Recently I asked a person who has worked with credit unions in the past four decades, what she would like to see in the next NCUA Chair.

Her response: “Someone who cares about us.”

That simple statement felt profound. I circled back to ask how she might know if someone met this criteria.

In her words, the person would not be an outsider. Rather someone who has worked in or with credit unions. An example she cited are those CEO’s today who began their careers as tellers or branch managers to become leading CEO’s. They know the operations and culture that create success from the ground up.

Communications

This person, she said, would reach out and talk with, and more importantly listen to, credit unions.

Credit unions would be included as regulatory policy and priorities are developed. Communication would be ongoing and open. The industry would not be preached to. Rather the system’s success would be celebrated especially with examples that make members’ lives better.

Mutual respect would characterize interactions. The Chair would recognize that not all credit unions perform at the same level. For that is how life works. The multiple legacies of personal time, cooperative resources and member loyalties that are the foundation of today’s cooperative system would be recognized.

What to Avoid

I believe most would agree with these characteristics. But her concern was if the Chair was “an outsider with an agenda.” That can lead to a tendency is to see credit unions as an “enemy” especially when in difficulty, rather than being part of a common cause.

This person reflected “how can you regulate if you keep credit unions at arm’s length?” Or if the appointee has never managed an organization, how can they be expected to do something they have never done before? Put simply, how can you regulate something you know nothing about?”

A Public Conversation on NCUA Leadership Now

The most consequential action by the incoming administration on credit unions will be the appointment of the next NCUA Chair. Hauptman’s term ends in August 2025.

It is easy to speculate how the broader Trump agenda might impact NCUA. There could be spillover from these efforts. However, the opportunity now is to articulate the factors that would characterize a successful NCUA leadership selection. One that would move the cooperative system forward in its special role addressing the needs of members and local communities.

This dialogue should include identifying potential candidates whose backgrounds suggest both experience and competence in leading an organization that has made a difference during their tenure.

Now is the time for those who believe in the cooperative model, to speak up and ask their affiliated organizations to do likewise. Bring forth names of persons who would bring insight and demonstrated competence to the Chair’s role.

For if credit unions and their affiliated organizations fail to express their views, how can the incoming administration see this appointment as anything other than a job for a loyalist?

If credit unions demonstrate their strong interest in this role, that enhances the chances of a meaningful choice for the next four years. And a more productive relationship between NCUA and all its constituents.

Pending member approval, the 51, 590 members of $805 million Thrivent FCU will receive all their credit union’s reserves plus a dividend upon merging. The bonus will approximate a 12.2% additional return on the members’ $628 million total savings as of June 28, 2024. The total payments will be $76 million.

An example: if a member had $5,000 in total deposits on June 28, 2024, their estimated payout would be $610. Plus they have full access to their savings if they do not wish to keep them with the merger partner, Thrivent Bank.

The payout is an important precedent. For in the current system member-owners receive nothing in ownership acquisitions except rhetoric and future promises.

More vital, could this example encourage more banks to seek acquisitions by offering members a fair deal-a missing factor in today’s intra-industry private cooperative merger games?

Thrivent Bank, is a newly state-chartered Utah based FDIC insured institution. It is indirectly wholly owned by Thrivent, a Fortune 500 company with over $114,000,000,000 in total assets at the end of 2023.

The Valuation-What is a Successful Credit Union’s Actual Market Value?

From the member Notice: A valuation performed by RP Financial, LC in 2021 established the merger value of TFCU to be $76,000,000. The TFCU Board of Directors has determined that in conjunction with the Merger, the members will receive a total distribution in the amount equal to the full valuation of $76,000,000.

At June 2021, the credit union reported a book value (net worth) of $69 million. So members are receiving more than the book value at this valuation date. At September 2024, the net worth had declined to $59 million which included the potential write down (FASB 115 valuation) of $21 million in underwater investments.

This is a fundamental data point that every credit union member-owner should be given in a transaction. Today members are never told the market value of their credit union and the potential for a premium. This has created a false market when a merger transfers operational control to an independent party and the owners receive nothing. Such a valuation should be part of all merger proposal going forward.

Who is Thrivent CU?

Chartered in 2012 the credit union’s mission is to help people achieve financial clarity by providing access to banking products and services that help bring balance to spending, purpose to saving, and intention to managing debt. We strive to put you at the center of everything we do, providing impeccable service and competitive rates, so you can make financial choices aligned with your values and priorities.

Why the Merger with Thrivent Bank?

The following is from the FAQ’s for the merger:

Just as TCU is different from other banks and credit unions, Thrivent intends that the Bank will continue our shared mission of helping people achieve financial clarity so they can live full and purposeful lives. It intends to build a simple and transparent full-service product suite, create easy-to-access digital experiences, and provide direct access to human support, with competitive rates.

Thrivent believes that a purpose-driven bank is differentiated in part by fewer, simpler and more transparent products. This will be manifested in simple, fair, and transparent fee structures, and experienced through behavior-influencing digital experiences that offer contextual and actionable insights and guidance that help customers advance on their path to better financial clarity and wellness.

Post merger: All current accounts will retain their rates, function and features. And, the rates and substantive terms of members’ existing loans and savings products will not change as a result of the Merger

Any Special Payments for Staff?

In many credit union acquisitions of other credit unions, the primary payouts are to the CEO’s and senior executives who set up the merger. The same disclosure is required for this transaction. Here are the details:

Merger-Related Financial Arrangements:

No senior executive officers of TFCU will receive an increase in salary as a result of the Merger.

On October 1, 2021, the TFCU Board of Directors voted to retain current board member Ronald S. Orrick, Sr. as the interim President and Chief Executive Officer of TFCU. A portion of Mr. Orrick’s compensation for his services as interim President and Chief Executive Officer, in the amount of $50,000, is conditional on TFCU successfully merging with and into Thrivent Bank.

There are no change in compensation for staff. The second fact in this disclosure is that this transaction has been underway for over three years.

The Voting Process

The proposal must receive votes from 20% of the total members eligible to vote (47,872). At the time we reach the threshold, regardless if members are voting For or Against the recommended merger, TCU will donate $20,000 to a charitable organization.

Of the votes received, a majority must vote in favor of the merger for the vote to pass.

Online voting will begin on January 7, 2025 through February 5, 2025. A mail ballot will be sent to all members that have not selected electronic communication.

Why the Merger if Nothing is Changing

A video explaining the merger and links to the member letter, official meeting Notice and FAQ’s can be found here.

There are two themes as to why this change is sought, even though the member experience may not be different in the short run.

The dominant motive is access to greater capital: TFCU has a fraction of the capital that Thrivent Bank will enjoy. Thrivent Bank’s capital together with the existing assets of TFCU will permit Thrivent Bank to make investments in improved technology, products, and services.

The second aspect is broader growth potential: As we look to the future, we’ve recognized the need and opportunity to grow and further our mission to serve more people with our differentiated approach to banking

The expected merger outcome: Thrivent Bank will offer a simple and transparent full-service banking product suite, delivered through easy-to-access digital experiences and direct access to human support, with competitive rates and fees. Ultimately, Thrivent Bank will help people achieve financial clarity, enabling lives full of meaning and gratitude.

