A critical strategic advantage for most credit unions is location, a place members can see and access as necessary. A local office serves a different and broader role than just convenience. While telephone or virtual web access are necessary, they are not the same as a unique presence.

A credit union office serves notice to the community that the credit union is theirs. Members not only have interaction with employees but also with each other. Many credit unions use signage and participation in events to reinforce being part of the community. Local emloyeess and directors provide real time market knowledge that are impossible to acquire in other delivery channels.

Following are two examples of service experiences, one remote and one in person. Both involve a member trying to resolve an issue.

A Remote Service Experience

Even before I read your article on Credit Union 1, I have been preparing to leave for another credit union. The credit union has become just a computer Bot. Call member service and it takes 15 minutes to get around the automated phone responder “LUNA”. You can repeatedly ask for a member service rep but she always has another set of buttons for you to press. I’m not against automation and use it often to transact much of my personal business. But when you need to talk to a person that is not an option.

Recently the credit card company they use overcharged me. I called CU1. Immediately they put the transaction on hold and referred the problem to the Credit Card Bank. After filling out several reports to file with the card bank and months (June to October) of waiting for them to remove the charges I was notified that they were going to go ahead and put the charge on my credit card as they did originally.

Contacting CU1, they gave me instructions on how to deal with my credit card bank and the airlines to maybe solve the issue. We’re talking about $775 and no help from the credit union. And I do not like the card processor. More electronics and fewer personal assistance.

I know this sounds like someone from the past not being up to date with what is going on in the present; but really I make many of my daily transaction payments with my Apple watch; having connected voice over internet protocol for my home phone service; and many more. I do like the speed and direct processing that the new electronics offer, but it can’t replace a person for everything.

Remote Islands, Microsites and Personal Service

Tongass FCU, Ketchikan, AK serves Southeast Alaska with locations in a region of islands (the Alexander Archipelago) and the Tongass National Forest. No roads connect these islands!

At September 30, 2024, the credit union reported $228 million in assets from 13,710 members served by 13 branches and 85 employees.

CEO Helen Mickel has worked at this 61-year old credit union for 22 years. For the credit union the distance to the nearest branch often requires a small plane or ferry.

It has developed Community Microsties to meet the financial needs of remote coastal villages. Microsites are built upon a relationship between TFCU and the local community. The community invests in TFCU by opening accounts and providing a free space to operate, while TFCU provides an ATM, lobby hours, and local jobs.

The future: TFCU seeks to build community-microsites and branches to promote prospering communities. We believe that a financial institution is a pillar of a community. It brings education, opportunity and financial access to the remote villages and towns of our beautiful state.

Here is a story with pictures from Helen of what this sometimes requires in practice.

A Grumpy Member

It started with a very grumpy member threatening to close her account, to one of the best visits I’ve had with a member!💯

The mail is tricky in southeast Alaska and our statement vendor is in the lower 48.

This grumpy and worried member told me over the phone she was going to pull her money out on Monday because she still hadn’t received her monthly statement for August. I told her I’d like to meet her when she comes in and asked what time she would be at the credit union.

She said she heard the weather was going to turn and maybe she wouldn’t come down after all. She uses a cane and has 45 stairs to navigate when she leaves her home.

I offered to bring her a printed statement and introduce her to our assistant branch manager, Sabrina, so she wouldn’t have to leave her house. She liked that idea.😊

When I called to make sure she was okay with us stopping by, she said, “Yes! I’ve been waiting for you!”

The Member’s Museum

What a wonderful time we had! We worked out our business problem and then got a tour.

She had a “museum” of artifacts she had dug up on beaches and old community sites all over southeast Alaska! We talked about the good old days of early Ketchikan and shared stories.

I took pictures and told her I would be posting them and she was okay with that. She has lived in her home for 80 years – her whole life. It was the “cabin” for the first house that was built by her family on the side of a mountain.⛰️🌲

Pioneer members are some of my favorites. I love it when something difficult turns into a blessing for everyone! I couldn’t have started the week off better! ❤️

In addition to consumer inflation concerns as in the price of groceries, another economic topic on voters’ minds was affordable housing. High interest rates have brought the home purchase market to almost a standstill except for the well-to-do.

The average home price in the United States in 2024 is around $420,400, a 25% increase from 2020. Home prices vary widely by location. For example, the average home price in Iowa in 2024 is $205,988, while the average in Alabama is $217,75. Even with candidate Harris’ $25,000 down payment assistance for first time buyers, many would still see the aspiration as very difficult.

Today an update on the median home price for every state as of August 2024 was published by the Visual Capitalist website. The overall median (not average) for the US was $385,000.

Credit unions have been innovators in assisting members first home purchase efforts. These changes often go outside the standard secondary market underwriting requirements as many credit unions hold non conforming loans on their balance sheet. Product initiatives include low or sometimes no down payment, waiving transaction closing costs, and structuring variable rate loans with initial lower short term fixed rates followed by variable price reviews to ease the first years of payments.

