A reaction to yesterday’s comments on the merger of Vermont State Employees Credit Union and New England FCU.

…but y’know, something still doesn’t look quite right?!?

Chip Filson

In the It’s a Wonderful Life movie classic, George Bailey is granted his wish and gets to see what life would’ve been like had he never been born. He’s shocked by the results.

There was no one to fight for market competition, equality, opportunity and ownership for the working poor and middle class. Bedford Falls is renamed Pottersville.

Pottersville is packed with bars, strip clubs, casinos, and pawn shops. It’s full of cops and traffic and lights and noise and strangers. It’s filled with colder, harder people, with more violence, gambling, mental illness, debt, and rampant consumerism.

As George Bailey stated:

“Just remember this, Mr. Potter: That this rabble you’re talking about, they do most of the working and paying and living and dying in this community.”

Yesterday’s post presented a long-standing loyal member’s critique of the Vermont State Employees (VSE) merger with New England FCU (NEFCU). His objections included:

How did this idea of merging two “financially strong” credit unions arise? In a May 2016 interview with VT Digger, Rob Miller talks of his “learnings” after being hired to the VSE CEO position, his first job in credit unions:

“I thought it would be boring, frankly, to work at a bank,” he said.

Then he learned about the organization’s mission, that it was a not-for-profit financial cooperative, and that anyone in Vermont could be a member.

“VSECU’s mission – to improve the lives of Vermonters – that really spoke to me.”

“I suddenly saw an organization that had the capacity and the resources to really fulfill its mission,” he said.

His background isn’t one that typically leads to the position like he now holds, he admits.

“My first day as CEO was my first day working at a credit union. That was a big step for the board to hire outside of the industry.”

He lights up when he talks about VSECU’s latest initiative, to offer equity financing to cooperatives in Vermont, which typically only have access to debt financing. (not an FCU option)

“Coops are an important part of any regional economic development strategy,” he said. “They are locally owned, and the owners are the customers – it’s a business model that is inherently more sustainable,” he said. “It’s like paying yourself. That’s a natural incentive for success.”

“At our core, we are a cooperative. We embody people coming together to help one another,” he said.

These sentiments are certainly proper. In light of his merger initiative, the remarks suggest that human nature cannot always be nurtured.

In contrast, the CEO of NEFCU has held the top position since 1987 (almost 36 years) and will continue in that role after merger. Miller, as CEO of VSECU arrived in 2014, inheriting 65 years of members’ loyalty, resources and institutional success. He will be President and COO of the newly combined operations.

Here is a 1.34 minute video of the two men talking about this “partnership” and why a new name is important to “building a new organization.”

It is easy to understand how the two CEO’s developed the transaction between themselves, and then sold it their boards and staff. Their motivations are straight forward. It was a succession plan and capstone for the CEO nearing retirement. For VSE’s Miller it was a personal opportunity to take over a firm almost three times the size of his current job. A win for both, at the members’ expense.

No one would want stop a CEO from moving to a new job at a larger credit union. Happens all the time. But in this case the circumstance of the CEO bringing his credit union with him to this new job is highly unusual.

In the video the two men talk smoothly about “building a new organization” of 500 people. This necessitates a new name since the legacy of the old ones would hinder this process. This marketing video was part of the sales campaign. All members need to do is just vote their approval.

If you believe this “new organization” is built on the movement’s uniqueness, listen for the number of times the words cooperative or credit union are used. Or how this merger helps members. Zero. There are no beliefs like those used in Miller’s Digger awakening interview above.

This short video is professionally staged, in a garden-like setting, background theme music, the casual dress and coffee cups on the table creating an impression of shared camaraderie. It is all part of the grift.

A transaction so shallow suggests this merger of these previously sound credit unions may not be as straight forward as presented. Without a carefully considered roadmap, all the hard issues have been kicked down the road.

Here are several reasons why this merger, like many, may end up reducing, not enhancing member value.

In September VSE reported $25.3 million in borrowings as 12-month share growth fell to just 1.8%. Even with a $20 million increase in shares, the credit union’s dollar dividends to members fell 28% from the prior year. Members are paying the price for this underperformance. The credit union reduced its average cost of funds to just 16 basis points, even though short term rates have risen to almost 4%. The unrealized loss on the $136 million of investments went from nil to $25 million over the past year.

Prospects are so poor in Vermont that the plan is to take members deposits and earnings and invest those out of state. A sure fire way to retain Vermonters loyalty!

Throwing members under the bus to support an undefined merger plan is not a sustainable strategy.

It’s a Wonderful Life portrays the eternal conflict in a market economy between self-interest and those who believe in community values and stability. These two CEO’s are following Potter’s model, putting their futures ahead of their responsibility to members. The two Boards bought into the shell game; the employees put their names in the merger Notice in contrast to the values they had expressed making VSE truly special.

As the shallowness of this effort becomes more exposed, it won’t just be the members who will pay the price; the employees will learn that $100,000 plus jobs are a luxury when institutional success is the primary goal.

VSE member Don Kreis foresaw this possibility in his comment letter: If the $1.1 billion Vermont State Employees Credit Union cannot stand alone, cannot be just as convenient as a bank while giving members more value and more control than a for-profit financial institution can, then combining with another credit union is a waste of time.

The problem is not size or resources. It is a market-based society’s ever-present challenge of balancing personal self interest and community. In an earlier blog, The Tragedy of the Commons, I expressed the view that this and similar mergers were a test of whether a unique credit union system can survive:

A coop system reliant on values as a differentiator cannot long continue with coops and market capitalist wannabes side by side. For the latter will continue to prey on the former until everyone joins in the rush to get their share of cooperative gold.

Democratic coops should deliver more than for-profit banks. We need more Don Keis’s in the movement– people of goodwill who serve, who are pro-human and who knit together the fabric of society.

We need more Bailey-like credit unions that give, that contribute, and that cement communal stability.

Taking easy money is brutally hard on members.

It’s also hard on the soul.

This is the comment George would have written about the Vermont State Employees Credit Union merger proposal with New England FCU.

We all remember George Bailey from the holiday film classic set in the fictional Bedford Falls. Here is a quick synopsis from a writer who maintains the story is a dire warning about today. And perhaps the credit union movement?

