confirm their legitimacy, while the scammer continued to pressure her to withdraw funds and go to Walmart.

Seeing Mary becoming increasingly overwhelmed, Rose stepped in. She located the official contact information for Mary’s credit union, asked a colleague to cover her station, and invited Mary into a private office so they could call together. First, Rose ensured that Mary had fully disconnected from the scammer, despite being told not to hang up.

Together, they contacted Jean’s credit union directly and confirmed there were no unauthorized transactions or issues with her account. The credit union also shared that they had seen an increase in similar fraud attempts. Fortunately, because Mary had not shared sensitive information, no further action was necessary beyond documenting the incident.

Afterward, Rose helped Mary save her credit union’s official phone number in her contacts and block the scammer’s number. Mary expressed deep gratitude, sharing that the scammer had attempted to convince her to withdraw and send nearly $11,000. She acknowledged that without Roses intervention, she likely would have followed through.

This experience reinforces the importance of vigilance, empathy, and proactive service. Protecting individuals—whether they are members or not—requires awareness, patience, and a commitment to going above and beyond.

This is a powerful example of how our credit union lives out its mission and purpose every day. Through care and compassion, you transformed a moment of fear and confusion into one of hope, stability, dignity, and safety for someone who needed it most.

Evergreen Credit Union, Portland. Maine was founded in 1951 to serve the employees of the S.D. Warren paper mill in Westbrook. Today it serves six counties in the state with a complete line of personal and business services and with multiple community partnerships.

The credit union embraces the culture and spirit of Maine in its branding. But importantly with its many local, engaged roles with the communities where it has branches. Although Maine’s fourth largest at $641 million at June 30, it resonates with small town intimacy.

The CEO, Jason Lindstrom is a merger refugee from Belvoir FCU just outside Washington DC. In March 2016 the senior management and Board of Belvoir completed a merger with PenFed. In November 2016 this former Chief Marketing Officer was chosen to lead Evergreen as CEO.

The Call of Duty

Jason recently posted his thoughts on freedom, responsibility and legacy after a decade as the credit union’s leader. I might describe his thoughts as the Call of Duty. His words are a charter for anyone serving in a position of private or public responsibility for others.

I’ve spent a lot of time thinking about leadership over the years, and one thing has become clear to me.

The greatest leaders don’t ask, “What can I get?” They ask, “What can I leave behind?”

As America celebrates 250 years, I think that’s the real challenge for each of us.

The freedoms we enjoy today were paid for by people who believed their responsibility was bigger than themselves. They built, served, sacrificed, and invested in a future they might never see. That is a legacy worth honoring.

Every generation has the same opportunity.

Not just to celebrate America, but to strengthen it. To be present with our families. To serve our communities. To treat people with dignity. To lead with integrity. To leave every person, every team, and every place a little better than we found it.

History isn’t written only by the famous. It’s written by ordinary people who choose to do the right thing, day after day, even when no one is watching.

As we celebrate 250 years of this remarkable nation, I hope we are remembered not simply for what we believed, but for how we lived.

Happy Independence Day, America!

Editor’s PS: Before Belvoir, where I met Jason, he was Chief Political Officer at Schools First FCU and prior, AVP Business Development for Orange County CU.

Jason also has a podcast “Pilot 2 Co-Pilot” with Antonio Neves. The theme is Leadership isn’t a solo flight, it’s a team effort. There are 8 episodes. They can be found in all major podcast directories and here: (link) (https://pilot2copilot.buzzsprout.com/)

America’s Declaration of Independence opens with words that inspired a new era of world-wide democratic political revolutions. No more rule based on divine right, inherited position or pure force. The words:

We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness.

Centuries later America strives to achieve these ideals. Even with our imperfections and unfinished dreams, individuals and countries around the world are still inspired by America’s past and its future hopes.