This video is an example of how Community First (WI) structured their home lending to meet a family’s unique circumstances.

FHLB grants and other forms of community assistance are sometimes available. But given the continual rise in home prices even in the current slow markets, the prospect of a higher normal level interest rates, and the lack of affordable supply in many markets, is another approach required? Housing is also a market where technology would seem to have limited potential to change the cost side of the problem.

New approaches rethink the structure of home ownership by separating the cost of land from the house built on the property. Here are two examples of this approach. The descriptions are largely from the linked websites.

Neighborhood Housing Trusts

The first example is the Community Housing Trust (CHT) based in Ithaca, NY. CHT helps people with modest incomes buy their first homes. Since 2009, all of Ithaca Neighborhood Housing Service’s (INHS) home sales have been part of the Community Housing Trust. By using a special ownership structure, It is able to keep CHT homes affordable for the first buyer, and all future buyers as well.

INHS got its start by trying a new way to reverse the decline of downtown Ithaca: fixing homes up rather than tearing them down. In the 1960s and 1970s, Ithaca faced the problems challenging urban areas across the nation: a depressed economy, deteriorating housing, and the flight of homeowners to the suburbs.

Most of the homes in Ithaca’s downtown neighborhoods were more than 100 years old and owners could not get bank loans to buy new ones or didn’t have the skills or financial resources to make repairs.

In late 1976, inspired by an urban renewal program created in Pittsburgh which relied on a partnership between residents, businesses, and local government, Ithaca joined a network of successful Neighborhood Housing Services (NHS). Recognized by Congress in 1978 and known today as NeighborWorks® America, the national network of NHSs continues to recognize and nurture local solutions to local community development.

The Program’s Structure

The CHT is a “shared equity” program: the homebuyer purchases only the house and the Trust owns the land. The homeowner has a 99-year lease on the land, with a small monthly land rent. This arrangement greatly lowers the purchase price of the home. Because most CHT homes receive a special tax assessment, the property taxes can be much lower than a market rate house. INHS ensures that all CHT homes are built or renovated to be energy efficient and environmentally sustainable, another way that operating costs are kept low.

In exchange for these financial benefits, CHT homeowners agree to limit the amount of profit they can take from their homes when they are sold. CHT homes have a resale value that is capped at 2% increase per year. This allows the homeowner to build wealth in their properties, while ensuring that the home remains affordable for future owners.

The Funding

CHT homes cost on average more than $400,000 each to develop. The homes are sold for only about half that amount—between $150,000 and $210,000. INHS receives grant funds from a variety of sources to help fill the gap between development cost and selling price.

The permanent affordability of CHT homes means that the grant funds utilized to build them will benefit many lower-income households for generations to come!

The Durham Community Land Trustees

The timeline of this second example begins in 1987. The development of this North Carolina affordable housing initiative can be found here.This video, from 2017, shows a before and after look for one neighborhood built with members’ self-help.

How It Works

Similar to to Ithaca, a community land trust nonprofit organization retains land ownership, ensuring future housing affordability. Purchasers buy DCLT homes and lease the land these houses sit on for a low monthly fee for 99 years.

Owners can improve and maintain their homes.

They can leave their home to their children.

If a homeowner decides to sell, DCLT retains an option to repurchase the home to sell or rent to a future low-income resident or to assist the homeowner in identifying a new income-eligible purchaser.

The key feature: Homeowners share the equity they earn on their homes with future buyers, thus fostering long-term affordability even as surrounding neighborhood property values grow.

Credit Union’s Enhanced Role

Cooperatives are critical mortgage lenders in their local communities versus the nationwide all-comers model such as Rocket Mortgage. Many credit unions also sponsor foundations for local grants. Partnering with local housing agencies can facilitate oversight of land trusts or gain zoning support for both building and then managing the subsequent turnover with foundation land ownership.

Credit unions creative lending with on balance sheet solutions are a start to home ownership for some situations. But the broader challenge of affordability requires a collaborative effort that brings multiple resources and a different ownership design to the economics of single home ownership. A design that is partly cooperative but also combines with individual ownership responsibility.

If you are aware of credit unions participating in efforts to develop new ways of organizing home ownership and address affordability, I would welcome examples.

If one looks at the amounts of foreclosed property reported on the quarterly 5300 call reports, this suggests credit unions are already vested in home ownership turnarounds. Why not go the next step and create CUSO’s or other organizations that will restore neighborhoods and members’ ability to build financial well-being from home ownership?

November 5th’s outcome is not the end but just the next stage in our country’s political life. Regardless of the final party balance in Congress, for credit unions our work is cut out for us. We will find more ways to help members in need thus beginning to heal political divides in our communities and country.

While credit unions are rarely overtly partisan, their purpose is inherently political. The collective resources managed on our members’ behalf are intended to address member circumstances in ways for-profit market forces may overlook.

The role for the cooperative spirit has never been greater. Our mostly local focus is a critical advantage. Credit unions can again be leaders bringing light and hope to those who feel left out, or left behind, by economic events. Let’s get to work.

