There came a dove, an Easter dove, When morning stars grew dim; It fluttered round my lattice bars, To chant a matin hymn.

It brought a lily in its beak, Aglow with dewy sheen; I caught the strain, the incense breathed, And uttered praise between.

It brought a shrine of holy thoughts To calm my soul that day; I caught the meaning of the note, Why did it fly away?

Come peaceful dove, sweet Easter dove! Above earth’s storm and strife, Sing of the joy of Easter-tide, Of light and hope and life. (1910)

After

Easter’s Freedom

In a famous passage of Paradise Lost, Milton’s God acknowledges that He could have created Adam and Eve without freedom. But what would there be to praise? “Not free, what proof could they have given sincere / Of true allegiance, constant faith or love, / Where only what they needs must do appeared, / Not what they would?” (Source: Legalizing the Resurrection)

In “The Prologue” to The Canterbury Tales Chaucer celebrate nature’s awakening life and, in humans, the need to once again gather together on pilgrimages. “April” comes from the Latin aperire (to open) and apricus (sunny) as the month of the sun and growth. (Source: Jefferson Reads)

From “The Prologue” to The Canterbury Tales:

When in April the sweet showers fall

And pierce the drought of March to the root, and all

As Easter approaches, the joyous celebration of new life, hope, and renewal is juxtaposed against the backdrop of ongoing conflict in Ukraine. Yet despite the solemn realities of war, many still find comfort and fortitude in the timeless traditions and spiritual significance of Easter. It serves as a reminder of the enduring power of faith and the resilience of the Ukrainian people in the face of adversity. Hopefully, it will also magnify your own Easter celebration.

The Orthodox Easter is celebrated on May 5th in Ukraine this year; more than a month apart from our March 31st Gregorian calendar celebration. For Christians everywhere, Easter marks the resurrection of Jesus Christ and signifies the triumph of hope over despair, light over darkness, and life over death. It’s a time when families gather, communities of faith come together, and hearts are lifted in praise.

Hand-painted Easter eggs hold particular meaning in Christian symbolism. They represent the resurrection of Christ and are often adorned with traditional designs, each carrying their own significance. Triangles, for example, characterize the Holy Trinity.

Today is Maundy Thursday of Holy Week. The day of the Last Supper and Jesus’ arrest in the Garden of Gethsemane.

Events on this and subsequent days include two intense examples of human motivation not limited to strictly spiritual contexts. Rather the story shows how any individual might react to events in their own life.

Prophets and Honor

Every social system has ways of recognizing the successful and the benefactors of their profession. In credit unions a major event is the Herb Wegner dinner, the occasion for presenting lifetime achievement awards to honor selected leaders.

These traditions salute individual’s values and/or performance that fulfill the goals of the industry: profit, service, innovation, growth or even longevity. Some goals are very tangible, others more qualitative.

Those Without Honors

But whose contribution does not get honored? The topic is raised at least twice in the New Testament:

In Mark 6:4 Jesus said to the crowd, “A prophet is not without honor except in his own country, among his own relatives, and in his own house.”

And, in Luke 4:24 (English Standard Version 2016): “Truly, I say to you, no prophet is acceptable in his hometown.”

Why this disbelief? Does familiarity breed contempt? Are we skeptical of any special insight let alone prophetic wisdom from persons we know well, have worked with over years. and who seemingly share the same experiences as everyone else? Why should one peer’s views be trusted over another’s?

There is an inherent caution to see those among us, whom we know well, as having special insight versus merely expressing a different opinion. Persons, often outsider who focus more on the message, are often more inclined to listen to these singular views.

Ordinary people can have extraordinary wisdom. Sometimes their outspokenness make them unpopular with those in authority or leadership. The “prophetic voice” is uncomfortable. It challenges current shortcomings often with a passionate hope for a different future. For those who are being challenged, this passion feels like anger.

I am not referring to the purveyors (often consultants) of innovation who promote operating improvements. The prophet’s concern is more deeply rooted in fundamental meaning and purpose.

The question for credit unions is, are there any prophetic voices challenging local or national priorities today? Who might they be? What is basis for their critique?

And if we can name none, what does that say about the state of our “movement”? Has consensus trumped wisdom?

The Thirty Pieces of Silver

A second example routinely pulled from Maundy Thursday is Judas’ betrayal of Jesus in the Garden for 30 pieces of silver.

Think of how often this metaphor is used to accuse someone taking an action for monetary or other rewards seemingly to betray their personal beliefs.

Rev. Megan Brown takes a more nuanced view of Judas’ motivation:

“Judas was not a peripheral bystander, but one of the twelve, the inner circle of disciples who had accompanied Jesus in his ministry and in a shared, communal life together.