Democracy Is Not Easy

Democracy and its embrace of individual freedom is an ongoing challenge. One of the contributing factors is that the very freedom that encourages debate, dissent and speaking truth to power is used by all points of view. The irony is that some of those views oppose the very values in the opening words of the Declaration.

Changing the status quo, or prior error, has never been a quick task for America. Necessary reforms are opposed as threats to existing structures of power and privilege.

This has always been the case. Some divisions can take decades, or generations, to heal or overcome.

Righting the nation’s or an institution’s misdirections is never easy, whether politically, culturally or economically. But it is also an opportunity for new voices and new generations of leaders.

Credit Unions’ American Context

The shortcomings between our cooperative ideals and our daily realities are part of the credit union story. This challenge was recognized by the founders of the movement.

In Filene’s Speaking of Change, a collection of his speeches and articles published in 1939, there is a chapter, George Washington and Financial Liberty.

Filene’s view was that one of Washington’s greatest achievements wasn’t winning the war for Independence, it was having Hamilton and Jefferson in one cabinet and getting results from both.

He uses that as the model for the credit union movement saying, “temperamental conservatives” and “temperamental radicals” can work together because they’re dealing with facts, not philosophies.

One example of the effective partnership of philosophical opposites is the pairing of Ed Callahan, a conservative who believed in limited government regulations and efficient use of public funds, with the Chicago, ward 1 Democratic precinct captain progressive Bucky Sebastian. Their combined talents revolutionized credit union oversight first in Illinois and then nationally at NCUA.

Several of Filene’s observations are especially relevant this July 4th, 2026, in the movement’s 117th year:

“What is needed is that the American masses shall learn the art of constructive self-government in this machine age — in this age in which life is no longer organized on a small community pattern but in which all Americans are more or less dependent upon what all other Americans are doing.”

“For unless we can achieve economic democracy, our political democracy must be a sham.” (Filene Source: Sarah McNeil CEO, United Trades FCU)

The challenge of member-owner rights and democratic governance is even more critical in today’s $2.5 trillion cooperative financial sector. Credit union leadership is increasingly exercised as a privilege for the few, not a responsibility shared with the many member-owners.

Conflicting Coop Priorities

The rich and diverse legacy built by generations of loyal members is being swooped up in a merger frenzy driven by personal greed and ambition. But many other leaders have remained dedicated to the unfinished work serving members in their communities.

Cooperative history is about more than the many volunteer founding stories and their early efforts to build a new financial system of worker and community groups. It is also about those whose courage called attention to the inequitable financial member circumstances that should be the focus for cooperative solutions.

Those voices are present today. But is their call to rediscover who we are and who we can be being heard? Especially in the present circumstances of coop business dynamics, social and political turmoil. Will the ever-present siren appeals of market opportunity drown out our unique founding goal of public purpose?

On this national holiday, the country is again having a critical conversation about our past and future greatness. So too are credit union leaders.

My hope for how we will respond to the present challenges, as a movement and as a country, is based on two factors: our moral conscience and our history of doing the right thing in time. Our individual duty as citizens and as cooperative adherents is to witness what we value by our daily acts.

The Call for Grace in Times of Need-A Musical Reminder

Nowhere is this combination of America’s lofty aspirations and human reality more evident than in one of the most well-known songs with words from the poem, America the Beautiful.

The author, Katherine Lee Bates; (1859-1929) was inspired by a trip to Pikes Peak in 1893. Her poem first appeared in print on July 4, 1895, in The Congregationalist, a weekly journal.

All eight stanzas open with praise for America’s glories (purple mountain majesty) and accomplishments (pilgrim feet). But each verse then closes with a prayer, a call for grace or a plea. America’s beauty is both her past and the aspiration for a better tomorrow..

Here are the verses edited to show first the real glory of America and then the ongoing needs:

O beautiful for spacious skies, For amber waves of grain,. . . God shed His grace on thee, And crown thy good with brotherhood, From sea to shining sea!