What This Example Could Mean for the Cooperative system

In addition to a process that reveals the market value of a credit union in an acquisition, there is potentially a more consequential outcome.

It is this: If credit unions can buy banks an increasingly common growth strategy, why can’t a bank with a mission, purpose and abundant capital take Thrivent’s model to other credit unions around the country. This would open up true market options that are now not sought out in today’s rigged merger transactions. The members then have a real choice. They can receive full value for their loyalty, choose to stay with the acquirer or take their relationships elsewhere if not pleased.

Today credit unions are readily paying 1.5X to 2.0X book value to acquire a bank. But member-owners are rarely offered anything in such mergers for their ownership and years of loyalty.

Credit union professionals have been taking advantage of members in the current merger-driven, CEO’s private deal making process. It’s time real market options are required for the members’ benefit. Thrivent FCU’s disclosures and payments should be an example required in all future coop acquisitions. Then members can hope to receive a fair deal.

My earlier analysis, part 1, of the NCUSIF’s financial performance in 2024’s first three quarters, highlighted the fund’s soundness. It concluded with Board member Otsuka’s statement about the board’s role to be good “stewards” of the fund. This post shows how that oversight role could be improved.

The Benefit of Public Board Meetings

The board’s quarterly discussion of the fund’s performance is an important responsibility. It demonstrates each board member’s “grasp” of the subject matter, their preparation and their reasoning for any conclusions. Just like a credit union board’s role, their judgment is critical in overseeing staff’s recommendation.

It is in the board’s particular roles in this quarterly review, that the public learns each member’s understanding of general policy, especially the role of America’s cooperative financial alternative.

Additionally, NCUA’s monthly publication of the NCUSIF’s performance provides the fund’s cooperative owners the opportunity to monitor how their 1% deposits are managed by following critical financial indicators. This monthly update was a condition for the open-ended funding model of the 1% deposit by credit unions. If the trends are in the wrong direction, then credit unions have the facts to speak up.

Critical NCUSIF Financial Issues

The fund’s finances have one primary revenue driver, the yield on the investment portfolio. This was by design. It was a dramatic change from the premium based approach of the FSLIC and the FDIC which was also followed for the first 15 years of the NCUSIF’s operations. That premium model proved fundamentally flawed. That history is described at the end of this post.

The NCUSIF’s Investment Underperformance

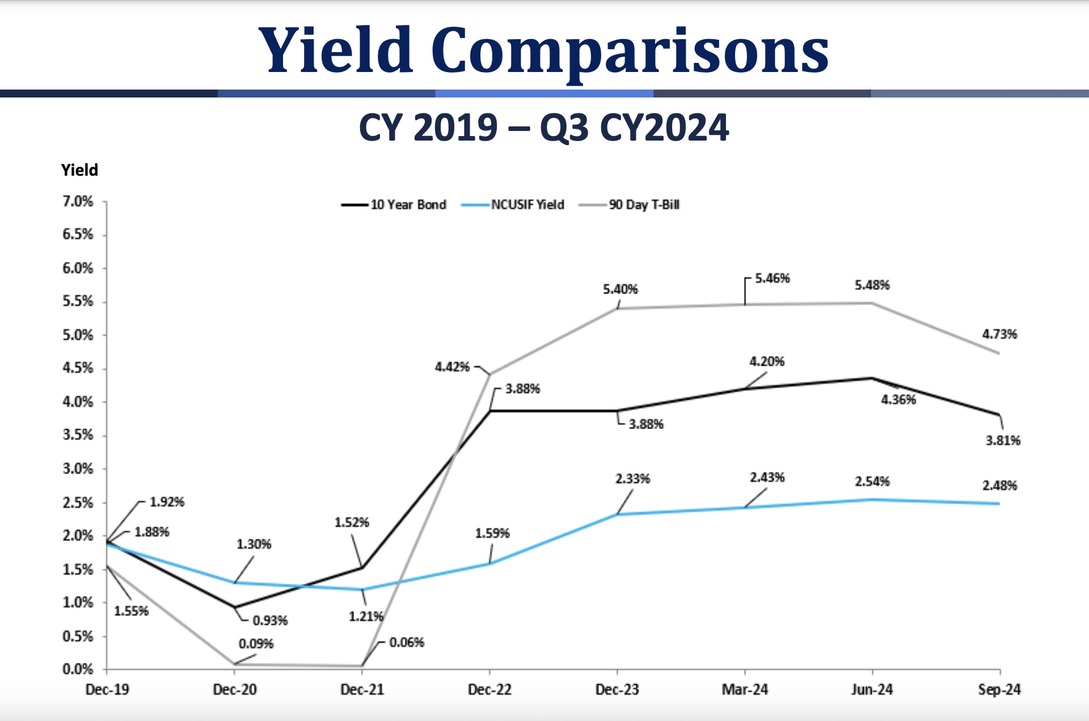

Slides from the September financials in November meeting clearly demonstrates the agency’s continuing shortcomings in managing the Fund’s interest rate risk.

The first tracks how the fund’s yield (blue line) began trailing its market indicators as of mid-2021.

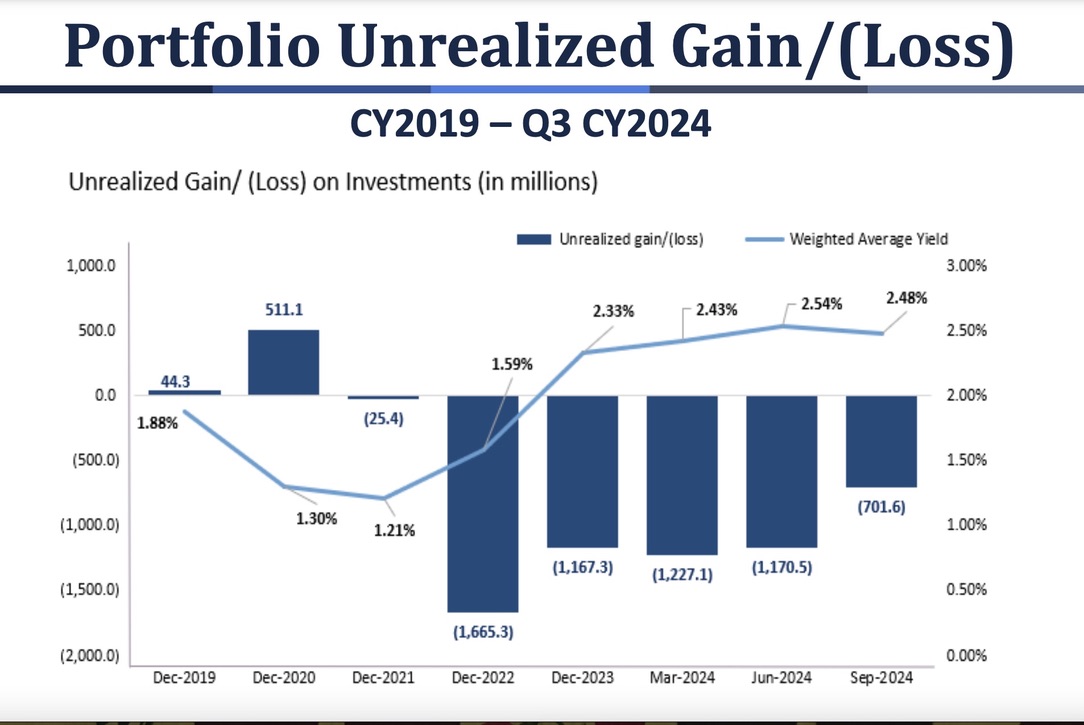

The next shows that the NCUSIF portfolio has been “underwater,” that is below market in value and return, since December 2021.

