Most individuals and organizations realize at some point in their journeys, that money does not guarantee success. Nor happiness.

Thursday’s NCUA Board is, at first glance, all about money. Tens of millions. And how it is to be raised, allocated and spent.

Since all NCUA’s funds are from credit union members, it behooves we all pay attention. For NCUA has no other revenue. It is the steward of almost $400 million in annual costs paid by members.

The Board’s financial decisions on Thursday include:

- The size of NCUA’s annual and capital budget spending;

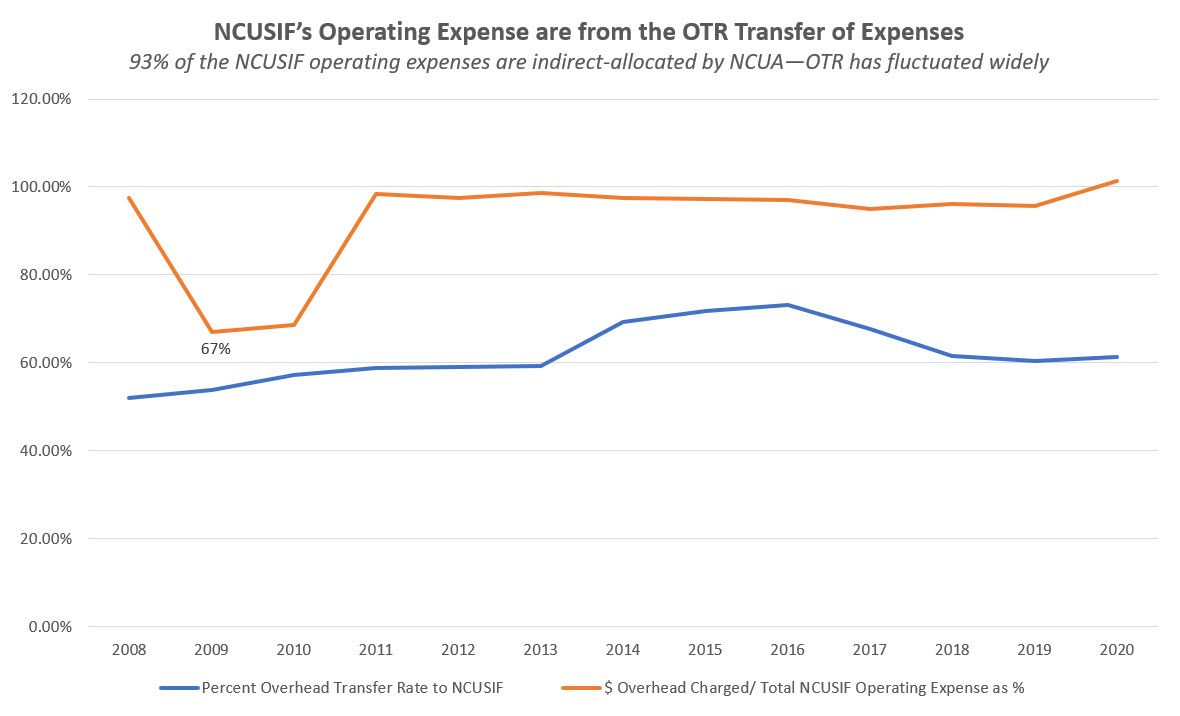

- How these costs are allocated (OTR) between the CLF, NCUSIF and Operating Fee;

- The limit, or cap, on the maximum relative size of the NCUSIF via the NOL, after which a dividend must be paid;

- The disposition of the approximately $100 million in surplus retained in the Operating Fund from excess FCU annual fees collected over recent years.