Surely Judas knew the implications of his actions. Surely, he knew that the chief priests and the elders were growing weary of this rabble rouser, Jesus, and that they wanted him gone. This exchange, and the kiss that follows later are ominous moments in the life of Jesus and his followers. They leave one wondering about Judas’ motivations. “

Judas was a believer. Some have interpreted his action as driven by deep disappoint that Jesus was not radical or bold enough in his Jerusalem journey. The march from the Mount of Olives to the Temple should signal a rebellion against Roman rule, not a pacificist call to turn the other cheek.

Or, maybe he sensed that the multiple political forces mobilizing against this upstart rabbi from Nazareth were becoming too strong; so he decided to go to the other, more likely “winning” side.

Perhaps he was emotionally confused by the historical intensity of the Passover remembrance, the increasing crowd appeal of Jesus and the growing immanence of a life-making choice.

What we know is that Judas deeply regrets his actions, attempts to return the silver coins and commits suicide.

Judas shows us the very human side of intense hope and belief. Is this a movement that will go in the directions I believe it should? Is there another option to this leader’s course of action? How does one express dissent if convinced current directions are not the best?

How many initial “reformers” give up their quest from exhaustion, just to get on with life, and be comfortable with their peers?

Whether Prophetic Voice or Judas?

All movements have both personalities in their adherents. We all might cite leaders who took courageous stands or whom we believe compromised their duty to their followers.

That is what makes leadership so critical, and often controversial. It is also what makes public dialogue so vital.

We live in an era where there is continuing reinterpretation and debate after millennia about faith, whether Christian, Jewish, Muslim or just a value-centered life. While many believe that truth, when proclaimed, is universal; even some would challenge that assumption.

The one common approach that all faith and other “movements” followers have ultimately taken to succeed, is to pursue these issues in community. People aligned with one another agree to listen and learn together how their differing perspectives can arrive at common purpose or priority.

The Necessity of Community

Scott Galloway has put the power of relationships in a much broader context in his precent post Mammal.ai.

“Within and across species, relationships are essential to surviving and thriving. . .

“Humans have speedballed the power of relationships. Physically we are weak, slow, and fragile, with mediocre senses and absurdly long infancies. Yet, thanks to our superpower of cooperation, we’ve dominated our environment and become the apex of apex predators. There are more birds in captivity than birds in the wild. . .

“We are wired to seek and sustain relationships and cannot survive without them. The future of the human race won’t turn on space travel or climate tech, but on our ability to attach to others. A sense that we matter, that we can call on and be called upon by others to ease burdens and celebrate joy.”

It is not coincidence that the last moments of Maundy Thursday’s Biblical events were spent in community. Christians call it The Last Supper.

Music for Holy Week

Stabat Mater, by Antonio Vivaldi (1712). There have been many beautiful settings depicting the scene of the Mother of God standing in sorrow at the foot of the cross.

Oscar Abello is the senior economic writer for Next City. His focus is community initiatives that bring opportunities to those left behind by existing financial options. New credit union charters are an area of special interest.

The announcement of this new charter’s background has been reported by the credit union press. Abello’s story focuses on the difficulties of the process. Here are some of his observations:

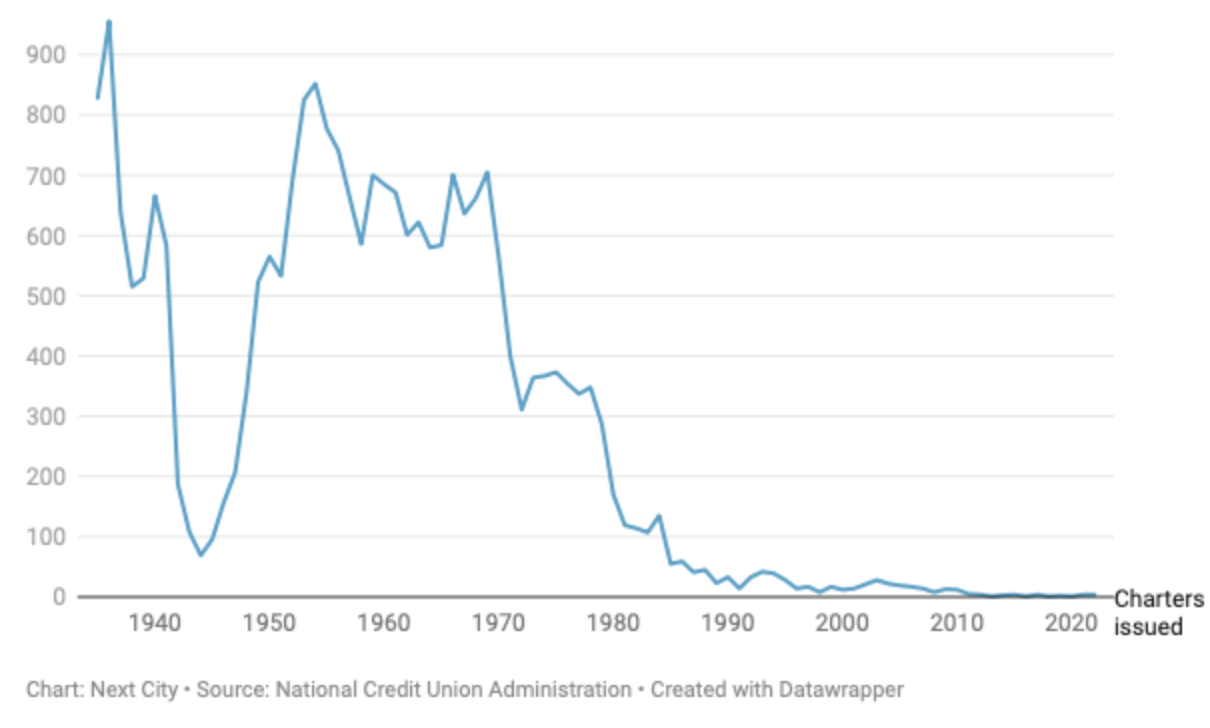

Chartering a new credit union today is like traversing a long-lost trail through the woods, one that used to be well-traveled but is now overgrown, littered with fallen trees and other obstacles no one has had to navigate in many years. Prior to 1970, there were 500 to 600 new credit unions chartered across the country every year. After a steep decline to near zero, the numbers have never recovered. Over the past 10 years, fewer than 30 new credit unions have been chartered across the country.

New Credit Union Charters

The annual number of new credit union charters issued nationwide by the federal government, as published in the annual reports from the NCUA.

According to Inclusiv, a network of credit unions that focus on community development, minority credit unions across the country are closing at the rate of one per week, making the new Arise Community Credit Union’s chartering even more urgent if that trend is to ever be reversed. (Editor’s note: all credit unions close at a rate of more than three per week). . .

Arise hopes to fill in the gap left behind by other more conventional banks and even other credit unions. Predatory lenders have jumped into the gap left behind by the retreat of the mainstream banking system from certain communities. African Americans are twice as likely to live within 2.5 miles of a payday lending storefront, compared with all Minnesotans. . .

Chartering a new credit union is a huge lift. It’s been nearly eight years of organizing for Arise, but it’s not uncommon for aspiring credit union organizers to take multiple years between initial conversations to raising startup capital to finally getting a new charter. The Association for Black Economic Power also had to deal with a leadership transition along the way — it’s now led by Debra Hurston. The new credit union has its own CEO, Daniel Johnson, who has deep family ties and professional ties to the Northside of Minneapolis.

It would have been easier — and quicker — for Hurston if her group just brought in an existing bank or credit union as a partner organization to provide access to credit and basic financial services to the Northside.

But Hurston says in surveys, town halls and just informal conversations over the years, the Northside’s desire for its own institution has only gotten stronger.

“The mistrust in the banking community, it’s not a small thing, and it can’t be fixed overnight,” Hurston told me last year. “We’re starting from the wrong spot…if I have to protest in front of you to make you treat me right. Something’s not right about that. So no one from our communities has ever asked me if we should just partner with a larger bank.”

Insight for Those Who Care

Abello’s reporting should be a boon to the credit union community. For as Robert Burns wrote of this ability to see what others may not:

O wad some Power the giftie gie us To see oursels as ithers see us! It wad frae mony a blunder free us, An’ foolish notion: What airs in dress an’ gait wad lea’e us, An’ ev’n devotion!

Music For Holy Week

Christ on the Mount of Olives, by Ludwig van Beethoven (1803)

The local Shakespeare Theater’s run of the story of Lehman Brothers family in America incorporates multiple themes. They are all very much present in America today. I believe they can inform the credit union story.

The play is an adaptation of a novel about the Lehman family. Three actors portray 55 different characters in the 163 years of the family’s timeline.

Although the firm’s $600 billion bankruptcy was the central drama of the 2008 financial crisis, the family had long been absent from any leadership roles when this occurred.

An Immigrant Story

The play is the story of a German Jewish family settling in Montgomery Alabama in 1844. After first opening a dry goods store, they expand to become “middle men” in the cotton trade between southern plantation growers and Northern textile mills.

They eventually open a New York office to enhance their trading activity and expand to other commodities post Civil War. These trades include wheat, coal, iron ore, that is the raw materials at the center of America’s industrial revolution.

As their trading activities expand they become a “bank” and underwrite the new industries being founded from railroads to computers and entertainment after WW II. Eventually these material commodities are supplanted by stock trading which brings the firm close to collapse in 1929. Outside owners will now control a majority of the firm.