O beautiful for pilgrim feet Whose stern impassioned stress, A thoroughfare for freedom beat. . . God mend thine every flaw, Confirm thy soul in self-control, Thy liberty in law!

O beautiful for heroes proved In liberating strife. . .May God thy gold refine, Till all success be nobleness, And every gain divine!

O beautiful for patriot dream, That sees beyond the years, . . . God shed His grace on thee, And crown thy good with brotherhood From sea to shining sea!

Oh beautiful for halcyon skies For amber waves of grain . . . God shed His grace on thee, Till souls wax fair as earth and air And music-hearted sea!

O beautiful for pilgrim feet, Whose stern impassioned stress. . . God shed His grace on thee, Till paths be wrought through wilds of thought, By pilgrims foot and knee!

Oh beautiful for glory-tale Of liberating strife, . . Till selfish gain no longer strain The banner of the free!

O beautiful for patriot dream, That sees beyond the years, . . . God shed His grace on thee, Till nobler men keep once again Thy whiter jubilee!

One of America’s founding ideals is captured in this poem with its familiar and oft-quoted final lines from her “silent lips:.”

The New Colossus

Not like the brazen giant of Greek fame, With conquering limbs astride from land to land; Here at our sea-washed, sunset gates shall stand A mighty woman with a torch, whose flame Is the imprisoned lightning, and her name Mother of Exiles. From her beacon-hand Glows world-wide welcome; her mild eyes command The air-bridged harbor that twin cities frame. “Keep, ancient lands, your storied pomp!” cries she With silent lips. “Give me your tired, your poor, Your huddled masses yearning to breathe free, The wretched refuse of your teeming shore. Send these, the homeless, tempest-tost to me, I lift my lamp beside the golden door!”

Emma Lazarus, written in 1883, on the Statue of Liberty

Freedom, Liberty and Opportunity

One of many possibilities beyond the “golden door” was begun some 25 years later during one of America’s earlier progressive reform eras. St. Mary’s Bank, the first credit union, was organized in 1909 by a priest to help workers in a factory with small personal loans. From that small seed, today’s cooperative financial system has grown to $2.5 trillion serving tens of millions of American consumers.

More than seventy years later, a new era of credit union potential was launched. This new chapter was described by the Chairman of NCUA in his Three Freedoms speech to the Massachusetts CUNA league’s Annual meeting on November 3, 1984.

Freedom is commonly understood to be free from something that limits or controls an individual’s actions by fear, want, arbitrary rules or sometimes coercion.

But freedom also enables individuals and society to undertake collective efforts essential for living in communities in which interdependency is crucial for the well being of all. This “empowering” opportunity is how Callahan described the transforming outcomes of deregulation for the credit union system.

The changes in government’s role had provided a new context where credit unions were enabled to make decisions not previously open to them. The upshot of these multiple efforts were described as three freedoms

* Freedom of security: credit unions have their own unique cooperatively structured insurance safety net (NCUSIF) and liquidity fund (CLF).

* Freedom to compete: credit unions could now make their own business decisions on products, services and interest rates for members;

* Freedom to serve: credit unions now decide who their membership will include (FOM choice).

Cooperative design combines individual choice in an interdependent-cooperative financial system founded on self-help, self-governance and self-reliance. Not private capital or ownership or government subsidy.

By 1984, the foundation had been set for a quarter century of deregulatory leadership by cooperatives until the regulatory backlash from the 2008 financial crisis.

With its focus on personal financial opportunity, credit union purpose promotes the country’s founding pursuits of life, liberty and happiness. Cooperative choice is a special American innovation entered though Lazarus’ golden door.

A Sleeping Giant Within the New Colossus

In his many credit union presentations, Ed Callahan described credit union’s future potential as a “Sleeping Giant” or “America’s best Kept Secret.”

This was also a vision in an American folk and labor protest song written in 1948 by Les Rice. He was an apple farmer in Newburgh, New York, who also served as president of the Ulster County chapter of the Farmers Union.