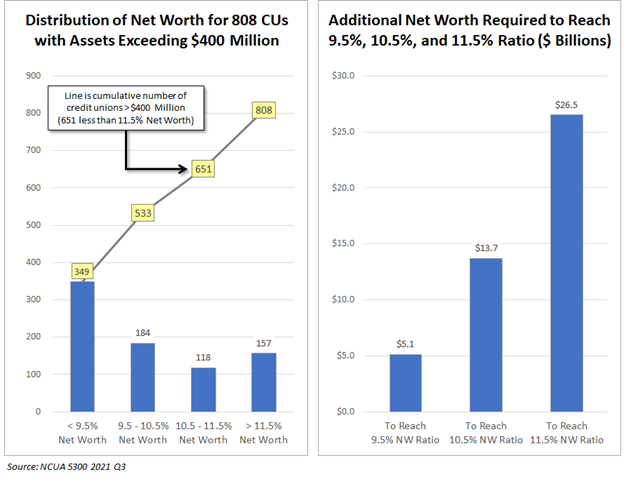

- Even the proposed CCULR/RBC rule is about money, not just burden. It would require credit unions to retain from revenue initially as much as $26 billion more in reserves that would otherwise be available for greater member value and service.

All About Money, or Is It?

The justifications for the amounts NCUA is seeking, is that the regulator’s financial resources are what sustains a safe and sound movement. More financial resources enables more effective supervision.

This leadership approach is a fallacy. It is often used to explain NCUA’s and even many credit union decisions. Institutional strength or capability is measured by asset size, by net worth ratio or for NCUA, the annual spend or dollars on hand.

Resilience Not Resources

However, over and over again especially this year, events have shown that resilience is a leadership characteristic, not the amount of resource an organization controls. Credit unions with double digit net worth, managing hundreds of millions, even billions, are routinely merging saying they lack the resources to cope with future challenges. That is a leadership failing, not a resource gap.

Every credit union in existence today was started with no financial capital. They survived, prospered, and thrived because of volunteer sweat equity, sponsor support, member self-help and shared belief in their purpose. In other words, leadership.

These critical intrinsic motivations are being replaced with an assumption that more and more dollars are the key to survival. The thought that resilience depends on more dollars cuts against the grain of what a coop financial system is and can be.

This reasoning is used by some CEO’s who end their tenure with mergers accompanied with large added retirement or financial bonuses. Greed not gratitude becomes the hallmark career-end.

Who Will Credit Unions Become?

How the Board decides the issues before it tomorrow will send a clear message who they believe credit unions are today and what they will become in the future. Will it be about more money for NCUA or an effort to inspire credit unions through careful stewardship of their resources and decisions based on objective data?