Post WW II trading activity dominates its traditional investments in other industries. These traders buy out the firm’s presiding CEO, Pete Peterson, putting their priority on a strategy that eventually leads to the 2008 failure.

The story of growing economic wealth is interwoven with the family’s old world religious and family values. Jewish celebrations are initially central to life, but gradually become less so as succeeding generations assimilate into American culture. Their religious observance is “reformed.”

A Three Part Saga

Part family history, part portrayal of evolving moral values and part the story of how finance becomes central to American enterprise give the play multiple layers of meaning.

As I watched this century and a half saga, many parallels with the present day credit union story come to mind.

Credit unions have largely moved away from their focus on a local group or community to become a diversified mixture of legacy founders and new market expansions. The values and passion so critical for success in early years have been replaced by professional managers brought in for their expertise.

Growth becomes central to reporting success. Corporate wealth creation versus member well-being is celebrated. Instead of open governance, oversight is increasingly concentrated in a few hands where leaders perpetuate their tenures. Rather than paying their success forward to future generations, incumbents explore options to cash out when their term in leadership is ending by turning control over to other firms.

The Past Is Gone

The Lehman family gradually lost control of their “bank” when market circumstances required new capital. Evolving financial trends for their trading skills also changed the firm’s purpose. Middleman roles gradually evolved from buying and selling actual commodities, to underwriting new businesses and then merely trading pieces of paper, i.e. stocks. Ultimately finance became just digital transactions.

In this new world, everything becomes a number. And everything has a price. Finance becomes just a way to make money, versus investing in tomorrow’s economy.

Buying and selling (acquisitions) become critical skills. Member/customer trust is eroded because consumers no longer believe you will be there for them. Money management becomes the epicenter of success. All ties to previous values and economic roles are ended.

That in short is the story of Lehman Brothers creation. Is it an object lesson for credit unions?

