The cooperatively created NCUSIF is an insurance resource designed for all economic seasons. Whether there are clear financial skies, clouds or even once-in-a-hundred years storm (e.g. the COVID economic shutdown in the 2nd quarter 2020) the structure is flexible, transparent and proven.

Most importantly, its current performance is easy to monitor, by anyone. It does not require a PhD in economics, 20 years of regulatory experience or even the expertise of a Black Rock.

There are only four moving parts. There are 36 years of actual data to call upon. Each component has historical and contemporary data to employ in the model.

The model’s four variables are:

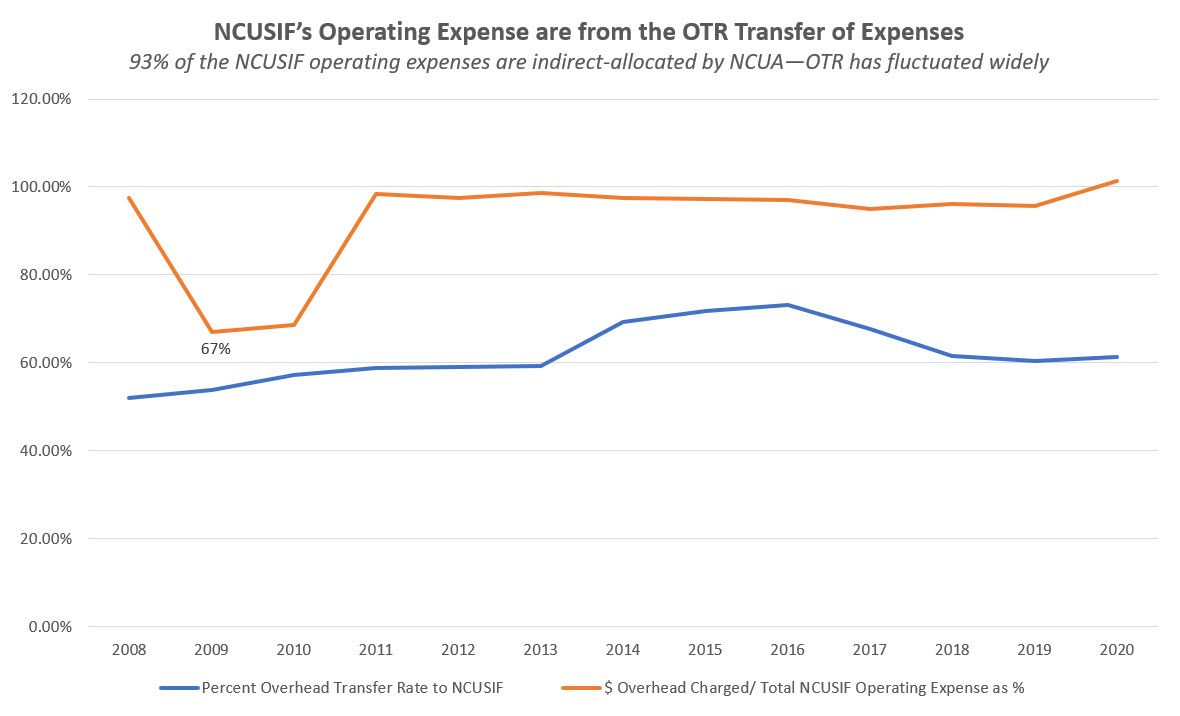

- The operating expenses taken off the top from NCUSIF income through NCUA’s OTR process;