The first consequence of this portfolio strategy is that the fund’s primary revenue source is shortchanging the fund and credit unions. The second is that the majority of the fund’s investments are not readily liquid in the event needed without either borrowing or selling investments at a loss.

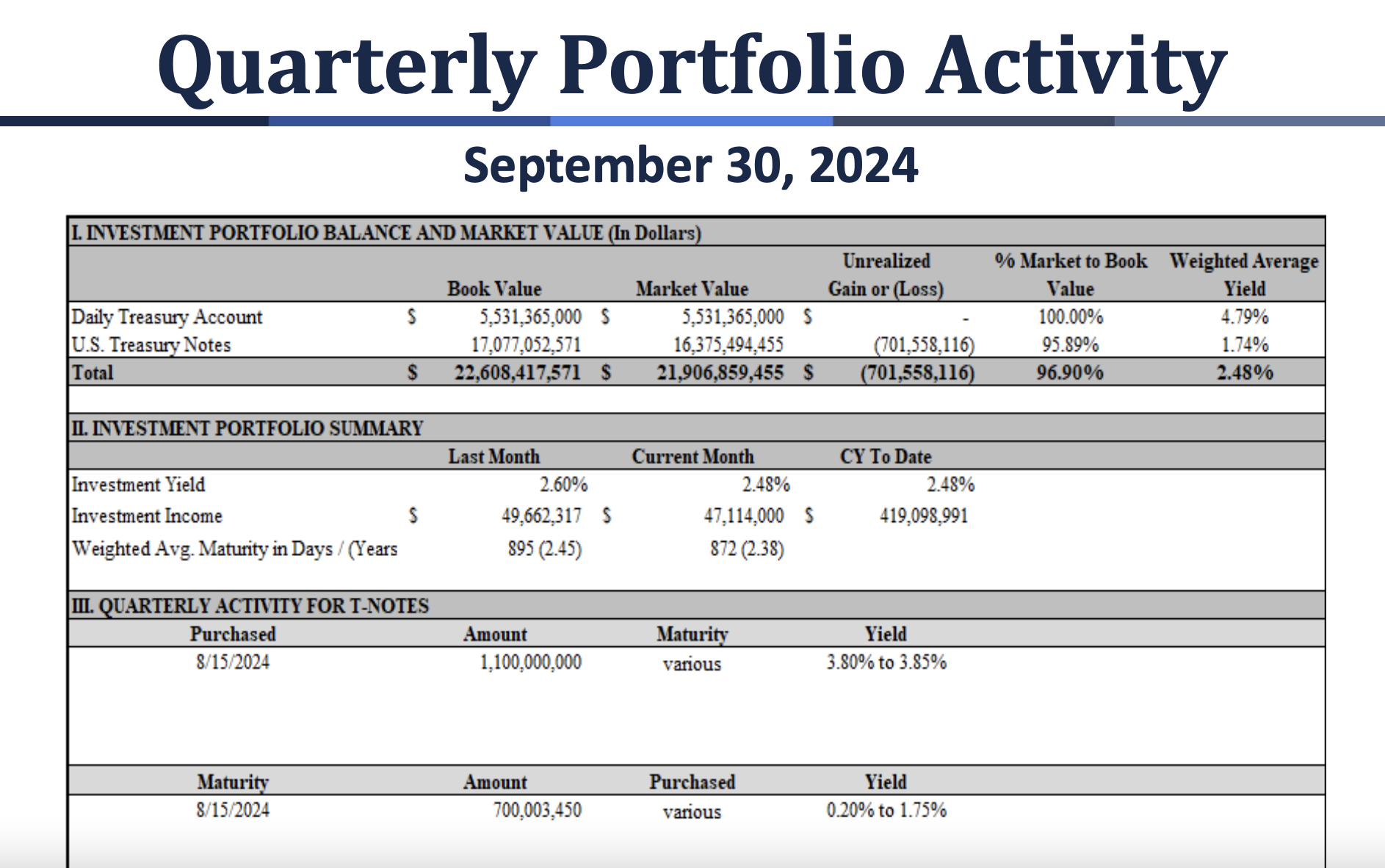

Below is the latest investment report provided to the board in the quarterly review.

It shows an overnight yield of 4.79% on 24% of the portfolio; 1.74% on the remaining 76%; and a weighted average YTD yield of only 2.48%. This below market return is due to the fixed rate bonds purchased following a robotic investment ladder out to over seven years independent of any ongoing IRR assessments.