It’s A Wonderful Life (Jared Brock)

For those who haven’t seen the movie — no judgment, but what are you doing with your life?! — it’s a story about an angel who is sent from heaven to help a desperately frustrated businessman by showing him what life would have been like if he had never existed.

But the B-story is a prophecy about the times in which we live.

George Bailey (played by the great Jimmy Stewart) runs the Bailey Bros Buildings and Loan Association, a company that contributes to the community by building affordable homes for owner-occupiers.

Henry F. Potter hates George’s guts. Rather than contribute to the town of Bedford Falls, Potter’s full-time job is extraction — he owns the bank, the bus lines, the department stores, and plays slumlord to a tenement called Potter’s Field.

While Potter dreams of bankrupting the Baileys so he can create a housing monopoly to milk the middle class to permanent poverty, George Bailey dreams of building “airfields, skyscrapers a hundred stories high, bridges a mile long.”

But George Bailey’s day-to-day goal is singular:

To help every working family own their own home.

Donald Kreis, a long-time credit union fan, responded to VSE’s proposal to end the credit union’s 75-year charter. His comment letter as filed with NCUA:

From the other side of the Connecticut River, the plan to merge the Vermont State Employees Credit Union (VSECU) out of existence seems like a bad idea, and I will be voting “no” on the proposal. Here is why.

Why I care about VSECU

VSECU – which I first joined when serving a judicial clerkship at the Vermont Supreme Court in 1997 – is one of the five credit unions to which I belong. I have only one rule when it comes to financial services: I don’t do business with banks, at least not voluntarily.

Investor-owned banks are in business to extract profits from their customers. I have always wanted to share my financial resources with my neighbors (or fellow employees), and I would like them to share their resources with me. A credit union is a financial institution that exists to help my neighbors and me do that, in a manner that we democratically control for our mutual benefit.

Thus, when I needed to buy my first car almost 40 years ago because my employer, Associated Press, was transferring me to a place (Portland, Maine) where I could not function without an automobile, I secured my first-ever loan from the AP Employees’ Credit Union. I was still a kid, fresh out of school, and not terribly desirable as a credit risk.

But a loan committee comprised of my fellow AP employees understood the need as well as the high likelihood that a young wire service newsperson would not renege on a promise to his colleagues. So, I got the loan.

Unfortunately, the AP credit union is long gone. Almost every credit union to which I have ever joined since then is indistinguishable from a bank. The neighbor-to-neighbor, colleague-to-colleague quality is gone. The organs of democracy have atrophied, and annual elections have become an empty formality.

There is only one exception, and it’s the Vermont State Employees Credit Union. Over the years, it has taken the idea of democratic member control seriously. It is the only credit union to which I have ever belonged that actively and enthusiastically promotes its annual election process.

What Beats Jet-Skis and Snowmobiles?

I don’t think it’s a coincidence that the VSECU is the only one of my five credit unions that actively promotes “green” lending. While other credit unions send me flyers and e-mails urging me to borrow money for leisure purposes (snowmobiles, jet-skis, extra cars), VSECU understands that what consumers really ought to be doing is borrowing money to make their homes both more energy efficient and self-sufficient.

This resonates profoundly for me, as the state official in New Hampshire (the Consumer Advocate) whose job is to advocate for the interests of residential ratepayers. Electricity and fuel prices are soaring right now, a result of our over-reliance on natural gas and other fossil fuels. But consumers are reluctant to borrow money to pay for things they can’t see, hold or drive around.

A credit union that is serious about the welfare of its member-owners will strive to educate them and encourage them to make long-term commitments to things that will make them wealthier and more secure over the long run.

The Case for the Merger – Platitudes and Generalities

Thus I was frankly shocked to learn earlier this year that the board of the VSECU had voted unanimously to merge our democracy-and-green-energy loving credit union into the much larger (and much more bank-like) New England Federal Credit Union (NEFCU). It seemed so out of character.

Naturally I assumed there were facts and circumstances of which I was unaware. When I inquired, I was told that to the extent I am entitled to information that would help inform my vote, the insights would be contained in the official document I then received. It is entitled “Notice of Special Meeting of the Members of Vermont State Employees Credit Union and Plan of Merger.”

The official Notice document does indeed make a compelling case for the merger – but only if you are willing to accept platitudes and generalities.

In the section of the Notice labeled “Reasons for merger,” VSECU states that “both credit unions are financially strong” but “face many of the same obstacles and challenges, including an aging Vermont population with slow to no growth; rapid and accelerated technology changes; environmental, economic and social change; and increased competition from out-of-state financial institutions.”

Fair enough, but this begs the question of what advantages the merger would confer as the new mega-CU seeks to confront those challenges. Answer: having swallowed up VSECU, the former NEFCU will be “better equipped to tackle the challenges facing financial institutions in a rural state.”

The Notice goes on to promise “economies of scale and combined resources” that will lead to unspecified “further improvement and opportunities” in eight listed areas – everything from “expanded branch and ATM access,” to “improved homeownership and financing initiatives to reduce energy consumption and environmental impact,” to “favorable rates and lower fees to members.”

These justifications are unpersuasive. Note the lack of promises or concrete examples of things that VSECU cannot simply do as a stand-alone billion-dollar credit union.

Economies of Scale and the CU Merger Frenzy

The “economies of scale” claim is especially troubling. The usual route to merger-related economies of scale is for the newer and bigger organization to trim staff to avoid duplication of effort. But in this instance the Notice promises that “all employees will keep their jobs and current salaries as part of the proposed merger.”

Economies of scale are indeed a ‘thing’ in the world of credit unions, but the proposed demise of the VSECU stands out. According to the trade publication Credit Union Times, the National Credit Union Administration (NCUA) approved no fewer than 86 credit union mergers during the first half of 2022 – overall, credit unions are stampeding to combine with one another – but the proposed VSECU deal is bigger than all but one of them. And in that biggest deal of the first half of 2022, VSECU’s New York counterpart – the $5.5 billion State Employees Credit Union – is taking over the smaller Cap Com Federal Credit Union.

Most of the credit union mergers in the current frenzy involve much smaller institutions. And, indeed, the consensus among industry insiders is that a credit union with less than $300 million in assets should indeed consider merging with another CU in the interest of amassing the resources to confront technological change and industry competition.