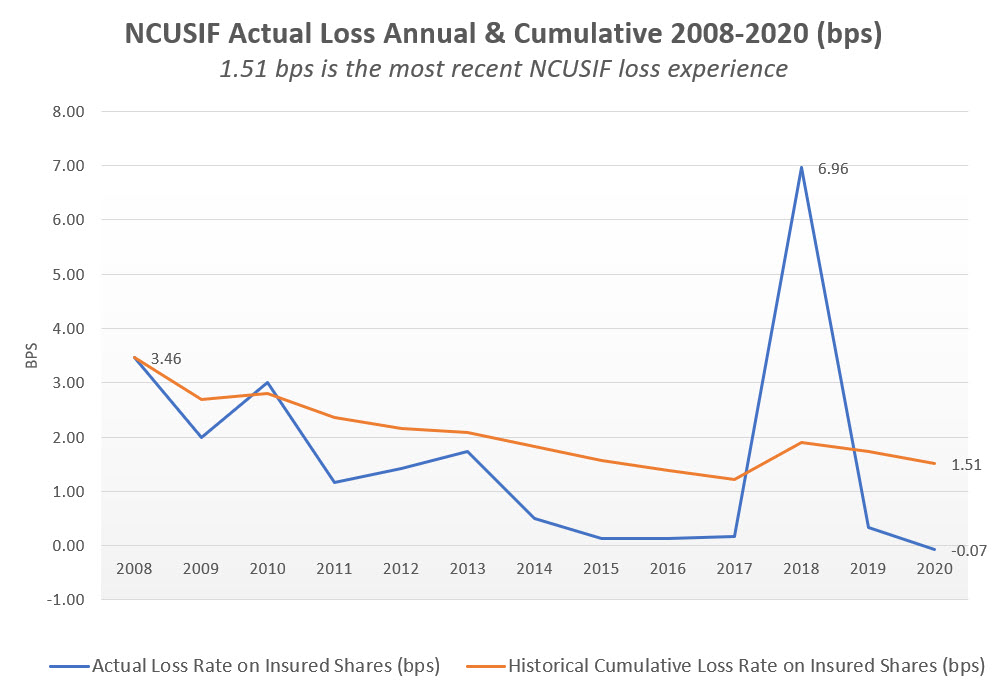

- Insured losses–there is data for all economic cycles. In the past 13 years and two crises, the cumulative rate is loss rate is 1.51 basis point for each $1 of insured savings.

- The yield on NCUSIF’s portfolio reflects the staff’s investment decisions, and is semi-fixed in the short term due to its current weighted average life of over three years.

- Credit union insured share growth. It is reported quarterly. The most recent 13 year CAGR is 7% even including 2020’s unusual rate of 22%.

The Model Demonstrates A Better Way

In 1984 credit unions and NCUA worked together to create a cooperative fund that would be A Better Way than the failing premium-based systems. This dynamic model shows how this financial design works and more importantly how it can be even better managed today.

The model has two key capabilities. It dynamically links the four financial variables so that any input change automatically recomputes all outcomes.

Second it translates the variable input measures into understandable, actionable data. Converting historical insured loss experience (bps), rates of share growth and investment yields(%), and operating expense ($) into one integrated financial design ensures the model always aligns with the size of insured risk. For example 1 basis point loss in 2010 is $76 million; however in 2020, that same loss rate is $144.5 million due to the growth of insured shares. The model’s output is provided in all three measures: $, % yields, and basis points to easily understand the options for the yearend NOL.