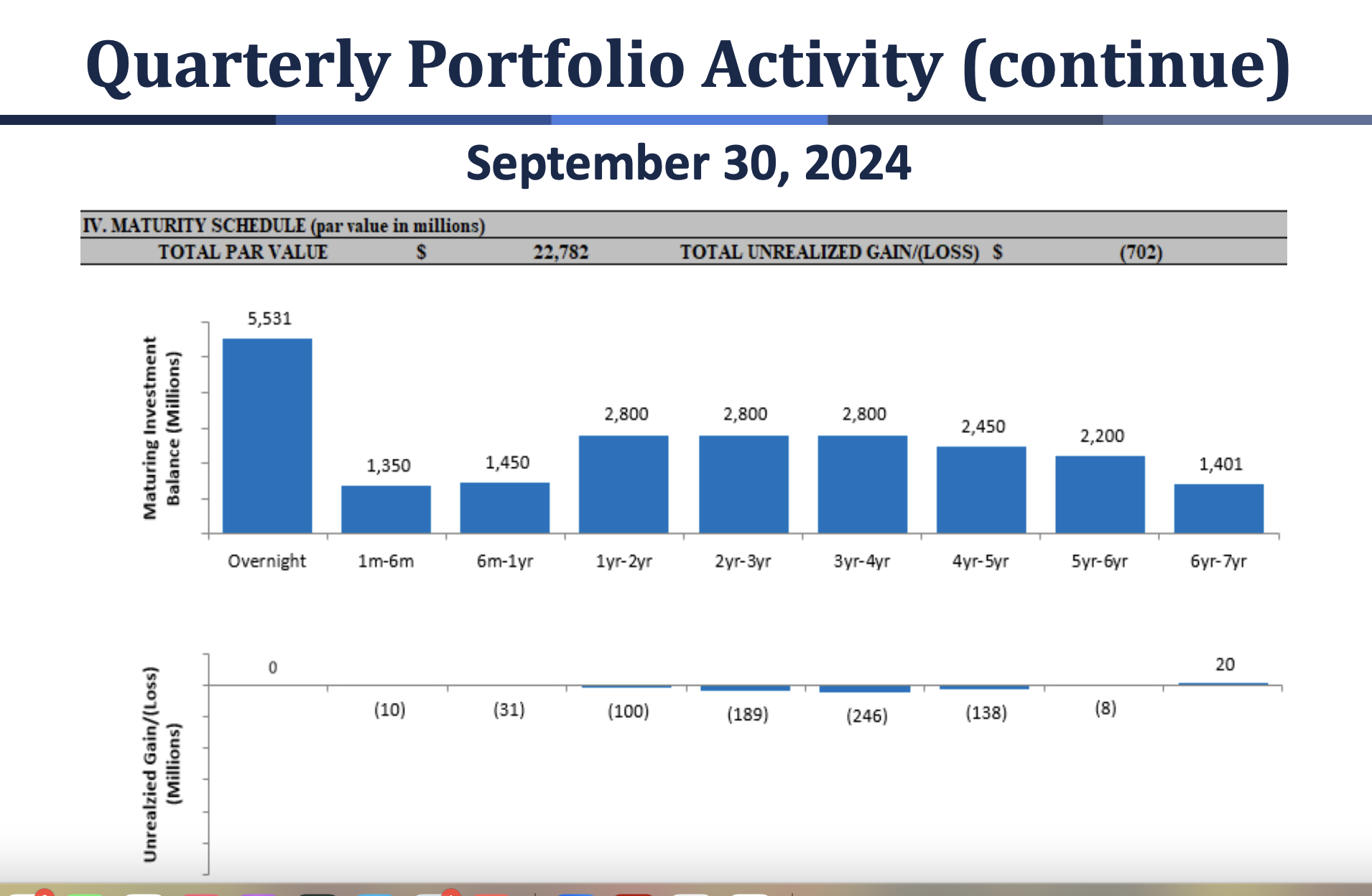

At September 2024, every investment maturity bucket except overnights, and recent investments for seven years, are below market value.

This update shows one investment action during the third quarter: $1.1 billion of bonds purchased on August 15, 2024 at “various” yields of 3.5% to 3.85%. Following are the other yield-investment options that same day from the Department of the Treasury.

Date

8/15/2024

1 Mo

5.53

2 Mo

5.4

3 Mo

5.34

4 Mo

5.22

6 Mo

5.04

1 Yr

4.52

2 Yr

4.08

3 Yr

3.9

5 Yr

3.79

7 Yr

3.83

10 Yr

3.92

20 Yr

4.28

30 Yr

4.18

This August investment decision yields less than all other Treasury options with maturities less than three years-shown in blue. It extends the interest rate risk as measured by the fund’s weighted average life (WAL). It follows the same pattern of activity that resulted in the fund’s past three plus years of underperformance.

With the portfolio’s current WAL, this revenue-yield shortfall could extend for another 2.5 years. Have no lessons been learned from this latest interest rate cycle?

Since 2008, the fund’s data shows that a portfolio return between 2.5% and 3.0% is more than sufficient to maintain an NOL of 1.3%. Returns above that breakeven range would give credit unions a dividend to recognize their open-ended underwriting commitment. More importantly, it rewards their collective risk management.

The Fund does not need more assets relative to risk, as some board members have stated. It needs more effective management of the portfolio investments it already receives.

The Chairman of the investment committee and two of its four members were at November board table responding to questions. This would have been the perfect time for a dialogue about whether alternative investment options were considered. This one day’s investments in August increased IRR risk, reduced liquidity and returned a lower yield than multiple other options.

Instead of explaining this decision, the board continues to put its head in the sand. It glosses over performance charts that would not get past questioning by the newest examiner should a credit union report this outcome and unexamined policy.

In the meantime, credit unions are on the hook for NCUA’s mismanagement of the fund’s return, not just the industry’s potential insurance risks.

The Lack of Transparency

There are a several calculations used in the final numbers that are vital to understanding their reliability. At times in the past these assumptions and data are shown in detail at briefings. This time only a final number is given so that it is impossible to validate the results presented.

The classic example of a lack of transparency was that until February of 2024, the staff had provided its calculation of the modeling data used for recommending the normal operating level (NOL) for the fund’s coming year. This cap determines when a dividend must be paid from net income. In February however, the board continued the 1.33% with no underlying data or assumptions presented to justify a cap higher than the long time, traditional 1.30%.

That 1.30 was exactly the actual NOL reported for December 2023. The financial model was working exactly as designed, yet the staff and board just rolled over the old higher level with no factual justification. The fund’s own performance belied the need for an NOL above the historic cap.

In the prior two years of staff’s 1.33% NOL recommendation, the underlying data were provided. But when modeled out this information did not support their recommendation. Rather it showed that the historic 1.3% cap would have covered all the forecasted model’s contingencies in the next five years. Is that why no details were given for 2024’s NOL setting?

One board member commented in the Q&A for 2024’s NOL that he did not know what the right number should be. Moreover he didn’t think it would make a difference for credit unions whether the cap was 1.3% of 1.33%. As of September 30, the fund’s equity ratio was .303% and headed higher by year end. Should the December 2024 exceed 1.3% that decision will matter greatly, causing credit unions to forego tens of millions in NCUSIF dividends.

The question is not, what is the right cap on the NOL; rather, it is what is the appropriate range for the fund’s equity so that credit unions can share in the success when all goes well. That judgment is no different from managing a credit union’s capital ratio, a decision and responsibility familiar to every credit union board member and CEO.

Other Missing Details

Another disclosure shortcoming was the investment report. Instead of listing the individual investment purchases as in past reports, “various” maturities and a range of yields (3.8 to 3.85%) were given. This suggests the individual securities were for at least 7 years. This investment choice was at a time when the yield curve offered multiple higher returns on all options with maturities less than three years.

These shorter investments would reduce liquidity risk, improve yield immediately and enhance portfolio flexibility—but no board member questioned these August 15 investment decisions.

Undocumented Projections

The 2024 year end NOL projection by staff was given in a footnote as 1.28% in the last slide. In previous December year end forecasts, the staff has presented a full NOL calculation in a single slide. The data included projected retained earnings, insured share totals and the resulting NOL outcome.

Insured shares grew only .46% in the third quarter. If that growth pattern continues in Q4, then the NOL could be much higher than the 1.303 at September. Why present such an important forecast result (1.28%), which is below the current actual level with no substantiating numbers or assumptions?

Yet no board member commented on this lack of disclosure—and its implications for credit unions.

An Increase in Allowance Account and No Losses

Another critical number is the loss expense which is used to increase, or sometimes lower, the total dollars in the reserve account. For the quarter the additional expanse was $21.7 million raising the total allowance to $232 million or 1.32 basis points of September 2024 insured shares. So far in 2024 the total actual insured losses are near zero.

Th allowance ratio is greater than the NCUSIF’s average annual loss experience since 2008. In the most recent five years there have been no major losses. Yet the reserve continues to grow in both dollars and relative to insured risk.