On the eve of the final voting in our quadrennial Presidential election, many feel anxious, nervous and even contentious.

Leaders, whether elected, appointed or rising to the top through performance, can be temped to sustain their positions by highlighting external threats.

Political contests especially bring out this tendency to identify internal or external “enemies” that should frighten us. These dangers might be foreign countries, economic uncertainties, governmental overreach, climate change, and sometimes even the character of one’s opponents. These risks become our “enemies” to be overcome and defeated.

Political campaigns are especially prone to this form of hyper rhetoric. Here are several observations, old and new, to help put this tendency in perspective. Because objectifying our worries may instead be revealing something about the inner voices we are paying attention to.

Do Enemies Make Us Whole?

Aspiring leaders efforts to persuade us to see external “enemies” has a purpose: to unite us behind someone or an entity which will protect our well-being and security.

However, what if these appeals just reflect internal confusions about shared values and purpose. Are these appeals more a reflection of an “enemy within,” an “uncertain soul,” as much as an external danger?

Decrying enemies is a common tactic to seek public support for a candidate or public action. The chorus lyrics of Andrew Bird’s Indie song Archipelago describes this as an attempt to “make us whole.”

Chorus

Whoa

We’re locked in a death grip and it’s taking its toll

When our enemies are what make us whole

Listen to me

No more excuses, no more apathy

This ain’t no archipelago, no remote atoll

Wisdom to Know the Difference

Leaders who p;oint out different social groups or “the other” in our midst to divide is a tactic as old as the country. It can be a short-term gambit to gain power. But It can damage future aspirations.

Here is a long-term perspective on the American democratic experiment by theologian Reinhold Niebuhr, a Reformed pastor, ethicist, commentator on politics and public affairs:

Nothing that is worth doing can be achieved in our lifetime; therefore, we must be saved by hope. Nothing which is true or beautiful or good makes complete sense in any immediate context of history; therefore, we must be saved by faith.

Nothing we do, however virtuous, can be accomplished alone; therefore, we are saved by love. No virtuous act is quite as virtuous from the standpoint of our friend or foe as it is from our standpoint. Therefore, we must be saved by the final form of love which is forgiveness.

Niebuhr’s most often quoted phrase or closing blessing is: Grant me the serenity to accept the things I cannot change, the courage to change the things I can, and the wisdom to know the difference.

Those words may be his challenge to us as we head to vote tomorrow.

No Man An Island

In most of life’s remembered moments, cooperation builds success, not domination whether personal or institutional.

All Souls Day (yesterday) is one of the times when a bell is rung as the names of those who have died are read aloud. This can occur in a religious service, reunion or other communal remembrance event. On these occasions the words of English poet John Donne are a reminder of our shared destiny:

For Whom the Bell Tolls by poet John Donne (1572-1631)

No man is an island, Entire of itself. Each is a piece of the continent, A part of the main. . .

Each man’s death diminishes me, For I am involved in mankind. Therefore, send not to know For whom the bell tolls, It tolls for thee.

Winners and Losers Will Need Shared Purpose

After the voting results are counted, the imperative will be to revive the common individual and institutional journeys on which we are all joined. America faces very real challenges. Overcoming our own internal feelings of deep uncertainty or dread may be the most important first step. Hope must win.

in this brief video from the Buffett’s 1996 Annual Shareholders meeting archive, he answers a question on what makes a good manager.

The questions for credit unions from his comments might be:

Are credit unions a “great business” or do they need “great managers” to succeed?

Does Buffett’s description of a good manager apply to credit union CEO’s?

What are the implications that the leaders of the Fortune 500 are not uniformly top quality and that there are a lot of mediocre ones, suggest about credit union CEO’s?

Here’s the brief video where he responds to the question of what good management is. You will need to click on the link and then again on the video.

Synopsis:This detailed analysis of Credit Union 1 (Illinois) presents a pattern of declining financial performance covered up by multiple merger acquisitions, one-time sale events and rented capital. The future fortunes of eleven local sound credit unions have been destroyed in just two years. I believe this kind of predatory activity, left unexamined by all those in positions of responsibility, will lead to a reassessment of the advantages of the credit union charter by external legislators.

The article’s length is to present as much of the facts from these events so readers can make their own assessments. The situation summarized is I believe an example of internal industry reckless actions which present a false perception of success. The question for readers is: Does something need to change?

When there are no guardrails for a financial institution, anything goes. It is the law of the jungle; or what some describe as free market capitalism.

The dictionary definition of rogue is “an elephant or other large wild animal driven away or living apart from the herd and having savage or destructivetendencies.” Another reference is to unprincipled behavior by a person or persons.