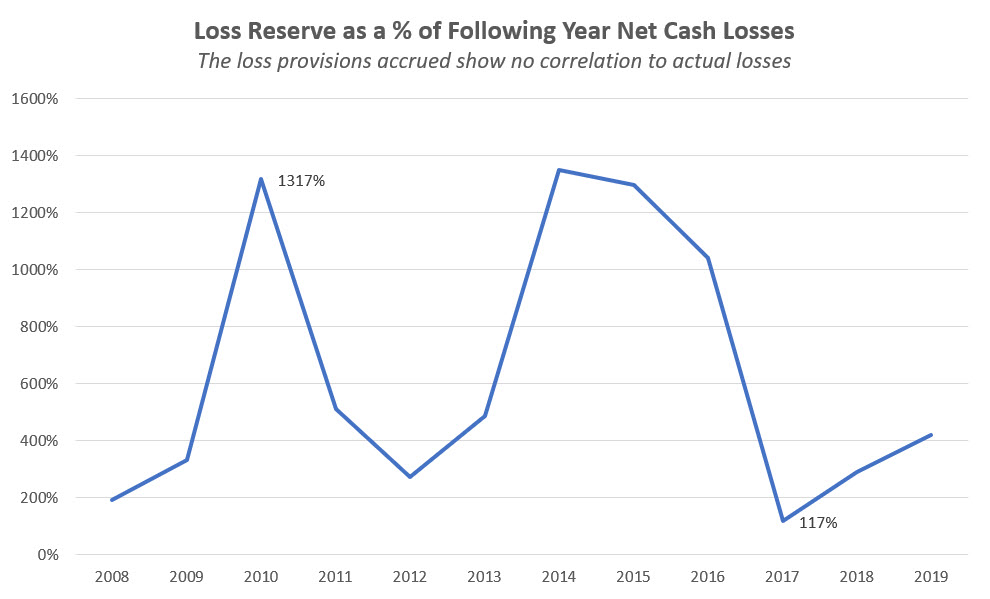

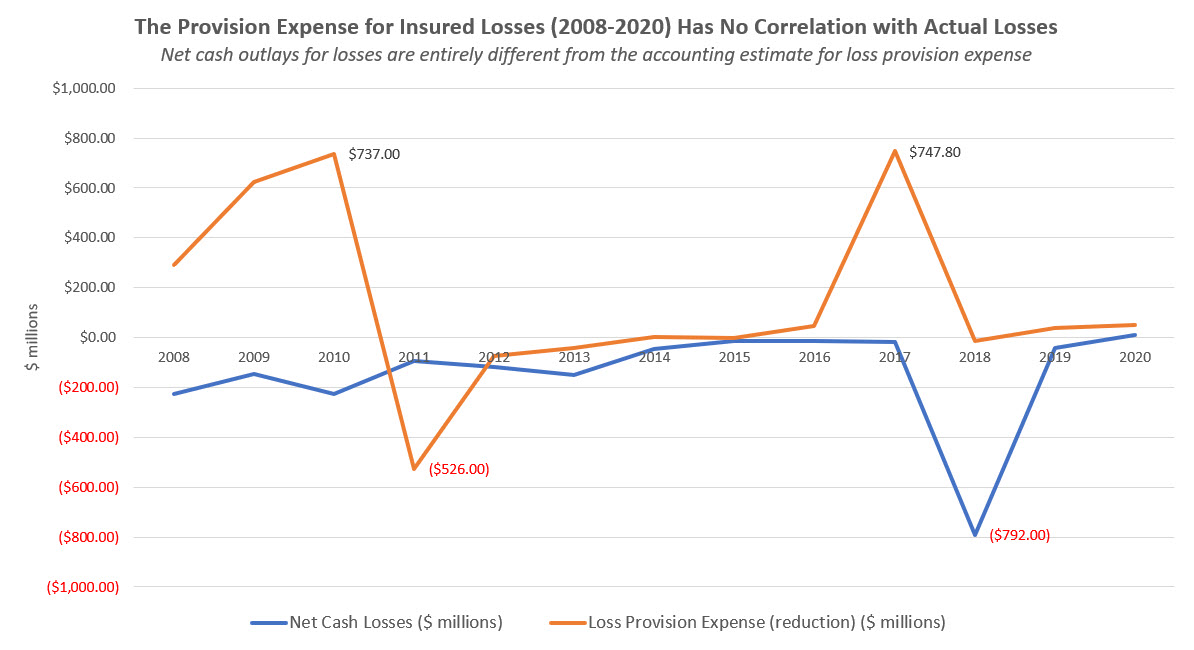

Events have demonstrated that NCUA’s NCUSIF models used in 2017 through today are not based on any objective reality. The so called scenarios are financial myths developed to support NCUA’s desire to remove the guardrails on the most successful deposit fund ever managed by the federal government.