He wrote a song out of frustration during the post-WWII years. As small-scale farmers were being squeezed by large agricultural corporations that dictated the prices for produce and overcharged them for supplies.

The lyrics in The Banks Are Made of Marble contrast the labor of working-class people, including farmers, seamen, and miners, with the vast wealth of the banking and corporate elite.

The repeating chorus points out the stark inequality: the vaults are filled with the wealth that the working class sweated for, while real people struggle. The last two stanzas predict the rise of banks owned by the people:

I’ve seen my brothers working,

Throughout this mighty land,

l prayed we’d get together,

And together make a stand.

Then we’d own those banks of marble,

With a guard at every door,

And we would share those vaults of silver,

That we have sweated for!

As we head to this Saturday’s national celebration, this week’s posts put credit unions’ role in the context of the country’s ongoing pursuit of “life, liberty and happiness.”

The country’s fulfillment of its ideals has not been a straight line for either individuals or our collective accomplishments. Independence and interdependence in our common life often seem at cross purpose.

Credit unions operate in an economy dominated by capitalist ownership and the incessant drive for financial success, individually and corporately. The cooperative way is a decision we must actively choose for ourselves.

As one commentator observed: It is almost impossible to turn away from what seems like the only game in town (political, economic, or religious), unless we have glimpsed a more attractive alternative. It’s hard to imagine it, much less imitate it, unless we see someone else do it first.

Cooperatives are designed to meet individual needs with collectively managed resources in a democratic structure. Theory and practice unfortunately do do not always align in specific cases. As in the country at large, credit unions must constantly strive to achieve their goal of enhancing members’ economic freedom.

Doing the Right Thing and Me-First Ambitions

Credit unions’ ongoing challenge to be an alternative to the dominant ethos is not new. It is a struggle for individuals in all generations as described in this story-poem.

During World War II, Grandma Shorba handed plates of bread and meat to strangers who asked for work in exchange for food. After chopping wood and mending fences, the lean, stoop-shouldered men went on their way. “May God watch over them,” Grandma said.

I was glad I didn’t have to follow them down the long train tracks silvering west. I didn’t want to sleep beside a strange campfire around the bend, in the next world. But I worried how they’d survive, and asked my parents if they could live with us.

My begging only made everyone nervous. Maybe Grandma’s stories of The Good Samaritan and the Loaves and Fishes weren’t true? If I’d been in charge, I’d have asked those men to stay— but Gramma, who trusted God, fed them, then sent them on their way.

The Eternal Striving for an Unclouded Day

We all have a dream in which life’s contradictions are resolved. A home where we don’t have to face all the ambivalent choices of life This dream of perfection. of “a city on a hill” motivated America’s founders. Credit unions are one example of searching for this “home where no storm clouds roam.”

Credit unions are a uniquely American accomplishment. In just over 100 years an alternative, member-owned financial choice is thriving in a system dominated by privately owned, profit making institutions. And in doing so they constantly strive to bring “unclouded days” for members.

Today credit union momentum for the 250th birthday of America was interrupted by a Supreme Court decision. The 6 – 3 conservative majority ruled the President had authority to fire members of independent agency boards established by Congress to be partially shielded from total Presidential direction.

The decision overturned almost 100 years of precedent. It means Trump’s firing of NCUA board mebers Harper and Otsuka will be upheld by lower courts where the case is on hold. Trump may then choose to select two new board members to join his recently nominated Chair John Crews, a republican working in the Treasury Department. Or he could leave the positions vacant.

This event and its conseqences will be greeted with mixed reactions by credit union supporters.

But history can also provide us perspective to the current moment. And more importantly, point the way forward.

Not the First Time for President’s Firing NCUA Leadership

On March 10, 1976, Administrator Herman Nickerson, Jr. of the National Credit Union Administration testified before the Senate Banking Subcommittee on Financial Institutions (chaired by Senator Thomas McIntyre) regarding S. 1475. The hearing focused on proposals to restructure the NCUA from a single-administrator agency to a multi-member board.