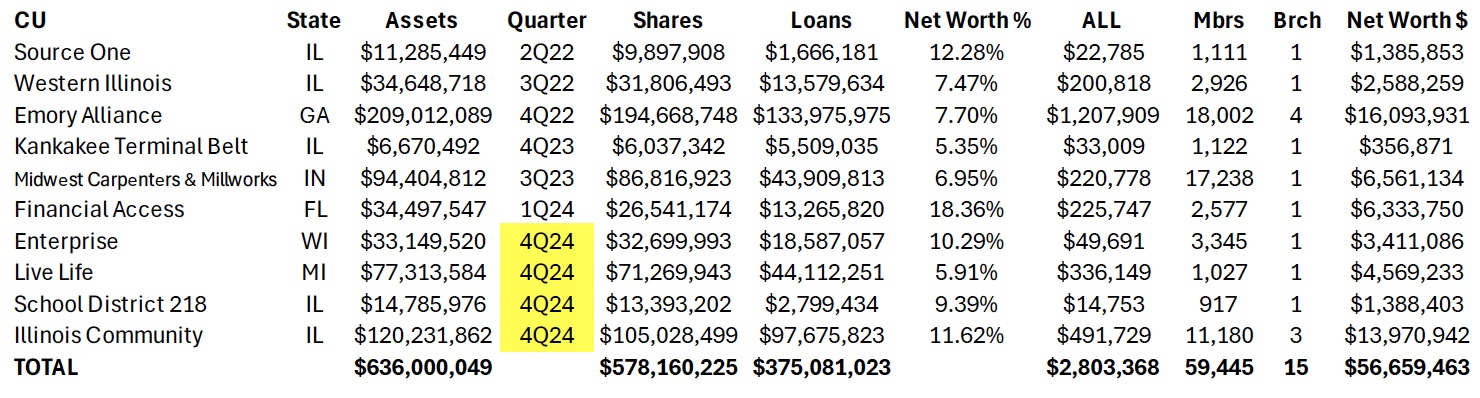

This word rogue came to mind as I reviewed the activities and results of Credit Union 1 in Lombard, Illinois, since its conversion from ASI share insurance to NCUSIF in February 2022. A summary of the credit union’s merger tempo since this insurer changeover is shown in the following table for the ten already completed or scheduled to be by the 4th quarter of 2024.

In addition, the $12 million Synergy Partners CU, Chicago announced on October 17 a members’ vote for January 2025 to merge with Credit Union 1. That would increase to 11 mergers in only two- and one-half years. These will transfer over $650 million in total assets and over 62,000 members’ financial futures to Credit Union 1’s control.

In its October 2024 Member Notice, Synergy listed 23 Credit Union 1 branch operations in six states including the head office in Lombard, Illinois. The two furthest branches are in Bradenton, FL (1,230 miles) and Henderson, NV (1,750 miles apart).

Other new or ongoing initiatives along with this accelerating merger expansion activity include:

The credit union’s continuing and new sponsorship and marketing promotions with four outside organizations:

The Western Conference tie-in: On October 3, 2024 the Big West Athletic conference announced Credit Union 1 had become its official financial and literacy partner and the entitlement partner for the Mountain West Basketball Championships and all Olympic Sports Championships.

On June 3, 2022 Credit Union 1 announced agreement to purchase the $311 million NorthSide Community Bank, located an hour north from Lombard in Gurnee, IL. Both boards approved the transaction subject to regulatory and bank shareholder approval. The deal was not completed. There was no public explanation.

In May 2023 Credit Union 1 announced it would serve New York cannabis entrepreneurs who plan to open marijuana businesses as part of the state’s CUARD coalition. The same CUTimes article reports, “Credit Union 1 has been selected to participate in the Illinois Department of Commerce’s Cannabis Social Equity Loan Program and is also the preferred banking partner of the Chamber of Cannabis in Las Vegas..”

Even with these multiple marketing and business initiatives, the core of Credit Union 1’s growth efforts are mergers. The operational intensity of acquiring and converting 11 credit unions (six outside Illinois) and all associated member and vendor relationships in just over two years would be a major operational challenge for any organization.

The immediate question is how will the members of the merged credit unions benefit?

In the Member Notices posted on NCUA’s website for these combinations, the wording used under Reasons for Merger, Net Worth and Share Adjustment or distribution are identical. Members’ collective reserves are never distributed to owners even when the merged ratio is higher than Credit Union 1’s.

But zero is not what several of the merging CEO’s and senior staff are gaining.

Rewards for the Enabling CEOs

In the case of the $34.4 million Enterprise CU in Brookfield, WI, the 24-year tenured CEO, Jeff Bashaw, will receive a minimum ten-year contract with a base salary increase of $38,000 on top of his current compensation. I estimated (absent the required 990 IRS filing) that to be a minimum of $125,000 per year plus a $100,000 bonus upon closing. Total minimum amount $$1,350,000.

The credit union is in sound shape at 10.6% net worth, a profitable, single branch with low delinquency. After turning over his CEO responsibility, Bashaw’s role if any will be a branch manager or other honorary title. This ten-year contract with a pay raise seems merely a lengthy sinecure. The 8 employees and 2,815 members receive nothing-except the retiring CFO who will receive a bonus and severance of $110,000.

