On Tuesday Oct 1, remote virtual voting for SECU’s (NC) 2.8 million members’ annual director’s election will end. Mail ballots must be postmarked by then, but in-person votes can still be cast at the Annual Meeting on October 8th in Greensboro.

I summarized several issues between the two slates of four candidates a week ago. For I believe the significance of this unique event extends far beyond SECU’s members, North Carolina and into the entire credit union system.

Member-owner voting on anything, except a credit union’s demise via merger, is extraordinarily rare. This example of the member franchise being conducted demonstrates that elections in large credit unions are feasible.

Members now have a say via voting about the credit union’s future. It challenges the current routine practice of self-perpetuating board oversight with no member-owner input. This latter approach is, unfortunately, the process followed by most credit union at the moment.

Campaign Updates

Facebook posts with social media ads are being run by both sides. The four member nominated SECUforALL site includes dozens upon dozens of member comments and videos. It is updated daily. For example, it now includes “links to local news outlets providing lists of trusted charities and relief organization accepting donations” for North Carolina victims of hurricane Helene.

These members and many former employees have criticized the announced annual meeting rules which limit member participation and comments compared with prior practice. Their posts also pointed out that the credit union is paying for the incumbents slate’s ads on social media.

I believe both sides would agree with Chairman Moon’s video election comment that “The power of your vote cannot be overstated. Let your voice be heard.” That’s why this election is about more than choosing between two slates of candidates. It illustrates what the member-owners’ role in a credit union is supposed to be.

Two Contrasting Views of Credit Union Leadership

Cooperative design inverts the traditional structure of financial services leadership. In long-established and certainly modern day financial firms, power is concentrated, either in the hands of those at the top or those who contribute the most capital (ownership stake).

In credit unions power flows up from the bottom, from the member-owners. This was the intent of the democratic one-person-one vote election for directors at the required annual meeting.

This grass roots, member-driven founding became so successful, credit unions began hiring full time managers. Growth and expansion accelerated after deregulation. Successive leaders grew increasingly distant from their credit union’s founding generations and motivations.

This ever widening scope of operations separated management and boards from routine interaction with members. Today’s leadership teams who benefit from the legacy of hundreds of millions in assets, believe it is now their sole prerogative to configure the organization apart from any prior commitments—even to the point of merger and charter dissolution.

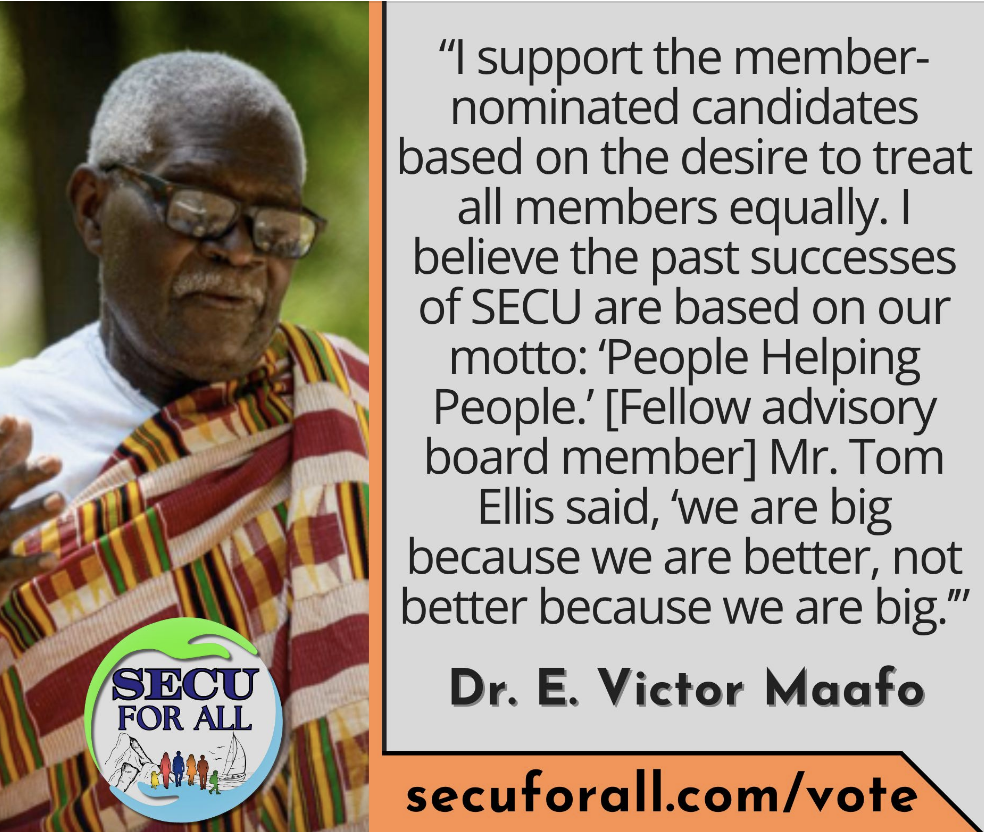

The boards of large credit unions have become insulated, like a private group who amplify and reinforce the instincts of this self-selected few. It is their authority to alone shape the future. The unique coop design is now turned upside down mirroring the current structure of for-profit financial organizations. Here is a comment from another credit union’s member on the SECUforAll site:

Recasting the Coop Model

Credit unions were created to break from the traditional way financial services were practiced: for example, paying interest on share draft accounts; offering skip-a-pay and loan rebates; permitting cosigners as “collateral” for loan limits. Or to use the biblical phrase, “overturning the tables of the money changers” providing consumer financial options.

As credit union’s market ambitions grew, the prevailing ethos became “to beat the competition, a credit had to become the competition.” And their leadership and advice was increasingly drawn from that perspective, not from the legacy culture that built the system’s present financial standing.

SECU’s Election and the Stakeholders Watching

SECU’s election choice is between two visions of what a credit union is. Most large credit union leaders believe the power of the organization rests at the top. Success entails unfettered growth, seeking mergers and/or buying assets such as banks, and using all the tools of financial leverage such as subordinated debt, third party originations and borrowing, should shares fall short.

However, credit unions were founded on the principle that power was created by empowering others. Credit union pioneers believed the wealth of an organization was measured by how much it was shared, not how much the firm accumulated. That the strength of a coop was in trusted relationships, not superior financial ratios. Member service and values is how to attract committed employees. not bonuses.

The outcome of this year’s vote will likely resonate far beyond Greensboro and North Carolina. If ten thousand, a hundred thousand or even more members see their democratic ownership role more clearly, every SECU meeting going forward will have a more engaged participation. And the credit union system will have an example of what modern day cooperative governance can be.

I will publish the link to the October 8 SECU Annual Meeting when it is available.

“That the strength of a coop was in trusted relationships, not superior financial ratios.”

Tell that to the NCUA. Examiners love nothing more than to tell you how to run your organization.