The Dynamic Spread Sheet

This is the link to view the xcel calculator with the numbers used below. To enter your own numbers, feel free to make a copy (open this view-only copy with google sheets, click File, then Make a Copy). Using your copy will automatically calculate the yearend outcome with your inputs.

Models are not answer machines. They inform judgments. They require objective validation. When used properly, they identify options and improve management effectiveness. The following is the example shown in the “view-only” model link above.

An Example With Actual Data

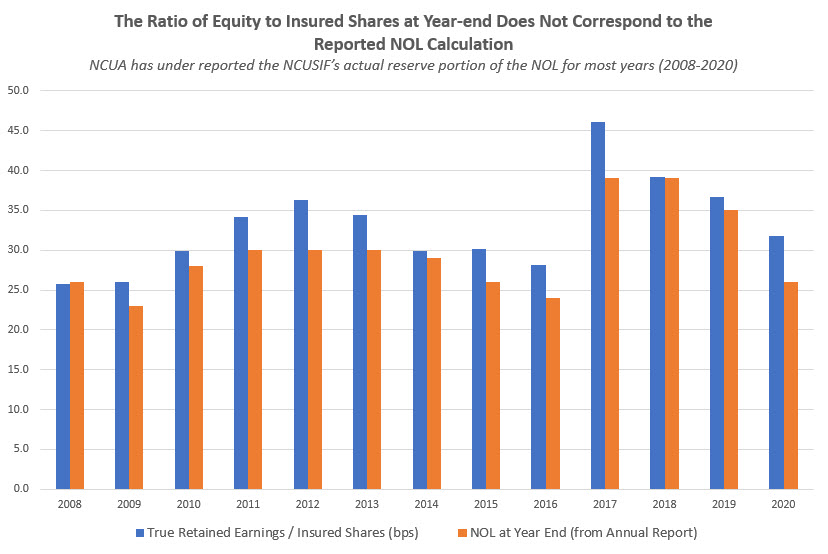

The audited yearend NCUSIF data from December 31, 2020 is entered in the view-only example. This includes the audited reserves ($4.7 Bn), insured shares ($1.467 Tr), the reserve ratio (.318) and a 2021 yearend goal for this ratio (.30). With the 1% credit union deposit, the spread sheet calculates the performance required to reach a 1.3 NOL at 2021 yearend.

The columns E, F, G and H are four variables that can be updated anytime. I have entered both current numbers and informed estimates. For share growth I used the first quarter’s annual rate of 23%; for loan loss I entered .5 of a basis point which is below the long term 1.51 rate because to date, the NCUSIF has reported net recoveries.

For total investments I have added the increase in 1% deposits from the year end true up and a mid-year estimate. However, the portfolio’s size is not increased 100%, reflecting that these additional deposits will only earn for 9 and 3 months, respectively. The $190 million expense total is higher than 2020’s expense and uses the 2021 budget modified by actual results through May. Finally, for the yield, I entered NCUSIF’s current year-to-date portfolio return, 1.27%.