A $1.1 billion institution like VSECU already has, or already should have, all the economies of scale it needs.

Not a Merger of Equals-Equity Transfer

Although VSECU claims the proposed deal is not a takeover of our CU by the NEFCU, here is how you know that claim is wrong. If this were truly a merger of equals, then the members of both CUs would have to approve it. Because VSECU members are surrendering control of their financial institution, they and only they get to vote.

If you don’t believe me, consider what this deal would look like if both institutions were publicly traded, investor-owned businesses. The board of the ‘new’ credit union will have 11 members, six of which are from NEFCU. In the for-profit would, that would be considered a surrender of control – effectively, a takeover.

The $3 billion NEFCU intends to pay no consideration whatsoever to the current owners of the VSECU for the right to control what used to be their credit union. According to the latest 2021 balance sheet in the required Notice, VSECU members have built up $95.3 million in equity over the years – not a dime would be paid out to them in exchange for surrendering control of their credit union to its bigger and more bank-like Vermont competitor.

Such a payout would be easy enough to achieve by liquidating some of the $434 million in investments the combined credit union would have, above and beyond the $2.5 billion in loans on the books.

But, instead, the proponents of the merger are asking the members of the VSECU to surrender control of their credit union to a former competitor for free. No board of an investor-owned business would ever dare recommend such a proposal to its shareholders.

What’s at Stake? The Very Soul of the Credit Union Movement

In a sense, the impending vote on the takeover of VSECU should be seen as a referendum on the future of the U.S. credit union movement itself.

As I have already noted, VSECU stands out as a credit union that takes its cooperative identity seriously, along with its fidelity to the Cooperative Principles – the key principle being democratic member control. The New England Federal Credit Union is just another credit union that is content to operate like a bank does.

Why is this so important to me? After all, I no longer live in Vermont. I belong to four other credit unions and I even serve on the supervisory committee of one of them. So I could easily just sign and turn my back on VSECU.

I care about this because of something said to me by the CEO of the credit union on whose supervisory committee I serve. When I first met the CEO, I told him about how much democratic member control, and the other six Cooperative Principles, meant to me as a volunteer credit union leader.

In response, the CEO pulled out a cell phone and waved it in my face. The CEO mentioned an adult daughter – this executive’s go-to proxy for a typical credit union member. “Do you know what she cares about?,” asked the CEO. “It’s not voting. It’s this.”

The “this” to which the CEO was referring was the credit union’s phone app that allows members to do their banking from the device they carry around with them in their pockets and purses.

If that’s truly what all of this comes down to, then I give up and so should everyone else in the credit union movement. Credit unions can and should strive to keep up with the convenience-enabling technology deployed by the mega-banks.

But if credit unions can’t deliver value to members above and beyond the convenience that for-profit financial institutions already offer, there is no reason for them to exist.

In other words, if the $1.1 billion Vermont State Employees Credit Union cannot stand alone, cannot be just as convenient as a bank while giving members more value and more control than a for-profit financial institution can, then combining with another credit union is a waste of time. Instead, the Board of VSECU should just pay out that $95 million in member equity and turn over its loan portfolio, its deposits, and its checking accounts to some ultra-convenient bank.

Do Not Succumb to Cynicism and Fear

Indeed, maybe we no longer deserve VSECU as we have come to know and love it. Maybe we are unworthy of a democratically controlled financial institution.

When VSECU first announced the merger, and the skeptics began speaking out, the Board and management circled the wagons instead of treating member activism the way it deserves to be treated – as a welcome expression of commitment to the institution they collectively own.

In that sense, the leaders of VSECU are no different than the board and management of every other cooperative that has had to deal with members who flex their ‘democratic control’ muscles and question their elected representatives.

Maybe it’s just human nature – but, if so, then maybe “democratic member control,” and other Cooperative Principles like “education, training, and information” (which suggests members should be fully informed about the business realities their cooperatives confront), are just outdated platitudes.

We live in cynical times. So, it is not surprising that, even in Vermont, both the proponents and the opponents of the buy-out of VSECU by a bigger credit union question the motives and integrity of the other side in this discussion. I refuse to succumb to that cynicism.

Thus, I am grateful to the VSECU Board of Directors for presenting this proposed merger to us for a vote, and for making its best case for why we should ratify the deal. They, in turn, should understand my frustration over not having access to all of the information they had at their disposal as they deliberated.

Lacking that information, or any other compelling reason to vote in favor of consigning the Vermont State Employees Credit Union and all it stands for to oblivion, I vote “no.” I urge my fellow VSECU members to do likewise, in the hope that the VSECU of the future will look less like a bank and more like a cooperative.

If this credit union, with its commitment to cooperative culture and public service, cannot survive and thrive as an independent, community-owned, democratically controlled financial institution, then all is lost. I refuse to believe that.

END

He has served since 2016 as New Hampshire’s Consumer Advocate, heading up a small but feisty state agency whose purpose is to advocate on behalf of the interests of residential utility customers before the state’s PUC and other bodies (including FERC). Previously he served as general counsel at the New Hampshire PUC, as a hearing officer at the Vermont PUC, and as a professor at Vermont Law School, where he still teaches on a part-time adjunct basis.

Prior to becoming a lawyer, he was a full time journalist for nearly a decade, first with Associated Press and then at the fabled newsweekly Maine Times.

He served for eleven years on the board of the nation’s second biggest retail food co-op (the Hanover Consumer Cooperative Society) including three years as president. He was a nine-year trustee of what is now known as the Cooperative Fund of the Northeast, a CDFI that loans money to cooperatives.

He believes credit unions ought to live by the cooperative principles – and take democratic member control seriously.

His custom when joining a new credit union is to follow up about a week later with a request for the CU’s bylaws and express interest in seeking election to the board. That has inevitably been met with something on the continuum between bewilderment and hostility, except at the CU that invited him to join its ALCO and Supervisory committees.