The formula being used for this reserving should be disclosed. This expense comes right out of retained earnings and thus reduces the NOL number. Just as when presenting an NOL forecast, the underlying assumptions and data should be open for board, public, and credit union scrutiny.

The State of the Board’s Stewardship

As for Otsuka’s call out of the board’s stewardship of the NCUSIF, the examples above are some of the specific opportunities to enhance this responsibility. And we haven’t even gotten to the backward looking calculation of the NOL, but that issue is for another day.

Endnote: Brief History of NCUSIF Redesign

The new NCUSIF financial design in 1984 was based on a study of insurance alternatives and the fund’s initial 15 year trends. The traditional premium approach in the first years of the 1980’s required double premiums assessed by NCUA. But even then, the fund made no headway toward the statutory goal of 1% of insured shares.

There were two major reports of this in-depth reassessment. One was a 100 page study sent to Congress on April 15, 1983 by Chairman Callahan. The report addressed specific congressional questions, provided a history of cooperative stabilization and share insurance funds, and gave recommendations for change. It also included extensive comments from credit union leaders.

When the new design, A Better Way, was established by Congress in 1984 the background analysis for a new model was explained in the video below. It was sent to all credit unions outlining this unique collaborative effort and its benefits for credit unions. For without the credit union support, there would have been no congressional action to authorize this unique cooperative approach to NCUA’s share insurance model.

I missed the November 21 NCUA board’s NCUSIF update so went back and listened to the 30 minute discussion via video. The report was incredibly positive. About both the financial performance of the fund and credit union industry trends.

There were several data “blanks” and areas that were not covered that I will discuss tomorrow.

The slides used to update the NCUSIF can be found here. YTD net is over $226 million which raised the Fund’s total retained earnings to $5.4 billion. This is .3033% of total insured shares ($1.767 trillion) at September 30, thus exceeding the .30% historical NOL cap.

Total insured losses for the year are negative, that is, recoveries of $2.0 million on prior losses have offset current writedowns of just $1.1 million. Nonetheless, NCUA has increased the loss allowance reserve to $232 million, or 1.3 basis points of insured shares in addition to the .3033 in retained earnings.

Since 2014 the NCUSIF has recorded actual net cash losses that exceeded 1 basis point of insured shares in only one year, 2018. That year the Fund wrote down the value of its portfolio of taxi medallion loans. In 2020 it sold this portfolio to a New York distressed asset fund manager (Marblegate) which benefitted from the full recovery in portfolio value as credit unions took all the write downs via the NCUSIF.

The CAMEL Trends

Even the CAMEL trends are positive. Kelly Lay Director of Examination and Supervision was at the table. The % of credit union assets classified as Code 4 & 5 declined from the June quarter. When asked about the change, Lay said it was because of improvements in specific credit union’s liquidity positions-a trend validated in Callahan’s third quarter TrendWatch analysis presented on November 12, 2024, nine days prior to the board meeting.

These two slides from that presentation show these changes in system liquidity:

She further stated that any large credit union that is downgraded in rating or with a 4/5 CAMEL ratings is examined at least annually. When pressed by a board member about potential exposure in commercial real estate loans, she replied that “there was nothing very concerning.”

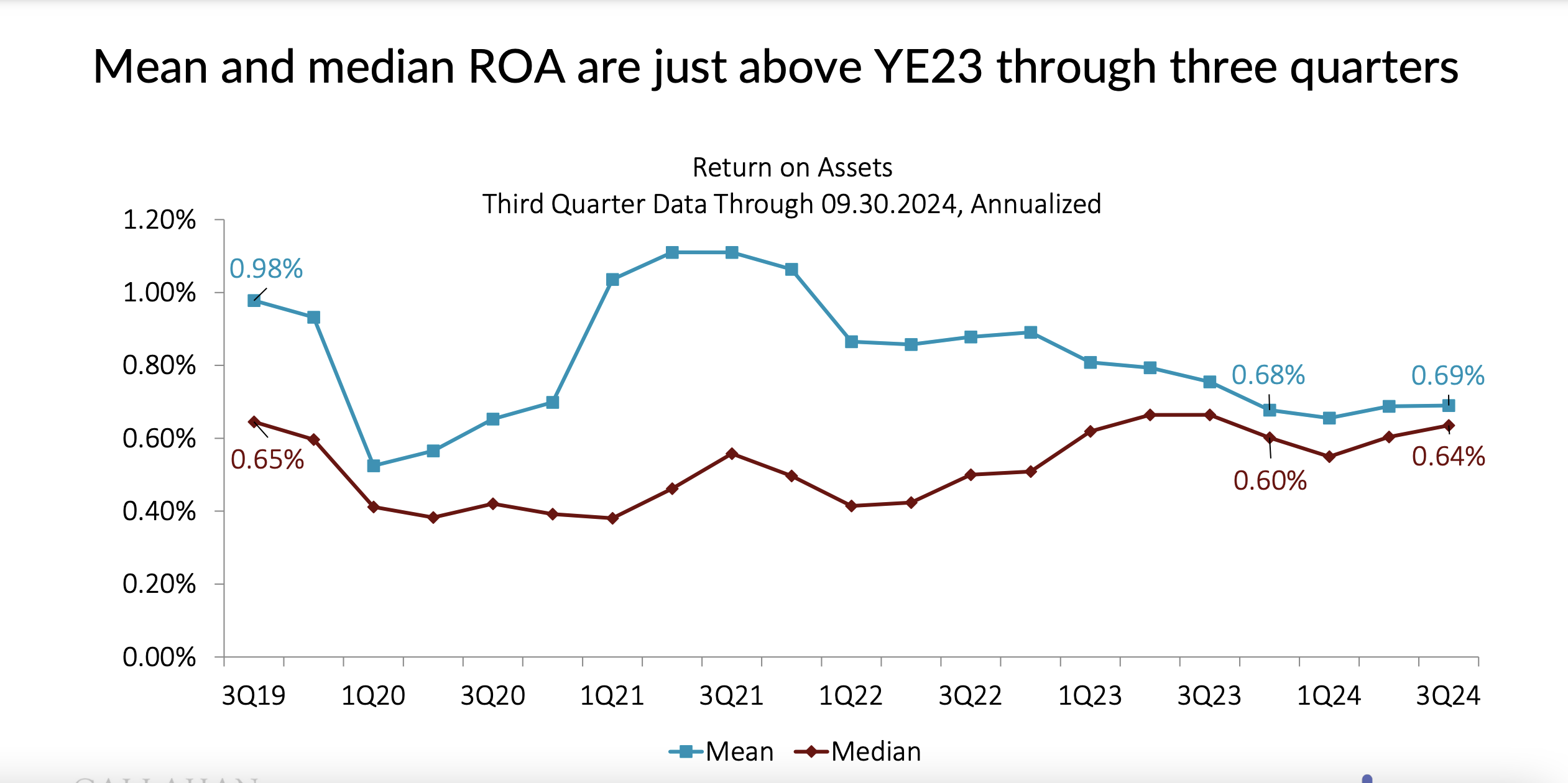

External Third Quarter Data Analysis Positive

Several times board members referred to second quarter data, one citing an increase in delinquency and lower ROA at June 2024.