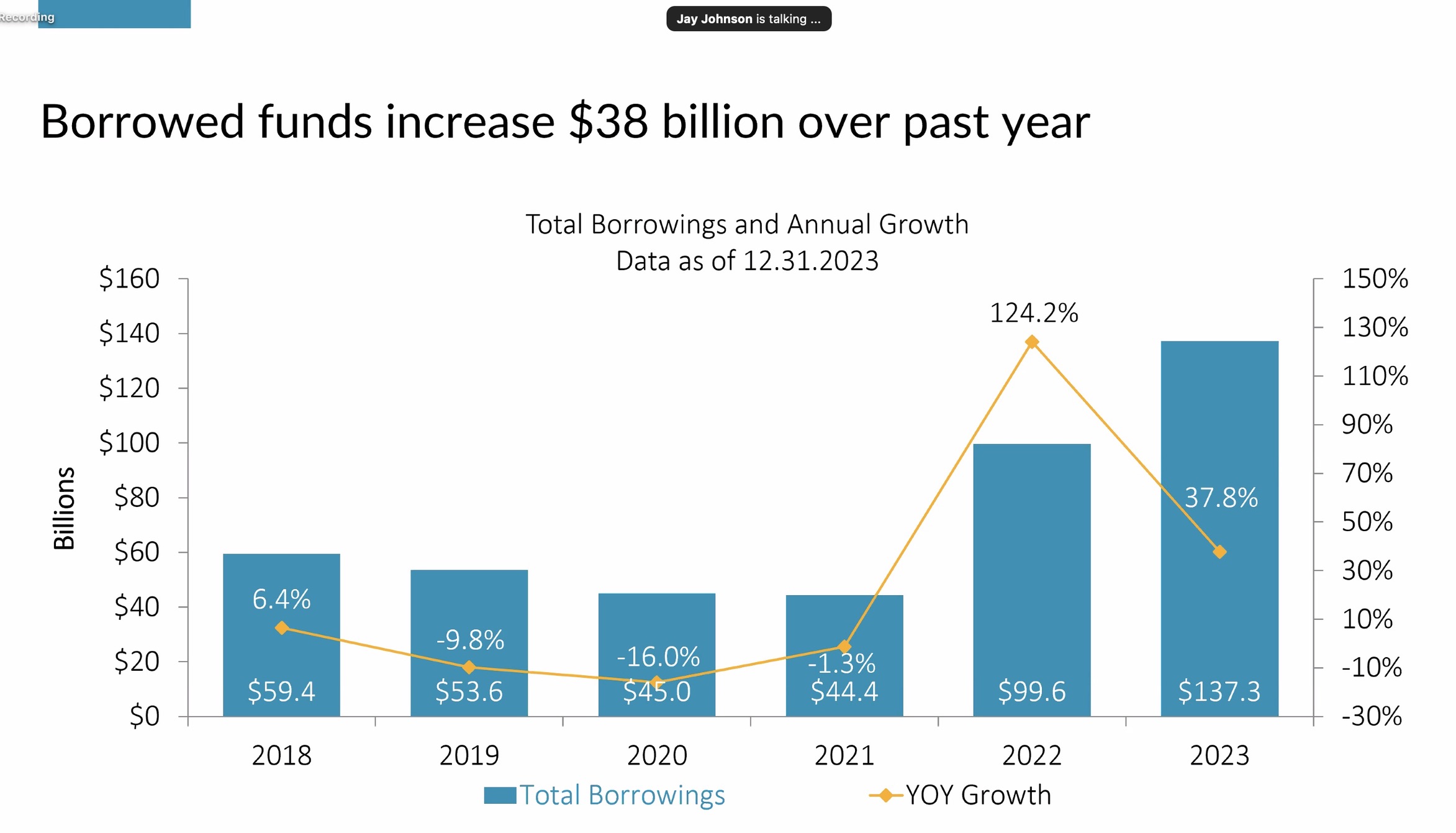

This month the Congressional Budget Office (CBO) released a 27-page report analyzing the Federal Home Loan Bank System.

The significant chapters include an Overview, Financial Condition, Subsidies and Risks.

The FHLB system is the largest lender to credit unions. Hundreds of credit unions have capital invested in individual banks and rely on them as critical partners for liquidity and ALM management. At 2023 credit union borrowings reached a peak in the system’s history:

The Central Liquidity Facility

How can the cooperatively owned, tax exempt FHLB, created to serve the savings and loan system, thrive with credit unions while their own funded CLF plays no role at all? Certainly, the borrowing demand is there.

At February 2024, the CLF reported $913 million in total assets, equity of $862 million and one loan for $1.0 million.

A 5% return on the fund’s retained earnings of $42 million would pay all CLF’s operating expenses. It’s 4th quarter 2023 dividend of 4.62% trailed the overnight market by .75%. Why aren’t members even receiving a market return on their shares?

More importantly, what can credit unions learn from the CBO’s analysis and the system’s response?

The CBO and FHLB Summary

Ryan Donovan, CEO of the Council of the Federal Home Loan Banks posted a reply #FHLBank to the CBO report: “it does a fair job of acknowledging the many things we have been saying.” He singled out a number of key success factors:

Private investors — not the government or taxpayers — bear the cost of any “subsidy” associated with the FHLBank system.

The FHLBank system plays a valuable role in providing liquidity to its members, particularly during times of market stress.

The benefits the system provides accrue not only to the members but to borrowers and the public. In fact, it says,

“Lower financing costs on FHLBs’ debt are passed along through lower rates on advances than members would receive when borrowing in private debt markets. In turn, competition leads members to offer lower rates to borrowers.”

“Because members are both owners and customers of FHLBs, almost all of the subsidy (after afford-able housing payments are deducted) probably passes through to them, either in the form of low-cost advances or, to a lesser extent, through dividends.”

The existence of the FHLBank system “reduces mortgage rates and provides liquidity to the housing market, particularly during period of financial stress.”

The FHLBank system poses very little risk to taxpayers. If one accepts the CBO’s figure of $600 million in federal tax exemption, the roughly $1 billion that the FHLBanks will distribute in affordable housing and community development grants this year seems like a very good investment for taxpayers.

Donovan concludes: The report stymies critics . . .because CBO makes clear FHLBanks pose little risk, they provide significant public benefit, the implicit guarantee is perceived by bond investors and the benefits of the system flow through to borrowers and communities.

The FHLBank system is poised to deliver $1 billion toward affordable housing and community development . . .We’re engaged every day with our members and other stakeholders on how those resources can be used most effectively. (end)

All these housing and community benefits should be possible with the CLF. Why isn’t this happening? What might a CBO report on the CLF say? Would anyone care?

Music for Holy Week

With each daily post I will be adding excerpts from some of the great classical music inspired by this Holy Week. Today’s is the “Resurrexit” from Berlioz Messe Solennelle.

Feb 8 (Reuters) – Bank of America has brought in $10.5 billion in deposits and investments in the last four years after making deals with companies to provide financial services to their employees, the lender said on Thursday.

On Immigration

In 2015, when the migrant and refugee influx from war-torn countries was considered of epic proportions in central Europe, one world leader stood out — German Chancellor Angela Merkel, a devout Lutheran.

During a public forum at the time, Chancellor Merkel was asked a question by a woman in the audience saying, What does that mean for us, what does that mean for our country and our identity? I’m afraid that it will mean more terrorist acts in our country by militants like ISIS.