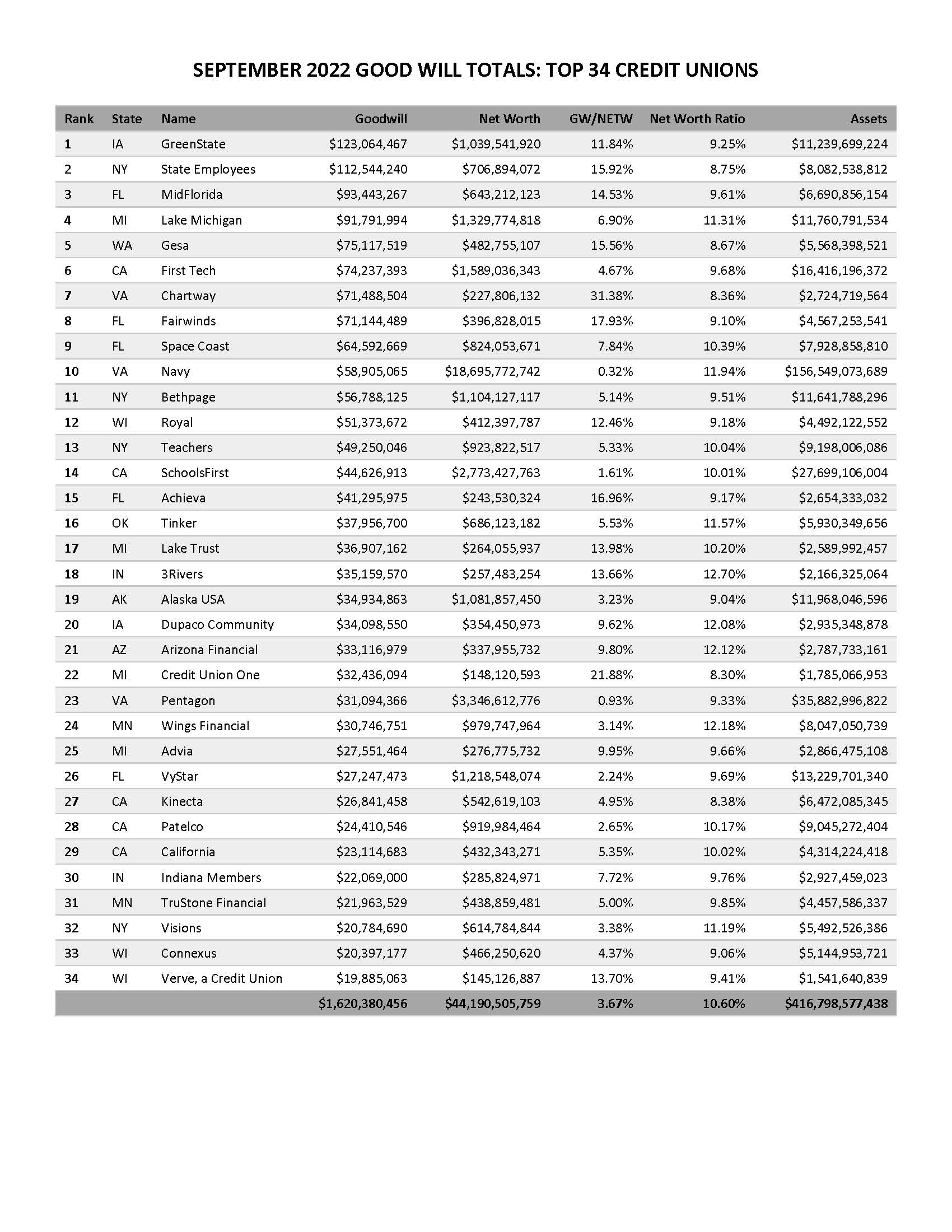

In this second blog I look at examples of goodwill. What are some of the financial and regulatory implications of this ever increasing intangible asset?

The following are the 34 credit unions (out of 277) with the largest amounts of good will at September 30, 2022.

The goodwill net worth ratio, column three, compares the size of this intangible asset to net worth. This ratio ranges from a high of 31% for Chartway to a low of .32% for Navy FCU. There is no regulatory limit on how high this percentage can be.

The goodwill net worth ratio, column three, compares the size of this intangible asset to net worth. This ratio ranges from a high of 31% for Chartway to a low of .32% for Navy FCU. There is no regulatory limit on how high this percentage can be.

While I do not know the details of every credit union listed, most of these goodwill leaders occur from either whole bank purchases or mergers with other credit unions. The first two names, GreenState and State Employees (NY) are examples of each activity.

As discussed in Part I goodwill is an intangible asset representing future economic benefits arising from assets acquired in a business combination, traditionally mergers or purchases.

It is not part of equity or retained earnings from a presentation standpoint.

Goodwill lacks physical substance. It is an accounting estimate based on assumptions used to project potential future value. Unlike mortgage servicing assets which are also an intangible, goodwill can’t be bought or sold.

If credit union A merges with credit union B which has goodwill on its books, credit union A receives no benefit. Credit union B’s goodwill is devalued to zero. It is not carried over onto credit union A’s books.

As the underlying benefits are realized, impairments to goodwill can be recorded. A credit union can also amortize goodwill over ten years. In both instances those charges flow through the income statement and reduce retained earnings.

In either option, all goodwill must be assessed for impairment at least annually.

For credit unions following CCULR: Goodwill is not part of Net Worth (numerator) for ratio purposes but is included in total assets (denominator) to determine the net worth ratio (NWR). Goodwill balances must be less than 2% of total assets to opt into CCULR.

For credit unions subject to RBC: Goodwill is a reduction from the RBC Numerator and also from the Denominator.

In corporate America public companies report over $4 trillion of goodwill on balance sheets, primarily from mergers and acquisitions.

While accountants agree on what goodwill is, how to value that goodwill after it’s passed onto the buyer’s ledger sparks plenty of argument.

There is much uncertainty about forecasting goodwill’s future benefit for a firm – it involves more judgement calls than many accountants are comfortable with. And while goodwill is listed as an asset on the balance sheet, is it really worth its stated value? What if it was a bad buy at an inflated price in the first place?

In June 2022 FASB announced it had given up on a four-year effort to simplify goodwill accounting determinations. The current annual impairment test remains the requirement versus a straight line annual amortization approach.

When creating goodwill, credit unions have all of the same accounting challenges as public companies but none of the checks and balances .

The ongoing difficulty is assessing post acquisition performance to see if it is meeting the values projected when the goodwill was first established.

In cooperatives this is made much more difficult because in both mergers and acquisitions, there is virtually no public disclosure of an acquisition’s costs let alone future projections.