However both the macro-analysis in Callahan’s 3Q Trend Watch Video and the large, individual credit union performance comparisons by Jim DuPlessis of Credit Union Times all show marked improvement in the third quarter.

Two excellent data analysis by Jim DuPlessis include graphs that do not support this observation from older data:

And if the macro trends in credit unions was not convincing by itself, the final TrendWatch slide showed this perfpr,amce comparison with competitors thru June as later data is not yet released:

Stewards of the NCUSIF

In her opening statement board member Otsuka commented: Being stewards of the National Credit Union Share Insurance Fund is one of NCUA’s primary jobs—a critical component of our duty to protect members’ shares at credit unions. Thus, I continue to be encouraged by the strong performance of the Share Insurance Fund.

Tomorrow I will cover areas where the data was lacking compared to prior updates and the one primary performance topic that the board failed to address.

In future updates, the presentations could be improved if more timely data were used, so the board members have the benefit of the latest information when asking questions or making comments. Or even when testifying before Congressional committees.

Ed Callahan was a leader who made you feel we were part of something big.

from a George Will column: “Musk was ten years old in 1982 when Ronald Reagan appointed entrepreneur Peter Grace to purge government of waste and mismanagement. . .Grace’s commission produced 2,478 recommendations including this: Electricity produced by the Hoover Dam was being sold to parts of three Western states at Depression era rates that were one-fourth to one fourteenth of the rates paid by unsubsidized Americans. Congress responded to Grace’s proposal-stop this-by stampeding to extend for thirty more years this way below market price for a federal resource.”

From Canada-an example of accountability:The Alberta government fired the entire board of its pension manager, saying the $116 billion Aimco increased compensation and staff, but not its returns. (an example for Coop Boards?)

Why CEO’s who offer their credit union in merger to enhance their retirement benefits: “People love unjust gain because money is their highest trust.”

On the challenge for informed public discourse:Reducing complex issues and any public policy into one sentence is not conducive to the civility, magnanimity, and intellectual processes needed for a free society to flourish. Doing so performs a double disservice, in that even while it redirects one from issues to personalities it also kills the search for truth by ignoring the need for real arguments, even ones made with magnanimity. The human mind was created to seek and know the truth. . . Democracy requires compromise, and compromise requires the two virtues lacking most in American society–prudence and humility.

What hope is there, then, now that technology and social media have only deepened the virtue deficit? To paraphrase the great orator, Cicero, who lived at the time of the Roman Republic’s decline into instability, impiety, and autocracy, “silent prudence” is always better than “loquacious folly.”

We may live in an age of succinct folly but the first part of Cicero’s dictum still applies.Silence involves listening, for one cannot argue without first listening to one’s opponent. As the writer of Ecclesiastes reminds us, “The words of the wise are heard in silence, more than the cry of a prince among fools.” Thankfully, Solomon has not yet called and asked for his wisdom back.

The 1980 election of Ronald Reagan brought a spirit of hope and joy for some. For others , deep concern about the future of the federal government’s role.

Recall Reagan’s policy priorities: Supply side economics-tax cuts, defense spending to counter the Soviet Union, tighter money supply, reducing the rate of government spending and deregulation. In August 1981, one of his first dramatic actions was firing 11,345 striking air traffic controllers and banning them from federal service for life after they refused to return to work following a contract dispute. Federal agencies and employees were worried about their future.

The Private Sector Survey on Cost Control (PSSCC), commonly referred to as the Grace Commission, was an investigation requested by President Reagan authorized in Executive Order12369 on June 30, 1982. In doing so President Reagan used the now famous phrase, “Drain the swamp“.[1] The focus was on eliminating waste and inefficiency in the United States federal government. The head of the commission, businessman J. Peter Grace,[2] asked the members of that commission to “Be bold and work like tireless bloodhounds, don’t leave any stone unturned in your search to root out inefficiency.”[3] (Wikipedia)

A year later when the Commission issued its report it called NCUA Board Chairman Edgar Callahan a “role model” for government agency executives. It noted that, “in one year, NCUA cut Agency staff 15% and its budget by 2.5% while maintaining their commitment to preserving the safety and soundness of the credit union industry.” (NCUA1983Annual Report page 3). What was this transformation like?

How NCUA and Credit Unions Fared During Reagan’s First Term

When Reagan took office, inflation for the prior year 1980 was 13.5%. The short-term Fed Funds rate was 13%. Federal Reserve President Volker’s goal was to drive inflation down by raising rates further if necessary.

The NCUA’s new Chairman was Edgar Callahan, whose immediate prior responsibility was over five years as Director of the Department of Financial Institutions in Illinois. DFI supervised over 1,000 state chartered credit unions. At the February 1982 GAC conference, the primary concern for the audience of national attendees was industry survival. Callahan said the response was to put responsibility for fundamental business decisions in the hands of credit union boards and managers, not the regulator. He called this multi-faceted change “deregulation.”

During the next three years NCUA became what the Grace commission described as a model for effective governmental performance.

The following are highlights of how NCUA changed from a November 15, 1984 agency press release titled: FCU Operating Fee Scale Slashed 24%; Third cut in Three Years

The excerpts from this two-page, detailed release describe how this unprecedented reduction was achieved.

The NCUA Board today slashed by 24% the operating fee scale for federal credit unions in 1985, bringing to 64% the fee scale cuts over the past three years.

The dramatic 24% cut will save federal credit unions more than $4.3 million in 1985 and has saved them $14 million since 1983, the first year in NCUA’s history that the fee scale was cut.

“For the third straight year, the efficient operation of the Agency has allowed us to put money into the pockets of federal credit unions, “ said NCUA Chairman Edgar Callahan. “It’s an impressive track record, one that the agency and entire credit union system can be proud of.”

“NCUA is the only federal financial regulatory agency that is assessing its constituents less this year, than it did three years ago and I think that is a tremendous accomplishment,” said NCUA Board Vice Chair P.A. Mack.

Federal credit union operating fees, which are pegged to a sliding scale based on federal credit unions’ assets, are the primary source of funding for the Agency’s operating budget. The fee pays for the Agency’s annual examinations of each federal credit union as well as its chartering, supervisory and administrative activities. NCUA receives no tax dollars. Operating fees, the earnings on the investments of those fees, and insurance premiums are the sole sources of funding for the agency.

(The next six paragraphs show the specific dollar impact on credit unions of different asset sizes including Ft Shafter, Hawaii Federal and State Employees and Navy Federal Credit Unions.)

Continued cost cutting efforts at NCUA, coupled with a projection for robust federal credit union asset growth and increased earnings on NCUA investments are the key elements that made a third consecutive operating fee scale cut possible.

The NCUA board attributed the Agency’s success in keeping costs down to high productivity by NCUA staff, personnel reductions and the shifting of resources from the central offie to the field where they are needed most.

For example, NCUA for the second consecutive year has completed an annual examination of each federal credit union, and achievement not seen since the mid-1970’s. Although total agency employment has been reduced by 15%, the number of examiners has increased to an all-time high (369). Getting back to a once-per-year exam cycle exemplifies the Board’s desire to promote safety and soundness while leaving the management decisions in the hands of each credit union.