Chancellor Merkel took a long breath before responding, and said, “Fear has never been a good advisor for us as individuals or for societies. Cultures and societies that are shaped by fear can’t grip the future.”

I recently became involved in a restoration project of a local church first built in 1829 and designated an historical site. One person’s observation on getting work approvals to preserve this property:

Once I started dealing with County personnel and permitting and approvals, I found out another truism that everyone has to remember, IF YOU ASK FOR APPROVAL in Montgomery County, usually there isn’t anyone that knows enough to answer and they will have to check.

No one wants their neck on the line and no one wants to give an approval without someone else from the county involved.

Postscript

I’ve done what is mine to do, now you do what is yours to do.

One of the extraordinary advantages of a credit union charter is the choice of either a state or federal license. This choice has been a critical aspect in credit union’s expanding role in the economy and responding to changing market conditions.

So when I recently received a letter from the CEO of Harvard University Employees Credit Union (HUECU) announcing a members’ special meeting to approve a conversion to a federal charter, I was very interested in why the change.

Was this a one-off situation or an indicator of an imbalance in charter choice in Massachusetts?

A Current Study

HUECU reported $1.2 billion in assets and loans of almost $1.1 billion, serving 55,000 members at December 2023. Most operating ratios are in a stable to strong range: Net worth 8.5% Delinquency .65%, ROA .28 and operating expenses of 2.74% of average assets.

The loan portfolio continues its healthy growth in three distinct components: an alumni credit card with $44 million in balances, a $252 million student loan portfolio and $721 million real estate loans.

The CEO’s cover letter included five pages summarizing the pros and cons for the action:

Advantages:

Reduces multiple credit union exam and compliance requirements;

Potential flexibility with various initiatives, especially branching and CUSO investments;

MSIC insurance for all deposits above $250,000 will be continued, but is no longer required;

Easier to open branches outside the state;

A redefined and broader field of membership with a multiple FCU common bond to seek growth outside Massachusetts:

No state sales tax, lower supervisory fees, and elimination of state CRA compliance.

Disadvantages:

The costs of conversion including signage, changes in legal documents, and consultant’s fees totaling as much as $600,000;

Loss of local regulator accessibility and responsiveness;

Limited ability to influence national regulation and issues;

State law offers greater interest rate loan flexibility and longer maturities on other loans.

The special meeting requires a quorum of 18 members and a majority of votes by ballot or in person in favor to approve the conversion.

The CEO’s cover letter states the members will see no operational differences after the conversion.

In addition to my membership in the credit union, the CEO Craig Leonard encouraged members to call in with questions. I was given his email, and we talked for an hour this past Monday.

He outlined three priorities which he hoped to accelerate with this step.

Faster growth, beyond the Harvard community into other New England states and perhaps Florida;

Immediately draw in more savings especially as loan demand has always been plentiful—with an initial focus on the small business market;

Retain the Harvard name (Harvard Federal Credit Union), its strong brand and the relationship of its employees to the University and its benefit plans.

Craig said this topic had been raised several times as he perceived a lack of a “level playing field between state and federal” charters in Massachusetts.

The state is home to approximately 135 credit unions that rank it as the 12th largest in total credit union assets. Of this total, 50 are state charters.

Both regulators have approved the credit union’s business plan forecast. It is now up to the members. Craig holds periodic town hall meetings with members because he believes “I work for you.” This Special meeting is March 26 at the Harvard Faculty Club.

While this may be a unique event, the balance and perceptions of charter advantages are an important metric on the soundness of the credit union system.

Whenever state or federal regulations become less responsive to their credit unions, charter change is a real option for many. It is one means of keeping regulatory accountability. It is also a spur to keep the multiple state regulatory systems, individually much smaller than NCUA. responsive to their local charters.

The State of Dual Chartering

The ability to convert from a state to a federal charter and vice versa remains a uniquely cooperative option.

In 2023 there were twelve charter conversions. Nine state credit unions (from seven different states) converted to FCU’s, two federal charters went to state and one state chose ASI insurance versus the NCSIF. The longest serving state charter was Mississippi’s Mutual Credit Union, founded in 1931. Two other Mississippi credit unions also converted to federal.

A choice of share insurance is also permitted in ten states which allow their charters to choose between ASI cooperative insurance or the NCUSIF. This option remains central to a real choice as well as validating the underlying the 1% deposit design of the NCUSIF.

Dual chartering option creates a check and balance, even positive competition, among regulators. It provides an opportunity for a credit union program as some states still do not have a charter option. However, the state system can often change more quickly to meet new market and member needs when response by NCUA may take years or in some situations, never happen.

The dual system is a critical aspect of credit union history. The first credit union charter was in 1909 for St. Mary’s Bank. Until the federal credit union act was passed in 1934, only state charters were available, and then limited to about two thirds of the states.