Nickerson testified that a single-administrator structure left the agency highly vulnerable to political pressure, stating that under his “day-to-day” tenure “you don’t know whether you’re going to take a position that would be your last day in office or not”. He argued that a three-person board would provide better long-term stability and continuity for regulating federal credit unions.

In the hearing Administrator Herman Nickerson, Jr. was asked about his vulnerability to being fired, and Senator Thomas McIntyre confidently responded by assuring Nickerson that “it would never happen”.

Merely two hours after the hearing concluded, President Gerald Ford summoned Nickerson to the White House and fired him without cause.

March 19, 1976 Office of the White House Press Secretary

————————————————————

NOTICE TO THE PRESS

The President has accepted the resign.,tion of Herman Nickerson, Jr., as Administrator of the National Credit Union effective upon the appoint ment and quaJification of a succes sor. He was appointed on September 15, 1970. There is no successor to announce at this time.

The Three Person NCUA Board Legislation Approved

Senator McIntyre was reportedly shocked by the firing. He used the incident as a stark, real-time example on the Senate floor to successfully argue that the NCUA must be restructured into a multi-member independent board to protect its leadership from sudden political retaliation.

This hearing served as a major catalyst in the legislative shift that eventually established a multi-member, bipartisan board to govern the agency.

(Sources: Rosemary Hardiman, then a reporter for CUIS, Gerald Ford Library, AI search for hearing summary)

Today’s Response and the Future of Credit Unions

The three person, independent NCUA board was intended to moderate the extreme policy fluctuations if every President could choose to appoint new regulators who would then implement whatever policy priorities he wanted.

In contrast, the theory supporting independent agency status was to ensure experienced, knowledgeable board members would be appointed to protect and promote the public interest not partisan political agendas.

Only two NCUA board members could be from the same party. In theory this assured some public debate or even opposition in policy and agency oversight.

The theory worked for NCUA’s first two chairs, Larry Connell and Ed Callahan. Both were experienced state regulators with direct knowledge of credit unions. While other board appointments would appear more like political sinecures, agency leadership was in expert hands.

The assumptions of industry expertise and apolitical Chairs ended with the appointment of Senator Roger Jepsen (defeated in a re-election effort) to succeed Callahan in 1985. Rarely have future Chairs had regulatory or credit union experience with the exception of JoAnn Johnson from Iowa.

She had been Superintendent of credit unions for the state and joined the NCUA board in 2002, becoming chair from 2004-2008. After returning to Iowa she was again Superintendent of Iowa’s credit unions until her retirement in May 2017.

The vast majority of NCUA board appointments have had little to no credit union affiliation. NCUA’s board appointments have been filled with former congressional or agency staff members seeking continued federal employment. Some have had strong professional credentials (McWatters) but virtually none had prior credit union associations or knowledge.

Credit unions have long abandoned efforts, individually and as a system, to identify and promote knowledgeable individuals for NCUA positions.

Both democratic and republican administrations have used NCUA board seats to reward political loyalists versus those with credit union credentials.

In pactice the theory of the independent agency with expert leadership acting in the best interests of credit union members has rarely happened Instead NCUA board appointments have become a backwater for those seeking the prestige, or sometimes the spoils, pf a political appointment.

The Future of Federal Credit Union Regulation

Just as in 1976, there will be a reaction to the current political excesses and NCUA’s increasing impotence shaping the future of the cooperative system.

The Agency may become a department with a single administrator within Treasury, like the OCC. The NCUSIF merged with the FDIC.

The future may be a more cooperative and innovative state support system.

NCUA may be caught up in a sweeping federal government reform post election or post Trump.

Following yesterday’s precedent in this week leading America’s 250th , it is useful to express our future hopes for the country and cooperatives in music. While this was not my original choice for today, it seems to be one approach to future events when asking Who shall wear the starry crown?.