A Minority Depository Institution Leader?

At the $34 million Financial Access FCU in Bradenton, FL, the situation is more complicated. The credit union prior to merging, reported a 1Q ’24 loss of $517, 310. However, its net worth was still high at 18.4% ($6.4 million) and delinquency of only .39%. Was this a temporary loss or other problem?

In this merger CEO Sherod Halliburton is receiving a total of $3.2 million composed of a bonus of $125,000, an eight-year employment contract at $200,000 per year, and 100% immediate vesting of a $1.5 million split life benefit plan. He no longer has any CEO responsibility as the credit union will become merely a branch operation. The 15 employees and 2,577 members of Financial Access received nothing for their loyalty.

In a CEO Profile published by Inclusiv in February 2022, prior the merger efforts, Halliburton is lauded for his leadership. The article remarks on “his strong community ties and business acumen and how he decided to “bet on me” when offered the CEO position” eight years earlier. Further he points out that he is “one of a limited number of African American men running a financial institution and he accepts the great responsibility accompanying that honor.”

The profile lists his efforts “toward racial equity and responsibility.” He states, “We’ve gone from a somewhat negative perception . . . to now being viewed as a vital part of the economic infrastructure.” The credit union received two technical assistance grants to upgrade technology to meet his goal to double membership in three years. He closes with this affirmation: “We’re here to change lives. I want that to be the enduring message even when I’m gone.”

This Bradenton community credit union which he described as “a vital part of the economic infrastructure” no longer exists. Halliburton is now a Market VP for Credit Union 1 for the next eight years.

An October 2024 Approved Merger

The most recent example of CEOs cashing in is the $116 million Illinois Community CU with over 11% net worth and delinquency of .5%. In this acquisition, CEO Thor Dolan will receive a minimum in immediate total benefits of $1,904,494.

This total is described in the Member Notice as follows: a retention bonus of $150,000; deferred compensation of $50,000; a salary increase of $33,724 added to his 2023 reported 990 compensation of $245,770 or $279,494 per year (no employment length given}; and immediate 100% vesting of a $1,425,000 split dollar 20-year life insurance benefit plan.

This salary increase is despite the fact he is no longer CEO, either managing branches or a regional rep, both with no CEO operating responsibilities. Every additional year he remains employed will add another $280,000 to the package. There is no indication the 38 employees (except the CEO and CFO) gain any assurances of employment; and the 10,482 members receive nothing.

The Fates of the Merged Employees and Members

Each Member merger Notice posted by NCUA which I reviewed includes two standard assertions:

The credit union’s branch location(s) will remain open and become a part of Credit Union 1’s nationwide branch locations.

Employee Representation: Employees of the credit union will be offered employment with Credit Union 1.

However intended, neither of these statements have proved lasting in practice. Comparing the branch listing in the August 2023 Kankakee Valley Notice with the latest listing in the Synergy’s October 2024 Notice, six of the branches in the earlier Notice no longer exist, including three for Emory CU in Georgia and three for Illinois credit unions with single branch operations.

As for employees’ fate, for the twelve months ending June 2024, Credit Union 1 reported a reduction of 67 FTE from 418 to 351.

As a result of Credit Union 1’s merger strategy, there will be eleven fewer local charters which were operating well, a reduction of 70-80 volunteer directors and member committees, and loss of all local relationships and legacy brands.

All member savings and loans, collective capital, liquidity and fixed assets are now in the full control of an institution for which the members have no connection or first-hand knowledge. And in some cases thousands of miles distant. Ironically, Credit Union 1 states in all its promotions that anyone can join, so if members really thought this was a better deal, they could join anytime. But that would be a much harder marketing task than just purchasing the business by paying the CEO—and getting the members’ accounts and accumulated reserves for free.

Members also have a totally new financial institution relationship to navigate. The Credit Uniion 1 material sent to each member post-voting is a 15 page pdf system conversion process and timeline. Member instructions include setting up new payment and loan options, establishing digital accounts and using online financial tools.

Depending on the version usent, the membership agreement for each merged credit union is a minimum and 20 pages. It contains essential information about fees, rates, funds availability, mandatory arbitration and multiple other disclosures which few will be able to read through. The members will learn through experience how everything has changed.

An important difference in Illinois state versus federal charters is the use of proxy voting in all member required elections, including mergers. For Illinois credit unions, proxies are controlled by the board. I did not see this fact disclosed in the FCU mergers, where proxies are not permitted. In essence, FCU members turn their voting governance power over to a new board. These directorst can routinely reappoint themselves without any member vote. More about this later.

Implementing a Capital Markets Strategy-Without the Risk

Credit Union 1’s merger campaign is an adaptation of a traditional capital market strategy of hedge funds and investment firms. Except these buyouts of numerous, smaller independent firms in an industry (think hospitals, barber shops, rental housing, or local HVAC firms) require putting their own capital at risk. These new hedge fund owners then burden their acquired firms with the debt used to finance the buyouts, strip and sell the highest value assets, reduce costs and services to pay for the debt coverage, and ultimately resell the merged business back to the market for a capital gain.