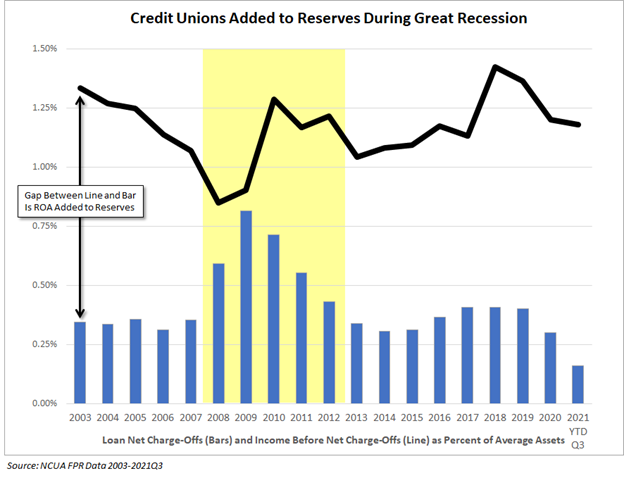

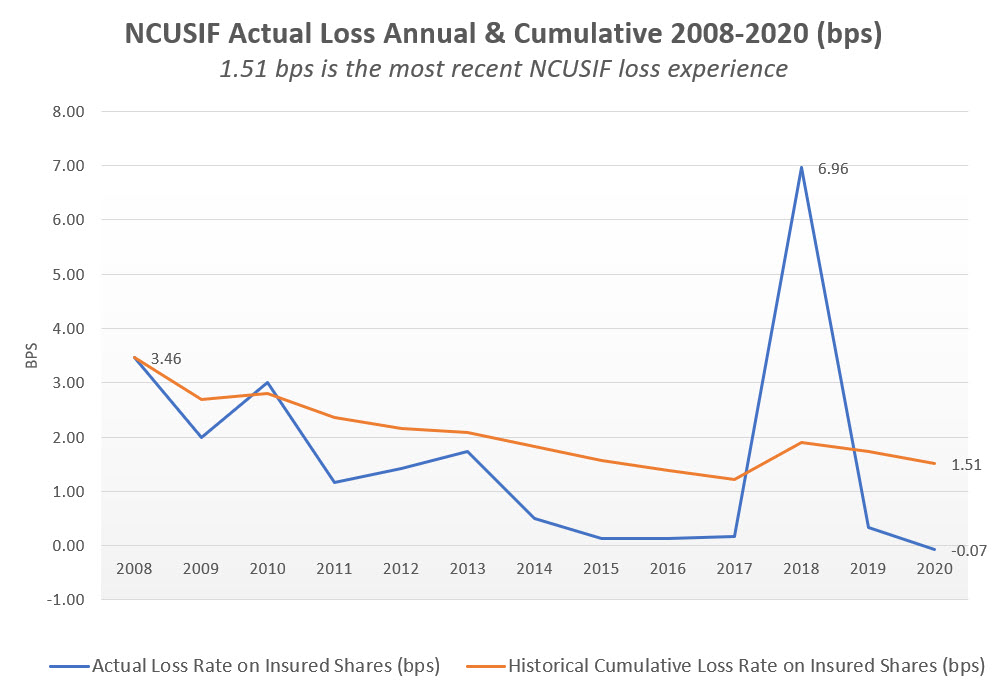

During the past two years of the pandemic credit unions have shown their best side. Waving fees, making loan adjustments, lowering charges, and being with members or in person no matter the severity of the epidemic. The growth in member savings and bottom lines have resulted in back-to-back record setting outcomes and zero NCUSIF insurance losses.

Daily credit unions are announcing bonus dividends to members to share their success in the millions.

The board’s decisions on resources will communicate their view of whether credit unions are special kind of financial service provider that warrants further inspiration, or just a minor-league version of banking.

Will the board present made up worries and projects lacking outcomes to support funding? Will it succumb to temptation to offer unknowable future risks to retain unneeded reserves? Will it affirm the idea that every credit union must stand on its own bottom—no system safety nets or mutual support in the event of problems?

All for One and One for All?

Credit union’s manage people’s money to promote other member’s financial opportunity. The well-being of one is linked to the well-being of all. The same approach has, in the past, applied to credit union’s intra-dependent cooperative system design.

The result is credit unions are much stronger than individual numbers alone would ever indicate. The member relationships, based on a premise that this financial community will help ones neighbors, creates goodwill and loyalty creating value that far exceeds financial ratios.

Credit unions are a classic example of American innovation with leaders that have attracted tens of millions of adherents or fans, called members. It is self-help, self-financed and self- governed, formed from the grass roots and built on community respect.

A Contradictory Stance On Credit Union’s Role

The NCUA board has represented a different portrait of the system. In the past decade, NCUA’s priorities suggest credit union’s meaning and value is measured primarily by how many dollars are on the balance sheet and in net worth.

The whole theme is to get more. There is no underlying recognition about the practical life of the members or their credit union’s role. Such a world view cannot inspire the movement let alone feed the soul of members.

NCUA’s increasingly dystopian views augmented by faulty analysis and misleading numbers blinds them to see what they can’t see. NCUA no longer see credit unions as they are, because NCUA see things as they are. They no longer seek information that would change their approach; rather they look for a story that confirms what they already have in mind.