The resulting gains in efficiency enabled the Board to reduce the Agency’s fiscal 1984 budget by 4.9%-the biggest cut in the Agency’s history. It was the third straight year the Board approved a total agency budget that was below the previous year’s request.

Federal Credit unions in the six months ended June 30, 1984 had grown 12.5% from $55.5 billion to $61.3 billion.

Taken together, the budget cuts, investment income and credit union growth are expected to leave NCUA’s operating fund with substantially more than it needs to meet its expenses. By slashing 24% from its operating fee schedule, the board is effectively eliminating a $3.4 million surplus. “We believe in returning as much as possible to credit unions,” Chairman Callahan said.

This action is another in a series fiscal and operational improvements the NCUA Board has approved of in the past three years. . . most recently the adoption of rules to revitalize the National Credit Union Share Insurance Fund (NCUSIF) transforming it from the lowest reserved to the strongest of the three federal deposit insurance funds. (End quote)

Some of the Lessons

Chairman Callahan’s leadership at the agency was based on professional competence, experience and pragmatic solutions. Some of his colleagues had worked with him on credit union issues for over five years. Internally Callahan placed responsibility for problem solving with the six regional directors. The agency had become top heavy in D.C. where issues got bogged down between 16 separate offices. He streamlined this structure into two primary responsibilities: an office of administration and the office of programs.

Resources were moved to the field so that an annual exam became the minimum standard for performance. Competence, not seniority or appointment status, were the criteria for responsibility. Mike Riley went from head office to become RD of the largest and most problem challenged region as the youngest RD ever. Rosemary Hardiman was board secretary and Joan Pinkerton, and Sandy Beach led public information and congressional affairs—all were appointees chosen by the previous Chair Larry Connell.

Money was not the most critical resource; it was management talent and willingness to innovate to resolve problems with effective supervision. Staff was provided enhanced training that included Video Network recordings such as Rex Johnson of Lending Solutions, leading sessions with examiners to identify sound and unsound loan underwriting. Another video session was a case study of an actual credit union problem for the agency led by a business school professor.

These efforts were supported by disciplined research, constant dialogue with credit unions and open, frequent communications. New data analytical tools (financial performance reports) from the call report were provided for both examiners and credit unions. NCUA board meetings were taken on the road so credit unions could attend and speak directly with senior staff and board members.

NCUA and credit unions worked collaboratively to transform both the agency-the CLF, the NCUSIF and the exam program-and the credit union system to the new world of open market-based competition. These institutional changes have endured even when subsequent Chairman were chosen from individuals with no coop experience, and several who had just lost a recent election (Senator Jepsen and Congressman Norm D’Amours). The agency staff and administration were comfortable working with the industry even when board members had little or no relevant credit union, regulatory or leadership experience.

Celebrating Success

The high point of this collaborative approach was the largest ever regulator-credit union conference held in December 1984 in Las Vegas, organized by NCUA. All state regulators and examiners and NCUA staff met with over 2,500 credit union attendees to hear from experts and debate the future. I will write more about this seminal event that has never been repeated.

The conference demonstrated the power of cooperatives to share and learn from each other. This was a summit that ushered in over three decades of credit union expansion and resilience as the S&L industry failed and the banking system and FDIC went through multiple bailouts.

The bottom line: as shown by this 1981 transition, new faces can be opportunities for creative leadership and strategic change. The 1981 selection of Ed Callahan as chair enabled NCUA and credit unions to become financial pacesetters for their members and the country. It is the quality of the appointee, not the party, that matters.

One should advocate for a similar considered appointment and proven leadership in this coming transition.

The Institute for Local Self Reliance (ILSR) has turned 50 years old. Its mission is to build local power and fight large corporate control through research, advocacy, and community assistance to advance vibrant, sustainable, and equitable cities and towns.

This 11-minute video below provides its history from founding in 1974 in D.C. to its present multi-faceted efforts. The organization became national in the early 1980’s when it opened its head office in Minneapolis.

In the 90’s It was an outlier in the world of “bigger is better” and the pull of the global economy on large corporate growth ambitions. However, its focus on local self-reliance regained momentum and focus as the power of monopolies became increasingly questioned, especially its impact on local economic communities.

The Institute’s approach is decentralization emphasizing local control and resisting corporate displacement of independent options. The goal is enhancing freedom and democracy with self-reliant economic projects and political control. Today it has four areas of focus: community broadband efforts, composting, energy democracy and promoting independent locally owned businesses.

While the advocacy and research efforts would seem to make the ILSR a natural ally of credit unions, there appears to be no overt participation in this cooperative financial sector.

Why Local Matters

In an era in which many tout scale as the most important competitive necessity, the real sustainable advantage for most credit unions is their “local” character, identity and related service advantages.

At September 2024, the industry’s call report data suggests that over 87% of credit unions offer some form of on online transaction access. The Internet advantage, no matter how sophisticated, is rarely a sustainable or unique delivery channel or even special user experience. However, being local is.

An Example of a Large, Local Advantage

Recently Jim Blaine has posted several articles on the founding of the country’s second largest credit union, State Employees of North Carolina (SECU). The post below details the founding character and common bond of the credit union.

Almost every state in the country had at least one or multiple credit unions with state employees as their core FOM. But only SECU made the breakout to record this growth achievement versus many states with much larger potential in their employee base.

How was this breakout accomplished? As the credit union’s operations expanded to locations and counties throughout the state, the critical advantage was keeping local input, oversight and responsibility at the branch level. Loans were made and collected by each branch; local advisory boards and committees were formed; employees were local; and the various aspects of community involvement were locally determined. Out of this local self-reliance, the second largest credit union in America was constructed.

“No one questions that credit unions were created in the U.S. to provide access to credit for working men and women – particularly those of “modest means”. Why? Because “back then” many payroll offices were confronted with regular, recurring employee requests for “a short-term advance” prior to payday. Money is always in short supply for most folks – both “back then” and now.

“Not helping an excellent employee in a time of need was “bad for business” and employee relations. Sending them to a loan shark was worse. “Payday lending” at rates usually exceeding 100+% – both “back then” and now – creates a death spiral of financial dependency for a consumer. Shackles not made of iron, but shackles just the same.

.

. …” I owe my soul”... that can be a problem, … beware.

“Employers embraced “company credit unions” as an added benefit which could be used to assist and retain employees. Employers liked having an independent, employee-owned and led lender making the decisions on which employees qualified for loans – choices the employer did not want to make. Employers didn’t want to be in the lending business, nor have to “advance” company funds. To help out, employers frequently provided back office support, payroll deduction, office space and assisted employee-member volunteer leadership of the credit union.

“SECU, although a separate, independent organization, was “the company credit union” for North Carolina state government and the North Carolina school systems. The idea of a credit union as an important employee benefit caught on!

“Other N.C. companies also formed credit unions – R.J. Reynolds, AT&T, IBM, Champion Paper for their employees – as did many municipalities, local post offices, our military, and churches. At its peak, there were 360+ different credit unions in North Carolina, today just 60 remain.