For purchases, credit unions rarely report the total price paid(except when a bank is publicly traded) the broker and transaction fees, the future impact on ROI or ROE and the longer term performance goals to be achieved. For mergers, no details of a combined operational plan are provided just the asserted advantage of bigger size and more capital.

Most large mergers and whole bank purchases take years for operational and business integration to be fully realized. These transactions generally end relationships and market presence created from years of continuous service. That history and local advantage is now gone.

In some large credit union mergers a whole new corporate brand and identity are part of the combined entity’s future business plan. Shedding past connections to create a whole new market persona would seem to undermine a valuable legacy.

Credit union mergers and bank purchases are not market based transactions. They are private deals negotiated for mutual advantage by CEO’s and then announced to members. Because there is no transparency or numbers provided, little future monitoring possible.

Both transactions create goodwill but the credit union is playing with members’ house money. If the deal works out after three or four years, whatever benefits of expansion have been achieved are trumpeted as the result. If the bank purchase was overpaid, there is no stock price or performance metric that would highlight this misjudgment.

The bank owners are paid a cash premium for their shares from the members’ savings. They have left with cash in hand. If a transaction is poorly priced or managed, then the goodwill is written down from members’ existing capital.

The goodwill concept allows managers to pay premiums for purchases absent any performance goals. In a merger, goodwill in excess of book net worth just enhances the ongoing credit union’s capital but members receive nil for this value.

When leaders operate in a closed environment, unconstrained by member or board governance, personal ambition can run amok.

With no meaningful credit union disclosures to members or the public in either mergers or bank purchases, managers are free to wheel and deal. A number of CEO’s have been very public about their “nonorganic” growth plans. Goodwill is the intangible asset created to make things appear OK regardless of price or terms.

The animal spirits of capitalism are quickly embraced versus the cooperative focus on members’ well being. But unlike truly competitive markets, there is no stock price or market assessments monitoring performance.

When goodwill accounts begin to approach 10% or higher of net worth, the credit union has disguised its ability to produce operating earnings. To keep the game going, more purchases and goodwill are pursued, always justified by scale and more diversification.

At some point the economy turns, the acquired assets become overvalued and members are given the short stick as dividends are reduced to keep up the ROA goals. In several of the credit unions listed dividend payments were reduced in 2022 versus 2021 to sustain ROA even though short term rates have risen by over 3%.

Staff layoffs are another indication of overcommitments. Examiners or accountants will start to question the goodwill asset’s value.

The goodwill that underwrites cooperatives can quickly turn to ill-will. When members realize their collective legacy in mergers was transferred to solely benefit senior managers, the loss of confidence will undermine both the new entity and the cooperative system’s reputation for fair dealing.

When the out of state or out of market bank purchase shows no growth, the tactic of buying market share begins to fail.

The facade of goodwill falls away for both the credit union and the members. Once gone, it is lost forever. That is what intangible means.

“Forgive us our debts, as we forgive our debtors.” We say these words in the Lord’s prayer. Where have we seen this ever done in “real” life?

Society, especially market-based ones, do not practice debt forgiveness. Capitalism is built on finance, i.e. all kinds of debt—corporate, consumer and government.

In the bible, the Jubilee year – occurring after every seventh Sabbath year, thus, every 50 years is an economic, cultural, environmental and communal reset, when the land and people rest, and all those who are in slavery are set free to return to their communities. (Leviticus 25:1-13).

Debtor’s prison or indentured servitude, was a reality in England and other countries for those who failed to pay up. It was the basis of more than one of Dicken’s novels. Scrooge is more than a Christmas story. It was reality.

President Biden’s forgiveness of either $10,000 or $20,000 in student debt has been met with gratitude by millions of former students who have applied for this reduction.

On the other hand, multiple organizations and opponents have taken to the courts to stop the plan absent Congressional approval. The question of whether the President has the authority to do this unilaterally is now before the courts.

Some former students who paid off their loans, feel this action is unfair to those who honored their obligations.

Credit unions were founded to provide debt. Credit for members funded by savers. Often the phrase “for provident and productive purposes” is intended to show debt as a positive event.

Founding stories such as that at BECU where a small group employees contributed 50 cents each in 1935 to create Covenant credit union to provide tool loans during the depression, are apocryphal.

Credit unions spend much effort and processes to make sound loans, track delinquency and minimize loan losses.

But debt forgiveness? That is rare indeed. Recently this video by Canvas Credit Union shows the power of debt forgiveness. Addie Greenacre, a long-time Canvas member, wife and mother was surprised with a $40,000 loan payoff as part of a drawing during an auto refinance promotion.

It is a powerful example of what removing the burden of debt can mean to a person.

(https://www.linkedin.com/company/canvasfamily/videos/)

How do credit unions founded to provide debt ensure that loans lift up and don’t become a lifelong burden?

Looking at the Canvas Credit Union model one sees an organization dedicated to financial well-being. In their words, We’re here to Help You Afford Life.

While this “debt forgiveness” may have been a promotion, it demonstrates the power of jubilee thinking for people, and a community.

As credit unions review their personal loan portfolio at yearend, seeking those with the longest tenure or constantly rolling over draws, might a debt jubilee be a timely addition to every credit union’s service profile?

It can literally change a person’s life. Isn’t that what credit unions were meant to do?

Last Friday’s blog described the multiple losses should the merger of Vermont State Employees (VSECU) with New England FCU proceed on January 1, 2023.

The members lose their credit union; 190 employees their career paths and individual agency; local communities– their partnerships; the state of Vermont– its leading cooperative financial institution; and the overall credit union system, another pubic example of purpose compromised by leaders’ self-interest.

The tragedy of the commons occurs when persons in positions of responsibility exploit the common resources of the community which they oversee for personal gain.

Should credit union leaders continually seek to acquire and merge sound, long serving credit unions, like VSECU, to fulfill their individual ambitions, I believe this will lead to the demise of the cooperative credit union movement.

VSECU’s example and innovative track record were so successful, that it was the subject of a 15- page analysis by Callahan’s September 2021 Quarterly Report. Several of these accomplishments were republished in five articles in January 2022 on cu.com, for example this description responding to the COVID crisis.

At September 30, 2022 the credit union reported $1.1 billion in assets; 71,625 members and 9 branches; $6.5 million in YTD net income and $102 million in equity. Average salary and benefits per employee exceeded $100,000.