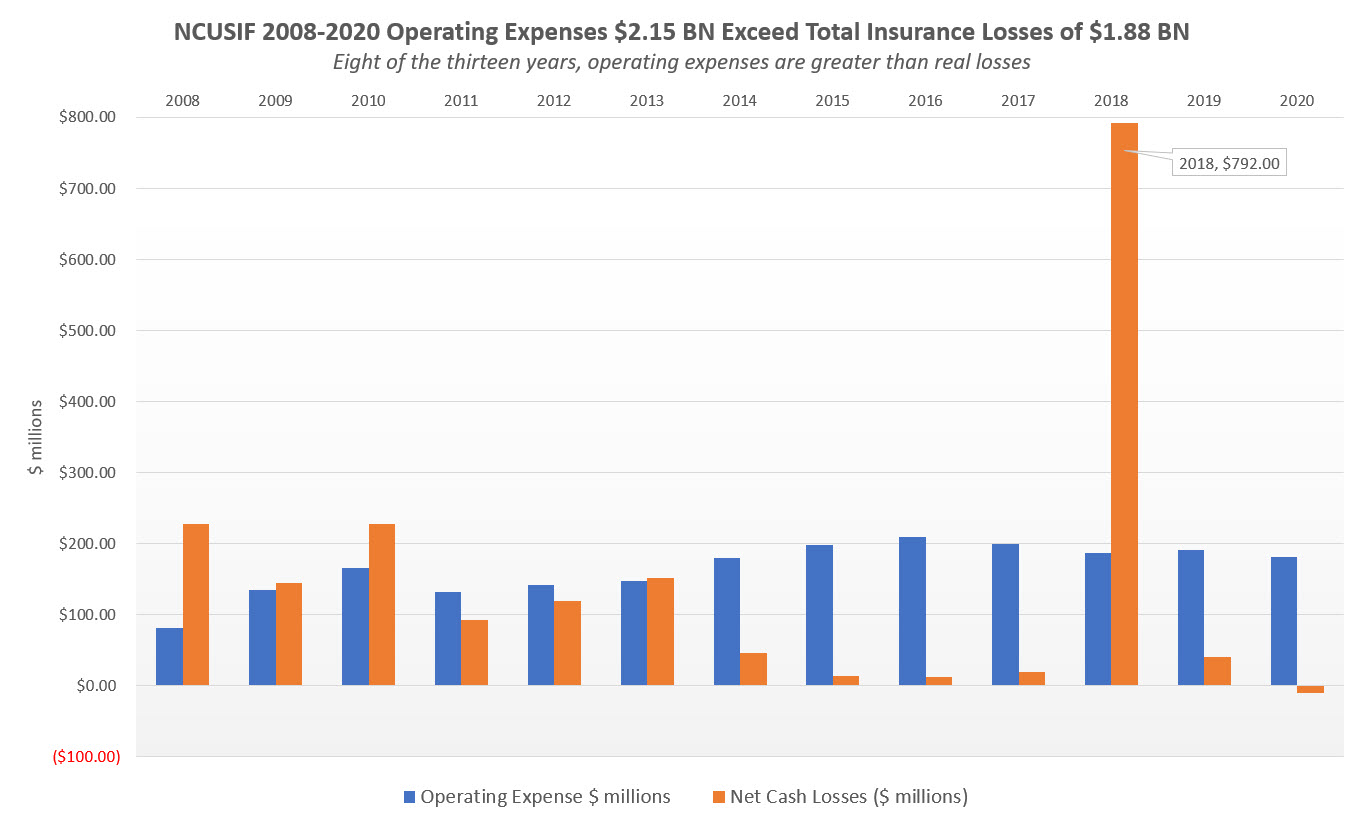

The five green columns show the projected yearend outcome from these inputs. The required portfolio yield is 5.28%, way above the current yield. This shows a yearend NOL of 1.257. To raise that outcome to the target 1.30 level would require a maximum premium of 4.33 basis points of 2021 yearend insured shares or $782 million—if nothing changes in these input assumptions.

That certainly seems a dour result in this relatively stable and growing economic climate. It does not necessarily require a premium. At numerous points in the past when the NOL ended below the 1.3% cap, NCUA has foregone a premium at yearend, most recently in 2016 ending with a 1.24 NOL.

A Different, More Probable 2021 Scenario

However, this forecast and assumptions are an unlikely outcome. Extraordinary share growth is driving this result. The rate is already slowing. June and September call reports will provide a more relevant number.

For example, if insured shares grow at the 13-year average of 7%, then the results are totally different. The required portfolio yield would be just 1.6%, and the year-end NOL, without any premium, is 1.296, almost at the 1.30 cap. Further, if there were no insurance losses (zero loss provision), and only continued recoveries, the yearend ratio would be 1.308, above the NOL target.