Credit unions reverse this model in mergers—they use the acquired assets, not their own members’ capital, to finance these acquisition sprees. Except when buying banks. The equity in these “mergers” is often transferred in full with no payout to the owner-members. The only necessary sales pitch required is to convince the CEO to bring the board along. There is zero risk to the continuing credit union. The “acquisition” is free. The members lose all their financial and institutional legacy and become subject to the control of a board and CEO that will be completely new to them.

We learn in the Notices that no staff or board due diligence or alternatives is presented. There is rhetoric about “technology and systems that align with members needs.” And, how “internal core values align with our own and . . . confident (that) members will experience a much needed upgrade in the quality of service.” No facts, just vague promises.

These same words were used in the eleven Notices showing the abdication of any director or CEO independent assessment. The words are merely a formula from previous transactions to pass regulatory approval. The members are given no objective measures or specifics that would identify better rates, fees or specific services. Just indefinite promises.

As for core values, institutions don’t have values, people do. So the acquirer’s goal is to find CEOs willing to cash out of their leadership role, rather than evaluate what is in the members’ best interest.

The Numbers Show the Urgency in Credit Union 1’s Merger Efforts

Some readers may believe this is just another example of self-dealing in mergers. It is. But there is a major financial imperative driving this effort.

Credit Union 1 is desperate for mergers not simply for growth, but because its financial performance is a house of cards. For the past five years it has been unable to generate a normal operating net income from its own balance sheet assets. As a result, it has turned to non-operating gains, acquired and borrowed capital (sub debt) and other financial options that disguise its very poor or sometimes non-existent internal rate of return. Here are some of the numbers.

At December 2021, Credit Union 1 had $106.8million net worth ($98.9 Undivided Earnings -UDE- and $8 m other reserves). The net worth ratio was 8.7%. Net income of $13.8 million that year was largely driven by a $7.5 million non-operating gain on sale of fixed assets.

At June 2024, the credit union reports just $88.6 million in undivided earnings, $8 million in other reserves for a total $96.6 million, that is $10 million lower than at December 2021 total.

To report an acceptable net worth ratio the credit union now includes $20.5 million in subordinated debt (borrowed capital), $45.1 million in equity acquired from credit union mergers, and a $7.1 CECL transition reserve. Without these non-operating additions to reserves, Credit Union 1’s net worth ratio would be only 5.8% versus the reported 10.2%.

But even the $88.6 million in UDE at June 2024 is misleading. At yearend 2020 the credit union reported $16.9 million in land and buildings. Three and a half years later, June 2024, the total is just $2.9 million. In the same period the credit union reported $15.1 million gains on sale of fixed assets. In the 18 months ending June 2024, the credit union also had non-operating gains on loan sales of $4.6 million.

It is not possible to determine how much of these sales are from Credit Union 1’s own assets or from the loans and fixed assets acquired via mergers. These sales amount to almost $20 million of the $88.6 reported UDE in June 2024. These are one-time events that are reported in net income thereby adding to retained earnings, but in fact are non-operating, one-off gains.

Safety and Soundness Questions

If these one-time gains are subtracted to show actual operating net worth generated from continuing operations, the net worth ratio from internal operations would be only 4.6%. Hence the credit union’s drive to raise external capital (sub debt) and acquire other credit unions’ reserves. Its dependence on external capital and one-time sales raises significant safety and soundness questions.

Internal operations are not generating sufficient capital to maintain required net worth minimums. For example, in the full year 2023, the credit union would have reported an operating loss of $429,000 except for the one-time gains on sale of fixed assets and loans. Through the first six months of 2024, the credit union’s ROA is only .39% or just .23% without extraordinary gains. (all data from NCUA tables)

The financial results are in even steeper decline than what is presented. If one considers the impact of adding merged shares and loans from the preceding four quarters prior to June 2024, there are critical balance sheet trends. These five mergers added approximately $210 million in loans and $346 million in shares to Credit Union 1’s balance sheet. Without these external gains, the credit union’s decline in outstanding loans for the 12 months ending June 2024 would have been $288 million or 24%. For shares, the falloff would be $73.3 million or a negative 5.5%, not the 4.6% increase reported. The credit union also relies on $35 million in external borrowings for funding.

Since converting to NCUSIF, the credit union has reported growth and acceptable ratios only through the acquisition and then sale of fixed assets and loans, and using the free transferred capital to maintain its required net worth.

What to Do About a Runaway Credit Union?

Once NCUSIF-insured in 2022, Credit Union 1 has been on a merger and marketing binge which is hiding serious financial performance shortcomings.

In all credit unions the Board, as a group, holds the direct, legal fiduciary responsibility for the performance of the credit union. The Board members approve all policies and hire the leadership. The buck stops with the Board members – all of them.