“Is SECU still “the company credit union” for North Carolina state workers? What has changed?In order to know where you’re going, it often helps to know where you have been.”

(End Quote)

SECU’s Relevance for Today

Some of the companies and many of the 360 credit unions referenced in Jim’s blog no longer exist. However, the local communities and their residents are still present—even if now in separate lines of work. Local does not go away.

Local does not mean an effort must remain small. No, local wins because it is built on the ultimate credit union advantage of relationships and self-reliance.

A billion dollar credit union’s car loan, savings account or even mortgage are often a commodity, no different from similar products offered by a ten million dollar institution. The difference is personal, being able to talk with a real person who is familiar with your community and circumstance.

The ILSR has continued to present the power of local solutions and control in its newsletter. A recent article was on grocery prices: High prices are a problem. Here’s how to solve it. Perhaps its opportune for credit unions to align and participate with the work of the ILSR. For it appears to capture the ultimate advantage of a member-owned cooperative-its local identity. control and focus.

Trump’s election victory has reawakened concerns about whether the checks and balance essential to America’s democratic institutions will hold.

I believe that credit union’s unique design for member-onwer governance offers a helpful example of the fragility of democratic oversight.

As the chasm between credit union’s original destiny and today’s performance and compliance shortcomings grows, purpose and practice may appear further and further apart in the public’s eyes.

Nowhere is this chasm greater than the failure to encourage member-owner participation in the formal annual meeting elections. Additionally, in daily communications rare are appeals to the special role of being owners versus messages common in all financial customer appeals.

Here are two recent observations on the delicate nature of democratic processes. And why credit union’s example might influence our perception of how political democracy functions.

America-An Experiment

A personal story. When I was in grammar school, our history book was titled, “The United States of America, An Experiment in Democracy.”

I froze. I got goose bumps. I was 8 years old. An experiment? I knew enough that some experiments worked, and others didn’t.

It felt like the bottom fell out. All sense of permanence left.

That day was life-changing. I have never seen this country the same since. (source: unknown)

The Transfer of Power

“The genius of democracy is its self-correcting nature. But the problem, of course, is if the person (or persons) being elected into office is (are) the kind of threat that intends to disrupt this happy self-correcting logic of democracy.” ( Daniel Ziblatt, co-author of How Democracies Die)

How do these observations about national political concerns apply to credit union’s democratic model?

Richard Rohr comments: We quickly and humbly learn this lesson in contemplation: How we do anything is probably how we do everything.

Writing about the future is easy. Rarely do readers look back when events have unfolded. Moreover such forecasts often reflect, not insight or wisdom, but rather one’s own efforts to protect vested interests.

However there are some reference points which can help us think about what a credit union might do going forward into a possible disrupted regulatory future.

Today I will review what Project 2025 says about federal regulation. I could find no direct reference to credit unions although I did not review all 900 pages.

Published in 2023, President-elect Trump has denied association with the ideas presented in the document. More than 100 conservative organizations were involved in its creation. I found the brief section I cite below had over four pages of extensive reference notes.

From page 705:One of the priorities of the incoming Administration should be to restructure the outdated and cumbersome financial regulatory system in order to promote financial innovation, improve regulator efficiency, reduce regulatory costs, close regulatory gaps, eliminate regulatory arbitrage, provide clear statutory authority, consolidate regulatory agencies or reduce the size of government, and increase transparency.

Merging Functions. The new Administration should establish a more streamlined bank and supervision by supporting legislation to merge the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, the National Credit Union Administration, and the Federal Reserve’s non-monetary supervisory and regulatory functions.

U.S. banking law remains stuck in the 1930s regarding which functions financial companies should perform. It was never a good idea either to restrict banks to taking deposits and making loans or to prevent investment banks from taking deposits. Doing so makes markets less stable. All financial intermediaries function by pooling the financial resources of those who want to save and funneling them to others that are willing and able to pay for additional funds. This underlying principle should guide U.S. financial laws.

Policymakers should create new charters for financial firms that eliminate activity restrictions and reduce regulations in return for straightforward higher equity or risk-retention standards. Ultimately, these charters would replace government regulation with competition and market discipline, thereby lowering the risk of future financial crises and improving the ability of individuals to create wealth.

From page 706: Direct government ownership has worsened the risks that government-sponsored enterprises (GSEs) pose to the mortgage market, and stock sales and other reforms should be pursued. Treasury should take the lead in the next President’s legislative vision guided by the following principles:

Fannie Mae and Freddie Mac (both GSEs) must he wound down in an orderly manner.

The Common Securitization Platform57 should be privatized and broadly available.

Barriers to private investment must be removed to pave the way for a robust private market.

The missions of the Federal Housing Administration and the Government National Mortgage Association (“Ginnie Mae“) must he right-sized to serve a defined mission.

(End Quote)

The text also states that Congress should repeal titles of the Dodd-Frank Act that created the Financial Stability Oversight Council (FSOC), a federal government organization which identifies risks, promotes market discipline and responds to emerging threats. Project 2025 defines the FSOC as a “super-regulator tasked with identifying so-called systemically important financial institutions and singling them out for especially stringent regulation.”

A Learning Event: The S&L Dissolution

In the late 1970’s the S&L industry held the largest deposit market share in California, much larger than banking competitors. This was before deregulation. Most depository firms were limited to operating in a single state or in some cases, a single location (Illinois).

Today S&L’s no longer exist as a separate industry even though 555 savings institutions with $1.2 trillion in assets still operated at June 2024. All deposits are FDIC insured. Of the total institutions, 241 are supervised by the OCC, 276 by the FDIC and 37 by the Federal Reserve. While state and federal chartered institutions still function, the system is under federal direction.

While there are many reasons for the loss of the S&L’s as a separate, independent financial segment, the dominant factor was that many of the causes were self-inflicted. These included a loss of special purpose, rapid multistate expansion through acquisitions, and balance sheets weighed down with fixed rate mortgages in a deregulated deposit funding environment after 1981.

After the mid 1990’s, there was no separate FSLIC insurance fund, no Federal Home Loan Bank Board to oversee the industry, and the FHLB liquidity system survived by serving all real estate lenders including credit unions. In most states the mutual charter exists as an anachronism, with no new charters being issued. At the state level supervision is provided by a single banking/financial institutions department.

While external financial events did contribute to the industry’s collapse, competitors did survive and thrive, especially credit unions. At the February 1982 GAC in D.C., CUNA President Jim Williams told new NCUA Chairman Callahan there was only one topic on credit union’s minds: survival.

Together credit unions and NCUA embraced deregulation and the changes in structure and oversight the new environment would require. Hunkering down , protecting existing ways and asking for more funding to address problems was not the approach.

Whether the new administration will be as disruptive of federal regulators as indicated in campaign rhetoric, remains to be seen. The lessons from an earlier era can be helpful: remember who you are and build on what brought success to this point in time.

Many of the factors in the S&L demise were self-initiated with leadership failures. Cooperative success in navigating external changes was accomplished though enhanced collaborative efforts between credit unions and their regulators. not each trying to go their own separate ways.