It’s Not Rocket Science

Credit union CEO’s and boards are living daily the operational experiences underlying these inputs. They know industry growth trends, delinquencies and certainly have a feel for interest rates. Their input assumptions can be informed by their real world understanding, not guesses about the future.

This simple model should empower every credit union to evaluate the information and NCUSIF projections used by NCUA. Responses should be formed from their expertise and data, not unsupported opinion.

But more importantly, anyone who uses it will understand the flexibility and viability of the NCUSIF’s cooperative design.

Every year the NCUSIF automatically grows at 80% of the share growth rate via the 1% deposit true-up (1/1.25).

If insurance losses, share growth or yields fall outside the long-term credit union system’s experience, then a premium is an option to maintain a targeted reserve ranging from .2 to .3. There were many adjustments to the NCUSIF equity during the 2008-2020 period. However, the two premiums in 2009 and 2010 averaged only 1.3 bps annually over these 13 years.

The Yield Calculator as a Management Tool

Another value of the NCUSIF model is using the Yield Calculator and the recent 13-year averages to calculate the breakeven yield on investments needed to maintain an NOL target, say 1.25, or within a narrow range. One must first convert the operating variables to basis points. Adding the 7% insured share growth rate(1.75 basis points) plus 1.51 basis point loss experience, and the 1.6 bps of operating expenses totals 4.86 basis points. Dividing this total by the portfolio size of 1.25 (the midpoint of the NOL) shows the “breakeven” investment yield needed to support this NOL is 3.9%.

The model clearly highlights the relative importance of each of the four variables.

Operating expenses come off the top of revenue. If the OTR had remained aligned with the proportion of state charters, or 50%, the operating expense share would have been 1.41 (not 1.6) basis points, thus lowering the required breakeven yield.

If share growth were 22%, not the long-term average of 7%, the bps for this variable would increase to 5.5 and the required yield jumps to 6.9%.

Managing the NCUSIF’s Portfolio

The model demonstrates the importance of monitoring the decisions about NCUSIF’s investment portfolio. If the current yield 1.27% and 4.86 basis point of inputs were frozen forever, credit unions might have to pay an annual premium of 3 basis points (1.27%-3.9% equals yield shortfall of 2.63%/.8/1.07 = bps premium on the new year end 1% insured share base) to maintain the NOL at a 1.25 breakeven level.

Informed oversight of the NCUSIF’s portfolio decisions is a vital responsibility of NCUA management and board. Market rates change. In the interest rate trough of this economic cycle, should NCUA be making 8-year fixed term investments for a 1.26% yield (April 2021) when knowing the breakeven goal for NCUSIF is 3% to 4%?

On November 18, 2018, the yield on the two-year treasury bill was 2.98%. Today the yield is .26%. If NCUA’s investment managers are supporting the NCUSIF’s financial model, should they be routinely filling out an investment ladder up to 8 years in this part of the economic cycle? Common sense says no—this will reduce NCUSIF’s income, shortchanging credit unions years into the future.

The economy is at an historical low point in this interest rate cycle. The dominant economic topic today is the inflation outlook. Are price increases here to stay or a transitory event? Whatever the outcome, realistic judgment suggests that rates will be higher 6-12 months from now–the only question is how much higher. An example of this change prospect from the past ten years is that the peak in the 5-year treasury yield was 3.07% on October 1, 2018, just two and a half years ago.

Tools Are Only as Good as the User’s Skills

Every credit union uses spread sheets. This model is a simple, automatic xcel tool-just add your own judgment. All the variables are in the formulas. Some inputs are set; others easy to project.

Interpreting the outcome(s) is the art. Bias will sometimes cloud these judgments. That is why it is vital that commentators on NCUA’s request for NOL comments document opinions with factual underpinnings and an understanding of how special this coop fund is.

Good luck with the model; critiques/questions are welcome. Tomorrow I will suggest points to make by credit unions responding to this NCUA’s NOL request.