This is especially true in Illinois which has an unusual provision in the state act that allows the board to collect proxies from all its members, thus giving the board full decision-making authority in all areas, including mergers.

This is the reason for the extended proxy explanation in the Notices of Merger of the five Illinois chartered credit unions which reads in part:

Illinois permits voting on merger proposals only at the meeting or by proxy. If you do have a proxy. . . you may do nothing, and the board will vote in favor of the merger in your sted. . . If you have a proxy on file, to vote NO you must revoke that proxy by giving written notice to the board secretary. . . and then assign a new proxy to an attending member.

This is why all mergers of Illinois’ state-charters are reported as virtually unanimous. The process also puts a higher standard for due diligence and fiduciary responsibility on board members as they are now acting directly for the member.

There have been several recent class actions against credit unions around improperly disclosed overdraft fees and cyber breaches. When merged Credit Union 1 members confront the reality of losing their independent cooperative some may be deeply upset. With their board’s unilateral actions and failures to document their duties of care and loyalty, these transactions could become fertile ground for such actions.

Where Are the Regulators?

Except for the several federal charters merged, initial approval is by the state as Credit Union 1 is Illinois chartered. Most of the credit unions merged in MI, WI, GA, IN and IL are state chartered. All the data cited above is in public call reports and in multiple year analysis formats on NCUA’s website.

The trends for Credit Union 1 are clear, the extraordinary payments to CEOs presented in the Notices, the copy-book wording in the Notices all the same, and the vigorous public marketing communications easily reviewed for this nationally aspiring credit union.

NCUA routinely signs off on all mergers even those characterized by extraordinary self-dealing (eg. CEO contracts with change of control clauses), no clear business logic or member benefit, and Notices with misinformation, disinformation and missing critical facts for any member to make an informed vote on the issue.

There are indications that this hands-off response is the NCUA staff and board’s preferred laissez faire policy. The outcome is fewer credit unions by encouraging smaller credit unions to merge with larger ones driven by monetary payouts to achieve their policy of industry consolidation. But of course there are no asset limits as recent merger announcements have demonstrated.

The explanations for this dual chartering supervisory failure are wanting. In some instances, it may be a repeated failure by staff to do any elemental analysis. To my knowledge, there has never been a regulator “look back” to see if any of the merger commitments were followed up—even in a situation involving $12 million in members’ capital diverted to the merging CEO and Chair’s newly organized non-profit.

Regulators appear to lack a common sense understanding of events, not wanting to see or address the obvious conflicts of interest and board fiduciary failures. They thereby become part of the problem, abetting the worst aspects of cooperative leadership.

The result is no regulatory guidance or even backbone to stand up for members‘ interests or rights. There is no director-board check and balance on CEO’s ambitions or performance. And no regulatory effort to hold accountable those credit union CEOs who use their positions of power and institutional wealth to take advantage of the member-owners of acquired credit unions.

A System Circling the Political Drain?

Instead of expanding member economic opportunity, credit unions are imitating the tried and profitable capital market efforts to roll up their smaller locally focused brethren though payoffs and the rhetorical promises of better service through—even if only virtual.

Credit Union 1’s “purchased members” have lost the heritage and identity their cooperative predecessors passed on to them. Trust and loyalty earned over generations is gone. Members will vote with their feet when they learn there is no more advantage to being with Credit Union 1 versus dozens of other online financial offerings just as easily accessed.

Credit Union 1 has maintained its regulatory financial requirements only by acquiring other credit unions’ capital reserves, one-time sales of fixed assets and loans, closing local branches and letting employees go, and borrowing sub debt capital. These are efforts to buttress its balance sheet and cover its inability to earn an acceptable return on its own assets for its member-owners.

This practice will eventually be found out, the mergers will end. and the credit union’s safety and soundness will be much more closely scrutinized.

However, in the meantime, eleven local credit union charters are destroyed, their professional and community leadership roles ended, members’ long-time relationships to their credit union dissolved and the industry’s reputation put at political risk.

As Credit Union 1’s financial short comings become increasingly apparent, their external relations with Notre Dame athletics, the U of I Chicago campus, the new WCC partnership and Tinley Park Amphitheater will be in jeopardy. So too the industry’s public image.

I believe Credit Union 1’s actions are a threat to the future of the cooperative model. Every system has “bad actors.” That is why there are regulators. When directors fail in their fiduciary roles, and supervisors abdicate their appointed oversight responsibilities, the system’s integrity is at stake.

When other credit unions remain silent, state regulators default in their oversight, and NCUA appears unconcerned about the consequences of these events, it is only a matter of time until cooperatives forfeit their unique role in the American economy.

And should that day of reckoning come, thousands of credit unions trying to do the right thing will be end up in the same reduced status as their rogue colleagues.

In former AT&T CEO Anne Chow’s best-selling book, Lead Bigger, she describes how to inspire an actionable purpose statement. Chow is now a senior fellow and adjunct professor of executive education at Northwestern’s Kellogg Management School.

What purpose will sustain you and your people through a commute in bad weather, or after your baby kept you up half the night?