Against this documented track record of long-term innovative performance, VSECU’s merger information offered nothing about the future. The credit union was already more than full service; it had pioneered special initiatives pursing a “greener” environment.

The continuing credit union’s leaders at NEFCU made no commitments to VSECU’s 71,000 credit union members’ who hold $922 million loans and $980 million savings. These members will be under the full sway of a board they did not elect and management that has no connection with their firm.

So undefined is this transaction that both CEO’s admitted in this twitter post, the consolidation would take over a full year to conclude and will require a completely new brand identity and name.

The back office conversions, product/service alignments and leadership selections will be the top priority at a time when members of both credit unions face economic uncertainty and anxiety from decades-high inflation.

In the Calling All Members website, the opponents point out that the two credit unions have very different fields of membership, histories, and market focus:

The continuing federal credit union’s Field of Membership will not be based on geography or residency. It will be numerous employer groups and organizations located in Vt, MA, ME, RI, CT, MI and even groups headquarters in San Diego and San Francisco. . . our statewide cooperative built by Vermonters for Vermonters will be gone—forever.

Two typical industry reactions to this latest example of a successful credit union being acquired by another include: “Not my problem” and “Didn’t the members approve?”

I believe this pattern of sellouts and acquisitions by cooperative leaders will ultimately lead to the end of a cooperative financial system in America. Here’s why.

The foundation of every credit union is member relationships. Almost all credit unions were started with no capital. They earned the loyalty of members by promising to be a different kind of financial firm.

Member-owners were invited to put their trust in their leaders and board. The affirmation of this process is the democratic one-member, one-vote design.

This merger now places VSECU’s relationships under the direction of strangers.

The action is based on the illusion that size is all that matters. Credit unions have never competed on size. It is a unique coop fantasy that coops can marry two mice and produce an elephant.

When size is the dominate goal, it becomes a trap of endless growth not creation of member value.

VSECU’s members have continually contributed more than sufficient resources to continue a long-term vision of hope empowered by local control and focus. The credit union has become a financial “sanctuary” established by members’ belief and trust.

Now their leaders (senior management and board) have abandoned them for the “Golden Calf” of “instant mass,” not substance. There has been no planning or discernment with those that built the institution and who own it.

The process of voting is nothing but an administrative fig leaf completely under the control and oversight of those temporarily in power and who have a vested conflict of interest. Only 21% of members voted. Of the total membership. just 316 votes (.4%) is the difference between those supporting and those opposing. This was certainly no vote of confidence in charter cancellation.

It would seem fool hardy to decide the fate of a 75-year old, high performing coop with such a micro thin margin of owner approval. It also raises the question of how the voting was managed by those who advocated only their side of the issue.

Regulators continue turning a blind eye and washing their hands of responsibility.

Mergers are the wild west of today’s financial markets. Second only to Crypto transactions, until that industry’s implosion is over.

Coop CEOs/boards are literally buying and selling millions of member relationships to firms with no connections, increasingly out of state, and who are unconstrained with what they can do with them. These kinds of hollow transactions and disclosures would normally attract the intense scrutiny of an SEC or FTC regulator if these were stock owned institutions.

Coop regulators would rather talk about inflation, consumer protection, fintech, DEI or other current topics rather than the elephant in their room.

Contrary to their assertion that this is just the free market at work, these are back-room deals, negotiated in private, devoid of transparency and without any public attempt to find the “best” deal for members.

Regulators avert their gaze pretending to be deaf, dumb and mute as they oversee the disintegration of the coop system.

VSECU’s leaders betrayed the trust members gave them. Credit unions embody the spirit of community. This action dissolves this special bond built by three generations of members.

The merger destroys the fundamental foundation of a cooperative leaving a financial eunuch in its place. It has no cooperative character or roots. Unlike a stock transaction, it lacks the credibility of a market affirming price. In these transactions, coops have devolved into purely private entities, controlled by individuals acting to consolidate and accrete their own power.

These are not people helping people; rather these mergers demonstrate CEO’s helping themselves.

One can understand why NEFCU’s CEO wants control of 71,000 member accounts with average combined member loan and savings balances of over $43,000. And to be given over $100 million of their collective savings while eliminating this vigorous, innovative competitor. No more “free” market choice for either firm’s members, or the general public.

This kind of transaction has no economic rationale or “market” driven basis. There is not a firm anywhere in America, coop or otherwise, who would not line up to accept such a generous “gift.”

VSECU’s leadership had embraced the Global Alliance for Banking Values (GABV) vision of “Finance at the service of people and the planet for the real economy.”

Their collective decision to transfer their fiduciary responsibilities to another firm show that corporate and personal values need not align. It certainly refutes the biblical adage that a person cannot serve God and mammon at the same time.

Self-interest may appear to succeed in the short term, but in the long term, it fails as a strategy. When the vision of the cooperative is “all I want is everything” personal ambition will fail for what only a community can sustain.

People are not stupid nor uninformed about these sham transactions. Most members follow their personal financial situation as a top priority. It is a heightened concern especially in a time of rising rates. When member generosity and loyalty is compromised by self-interested mergers, their support will fade away.

These transactions will end the unique public role for credit unions. Acting like banks, they will be treated like their for-profit competitors.

Regulators who have approved these pillages of common wealth for private gain will find themselves thrown in with all other financial overseers. The playing field will indeed be level.

There will be no credit unions on it. No tax exemption. Just wealth seeking institutions led by similarly motivated individuals.

The practice of buying and selling relationships is not new. It is part of the capitalist markets drive for greater and greater market share.

It is why the states and Congress authorized the tax exempt cooperatives as an option to prevent this exploitation.

A coop system reliant on values as a differentiator cannot long continue with coops and market capitalist wannabes side by side. For the latter will continue to prey on the former until everyone joins in the rush to get their share of cooperative gold.

Nothing will stop this pattern of private theft until persons of courage and confidence step up to call out this rapacious behavior. If this fails to occur, then as predicted on the Calling All Members site the national system of cooperatives, just like VSECU, will be gone-“forever.”

The elections this week were full of last minute drama. There will be many consequences yet to be sorted out from the results.

In one case the vote was especially close. Only 318 votes separated the two sides. The percentages were 51.1% versus 48.9%. Certainly one of the closest elections ever.