These state “startups” created multiple charter variations and operating authority. As there was no single example, charter details and oversight were sometimes drawn from already operating financial examples. For example, proxy voting is authorized by nine states, drawn from mutual S&L practice, but not an option for federal charters.

The Turning Point in Dual Chartering: The creation of the NCUSIF

The choice of either a fed or state charter from 1934 onward led to a 30-year period of rapid chartering across America. The states were often the laboratories for change, innovation and system leadership with local leagues and chapters forming potent political state-wide organizations. CUNA itself was an organization of state leagues, not individual credit unions.

The introduction of the NCUSIF in 1970 was led by a group of federal charters in the newly formed direct-member organization NAFCU in the late 1960’s. CUNA opposed this mandatory insurance requirement and supported multiple state-chartered alternatives to the federal program.

CUNA’s fundamental concern was that mandating federal insurance would inevitably create a single regulatory system for all charters. The diversity and choice created by dual chartering would be negated, if not lost all together.

The NCUSIF Override of State Options

This concern that the insurer could become a single regulator had a very quick example. Bob Bianchini, who was simultaneously President of the Rhode Island League and a member of the state legislature, encountered such an issue in the mid 1970’s.

NCUA refused to insure the NOW/checking accounts authorized for Rhode Island state charters. In response, the credit unions formed their own state chartered deposit insurance corporation. In Bob’s words:

The NCUA’s decision refusing to insure Rhode Island credit unions that offered checking account services to its members led to the creation of the private insurer RISDIC .. Seems to me there was never any specific law that would have led to that decision, but rather simply pandering to the commercial banking industry which claimed checking accounts fell strictly under their purview ..

RISDIC would have never gotten off the ground if Rhode Island credit unions that provided checking accounts to its members, could have obtained NCUA insurance.

The other RISDIC insured institutions were Loan & Investment companies. privately owned for profit financial institutions and it was one of those organization’s demise that led to RISDIC’s failure.

NCUA’s insurance power has led to other differences in regulatory interpretations. The insuring requirement has also been a major hurdle for groups seeking new charters.

Ultimately the major advantages of state charters continue to be their more accessible local regulatory oversight and the capacity to respond faster to changing market conditions.

The Final Word

The S&L crisis in the mid 1980’s resulted in that system’s failure of its state sponsored insurance options. It led some credit union leaders to back away from the credit unions’ insurance choice.

In a 1986 speech to the credit union league xecutives (ACULE), former NCUA Chair Ed Callahan, now CEO of Callahan and Associates spoke to the group. He described the importance of choice saying that “the insurer is the regulator.” His words are just as true today. Scroll down to the video.

Opening Day of the 2024 baseball season is eight days away. Players are being assigned to AAA from spring training or gaining limited roster spots on the major league varsity.

The sporting press is full of hope and enthusiasm. Every team’s ambitions are equal at this starting line. Accompanying these renewed expectations is the ever present realities of enormous player contracts, team moves to save money and whether multi-million dollar veterans will live up to their salaries and/or overcome temporary injury.

Baseball has become a game as much about money as competitive athletics. “Winners” are those with record contracts but not necessarily leading their teams to greater success.

However there is a counter story. It is about a player who stayed true to the game of baseball and his own values as told in the Imaginative Conservative:

The Baseball Hero Nobody Knows

By Stephen M. Klugewicz

His career stats indicate that he was a mediocre baseball pitcher—perhaps the epitome of mediocrity: 84 wins; 83 losses; a 4.49 Earned Run Average; a Walks-plus-Hits-to-Innings-Pitched ratio of 1.42.

Yet Gil Meche, who played for the Seattle Mariners and Kansas City Royals, was responsible for one of the most astounding, yet almost unnoticed, acts of virtue ever committed by a sports figure. In the winter of 2011, Mr. Meche, then with the Royals, voluntarily retired from the game, foregoing the final $12 million on his multi-year contract.

Mr. Meche was injured and would have sat out the 2012 season while receiving paychecks. “When I signed my contract, Mr. Meche explained, “my main goal was to earn it. Once I started to realize I wasn’t earning my money, I felt bad. I was making a crazy amount of money for not even pitching. Honestly, I didn’t feel like I deserved it.”

Mr. Meche’s decision is nearly unprecedented in professional sports; countless other injured players have gleefully accepted paychecks while they sat out entire seasons with injuries. “This isn’t about being a hero — that’s not even close to what it’s about,” Mr. Meche insisted. “Making that amount of money from a team that’s already given me over $40 million for my life and for my kids, it just wasn’t the right thing to do.”