I’ve found it helpful to go beyond the focus on what you’re doing. Ask yourself and each other: Why? Why you? What makes your how the optimal choice and different from current or future competitors in the market?

No matter the size of your team or the work you’re doing, you’re on a mission to reach a destination. . .. If you’re still struggling to express what you do differently, ask yourself, What if we didn’t exist? Who would care? And why?

This chapter provides several examples from large firms such as Ikea, Nike and Apple along with advice to use words that ensure actionability.

A CEO’s One Minute “Lecture”

If you don’t have time to read the book or take a course at Kellogg, here are virtually the same ideas from a credit union CEO. Now retired, this leader’s brief explanation is noteworthy because of the results the credit union achieved during his tenure.

Moreover his statement predates the professor’s work by 15 years. An example of wisdom in action, not in hindsight.

What lesson does the oldest continually operating restaurant in Bethesda have for credit unions? Especially those who believe they need size and scale to succeed?

In 1935 in the middle of the Depression, the Tastee Diner began operations serving twenty-four hours a day. (Note: the Federal Credit Union Act was passed the year before) The diner would close only 42 hours a year from noon on Christmas eve until 6:00 AM the day after Christmas. However, it reduced its hours from 5:00 AM to 10:00 PM after reopening from the covid epidemic.

Its long narrow layout is just like the typical diner: wooden booths or single seats at the counter where you can watch as the cooks prepare your meal at the open grill.

The menu specializes in “comfort food” such as a full breakfast anytime. Daily specials are offered– spaghetti or fish on Fridays, meatloaf and mashed potatoes , with two sides; and every familiar sandwich option including grilled cheese and hot dogs. The menu has daily specials and senior selections at reduced prices. Its real milkshakes are served in the metal mixer can which contains at least two full soda glasses of my favorite food.

The owner sits on a counter stool opposite the cash register to welcome you. Sit anywhere. Waitresses welcome you back. You know their names. Montgomery County police on duty stop by for takeouts. High school students gather after football games. Families have birthday celebrations with young kids and floating balloons;. “Seniors” like my wife and I, go to have an outing in a familiar setting. The tunes on the jukebox at each table still cost just a quarter to hear Johnny Cash Walk the Line or other 1960’s Rock and Roll favorites.

A New Neighbor

In September 2022 a new neighbor opened its doors. Marriott International cut the ribbon on its new headquarters, a 21 story building built using all the vacant land around the diner.

Screenshot

The chairman of this Fortune 500 firm (ranking at # 173) is David Marriott. In the September 21, 2022 Washington Post article celebrating the opening, he presented the company’s history and how it chose DC as the base for this Utah raised family.

In short, David’s grandfather opened a root beer business in Washington after completing his two year Mormon mission assignment on the East Coast. Ice ooid root beer from his first stand was not in great demand in winter cold, so the business expanded to hot food such as the Teen Twist Ham Sandwiches, Mighty Mo Burgers. The business’ new name: Hot Shoppes.

Today, there are no Hot Shoppes. Marriott long ago diversified into the airline catering and then lodging businesses. Now it operates 8,100 hotels with brands from Aloft to the Ritz -Carlton.

The New Building’s Notch

But what does this international food and hospitality conglomerate have to do with Bethesda’s Tastee Diner?

In the 2022 interview with Chairman David Marriott the oldest, longest operating Bethesda restaurant came up this way:

The views are great from atop the glassy new headquarters, designed by the firm Glensler. David pointed out the Sugarloaf Mountain in the distance. We were standing near a notch in the Building. Twenty floors below was the reason for the notch: the Tastee Diner building ,whose owners had declined to sell.

“When my parents were away, the woman who watched used take me there” he said.

Not to Hot Shoppes? “She liked “Tastee Diner,” David said.

The Priceless Moral of the Story

Want to know how to counter the threat and buyout temptations of even the most aggressive credit unions?

Have loyal customers who seek your product, especially those who care for the children of the founder of a restaurant chain or even a credit union executive. Such loyalty is a variation of SECU’s mission statement: Send us your Moma! And also, keep local ownership of the business.

Following the Post story, the next time we went to Tastee I asked the owner sitting at the counter why he didn’t just sell out. He said he owned the land and they “wouldn’t offer me what I though it was worth.”

In the recent decade all of the chains and restaurants our family visited growing up have closed: Roy Rogers, McDonalds, Dominos and Pizza Hut plus other locally managed eateries. Today I know of no restaurant in Bethesda that has been in business for over ten years. Most new entrants create new concepts to appeal to a well to do clientele. These primary locations seem to change business brands about every 3-5 years. Their “newness” gets old fast.

Local matters, especially when you “own the land.” So the next time some glib acquisition broker or salesman comes calling to buy your credit union, just remember a child’s babysitter who brought the future leader of Marriott International to the Tastee Diner because “She liked the place.”

A loyalty so special that the “child” recalls the experience four decades later. Local loyalty is priceless.