Voting participation however was not particularly high in this critical ballot. Of the eligible voters, only 21% cast votes.

The results were announced in this document on November 9th after polling had closed.

However this was not a republican vs. democrat political election. It was a vote to extinguish the charter of a 75-year, innovative state chartered financial cooperative.

The official tally was 7,622 for the merger and 7,304 against. The result is that $1.1 billion VSECU and its 71,000 member-owners will no longer have their own credit union.

It will be merged into the $1.9 billion New England FCU, officially on January 1, 2023.

Voting matters. By law the charter belongs to the member-owners, not management or the board. The leader’s duty is fiduciary, to always act in the members’ best interest. Voting is the core of democratic design.

So when almost 50% of members vote against a strategy that management has tried to sell them for almost a year, such a no confidence result would cause most responsible leaders to rethink their plan.

When announced in February, the opposition was visible, public and well thought out by conscientious members who launched their own website, Calling all Members. The State Employees Association Board of trustees voted to oppose the merger.

Even controlling all the communication and marketing resources, member contacts and legacy relationships, the vote barely exceeded the required majority. The members sense there is something that doesn’t add up in this charter cancellation.

The merger explanation contained two specific benefits: the NSF fee would be reduced by $10 and access to NEFCU branches would be opened. Both “benefits” could have been done immediately without merger.

The reasons for merging was given in rhetorical phrases about future plans and a new partnership, but no specifics.

The math for coop mergers is simple, 1 + 1 = 1. There is no increase in members, loans, capital or any objective market share measure. Instead one charter goes away along with its independent leadership and business strategy. VSECU relationships, good will and member loyalty is dissolved after 75 years and three generations of building its unique identity.

There was not even a thank you dividend for the $100 million in collective equity now transferred to the control of a new board and management with their own financial priorities and strategy. They have no operational or political connection with the 70,000 members who created this common wealth.

The merger announcement included the VSECU CEO’s observation: Our membership is highly engaged in the democratic process as member-owners evidenced by the highest credit union voter turnout ever in our history,” noted Miller. “As we look toward the future, we are excited about the opportunity this partnership promises and ready to take VSECU into our united future for all of our members.”

There are other consequential problems with this transaction. The first rule of financial soundness is to not put all one’s eggs in a single basket. This merger increases concentration and reduces diversification for both credit union members and the Vermont system.

Separately these two credit unions competed for market leadership and innovation. Now they are 47% of the Vermont credit union market by assets and 40% of members. That concentration should raise both financial as well as public policy issues. As the American Banker’s lead story on February 23, 2022 described the situation, Vermont’s Largest Credit Union Merging with Rival.

Vermont’s credit union system is smaller, losing it largest state charter with total credit unions numbering just 17. Traditionally, the state charter has been more innovative and flexible than the federal option, but the largest example of that difference is now gone. The political sway in state debates is lessened both institutionally and by members.

From VSECU’s press release:

The two credit unions will continue to operate separately as VSECU and NEFCU until January 1, 2023. On that date, VSECU will become a division of New England Federal Credit Union. No changes will occur for members of either credit union while integration of systems, services, and products occurs. While there is no firm deadline for the conclusion of the integration, it is expected that the combined credit union will operate as one entity later in 2023.

Currently, it’s banking as usual at VSECU, soon to be a division of New England Federal Credit Union, until we identify and create a new name for our combined organization.”

With 50% of “highly engaged” members opposing this cancellation of their independent charter, how many others feel the same way? The new name, organization and operational integration is over a year away. How many will wait around to see what this new identify and “vision’ looks like?

A number of years ago VSECU became one of a very few American credit unions to join the Global Alliance for Banking Values.

The vision of this global network is: Finance at the service of people and the planet.

Our collective goal is to change the banking system so that it is more transparent, supports economic, social and environmental sustainability, and is composed of a diverse range of banking institutions serving the real economy.

In support of this effort VSECU announced its own expanded vision five years ago:

“To inspire a movement that brings people together to empower the possibilities for greater financial, environmental, and social prosperity.”

The goal? To align our organization with a larger movement of values-based and impact-driven organizations in Vermont and around the world.”

Two major initiatives were begun as part of this restated purpose. One was called Powered by VSECU to stimulate social and economic opportunities through innovative partnerships around the state.

The second was Alternative Capital, to help small businesses and coops raise financing including direct investments in coops. VSECU was one of the few credit unions making these coop investments.

This new vision from 2016 lasted just five years. The merger has no expressed vision. The credit unions will continue what they were doing until they figure out the combined operations and develop a new name and brand. Both credit unions are giving up their historical legacies.

Many VSECU’s members sensed that this combination promised nothing and took away what the valued. The fact VSECU management gave up on their vision less than five years for an undefined merger, foreshadows a challenge retaining the trust of the members who built this organization.

More is at stake than just member-owner patronage.

At a time of increasing economic uncertainty and record inflation, the one institution members have counted on is no longer theirs.

Members have lost their capital, their independent leadership, their long established relationships and their unique identity.

Moreover in this stressed economic moment, members of both institutions will spend millions of dollars on vendor contract cancellations, product and operational conversions, and payments due when benefit plans are terminated.

Both sets of employees will eventually be rationalized. No organization needs two marketing, HR, mortgage lending, and operational leaders. There is no efficiency from scale without redundancy reduction. Aspirational professional career paths are eliminated.

The credit union system in Vermont loses its state leader and its ability to influence local regulatory and political institutions when change is desired. Larger credit unions tend to separate their self interest from the system that spawned their creation in the beginning.

The national credit unions system has lost one of its examples of green leadership. VSECU Eyes a Green Future in Vermont, is just one story of a series at creditunions.com portraying the credit union’s business innovations. The stories exist no more. The institution is gone. Size becomes the goal, not values.

With widespread opposition and an absence of any concrete benefits or plans, the merger has cost thousands of members and multiple interdependent organizations real losses. The transaction comes at a time of heightened vulnerability for members and institutions.

Positive momentum is lost. Priorities become institutional assimilation projects, not serving local communities.

As one member read the posted results he wrote that within a year or so employees will be gone to “pursue other opportunities” and collect the benefits from their terminated plans. He ended saying: The board and senior leaders were hired to serve the members. What makes me deeply sad is not the money, it’s the betrayal.”