NCUA’s decisions rest on a simple falsehood that more is necessary rather than a more complex reality. Resilience and credit union success is not built on financial performance, but by leaders imbued with purpose and community well-being.

Inverting Common Sense

Even worse is the proposed RBC/CCULR rule. It inverts the legal maxim that bad cases make bad law. In NCUA’s view a bad loss requires an ever more complex rule.

When NCUA approves a generally applicable rule like RBC to counter an extreme outcome or circumstance, the risk is that all credit unions’ freedoms are now restricted by the behavior of a very few.

The burden of the RBC/CCULR rule will fall directly on the membership, in the initial proposal by at least $26 billion.

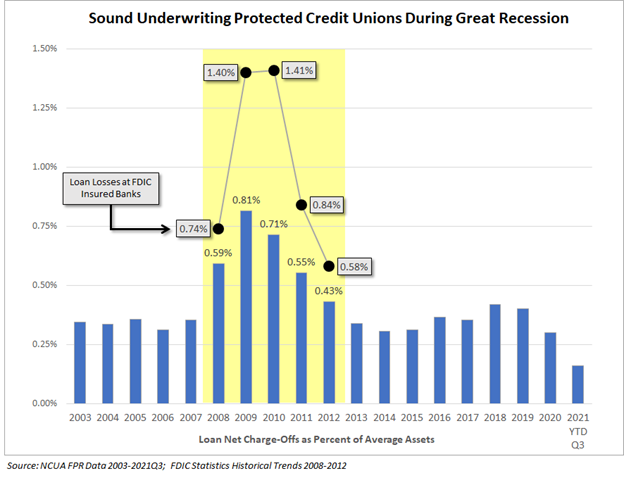

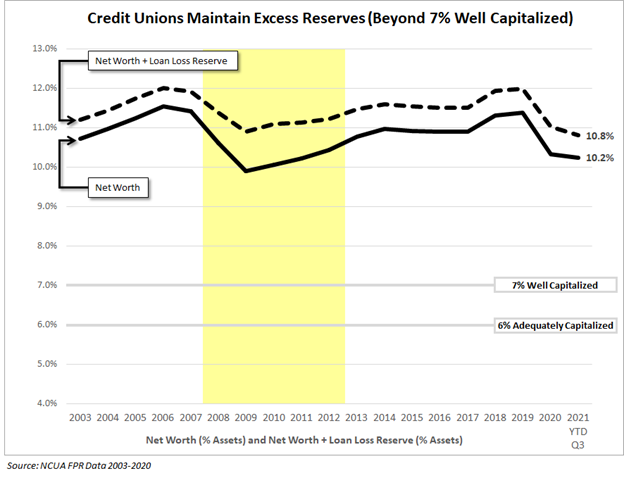

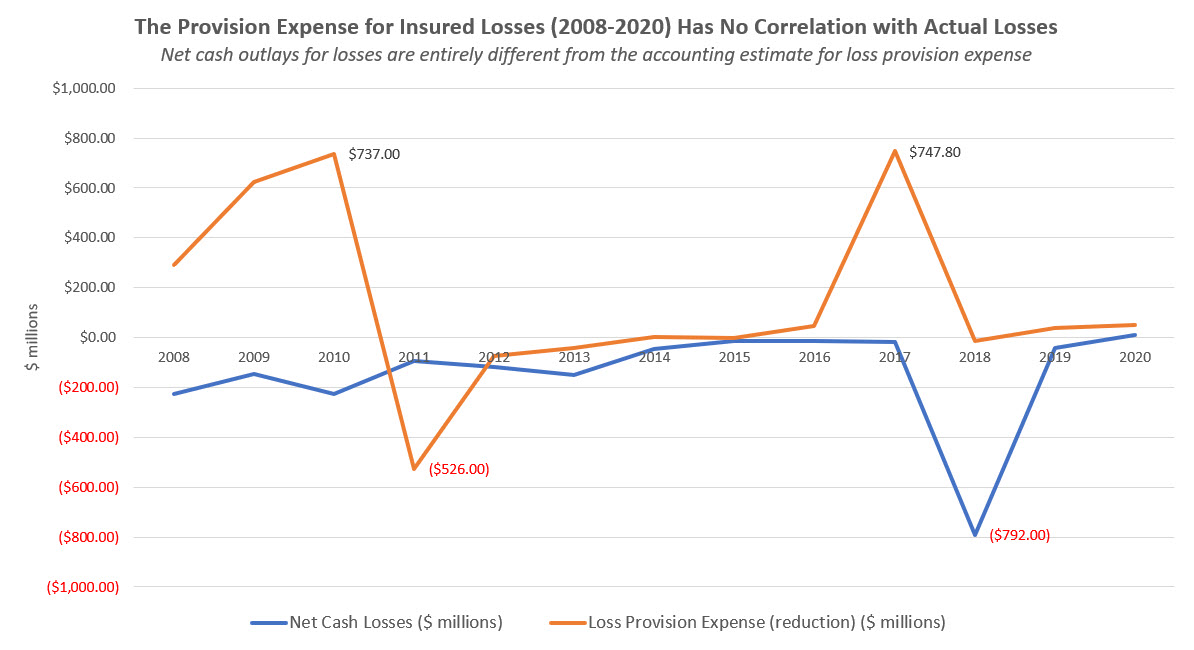

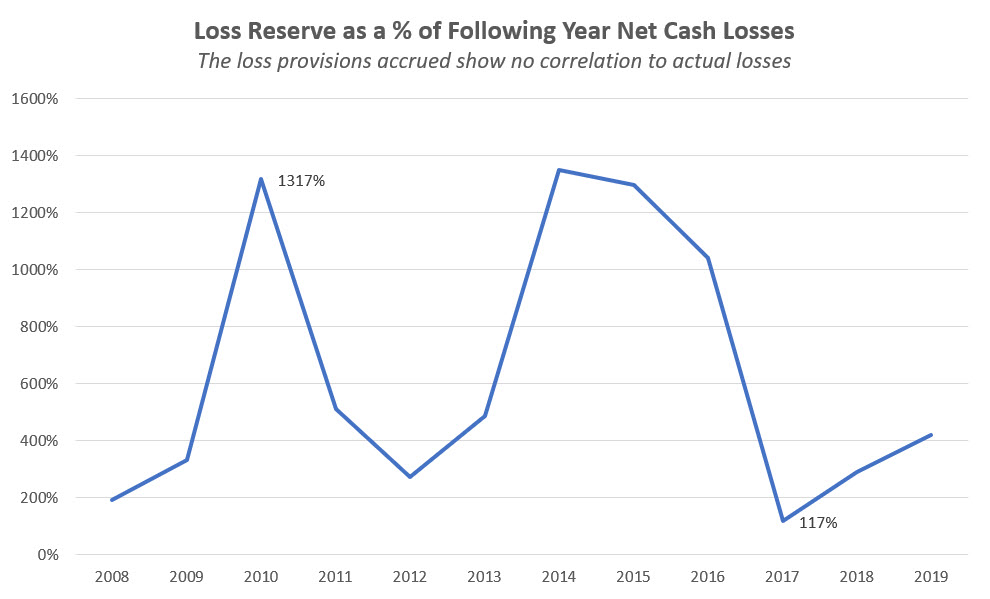

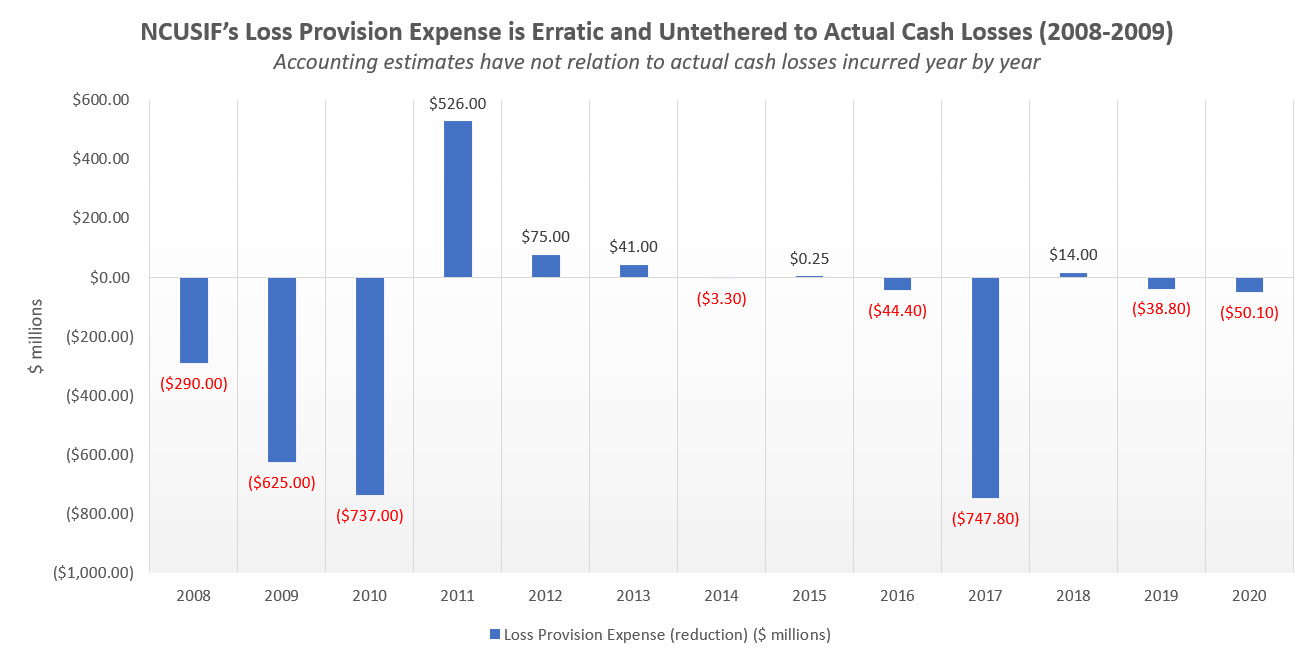

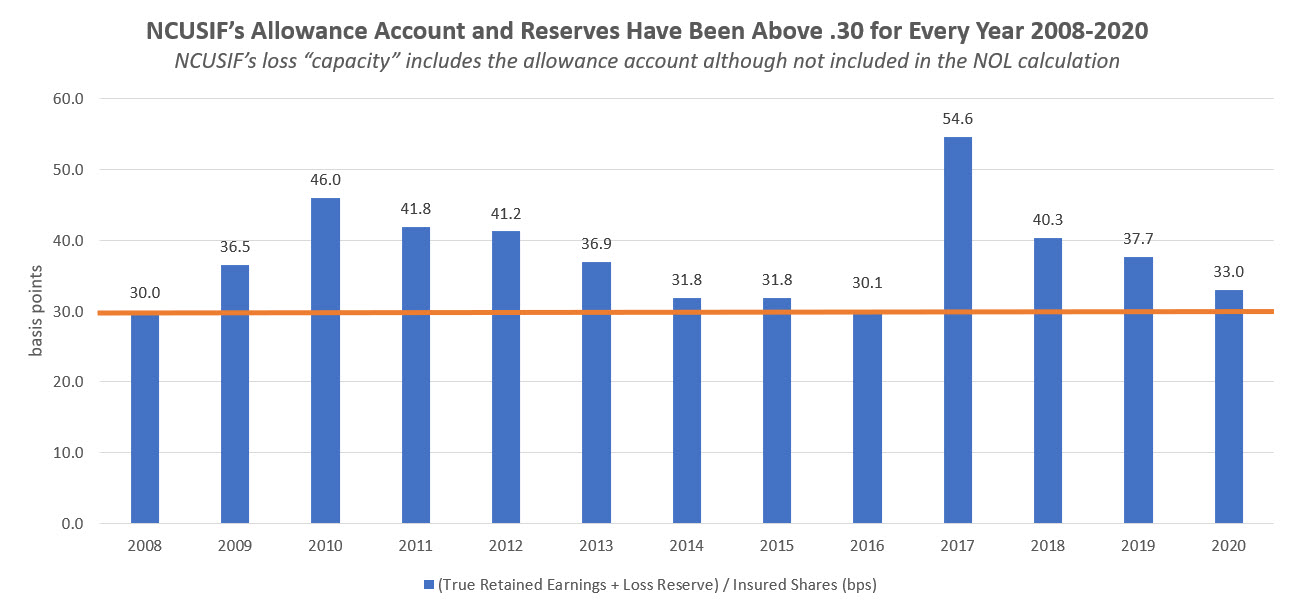

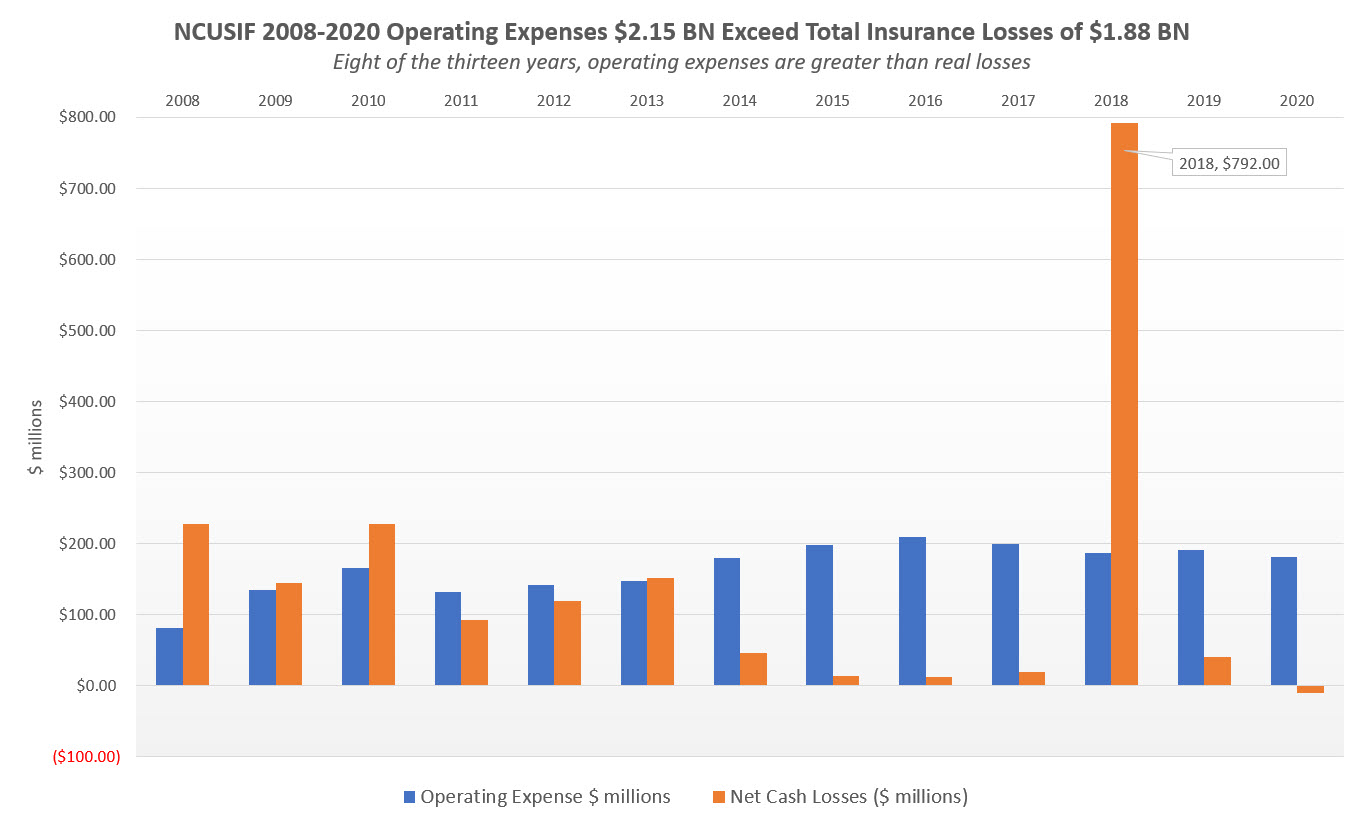