Though a small event in the great arc of American history, Mr. Meche’s action would constitute an example of good character in any age, but it is especially noteworthy in the America of the early twenty-first century, an era of dishonesty, self-absorption, and greed. It should not go unnoticed, nor should it be forgotten.

Lost Virtues in Credit Unions

Today the opportunity to cash out one’s credit union tenure and leadership position is advertised in direct marketing appeals.

One headline reads:

1,200 Credit Union Mergers by 2030 –

How Are You Positioned?The YOU refers to the CEO ‘s who are being solicited. Either give up and join the merger-sales endgame and /or join in the bidding to secure another credit union’s resources. The need is urgent. Here’s why:

With regulations set to zap fee income, interest rates slowing mortgage action, compliance burden increasing costs and the need for scale driving strategic decisions. . . predictions say there may be as many as 1,200 credit union mergers by end of year 2030.

· Do your financials put your credit union in the position to be a merger or merge?

There is no pretense or subtlety here. Your future is full of threats, give up now and we’ll help you cash out. No mention of members’ best interests. No recognition that virtually every credit union operating today has a charter that has served at least three generations of members and created meaningful reserves of collective wealth and service legacy.

The bottom line in this strategic outlook is that prospective failure can become a CEO’s present success story. So get out while the getting is good!

Instead of character and values being triumphant, some coop leaders and their consultant allies are directing the industry into an America of the early twenty-first century, an era of dishonesty, self-absorption, and greed.

These actions dishonor the character of hundreds of Co-op “Gil Meches” who retire each year and loyally pass the credit union’s torch to their successors.

In following up an article by David Bauman in which he referenced his FOIA request to NCUA, I was directed to NCUA’s FOIA Library.

Under the Frequently Requested Information section was what I had asked for: NCUA’s response to Congressman French Hill on December 14, 2023. Other items in this section included previous multiple requests that can be accessed by just clicking on the link.

Another section of the Library was the FOIA Request Logs which include 474 requests going back to 2019. I scanned the requests that were open and closed for 2023 to see what information had been asked for.

The log table has the date of the request, sometimes the organization, a description of the information sought and final disposition: granted-partial or full, denied, or “no records” responsive to the request.

I have reached out to NCUA to ask if anyone can use the FOIA log number to review previous responses without having to submit a whole new request—just to learn about the agency’s response. When the reply is received, I will add to this blog.

In the meantime here are some of the more intriguing request descriptions, all of which were filled in whole or in part.

Selected Titles In the FOIA Library from 2023

Copies of all FOIA appeal logs by year from 2010

Records sufficient to identify all employees who entered into a position at the agency as a Political Appointee since January 20, 2021, to the date this records request is processed, to include a list of enumerated parameters to include resumes and waivers.

Documents and data sufficient to account for the monthly occupancy or vacancy rates for the agency’s five largest buildings (measured by square footage) from January 1, 2020, to December 31, 2022.

A list of federally insured credit unions with agricultural loan portfolios greater than $100 million.

The application, approval, and any attached materials from the most recent field of membership change by Thrivent Federal Credit Union, headquartered in Appleton, WI.

A copy of the charter for NBC (N.Y.) Employees Federal Credit Union, charter 22351, prior to its merger into XCEL Federal Credit Union, charter 16218.

A list of nationally insured credit unions that have failed and/or been acquired since January 2001 to include credit union name, charter number, opening date, failure date, and acquiring institution.

The most recent NCUA salary data.

1)The number of federal credit union mergers completed each year between 1980 to 2020; and 2) The number of active federal credit union charters each year from 1980 to 2020 (as of 12/31 or other uniform date for each year). Note: If information is not available going back to 1980, please provide information going back as far as NCUA records allow.

A list of all credit union CEOs and volunteers as of March 31, 2023.

NCUA salary data specifically under the category of political appointee.

Quarterly lists of all credit union board members for each quarter from Q42012 through Q42022.

1)Field of membership (“FOM”) criteria and approval documentation for FirefightersFirst Federal Credit Union (“Firefighters”); 2) Firefighters’ application and documents related to add “employees of non-profit foundations authorized by their organizing documents to be for the benefit and support of firefighters” (“Foundation”) to its FOM; 3) OGC’s legal opinion and analysis that supports the addition of the Foundation to Firefighters’ FOM; 4) CURE’s office summary that supports the addition of the Foundation to Firefighters’ FOM; 5) CURE’s approval letter and GENISIS worksheets reflecting approval of the Foundation to Firefighters’ FOM.

Entire consumer complaint file from 2013.

An Important Resource

This is a partial 2023 listing. In addition to some interesting reading, it also shows the agency as a resource for names of CEO’s and volunteers (including even CUNA and NAFCU) and for credit union data or other files going back years.

There might even be some valuable credit union press stories in following up some of these past requests.