To build a successful credit union on a foundation on member loyalty and trust takes years. Both can be lost overnight. In a single election.

|

| Balanced lending… |

Many, many credit unions have successfully implemented risk-based lending to the benefit of each and every member. More and more members are calling out and demanding increased risk-based lending by credit unions. Never has one concept been so uniformly and enthusiastically accepted by the masses. RBL is the top requested service on every member survey – right?.

One CEO told me that RBL was an easy sale to the Board after one Board member got back from an RBL seminar cruise. Evidently, in the bar, the Board member was chastised by an RBL advocate with the arguments: “You mean you charge the same loan rate to an admiral as you do to an E-4? You mean your school superintendent pays the same rate as the first year teacher? The blue collars get the same deal?! Do your maid and gardener get the same rate you do? That’s not fair! You’ve got to start running that credit union like a business these days!”

|

| Secret formula… |

Critics try to make an issue out of the “unfairness” in RBL. They always want to claim that while RBL may achieve consistency in credit union lending decisions, RBL was never designed to achieve fairness. With RBL, members are divided into risk “classes” (A,B,C,D,E, etc.) based on a secret formula of risk criteria.

Although the secret formula for risk criteria isn’t advanced enough to tell us which exact member will default, it is explicitly accurate in knowing which “class” to which you and I should belong. There are no shades of gray in an empirical, statistical model. Don’t tell me about the divorce, the flood, the death in the family, or the reporting error. Your statistical record speaks for itself. The secret formula knows who you really are in your heart of hearts. Cut the whining, pay the rate; fair is fair!

Complainers also don’t seem to appreciate the need to eliminate the subsidies within a credit union to “low class” borrowers. The financial stability of the wealthy few is being imperiled by the working class majority. If the poor can’t pay their loans, logically they should be charged a higher rate.

|

| A New Class Act? |

But we haven’t even begun to fully exploit the benefits of risk-based pricing for the membership. Hope we can use the secret formula to help make some of the other operations of the credit union fairer. We’re already getting behind on the innovations being implemented by our guiding lights over in the banking industry.

Those creative banks have started coding customers into green, yellow, and red “classes” at the call centers. Regardless of how long you’ve been waiting, green goes to the head of the queue. Greens have separate, fast teller lines and receive special services. Bright, bright greens can even receive “private banking” services so they never have to rub elbows with “the riffraff”. Don’t we want to serve our “best” members, too?

Whose credit union is it anyway?

Serving the members based on the distinction of “class” will go a long way toward increasing a sense of fairness and building unity within the credit union. We certainly haven’t been “a class act” in the past but surely everyone agrees that – in a cooperative – some members are more equal than others.

(from Jim Blaine)

Many challenges confront credit union focused news reporting. Publishing daily via social media is hard. Staff is limited. Original stories take time to develop. Amplifying press releases is often an easy solution when faced with daily deadlines.

Credit Union Times and CUToday have developed important reporting niches however. If readers follow these original stories, they can provide insight into events that have consequences for the future of the cooperative system.

Peter Strozniak of Credit Union Times follows court cases about credit unions. On October 4, he reported on the embezzlement at the $3.2 Prairie View FCU: Former CEO Pleads Not Guilty to Embezzlement Charges. Some of the details in his coverage included:

In eight of this ten-year fraud time frame, the credit union reported annual operating losses on its call reports. The credit union was merged in the first quarter of 2022 due to “its poor financial condition.”

The question that jumps out is how could NCUA examiners have continually missed this illegal activity for ten years?

Peter did not go there with this story, but the details certainly raise a core question about NCUA’s supervision of the FCU. It was small, with few employees and only 600 members. The call reports showed losses for most years. What does this case imply about the efficacy of NCUA’s annual examinations?

For most of this year, CU Today has summarized the merger activity posted from NCUA’s web site, Comments on Proposed Mergers.

Their latest reviews showed “CUs seeking to merge in multiple other CUs at once, combo’s in which the merging and acquiring CUs are both losing money, and several examples of credit unions reaching across state lines and even across country for merger partners.”

This reporting which includes the latest data and quotes from the member notices, takes a lot of work. Some examples.

One summary is for AIM Credit Union in Dubuque, IA. It is merging two Keokuk credit unions. Members of both merged credit unions were given identical Notice statements. They will be voting on the same day at the same location, First Christian Church. The two towns are 150 miles or about three hours apart. Was a local merger of the two credit unions considered?

In the merger of two Michigan credit unions, Community Alliance Credit Union ($108 million) with People Driven Credit Union ($355 million), the top three executives can receive a total of $542,000 in severance.

Community reported midyear capital of 8.39% and a loss of $73,000. The members were offered nothing of the over $8 million in capital being transferred. Is this an example of taking the money and running away?

The three-year old Maine Harvest FCU with 56% capital is merging so that “its mission of lending to farms and food producers will be better preserved with a larger credit union that embraces that mission.” Was this option researched at the start? Why not create a partnership, versus merger, with a larger credit union if more services are needed?

The $210 million Emory Alliance Credit Union in Decatur GA is merging with Credit Union 1 whose main office is listed as Rantoul, Il. One wonders why? Were no local options available? Did Emory do any due diligence on behalf of their members, especially of Credit Union 1’s recent initiatives before recommending this out of state takeover?

Finally, the $226 million Parsons FCU in Pasadena, CA is merging with the $1.1 billion Skyla FCU in Charlotte, NC. Parsons has almost 11% capital. Merging with a credit union across the country, especially with very strong instate options, would appear contrary to every common sense notion of member service and value. What is the reason for this “merger” almost 3,000 miles away.

CU Today and Credit Union Times are serving a vital public, cooperative service developing this fact-based reporting.

Both media raise important questions about motivations and fiduciary duty of persons responsible for these events.

This original reporting raises critical questions about the directions of credit unions, the regulator’s oversight and how members’ best interests appear to be so cavalierly and repeatedly disregarded.

Sooner or later the stories behind these events will come out. The political and repetitional consequences will impact every credit union even when excesses may be the work of only a few.

A diligent, informed and questioning press is critical in holding those in positions of responsibility to account. CU Today and Credit Union Times are doing the job of the 4th estate. Are credit union leaders getting the message?