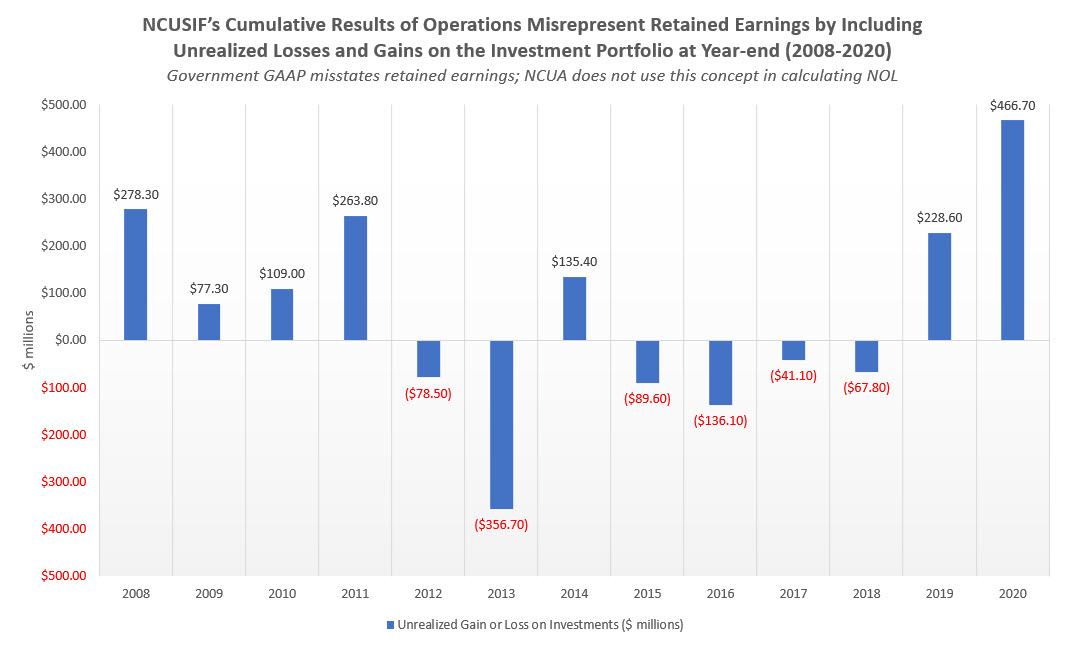

Will the NCUA board respond to the incredible credit union performance during the pandemic for members. Will it say, “Job well done?” Or now is our time to get more funds? Will they respect and recognize the documented track record of the industry since 2008 (reported yesterday) or will they continue to present misleading analysis and mythical future outlooks?

Whatever the outcome, it will set the tone and direction for years to come. It is unlikely there will be a better time or circumstance for the NCUA board to affirm its faith in the credit union system, the performance of cu leadership during COVID, and to restrain the never ending instinct to acquire more resources.